Corrosion and Scale Inhibitors Drive Industrial Water Treatment Growth: Market Value Analysis and Forecast

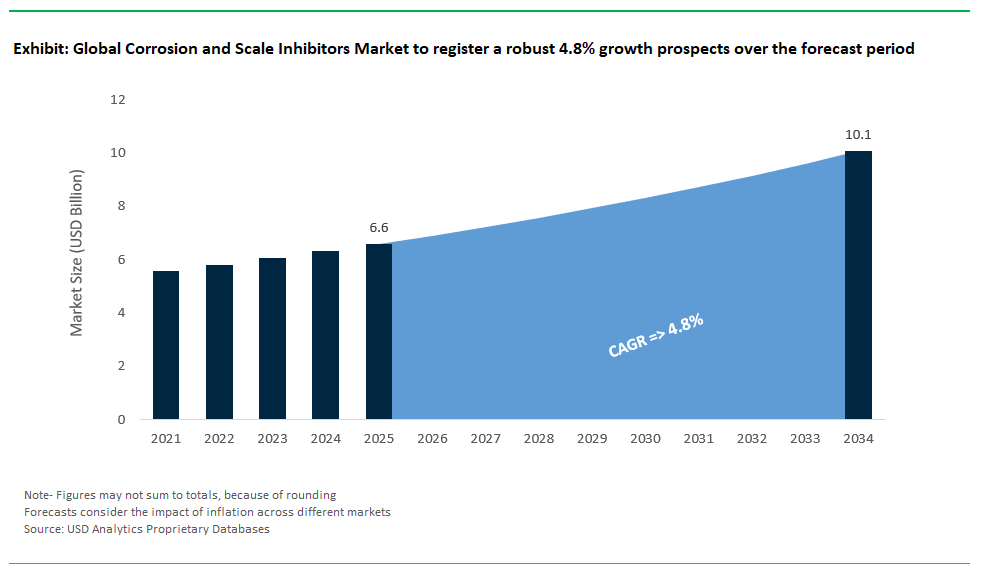

The corrosion and scale inhibitors market is valued at $6.6 billion in 2025 and is projected to reach $10.1 billion by 2034, with a CAGR of 4.8%. This sector plays a key role in industrial water treatment, HVAC systems, and desalination processes. The longevity of equipment and process uptime is closely linked to managing electrochemical degradation and mineral buildup. Traditional formulations mainly focus on phosphonate-based inhibitors, like HEDP and ATMP, which effectively prevent calcium carbonate scaling at concentrations of 2–10 mg/L. This helps operators keep LSI levels within the ideal range of +0.5 to -0.2, following the Cooling Technology Institute (CTI) guidelines.

In terms of corrosion control, cathodic inhibitors such as zinc orthophosphate are standard for metallic piping systems. This is particularly true in open-loop and once-through cooling circuits. These compounds generally reduce corrosion rates by 90–95% at doses as low as 0.5–5 mg/L, as confirmed under ASTM G199 protocols. This allows users to meet or beat ASME PPE-1's benchmark of <0.1 mm/year in critical applications. However, growing environmental and regulatory pressures are pushing for non-toxic, biodegradable alternatives.

Green inhibitors, such as polyaspartic acid, compete with traditional phosphonates. They achieve 85% scale inhibition at just 10 ppm, similar to HEDP's effectiveness at 15 ppm. They also offer better biodegradability and lower phosphorus content, which is a rising concern in areas sensitive to discharges. This shift is not just about regulations; it’s also operational. Zero-liquid discharge (ZLD) systems and membrane-integrated platforms need scale inhibitors that tolerate high calcium levels, require minimal dispersants, and work with polymer surfaces. The market is also moving toward multifunctional chemistries. These formulations combine anti-scalants, corrosion inhibitors, and dispersants, supported by smart dosing control and sensor-based corrosion rate feedback.

Green Chemistry and Advanced Technologies Transform the Corrosion and Scale Inhibitors Market

Market Trend: Green Chemistry and Smart Release Systems Redefine Corrosion and Scale Inhibitor Formulations

The corrosion and scale inhibitors market is changing significantly as environmental regulations, ESG mandates, and performance needs come together to phase out older chemistries in favor of green, bio-based, and smart-release options. Traditional formulations based on phosphonates, nitrites, molybdates, and heavy metals are quickly losing popularity due to their long-lasting environmental effects and regulatory issues. In response, manufacturers are speeding up the development of plant-derived and amino acid-based alternatives. Ecolab’s 2024 launch of OptiGuard™ Bio, a tannin-based inhibitor, has replaced phosphonates in key cooling applications, such as Microsoft’s hyperscale data centers. It achieves 90% scale control with half the toxicity, a crucial metric in industries sensitive to ESG issues. At the same time, Europe’s REACH regulation update has banned several traditional inhibitors, increasing demand for BASF’s Sokalan® AS series. This series uses amino acid and carboxylate complexes to protect metals without producing regulated byproducts. Additionally, smart release technologies are improving durability and dosage accuracy. Solenis’ IntelliRelease platform, which utilizes pH-responsive microencapsulation, has shown a threefold increase in active inhibitor lifespan in oilfield pipelines. This is essential in changing flow and temperature conditions, like those in the Permian Basin. These developments indicate a trend where choosing an inhibitor is no longer just about costs or scale control; the new focus emphasizes ecological impact, system responsiveness, and overall lifecycle performance. As industries, from data centers to desalination plants, adopt zero-discharge and carbon-reduction goals, the need for non-toxic, biodegradable, and condition-adaptive inhibitor systems is setting new global standards across water and industrial treatment sectors.

Market Opportunity: Hydrogen Economy and CCUS Systems Drive Next-Generation Inhibitor Demand

A rapidly growing and strategic opportunity for manufacturers of corrosion and scale inhibitors is the global rise of the hydrogen economy, carbon capture, utilization, and storage (CCUS), along with high-enthalpy geothermal energy systems. These sectors present extreme conditions, including high temperatures, harsh wet gases, and new fluid chemistries, which necessitate entirely new approaches to corrosion control. In green hydrogen setups, metal integrity faces challenges from hydrogen embrittlement and corrosion sped up by moisture and heat. On the other hand, in CCUS systems, the degradation of amine-based solvents by oxygen and acidic gases requires tailored inhibitor strategies for absorber columns. Exxon’s Houston Hub is focusing on cutting down O&M costs and downtime. In subsea CO₂ storage operations, such as the Northern Lights Project, scale inhibitors are being designed to prevent mineral buildup under pressure, ensuring the long-term function of salt-prone injection sites. Finally, in geothermal energy, inhibitors must work at temperatures of 300°C or higher. Iceland’s ON Power has developed silicate-free inhibitors that reduce calcium and silica scaling in superheated brines. This advancement helps avoid costly shutdowns, saving over $2 million yearly in unplanned maintenance. These essential infrastructures indicate a significant shift in corrosion risk and will need specialized, high-value inhibitors that traditional formulations cannot provide. As the Middle East’s desalination sector also drives the need for silica-specific scale inhibitors, the market is splitting. Commodity chemistries will decline, while engineered inhibitors for energy transition and high-value water systems will see rapid growth.

Corrosion and Scale Inhibitors Market Competitive Landscape

The corrosion and scale inhibitors market in the water treatment sector is highly competitive and diverse. Key players position themselves across three main value areas: integrated service models, specialized chemistries, and raw material leadership. Global leaders like Ecolab (Nalco Water), SUEZ, and Kurita Water Industries stand out with bundled offerings that combine chemical treatment with monitoring technologies. Ecolab’s success comes mainly from its proprietary 3D TRASAR system, which allows real-time performance tracking in both industrial and municipal settings. This system ensures operational efficiency and compliance. Similarly, Kurita offers TOC and conductivity controls aimed at ultrapure and precision-sensitive industries, such as microelectronics and pharmaceuticals. SUEZ competes by using its global water management expertise with digital platforms like AQUADVANCED and integrated long-term service contracts, strengthening its position in municipal and industrial sectors.

In contrast, companies like Solenis, Kemira, Lubrizol, and Buckman concentrate on high-performance chemistries and tailored treatment programs for specific industrial sectors, including pulp and paper, oil and gas, and chemical processing. Solenis offers phosphate-free and application-specific inhibitors, gaining popularity in industries that prioritize sustainability. Kemira combines its polymer innovation with knowledge of municipal systems and energy sectors. Lubrizol addresses tough conditions in HVAC and geothermal systems with its Tempest range of polymer-based inhibitors, which perform well under severe scaling and corrosion pressures. Buckman excels in operational consulting within pulp and paper and chemical manufacturing, enhancing customer loyalty through practical support.

On the upstream side, material suppliers such as Nouryon and Dow play a key role. They produce essential inhibitor building blocks, such as phosphonates, acrylic polymers, and phosphinocarboxylic acids, which are vital for many formulated products. These companies help downstream blenders and formulators maintain a steady supply chain and product consistency, especially in markets where regulations are strict.

The market is also putting more focus on environmental compliance. There is an increasing demand for phosphorus-free products and inhibitors that work effectively in high-recycle or high-TDS environments. Companies like Italmatch Chemicals (BWA Water Additives) have made significant strides in this area by providing advanced polymers and non-traditional phosphonates for silica-rich, barite-prone, and high-temperature conditions found in desalination, mining, and oil production. Niche innovators like Cortec offer vapor phase and migrating corrosion inhibitors (VpCI/MCI), which protect closed-loop systems, dry layups, and structural concrete, addressing needs outside the typical aqueous treatment market.

Corrosion and Scale Inhibitors Market – Segmentation Insights (2025–2034)

By Type: Organic Inhibitors Dominate the Market While Hybrid Inhibitors Grow Fastest

In the corrosion and scale inhibitors market, organic inhibitors hold the largest market share, accounting for approximately 49.8% in 2025. These inhibitors are favored across diverse industrial systems due to their high efficiency, biodegradability, and adaptability to a wide range of pH and temperature conditions. Commonly used in closed-loop systems, boilers, and cooling circuits, organic inhibitors such as amines, azoles, and polymers are increasingly preferred for their environmentally friendly profiles and compatibility with modern water treatment protocols. In contrast, hybrid inhibitors are the fastest-growing category, projected to expand at a CAGR of 5.9% through 2034. These formulations combine the strengths of organic and inorganic chemistries to deliver superior corrosion control, reduced scaling, and longer system lifespans, making them ideal for high-demand industrial applications. Meanwhile, inorganic inhibitors like phosphates, molybdates, and silicates continue to serve cost-sensitive applications, especially where regulatory constraints are less stringent, despite their relatively moderate growth.

By End-Use Industry: Water Treatment Sector Leads; Pharmaceutical Industry Shows Highest Growth

Among end-use industries, water treatment leads the corrosion and scale inhibitors market with a share of approximately 31.3% in 2025. The segment’s dominance is fueled by the widespread deployment of these inhibitors in cooling towers, boilers, and closed water systems within municipal utilities and industrial plants. Preventing metal corrosion and scale deposition is essential for maintaining operational efficiency and prolonging the life of infrastructure and equipment. The oil and gas industry follows closely, relying heavily on inhibitors to protect pipelines, drilling equipment, and refinery systems from corrosive environments. However, the pharmaceutical industry stands out as the fastest-growing segment, advancing at a CAGR of 6.5% over the forecast period. This growth is driven by strict compliance requirements for high-purity process water and the need to prevent contamination from corrosion by-products in manufacturing environments. The food and beverage sector also shows steady momentum, adopting these inhibitors to support sanitary equipment operation and regulatory compliance. Other contributors include metal processing, pulp and paper, and general manufacturing sectors, all of which continue to rely on corrosion and scale inhibitors for cost-effective maintenance and process integrity.

.png)

United States Leads Corrosion and Scale Inhibitors Market with Digital Innovation and High-Performance Formulations

The United States continues to shape the global corrosion and scale inhibitors market through relentless product innovation and the adoption of digital technologies in water treatment. In 2024, major U.S. chemical manufacturers accelerated the development of low- and no-phosphate inhibitor programs for boiler water treatment, responding to rising regulatory scrutiny and the need to minimize the environmental footprint of industrial discharge. The integration of artificial intelligence (AI) and real-time monitoring for predictive maintenance is becoming mainstream, enabling more efficient chemical dosing, lower operational costs, and superior system performance.

The oil and gas sector remains a primary application, demanding high-performance inhibitors to safeguard pipelines and drilling infrastructure under extreme conditions. Simultaneously, the pharmaceutical industry is ramping up consumption, requiring corrosion and scale inhibitors to maintain purity and reliability in high-pressure steam boiler systems for sterilization and production processes. This dual focus on advanced technology and strict compliance underpins the United States’ leadership in the evolution of global corrosion and scale inhibitor solutions.

China Drives Corrosion and Scale Inhibitors Market with Industrial Expansion and Eco-Friendly Advances

China’s corrosion and scale inhibitors market is expanding rapidly, propelled by extensive industrialization, infrastructure investment, and increasingly stringent environmental regulations. Ongoing growth in thermal power generation and manufacturing heightens the demand for advanced inhibitors to protect high-pressure boilers and cooling systems from scale and corrosion, essential for plant reliability and energy efficiency. The government’s campaign for pollution control is spurring the shift toward environmentally friendly, biodegradable inhibitor formulations, with local companies innovating phosphonate-free and polymer-based products for minimal environmental impact.

The widespread challenge of high water hardness in many Chinese regions drives persistent demand for effective antiscalants and corrosion inhibitors across multiple sectors. Active R&D pipelines ensure a steady flow of new, eco-efficient solutions, supporting China’s ambition to balance industrial growth with environmental stewardship and operational longevity.

Germany Champions Eco-Friendly Corrosion and Scale Inhibitors with Advanced Monitoring and Biopolymer Solutions

Germany is a recognized leader in the global corrosion and scale inhibitors market, standing out for its dedication to high-performance, eco-friendly products and rigorous EU compliance. German manufacturers are developing innovative, phosphate-free inhibitor programs for ultra-supercritical boilers, prioritizing both chemical efficiency and environmental safety. Partnerships between chemical producers and industrial operators are driving adoption of sensor-driven dosing and real-time monitoring systems, optimizing inhibitor performance and reducing waste across water and steam cycles.

Ongoing R&D emphasizes biopolymer- and plant-based solutions, supporting the EU’s push for sustainability and non-toxic chemical use. The strategic integration of these next-generation inhibitors with smart water management technologies is ensuring German industry remains competitive while meeting the strict standards of the recast Drinking Water Directive and the circular economy.

India Accelerates Corrosion and Scale Inhibitors Market Growth with Policy Mandates and Industrial Expansion

India’s corrosion and scale inhibitors market is on a robust growth trajectory, fuelled by ambitious government projects, infrastructure investment, and tighter regulatory requirements for water management. The "National Mission on War Against Corrosion," launched in partnership with industrial leaders like Jindal Stainless, is driving awareness and adoption of best practices in corrosion management nationwide. The Jal Jeevan Mission and strict enforcement of the Environment (Protection) Act, 1986, are compelling industries to install and upgrade effluent treatment plants (ETPs), creating sustained demand for advanced inhibitors.

Rapid growth in power, oil and gas, and chemicals sectors is driving further uptake, as these industries depend on reliable, long-lasting boiler and cooling tower operation. India’s evolving market also supports the development and commercialization of innovative, cost-effective inhibitor formulations to address the country’s diverse industrial effluent challenges.

Japan Advances Corrosion and Scale Inhibitors Market with Specialized Chemistries and High-Purity Solutions

Japan’s market for corrosion and scale inhibitors is distinguished by technological sophistication and a relentless pursuit of high-purity, sustainable solutions for demanding industrial applications. Leading Japanese firms are developing advanced boiler and cooling water treatment additives, including eco-friendly, low-phosphorus, and low-zinc formulations that reduce environmental load while delivering high performance. The focus on advanced oxygen scavengers and internal boiler treatments ensures the longevity and operational efficiency of high-pressure systems.

With an industrial base spanning power generation, pulp and paper, and precision manufacturing, Japan emphasizes innovative chemistry to meet the highest standards of corrosion and scale control. Specialized solutions for the paper industry such as recovery boiler technologies with corrosion-resistant materials highlight the market’s commitment to sustainable, high-efficiency operations.

Brazil Strengthens Corrosion and Scale Inhibitors Demand with Infrastructure Growth and Regional Exports

Brazil is rapidly expanding its market for corrosion and scale inhibitors, supported by sweeping infrastructure projects and the continued development of its oil and gas sector. The nation’s new sanitation regulatory framework is driving significant private investment in water and wastewater treatment plants, where corrosion and scale inhibitors are essential for protecting assets and ensuring compliance. The oil and gas industry remains a top consumer, utilizing advanced inhibitors to mitigate corrosion and scaling risks in both onshore and offshore environments.

Growth in the cooling and boiler segments is also notable, reflecting Brazil’s robust industrial base and the rising demand for efficient water treatment. Exports of corrosion inhibitors are increasing, solidifying Brazil’s position as a leading regional supplier to other Latin American markets.

South Korea Advances Corrosion and Scale Inhibitors Market with Science-Driven Innovation and Power Sector Demand

South Korea’s market for corrosion and scale inhibitors is experiencing robust growth as the country invests in advanced manufacturing, chemical processing, and power generation. A heavy emphasis on scientifically engineered chemical solutions has led to the introduction of highly effective inhibitors designed to combat scale buildup and metallic corrosion, extending equipment life and reducing maintenance costs.

Technological innovation is central to market development, with companies focusing on formulations tailored for the specific needs of thermal and nuclear power plants the largest end-users of inhibitors in South Korea. As the country continues to expand its energy infrastructure, the role of advanced corrosion and scale inhibitors in maintaining operational efficiency and asset integrity is only expected to rise.

France Enhances Corrosion and Scale Inhibitors Market with Smart Water Management and Sustainability

France is reinforcing its position in the corrosion and scale inhibitors market through a new national water management plan and a growing focus on sustainable water treatment. The 2023–2030 water plan encourages reduced water abstraction and the adoption of unconventional water sources, pushing demand for advanced inhibitor technologies in municipal and industrial systems. Major players like Suez are pioneering integrated digital water solutions that combine real-time performance monitoring with advanced chemical dosing for maximum efficiency and reduced environmental impact.

The market is also experiencing a shift toward smart water management, where inhibitor systems are increasingly integrated with monitoring and control platforms to ensure compliance and resource efficiency. France’s plan for the protection of drinking water catchment areas underscores the need for effective, non-toxic corrosion control throughout national distribution networks, further driving innovation in approved chemical solutions.

Corrosion and Scale Inhibitors Market Report Scope

Corrosion and Scale Inhibitors Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.6 Billion

|

|

Market Size (2034)

|

$10.1 Billion

|

|

Market Growth Rate

|

4.8%

|

|

Segments

|

By Type (Inorganic Inhibitors, Organic Inhibitors, Hybrid Inhibitors), By Formulation (Liquid, Powder/Solid, Oil-based, Water-based, Volatile Corrosion Inhibitors (VCIs)), By Application (Scale Inhibition, Corrosion Inhibition, Multifunctional, Dispersants), By End-Use Industry (Water Treatment, Oil and Gas, Power Generation, Chemical and Petrochemical, Pulp and Paper, Metal Processing and Manufacturing, Food and Beverage, Pharmaceutical, Automotive, Construction, Mining and Metallurgy, Other Industries

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ecolab Inc. (U.S.), BASF SE (Germany), Solenis LLC (U.S.), SUEZ SA (France), Kurita Water Industries Ltd. (Japan), Kemira Oyj (Finland), Dow Inc. (U.S.), Nouryon (The Netherlands), The Lubrizol Corporation (U.S.), Cortec Corporation (U.S.), Buckman (U.S.), AkzoNobel (The Netherlands), Italmatch Chemicals (BWA Water Additives),

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Corrosion and Scale Inhibitors Market Segmentation

By Type

- Inorganic Inhibitors

- Phosphates

- Nitrites

- Molybdates

- Silicates

- Chromates

- Zinc compounds

- Others

- Organic Inhibitors

- Amines

- Phosphonates

- Carboxylates

- Polyacrylates

- Polymers

- Quaternary Ammonium Compounds

- Sulfonates

- Natural/Green Inhibitors

- Other Organic Compounds

- Hybrid Inhibitors

By Formulation

- Liquid

- Powder/Solid

- Oil-based

- Water-based

- Volatile Corrosion Inhibitors (VCIs)

By Application

- Scale Inhibition

- Corrosion Inhibition

- Multifunctional

- Dispersants

By End-Use Industry

- Water Treatment

- Cooling Water Treatment

- Boiler Water Treatment

- Desalination Plants

- Municipal Water Treatment

- Wastewater Treatment

- Oil and Gas

- Power Generation

- Chemical and Petrochemical

- Pulp and Paper

- Metal Processing and Manufacturing

- Food and Beverage

- Pharmaceutical

- Automotive

- Construction

- Mining and Metallurgy

- Other Industries

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Corrosion and Scale Inhibitors Market

- Ecolab Inc. (U.S.)

- BASF SE (Germany)

- Solenis LLC (U.S.)

- SUEZ SA (France)

- Kurita Water Industries Ltd. (Japan)

- Kemira Oyj (Finland)

- Dow Inc. (U.S.)

- Nouryon (The Netherlands)

- The Lubrizol Corporation (U.S.)

- Cortec Corporation (U.S.)

- Buckman (U.S.)

- AkzoNobel (The Netherlands)

- Italmatch Chemicals (BWA Water Additives)

* List Not Exhaustive

Research Coverage

This report investigates the global corrosion and scale inhibitors market, offering in-depth analysis reviews, advanced segmentation, and coverage of the latest breakthroughs in green chemistry, smart release systems, and high-performance formulations across water and industrial treatment. With detailed assessments of regulatory trends, end-user adoption, and material innovations, this report highlights the evolving landscape of corrosion and scale inhibitor solutions—from traditional phosphonates to next-generation, eco-friendly inhibitors, and hybrid formulations. Delivering a strategic perspective on market value, growth drivers, and competitive positioning, this report is an essential resource for industry professionals, product managers, suppliers, and investors seeking actionable insights into technology developments, policy impacts, and regional opportunities. Developed by USDAnalytics, this comprehensive research delivers a robust foundation for high-value decision-making across multiple industries reliant on advanced corrosion and scale management.

Scope Highlights:

- Segmentation:

- By Type: Inorganic Inhibitors (Phosphates, Nitrites, Molybdates, Silicates, Chromates, Zinc compounds, Others); Organic Inhibitors (Amines, Phosphonates, Carboxylates, Polyacrylates, Polymers, Quaternary Ammonium Compounds, Sulfonates, Natural/Green Inhibitors, Other Organic Compounds); Hybrid Inhibitors

- By Formulation: Liquid, Powder/Solid, Oil-based, Water-based, Volatile Corrosion Inhibitors (VCIs)

- By Application: Scale Inhibition, Corrosion Inhibition, Multifunctional, Dispersants

- By End-Use Industry: Water Treatment (Cooling Water Treatment, Boiler Water Treatment, Desalination Plants, Municipal Water Treatment, Wastewater Treatment), Oil and Gas, Power Generation, Chemical and Petrochemical, Pulp and Paper, Metal Processing and Manufacturing, Food and Beverage, Pharmaceutical, Automotive, Construction, Mining and Metallurgy, Other Industries

- Geographic Scope: Covers 25+ countries across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

- Data Coverage: Historic data from 2021 to 2024 and forecasts from 2025 to 2034.

- Key Players: Ecolab Inc. (U.S.), BASF SE (Germany), Solenis LLC (U.S.), SUEZ SA (France), Kurita Water Industries Ltd. (Japan), Kemira Oyj (Finland), Dow Inc. (U.S.), Nouryon (The Netherlands), The Lubrizol Corporation (U.S.), Cortec Corporation (U.S.), Buckman (U.S.), AkzoNobel (The Netherlands), Italmatch Chemicals (BWA Water Additives).

Methodology

USDAnalytics applies a rigorous, multi-step methodology combining primary research with in-depth secondary data analysis. Quantitative forecasts are supported by proprietary market modeling, triangulating company financials, industry benchmarks, regulatory sources, and expert interviews. Qualitative analysis integrates technological trends, competitive benchmarking, and scenario analysis to ensure actionable insights and reliable guidance for stakeholders in the corrosion and scale inhibitors market. This comprehensive approach ensures accuracy and depth for both historic and forward-looking assessments.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements