Dynamic Growth and Breakthrough Performance in Scale Inhibitors for Geothermal Power Plants Water Treatment Market

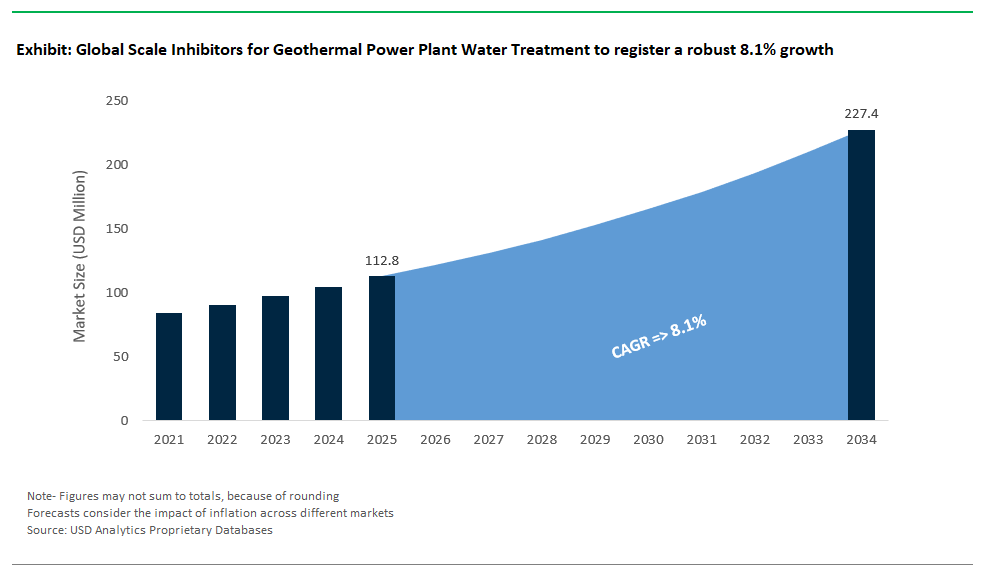

The scale inhibitors market for geothermal power plants water treatment is valued at $112.8 million in 2025 and projected to reach $227.4 million by 2034, advancing at a CAGR of 8.1%. This market is uniquely defined by high-temperature operational demands, extreme saturation conditions, and complex brine chemistries that routinely exceed conventional treatment design envelopes. Unlike surface water or industrial systems, geothermal fluids can carry dissolved silica in concentrations surpassing 500 ppm, well beyond the natural polymerization threshold of 150 ppm at 150°C. Polymeric dispersants engineered to delay nucleation and inhibit aggregation are capable of stabilizing silica at 500–650 ppm through adsorption-mediated mechanisms that extend the induction time for silica polymerization beyond 60 minutes. This extended kinetic window is critical for managing scaling across production wells, separators, and reinjection systems without sacrificing brine throughput (DOE Geothermal Technologies Office).

In parallel, metal sulfide precipitation, particularly of Fe²⁺ and Zn²⁺ species, is a persistent fouling concern in flash and binary systems. Chelating agents such as nitrilotris(methylenephosphonic acid) (NTMP) have demonstrated efficacy at concentrations between 5–20 ppm, effectively stabilizing divalent metals and preventing co-precipitation with silica or sulfide phases (NACE SP0595). However, inhibitor performance in geothermal plants is fundamentally constrained by thermal stability.

Flash steam systems operating above 200°C require chemical additives that can resist hydrothermal breakdown while maintaining dispersant function a standard supported by performance data from GRC Transactions and field deployments in volcanic geothermal fields. The market is evolving from static scale control regimens to dynamic chemical conditioning strategies, supported by downhole monitoring, real-time fluid chemistry profiling, and adaptive dosage modeling.

Suppliers offering high-temperature-stable formulations with multi-ion stabilization and field-proven brine compatibility are increasingly favored by geothermal operators under pressure to reduce well maintenance frequency, extend plant uptime, and increase megawatt-hour yields from aging reservoirs.

High-Performance Scale Inhibitors Transform Geothermal Energy and Critical Mineral Recovery Markets

Market Trend: Advanced Inhibitor Chemistry Targets Silica and Metal Sulfide Scaling in High-Temperature Geothermal Brines

As geothermal energy projects scale globally, the demand for high-performance scale inhibitors is intensifying, particularly in the management of silica and metal sulfide deposition two of the most costly and efficiency-limiting challenges in geothermal brine systems. Traditional phosphonate-based inhibitors are proving inadequate in the face of extreme temperatures (>250°C) and aggressive chemistries. In response, chemical innovators are developing next-generation formulations like Solvay’s Sokalan® HT100, a phosphino-polycarboxylate solution capable of stabilizing amorphous silica at 300°C and 100 bar pressure. Field tests at the Hellisheiði Power Station in Iceland demonstrate a 60% reduction in silica scaling and improved reinjection flow rates. Likewise, nanoparticle-modified inhibitors deployed at ORMAT’s Nevada plant have reduced silica fouling by 70%. On the sulfide front, Clariant’s Hastion™ 9500 delivers robust chelation performance against FeS and ZnS in highly acidic brines (pH 2–4), a breakthrough for Indonesian geothermal fields like Sorik Marapi. The implications are significant: even 1 mm of mineral scale can reduce turbine efficiency by up to 5%, while advanced inhibitors offer 40% lower dosing rates than legacy phosphonates, extending stainless steel component lifespans by 3x. This marks a critical inflection point in geothermal operations, where chemical innovation is directly linked to energy yield, equipment longevity, and carbon reduction.

Growth Opportunity: Scale Inhibitors Powering Lithium Recovery & Supercritical CO₂-Geothermal Hybrids

The next wave of geothermal development is being shaped by binary cycle and co-production technologies, where scale inhibitors play a pivotal enabling role. A prime example is EnergySource’s Hudson Ranch II in California, which integrates lithium extraction from geothermal brines a process vulnerable to silica-induced membrane and reactor fouling. Advanced formulations prevent silica polymerization while boosting lithium carbonate recovery by 15%. Additionally, supercritical CO₂ (sCO₂) geothermal systems, such as NET Power’s Texas pilot, are deploying specialty polyacrylates to suppress CaCO₃ scaling in closed-loop, high-efficiency turbines operating at 200 bar. Even in direct-use applications, like Tokyo Gas’ MegaCelsius™ district heating networks, non-phosphorus scale inhibitors are allowing 90% brine reuse with minimal maintenance. These advancements are not only improving project economics but also unlocking new revenue streams through critical mineral recovery and carbon credit monetization as seen in KenGen’s Olkaria Plant, which earns $2 million annually in emissions credits by reducing scale-related energy losses. As global demand for clean energy and battery metals soars, chemical suppliers that innovate in geothermal scale inhibitors especially with IP-secured, multi-functional, and environmentally safe profiles stand to capture premium market segments in an increasingly electrified and resource-conscious energy landscape.

Competitive Landscape: Geothermal Scale Inhibitors

The geothermal scale inhibitor market consists of a small group of specialized suppliers. They tackle a major challenge in the industry: the formation of silica and silicate scales during fluid cooling and reinjection. Solutions in this area depend heavily on a supplier's ability to control amorphous silica polymerization, handle extreme thermal and chemical stress, and work with plant-level monitoring and automation systems. Ecolab’s Nalco Water unit stands out as a leading provider of high-temperature scaling solutions. It does this mainly through its Nalco 5600 series and 3D TRASAR platform. These tools allow for real-time adjustment of dosing based on field conditions. Solenis, a dedicated water treatment company, sets itself apart with its phosphate-free silica control chemistries, like PHOSFREE, and its effectiveness in complex brines where traditional products struggle.

Italy-based Italmatch Chemicals, with its BWA Water Additives portfolio, has established a strong presence through its GEOTERM line. This line specifically targets extreme scaling environments, such as those found in high-pH and high-TDS geothermal fluids. Kurita Water Industries further enhances this competitive scene by focusing on thermally stable polymers and precise monitoring systems that aim to boost performance in harsh brine conditions. Veolia, formerly known as SUEZ Water Technologies, provides bundled solutions. These include Hydrex Geo inhibitors combined with process optimization platforms like Hubgrade and AQUADVANCED, making it a full-cycle solution provider. Niche players like TPC Technology and Buckman offer targeted capabilities. TPC specializes in brine-specific inhibitor customization for calcite and silica scales in high-pressure wells. Meanwhile, Buckman provides integrated systems for controlling corrosion and scale in geothermal sites with severe fouling issues.

Major global oilfield chemical companies, such as Baker Hughes, also use their upstream experience through platforms like WATERLYTICS to offer predictive scaling analytics and effective inhibitor blends suitable for extreme temperature wells. Lastly, regional suppliers like Accepta Ltd. offer flexible and affordable formulations for smaller geothermal systems, especially in the UK and parts of Europe. Here, regulations on phosphorus content influence product choices.

In this competitive landscape, differentiation relies on six key factors: inhibitor performance in temperatures above 150°C, the ability to suppress silica polymerization without phosphorus, compatibility with carbon steel and elastomers, integration with real-time monitoring, successful field results at sites like Salton Sea, Iceland, and the Philippines, and extensive formulation knowledge relevant to site-specific brine chemistries. Vendors that merge these capabilities with dependable service support and data-driven dosing control are best equipped to address the operational and regulatory needs of modern geothermal projects.

Scale Inhibitors for Geothermal Power Plant Water Treatment Market – Segmentation Insights (2025–2034)

By Type of Scale Inhibited: Silica Inhibitors Lead the Market While Sulfide Inhibitors Grow Fastest

Silica (SiO₂) inhibitors hold the largest share of the geothermal scale inhibitors market, accounting for approximately 39.1% in 2025. This dominance is driven by the prevalence of high-silica geothermal brines, often exceeding 800 ppm, which pose significant scaling challenges during flashing and pressure reduction stages. Silica deposits are notoriously difficult to remove once formed, leading to severe operational issues in production lines and surface equipment. As a result, advanced polymeric and organosilicate-based inhibitors are being increasingly deployed to prevent amorphous silica fouling across high-temperature geothermal operations. Meanwhile, sulfide scale inhibitors are experiencing the fastest growth, expanding at a 9.1% CAGR through 2034. Their rise is fueled by increased development of hydrogen sulfide-rich geothermal reservoirs, particularly in regions like Indonesia, the Philippines, and Turkey. These inhibitors are essential for mitigating iron sulfide and zinc sulfide deposition, especially in reinjection systems and production lines. Calcium carbonate inhibitors also maintain strong relevance, especially in moderate-temperature reservoirs, while sulfate inhibitors are critical for preventing barite and celestite scaling. Other mineral scale inhibitors including those targeting magnesium silicates and iron oxides support specific field conditions and niche operational challenges.

.png)

By Application Point/System Component: Production Wells & Lines Dominate While Re-injection Systems Grow Fastest

Production wells and associated pipeline systems account for the largest market share in 2025, at approximately 44.8%, reflecting their vulnerability to rapid scaling during flash steam expansion and temperature-induced precipitation. These systems are the first point of contact with geothermal brine and require continuous dosing of scale inhibitors to ensure operational stability, reduce cleaning frequency, and maintain flow rates. As geothermal plants push for higher enthalpy recovery, the risk of scaling in production pipelines grows, reinforcing demand for highly stable and high-temperature-resistant inhibitors. Re-injection wells and lines represent the fastest-growing segment, projected to expand at a 8.9% CAGR over the forecast period. This growth is tied to the global transition toward sustainable closed-loop geothermal systems, where re-injection is crucial for reservoir longevity and regulatory compliance. Scale formation in reinjection wells especially barite, celestite, and iron sulfides can significantly reduce permeability, necessitating aggressive chemical prevention strategies. Surface equipment, including separators and heat exchangers, maintains steady demand for scale control, while turbine systems require specialty inhibitors to prevent even minor deposits that could impair efficiency or cause turbine blade damage. Cooling water systems also contribute to overall demand, particularly in binary and hybrid geothermal configurations.

United States Leads Global Market for Geothermal Scale Inhibitors with Innovation and Digital Optimization

The United States stands as the world’s foremost producer of geothermal energy and an innovator in water treatment for these demanding systems. The U.S. Department of Energy’s Geothermal Technologies Office (GTO) continues to fund breakthrough research targeting operational challenges such as scaling one of the primary causes of reduced geothermal plant efficiency and increased maintenance. American companies are advancing chemical formulations for silica, silicate, carbonate, and sulfate scale inhibition, resulting in fewer injection well cleanings and extended plant run times.

Digital technologies are now at the core of U.S. operations. Predictive modeling services like Ecolab’s Geomizer forecast scale risk and optimize inhibitor dosing in real-time, minimizing downtime and reducing costs. These tools, along with data-driven chemical programs, are crucial for preventing scale build-up in production and injection wells a vital aspect of maintaining reservoir permeability and power output. The ongoing commitment to innovation ensures that the U.S. market remains at the forefront of geothermal scale control worldwide.

Indonesia Expands Scale Inhibitor Market with Rapid Geothermal Growth and High-Mineral Fluid Challenges

Indonesia’s geothermal sector is experiencing significant expansion, making it one of the world’s largest and fastest-growing markets for geothermal scale inhibitors. The government’s energy transition policies and large-scale developments such as Sorik Marapi Unit 5, Salak, and Lahendong expansions are increasing demand for advanced water treatment solutions. Indonesia’s geothermal fluids, often rich in dissolved minerals and found in volcanic regions, create challenging conditions that necessitate specialized scale inhibitors to prevent equipment fouling and maintain reservoir integrity.

As more projects break ground and capacity expansions continue, operators are relying on next-generation silica and carbonate scale inhibitors to tackle the unique scaling issues presented by Indonesia’s reservoirs. The move toward more sustainable energy, coupled with the country’s ambitious geothermal development roadmap, ensures continued growth for water treatment chemical suppliers specializing in geothermal applications.

New Zealand Sets Standards in Geothermal Scale Inhibition with Binary Cycle Technology and Environmental Stewardship

New Zealand’s mature geothermal sector is known for both its advanced technology adoption and its strong environmental ethos. Large-scale plants like Tauhara II (commissioned in 2024) highlight the country’s expansion, with binary cycle technologies enabling the use of lower-temperature and more chemically diverse geothermal fluids. These innovations require robust chemical programs, particularly scale inhibitors, to protect heat exchangers and plant components from mineral deposition.

The New Zealand market is characterized by continuous R&D, as plant operators seek out new inhibitor formulations capable of handling the unique geochemical profiles of local reservoirs. Environmental sustainability is paramount, leading to the adoption of scale inhibitors that are effective yet environmentally benign. New Zealand’s approach demonstrates how technological progress and ecological responsibility can drive market development for advanced geothermal water treatment chemicals.

Türkiye Drives Scale Inhibitor Demand with Rapid Geothermal Capacity Increases and Custom Treatment Needs

Türkiye’s geothermal sector is expanding at an unprecedented pace, supported by the commissioning of new power plants such as GreenEco 7, Open Mountain T-01, and Hez Morali. This rapid growth is driving strong demand for customized scale inhibitors and related water treatment chemicals. Türkiye’s geothermal fields feature diverse geological formations, which require site-specific chemical strategies to combat scaling from calcium carbonate, silica, and other minerals.

The integration of geothermal energy for both power generation and district heating underscores the need for robust chemical protection across the entire system from wellhead to heat exchangers. Government support for renewable energy continues to catalyze investment, boosting both the development of geothermal projects and the water treatment market supporting them.

Japan Innovates Scale Inhibitor Market with R&D Partnerships and Targeted Solutions for Unique Reservoir Chemistry

Japan’s geothermal industry is leveraging technological sophistication to overcome persistent scaling challenges, particularly those posed by silica-rich fluids. Projects like Appi, Suginoi, and Minami-Kayabe reflect renewed momentum in geothermal development, with operators partnering closely with chemical suppliers and research institutes. Japanese advancements include novel inhibitor chemistries and precision injection techniques, tailored for the unique chemical makeup of domestic geothermal reservoirs.

Real-time monitoring and diagnostic systems are increasingly used to fine-tune inhibitor dosing and prevent scaling before it impacts plant operations. As Japan aims to unlock more of its vast geothermal potential often located in protected or difficult-to-access regions innovative, efficient scale control solutions are key to sustainable development.

Germany Boosts Geothermal Scale Inhibitor Market with Deep Reservoir Development and Policy Support

Germany’s geothermal market is growing rapidly, especially in the area of deep geothermal resources for both heating and electricity generation. Recent legislative changes now grant geothermal projects “overriding public interest” status, accelerating their development and increasing the need for high-performance scale inhibitors that can operate in deep, mineral-rich reservoirs.

German operators and chemical providers are focused on tailoring inhibitors to match the unique chemistry of deep formations, which often differ significantly from conventional hydrothermal systems. Projects such as the new Kalina process plant in southern Germany exemplify the need for specialized chemicals to ensure system longevity and efficiency. As Germany moves to decarbonize its heating sector with geothermal energy, the market for advanced water treatment solutions is set for robust growth.

Canada Emerges as a New Market for Geothermal Scale Inhibitors Amid Project Startups and Resource Extraction

Canada’s geothermal market is still emerging but is poised for significant expansion thanks to government support and new project launches in multiple provinces. While there are currently no operational power plants, projects like the Mount Meager Geothermal Project are paving the way for future adoption of scale inhibitors tailored to the country’s unique geothermal brine chemistries.

Canada is also pursuing co-production opportunities, such as lithium extraction from geothermal brines, which creates demand for highly specialized chemical treatments that can prevent scaling while supporting resource recovery. Federal funding and regulatory backing are expected to further accelerate geothermal project development and the associated market for water treatment chemicals.

Russia Grows Scale Inhibitor Market with Long-Standing Plants and New Geothermal Development in Kamchatka

Russia’s geothermal scale inhibitor market is anchored in the Kamchatka Peninsula, where several plants including Pauzhetka and Mutnovsky rely on chemical treatment programs to manage aggressive geothermal fluids. RusHydro, the state energy company, oversees maintenance and operation, deploying high-performance inhibitors to control scaling and corrosion in some of the world’s most challenging geothermal environments.

New projects, like the 100 MW Mutnovsky expansion, are expected to further increase demand for advanced water treatment chemicals. Russia’s focus on upgrading and expanding its geothermal power base, despite the operational challenges posed by highly mineralized fluids, ensures a steady and growing need for scale inhibitors optimized for extreme conditions.

Scale Inhibitors for Geothermal Power Plant Water Treatment Report Scope

Scale Inhibitors for Geothermal Power Plant Water Treatment

|

Parameter

|

Details

|

|

Market Size (2025)

|

$112.8 Million

|

|

Market Size (2034)

|

$227.4 Million

|

|

Market Growth Rate

|

8.1%

|

|

Segments

|

By Type of Scale Inhibited (Silica (SiO2) Inhibitors, Calcium Carbonate (CaCO3) Inhibitors, Sulfate Scale Inhibitors, Sulfide Scale Inhibitors, Other Mineral Scales), By Chemical Composition (Phosphonates, Polymeric Carboxylates and Sulfonates, Green/Environmentally Friendly Inhibitors, Chelating Agents, Other Formulations), By Application Point/System Component (Production Wells and Lines, Surface Equipment, Re-injection Wells and Lines, Cooling Water Systems, Turbine Systems), By Geothermal Power Plant Type (Flash Steam Plants, Binary Cycle Plants, Dry Steam Plants), By Scale Inhibition Mechanism (Threshold Inhibition, Crystal Modification, Dispersion

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ecolab Inc. (U.S.), Solenis LLC (U.S.), Italmatch Chemicals S.p.A. (Italy), Kurita Water Industries Ltd. (Japan), SUEZ SA (France), Veolia Water Technologies (France), TPC Technology (U.S.), Buckman (U.S.), Baker Hughes (U.S.), Accepta Ltd. (UK),

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Scale Inhibitors for Geothermal Power Plant Water Treatment Market Segmentation

By Type of Scale Inhibited

- Silica (SiO2) Inhibitors

- Calcium Carbonate (CaCO3) Inhibitors

- Sulfate Scale Inhibitors

- Sulfide Scale Inhibitors

- Other Mineral Scales

By Chemical Composition

- Phosphonates

- Polymeric Carboxylates and Sulfonates

- Green/Environmentally Friendly Inhibitors

- Chelating Agents

- Other Formulations

By Application Point/System Component

- Production Wells and Lines

- Surface Equipment

- Heat Exchangers

- Flash Vessels/Separators

- Piping

- Pumps

- Re-injection Wells and Lines

- Cooling Water Systems

- Turbine Systems

By Geothermal Power Plant Type

- Flash Steam Plants

- Binary Cycle Plants

- Dry Steam Plants

By Scale Inhibition Mechanism

- Threshold Inhibition

- Crystal Modification

- Dispersion

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Scale Inhibitors for Geothermal Power Plant Water Treatment

- Ecolab Inc. (U.S.)

- Solenis LLC (U.S.)

- Italmatch Chemicals S.p.A. (Italy)

- Kurita Water Industries Ltd. (Japan)

- SUEZ SA (France)

- Veolia Water Technologies (France)

- TPC Technology (U.S.)

- Buckman (U.S.)

- Baker Hughes (U.S.)

- Accepta Ltd. (UK)

* List Not Exhaustive

Research Coverage

This report by USDAnalytics investigates the Scale Inhibitors for Geothermal Power Plant Water Treatment Market, offering comprehensive insights into technological advancements, competitive strategies, and key growth drivers. It highlights breakthroughs in inhibitor chemistry, digital dosing optimization, and geothermal resource utilization strategies. The analysis reviews trends in high-temperature performance, sustainability, and custom chemical formulations for complex brine systems. This report is an essential resource for industry professionals seeking to understand geothermal scaling challenges and strategic solutions for operational efficiency, lithium recovery, and hybrid energy projects.

Scope Highlights

- Segmentation:

- By Type of Scale Inhibited: Silica (SiO₂) Inhibitors, Calcium Carbonate (CaCO₃) Inhibitors, Sulfate Scale Inhibitors, Sulfide Scale Inhibitors, Other Mineral Scales

- By Chemical Composition: Phosphonates, Polymeric Carboxylates and Sulfonates, Green/Environmentally Friendly Inhibitors, Chelating Agents, Other Formulations

- By Application Point/System Component: Production Wells and Lines, Surface Equipment (Heat Exchangers, Flash Vessels, Piping, Pumps), Re-injection Wells and Lines, Cooling Water Systems, Turbine Systems

- By Geothermal Power Plant Type: Flash Steam Plants, Binary Cycle Plants, Dry Steam Plants

- By Scale Inhibition Mechanism: Threshold Inhibition, Crystal Modification, Dispersion

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

- Historic Data: 2021–2024; Forecast Data: 2025–2034

- Companies Covered: Ecolab Inc., Solenis LLC, Italmatch Chemicals S.p.A., Kurita Water Industries Ltd., SUEZ SA, Veolia Water Technologies, TPC Technology, Buckman, Baker Hughes, Accepta Ltd.

Methodology

This study employs a hybrid research methodology, integrating primary interviews with geothermal operators, chemical suppliers, and technology providers along with secondary research from credible industry reports, technical papers, and regulatory databases. Market estimation uses top-down and bottom-up forecasting techniques, supported by data triangulation for accuracy. Predictive modeling, sensitivity analysis, and adoption curve mapping ensure robust segment-level forecasts. Expert validation from geothermal engineers and chemical specialists enhances the reliability of the insights for strategic decision-making.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements