Water Treatment Chemicals in Data Centers and Electronics Manufacturing Market Outlook: Growth Analysis and Forecast

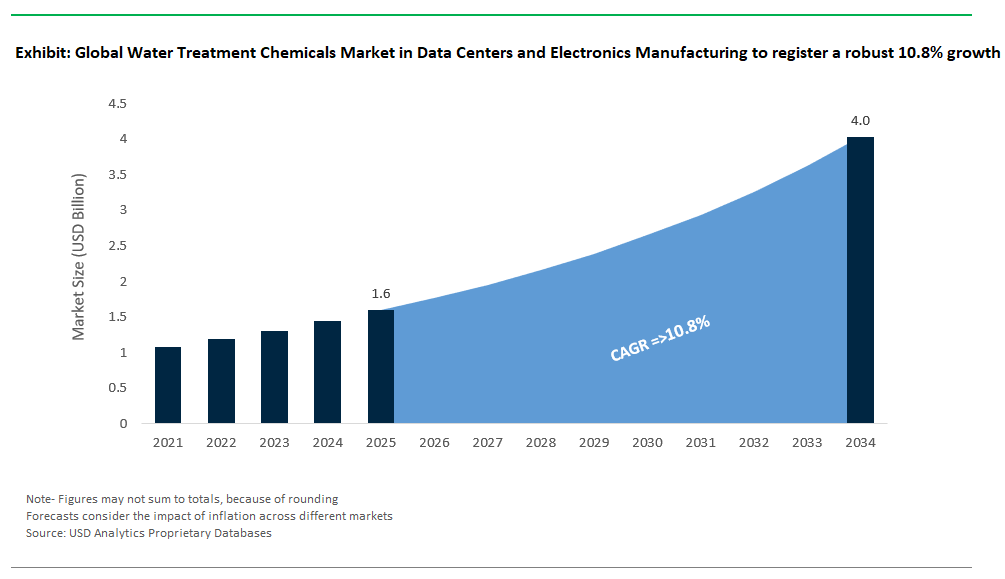

The market for water treatment chemicals in data centers and electronics manufacturing is valued at $1.6 billion in 2025 and projected to reach $4 billion by 2034, with a strong CAGR of 10.8%. This sector is uniquely shaped by the dual imperatives of purity and process stability, where even trace-level contaminants can trigger catastrophic outcomes from microchip failure to heat exchanger fouling. In electronics fabs, particularly semiconductor lines, water treatment systems are engineered to meet ultrapure water (UPW) specifications as defined by SEMI F63-0221. These stringent thresholds place exceptional demands on every upstream treatment stage, from pretreatment to polishing, where chemical additives must operate cleanly, predictably, and without trace residue.

Data centers especially hyperscale and colocation facilities are increasingly adopting closed-loop or hybrid water cooling systems that demand reliable biofilm control and corrosion mitigation without compromising thermal efficiency. Advanced oxidation processes (AOPs), particularly UV/TiO₂ systems, are gaining ground in both domains. These systems are favored for their ability to eliminate low-molecular-weight contaminants that elude conventional ion exchange or RO filtration.

In microbial control, ozone-resistant biocides are deployed in pulse-mode dosing, maintaining bacterial counts low in ozone-rich polishing loops, critical for maintaining system sterility without introducing halogenated byproducts.

As regulatory expectations around microelectronics effluent discharge and data center water usage intensify, the emphasis is shifting toward lifecycle-safe chemicals with extremely low residual profiles, compatibility with automated UPW skids, and global environmental certifications. Market leaders are differentiating not only through formulation purity and reactivity but also through compliance with ultra-high-purity standards, real-time monitoring integration, and low-adsorption packaging. In the current zero-failure environments, chemical treatment is central to operational integrity, yield protection, and long-term sustainability.

Market Dynamics: Water Treatment Chemicals Market in Data Centers and Electronics Manufacturing

Market Trend: Ultra-High-Purity (UHP) Water Treatment Surges with Advanced Chip Fabrication and AI Cooling Loads

The water treatment chemicals market in data centers and electronics manufacturing is undergoing a rapid transformation, fueled by the increasing purity requirements of next-generation semiconductor fabs and the thermal management needs of AI-driven data centers. As foundries push into the 2nm and sub-2nm chip nodes, the threshold for water contaminants has tightened from parts-per-billion (ppb) to parts-per-trillion (ppt), rendering conventional chemicals obsolete. Advanced fabs operated by TSMC, Intel, and Samsung are demanding SEMI Grade water treatment chemicals ion exchange resins, antiscalants, and oxidants with ultra-low metal impurities, low TOC, and zero particulate shedding. These requirements are reshaping supplier portfolios, with companies like BASF, Entegris, and Solvay introducing high-purity resins, low-foam dispersants, and catalytic oxidants specifically engineered for semiconductor-grade UHP systems. Parallelly, hyperscale data centers are experiencing exponential growth in liquid-based cooling systems. With cooling water coming into direct contact with heat exchangers or dielectric fluids, even trace biofilm formation or silica scaling can cause thermal inefficiencies and hardware failures. To combat this, new classes of low-silica, non-phosphonate antiscalants and biofilm-suppressive oxidants are being developed for critical loop operations. Moreover, regulatory tightening adds urgency: the EU’s revised WEEE Directive (2025) and China’s new electronics wastewater mandates are driving the market toward chelating agents and scavengers with extreme selectivity and minimal residue. In an industry where a single waterborne defect can wipe out $50,000 worth of wafers, water treatment chemistry is a strategic differentiator for both chipmakers and cooling-centric digital infrastructure.

Market Opportunity: Lithium and Metal Scrubber Chemistries for AI-Cooled Data Centers

As the global shift to direct-to-chip and immersive liquid cooling accelerates in hyperscale data centers, a new wastewater challenge is emerging: lithium-ion battery–derived contaminants from advanced cooling systems. Next-generation AI servers are increasingly cooled with dielectric fluids that interact with lithium-based battery backup and UPS systems, leading to the accumulation of LiPF₆, nano-cobalt, and PFAS analogs in condensate blowdown and wastewater discharge streams. Traditional water treatment trains optimized for silica, phosphate, or bacterial control are ill-equipped to handle these ionic residues. This gap has created a high-value opportunity for specialty water chemistries: selective lithium and cobalt ion-exchange resins, originally engineered for lithium mining, are being adapted by innovators like DuPont and Solvay for data center water loops. The economic case is compelling: with lithium prices surging due to battery supply chain constraints, recovery solutions could recoup $8–12/m³ in value while simultaneously ensuring environmental compliance. Beyond lithium, these same resin beds and scrubbers can be cross-configured to capture cobalt, nickel, boron, and fluorinated byproducts particularly relevant for electronics plants performing PCB etching or EV inverter assembly. Furthermore, modular, containerized scrubber units are gaining favor in colocation and edge data centers where footprint, automation, and remote monitoring are paramount. For chemical suppliers and technology integrators, this marks an untapped niche where next-gen metals recovery, AOP-integrated PFAS destruction, and smart chemical dosing converge to define the future of data water stewardship.

Competitive Landscape: Water Treatment Chemicals Market in Data Centers and Electronics Manufacturing

The water treatment chemicals market for data centers and electronics manufacturing features specialized, ultra-pure solutions designed for mission-critical environments. Leading companies operate at the intersection of regulatory compliance, process precision, and sustainability. Their chemical portfolios meet the specific needs of cooling systems, ultrapure water (UPW) generation, and wastewater treatment in semiconductor fabs and hyperscale data centers.

In the data center segment, treating cooling water is a key focus. Innovations aim to reduce corrosion, scaling, and microbial contamination in both traditional and next-generation thermal management systems. Companies like Ecolab and Solenis emphasize non-phosphorus and biodegradable biocidal solutions. They adhere to UL ECOLOGO® and NSF/ANSI standards to meet environmental expectations of large hyperscale operators. Solenis has validated its Purate™ Free and HyperSperse™ programs in AWS and Azure facilities. Ecolab’s 3D TRASAR™ system has also seen wide adoption, with over 500 active data center deployments worldwide. At the same time, companies like Dow and Xylem, using FilmTec™ RO membranes and Ionpure™ CEDI systems, provide crucial membrane-based water purification and continuous deionization for closed-loop cooling and reuse systems.

In semiconductor and electronics manufacturing, chemical suppliers work to achieve UPW purity at sub-ppb levels while adjusting to next-generation fabrication nodes (5nm/3nm and below). Kurita and Veolia are major players in this market. Kurita offers its KRW-8000 series and TraceGuard™ scavengers, which ensure metal content below 0.1 ppb. Veolia provides SEMI-certified Hydrex™ 9500 chemicals and PFAS-free formulations to comply with new EU and California regulations. Kurita’s innovation in nanobubble rinse water recovery improves yield in advanced wafer processing. Meanwhile, BASF and The Dow Chemical Company focus on high-purity formulations and resin technologies to meet the cleanroom and lithography needs of EUV fabs. Their patented low-fluoride and recyclable chemistries promote circularity and environmental compliance.

The competitive landscape also reflects regional strategies. Ion Exchange (India) has become a leader in India's expanding semiconductor and electronics sectors, supplying INDION™ UPW resins and ZeroBrine™ ZLD systems. These are tailored for high-silica, tropical climates. Kemira, known for its Purity™ coagulants, emphasizes zero-liquid discharge readiness and fluoride removal in East Asian fabs. These regional companies play important roles in national self-reliance initiatives like “China+1” and “Make in India.” They are supported by ISO 14046 and TUV SUD certifications that validate their water stewardship claims.

Water Treatment Chemicals Market in Data Centers and Electronics Manufacturing – Segmentation Insights (2025–2034)

By Type of Chemical: Corrosion Inhibitors Dominate While Biocides Grow Fastest

Corrosion inhibitors hold the largest share in the water treatment chemicals market for data centers and electronics manufacturing, comprising approximately 29.3% of total market demand in 2025. Their dominance is driven by the need to protect sensitive cooling system components particularly copper and aluminum from corrosion in closed-loop and open-loop systems. These inhibitors are critical for maintaining the integrity and efficiency of heat exchangers, pipes, and server cooling infrastructure, especially in mission-critical environments where equipment downtime is unacceptable. Scale inhibitors follow closely, seeing strong demand as high-efficiency heat transfer and flow stability are essential in both traditional and next-gen liquid cooling systems. Meanwhile, biocides and disinfectants are the fastest-growing chemical category, projected to grow at a 12.3% CAGR through 2034. The heightened focus on microbial control particularly in evaporative cooling towers where legionella risk is elevated is pushing adoption of advanced oxidizing and non-oxidizing biocides tailored for electronics-grade water systems. Dispersants are also gaining momentum for their role in keeping particulate matter and biofilm precursors in suspension, especially in systems where ultra-clean water is essential. pH adjusters and filter aids continue to support pre-treatment and conditioning processes, ensuring compatibility with sensitive downstream components.

By Application: Cooling Tower Systems Lead While Direct Liquid Cooling Grows Fastest

Cooling tower water treatment is the leading application segment, representing approximately 37.8% of market share in 2025. These systems, widely used in both large-scale data centers and electronics manufacturing facilities, require consistent chemical treatment to control microbial growth, scale deposition, and corrosion in high-volume recirculating water systems. As data centers scale up their cooling infrastructure to support power-dense servers, cooling towers remain central to facility operations. However, direct liquid cooling (DLC) systems are emerging as the fastest-growing application, projected to expand at a 12.9% CAGR through 2034. This growth is being driven by the adoption of immersion and cold plate cooling technologies in AI and high-performance computing (HPC) data centers, where precise temperature control and water purity are critical. DLC systems require highly specialized chemical formulations that maintain thermal fluid quality and prevent scaling within microchannel surfaces. Closed-loop and chilled water systems also contribute significantly to chemical demand, particularly for long-life corrosion inhibitors and low-residue dispersants that support uptime and thermal stability. Make-up water pre-treatment and wastewater treatment remain support functions, with the former ensuring feedwater quality and the latter addressing compliance and sustainability goals in high-throughput manufacturing environments.

.png)

South Korea: Semiconductor Investments Drive Demand for Ultrapure Water Chemicals

South Korea is a global leader in the semiconductor industry, creating massive demand for ultrapure water (UPW) treatment chemicals. The government’s K-Semiconductor Strategy and Semiconductor Powerhouse Strategy provide tax incentives up to 25% for investments and 50% for R&D, supporting infrastructure like advanced water supply systems in major hubs such as Pyeongtaek and Yongin. These initiatives ensure continuous growth for specialized water treatment chemicals, including membrane cleaners, corrosion inhibitors, and high-purity solvents critical for chip manufacturing.

UPW production is essential for electronics manufacturing, as thousands of gallons of water are required to clean a single silicon wafer. Technologies like Electrode Deionization (EDI) are gaining traction for UPW generation, further driving the demand for associated chemicals. The government’s push to strengthen domestic supply chains also emphasizes local production of water treatment chemicals and advanced dosing systems, ensuring the resilience of the industry’s infrastructure.

Taiwan: Sustainability and Metal Recovery Innovations in Electronics Wastewater Treatment

Taiwan’s dominance in semiconductors, PCB, and TFT-LCD manufacturing creates a complex wastewater challenge, leading to innovative use of water treatment chemicals for metal recovery and resource recycling. The industry is adopting advanced systems like electrowinning technology to extract copper and other metals from wastewater streams. Companies such as Waste Recovery Technology Inc. (WRT) have pioneered Build-Operate-Own (BOO) models, enabling manufacturers to adopt cutting-edge metal recovery solutions without heavy upfront investment.

Taiwan’s approach to water treatment is based on a cradle-to-cradle philosophy, where recovered metals are reintroduced into production processes, reducing waste and boosting circular economy goals. There is also a strong emphasis on low-carbon and energy-efficient water treatment chemicals, aligning with global sustainability standards and enhancing operational efficiency for electronics manufacturers.

China: Regulatory Push and Smart Dosing Systems Accelerate Market Growth

China’s water treatment chemicals market is booming, driven by the 14th Five-Year Plan and strict Zero Liquid Discharge (ZLD) policies targeting electronics and semiconductor industries. Rapid industrialization and water scarcity concerns necessitate advanced treatment solutions for both ultrapure water production and wastewater recycling.

Digital integration is a key trend, with companies adopting AI-powered dosing systems, IoT sensors, and real-time monitoring platforms to optimize chemical usage and maintain stringent purity levels. The rising demand for high-performance coagulants, flocculants, and corrosion inhibitors is amplified by the expansion of electronics clusters in Shanghai, Shenzhen, and the Greater Bay Area. Additionally, sustainability policies are encouraging the development of eco-friendly chemicals that minimize environmental impact and comply with China’s green manufacturing objectives.

United States: Federal Incentives and PFAS Abatement Shape Chemical Innovation

The U.S. market is witnessing accelerated growth in smart water treatment chemicals due to the CHIPS and Science Act, which incentivizes domestic semiconductor manufacturing and advanced water recycling. Semiconductor fabs require ultrapure water systems to maintain yield quality, driving demand for high-performance chemical formulations like precision cleaners, scale inhibitors, and membrane protectants.

A major regulatory focus is on emerging contaminants such as PFAS, commonly found in electronics manufacturing. Research initiatives led by the National Semiconductor Technology Center (NTSC) are prototyping PFAS removal technologies without disrupting sensitive manufacturing processes. Compliance with the EPA’s NPDES permits necessitates pretreatment using chemical precipitation, neutralization, and clarification processes, ensuring safe discharge. These stringent requirements and sustainability goals are pushing chemical manufacturers to develop innovative hybrid solutions that combine chemical and biological treatments for wastewater reuse.

Japan: Circular Economy and High-Purity Water Technologies Drive Innovation

Japan’s water treatment market is technologically advanced, with strong integration of eco-friendly chemicals, recycling solutions, and ultrapure water systems for electronics manufacturing. Companies like Oji Holdings provide tailored water treatment chemicals based on rigorous water quality assessments and lab-based process optimization.

Japan’s circular economy initiatives are fostering chemical solutions for water reuse and resource recovery, particularly in electronics sectors that require ultra-high-purity water. Leading firms are also developing functional polymers and advanced adhesives, indirectly increasing demand for specialized cleaning agents and corrosion inhibitors in water treatment. Additionally, membrane-based systems combined with precision chemical dosing are at the forefront of Japan’s approach to sustaining semiconductor and data center operations.

Singapore: Integrated Smart Water Systems and Sustainability Leadership

Singapore is positioning itself as a hub for smart water treatment technologies in the electronics sector. The Public Utilities Board (PUB) spearheads initiatives promoting integrated water management systems that combine chemical dosing with advanced oxidation and membrane technologies for ultrapure water production.

Global innovators like Gradiant provide turnkey solutions combining proprietary chemical formulations and IoT-based monitoring systems, enabling clients to reduce, reclaim, and renew water resources. Sustainability goals drive the adoption of biodegradable chemicals and energy-efficient processes, ensuring compliance with Singapore’s strict water management standards. The country’s strategic focus on water reuse and zero-discharge models further fuels demand for specialized treatment chemicals and smart dosing solutions in electronics and semiconductor manufacturing.

Germany: Digital Water Platforms and Green Chemicals for Industrial Applications

Germany’s market emphasizes green chemistry principles and digital integration in water treatment for data centers and electronics manufacturing. Compliance with the EU Water Framework Directive and the German Water Resources Act (WHG) drives adoption of smart dosing systems combined with eco-friendly coagulants, flocculants, and scale inhibitors.

Industry leaders like BASF and Solenis are innovating with biodegradable and high-efficiency chemical products, paired with AI-driven water treatment platforms that reduce chemical consumption and minimize waste. Data centers in Germany, which are significant water consumers, are increasingly adopting digital water optimization tools to monitor cooling water systems, ensure corrosion control, and reduce operational costs. Germany’s emphasis on sustainable water reuse strategies positions the country as a pioneer in the smart chemical dosing landscape.

Australia: Sustainability and Smart Monitoring in Data Center Water Management

Australia’s growing data center ecosystem and water scarcity challenges make it a critical market for smart water treatment chemicals. With the country’s commitment to sustainable water management, operators are adopting real-time monitoring systems and automated dosing controllers to optimize chemical usage for cooling systems while minimizing water wastage.

The focus on eco-friendly chemicals that prevent scaling and biofouling aligns with Australia’s environmental policies and water conservation efforts. Data centers are also integrating hybrid treatment solutions combining physical filtration, advanced oxidation, and chemical conditioning to meet high water quality standards. This convergence of digital dosing systems and green chemicals is reshaping the water treatment landscape in Australia, particularly in regions prone to drought.

Water Treatment Chemicals Market in Data Centers and Electronics Manufacturing Report Scope

Water Treatment Chemicals Market in Data Centers and Electronics Manufacturing

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.6 Billion

|

|

Market Size (2034)

|

$4 Billion

|

|

Market Growth Rate

|

10.8%

|

|

Segments

|

Data Center (By Type of Chemical, By Application, By Data Center Size/Type), Electronics Manufacturing (By Type of Chemical, By Application, By Manufacturing Segment)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ecolab Inc. (U.S.), Veolia Water Technologies (France), Kurita Water Industries Ltd. (Japan), Solenis LLC (U.S.), BASF SE (Germany), The Dow Chemical Company (U.S.), Xylem Inc. (U.S.), Kemira Oyj (Finland), ChemTreat, Inc. (U.S.), Ion Exchange (India) Ltd. (India),

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Water Treatment Chemicals Market in Data Centers and Electronics Manufacturing Market Segmentation

Data Center

By Type of Chemical

- Corrosion Inhibitors

- Scale Inhibitors

- Biocides and Disinfectants

- pH Adjusters

- Dispersants

- Filter Aids/Coagulants

By Application

- Cooling Tower Water Treatment

- Chilled Water Systems

- Closed-Loop Cooling Systems

- Evaporative Cooling Systems

- Direct Liquid Cooling Systems

- Make-up Water Pre-treatment

- Wastewater Treatment

By Data Center Size/Type

- Hyperscale Data Centers

- Colocation Data Centers

- Enterprise Data Centers

- Edge Data Centers

Electronics Manufacturing

By Type of Chemical

- Ion Exchange Resins

- Coagulants and Flocculants

- Membrane Cleaning Chemicals

- Antiscalants

- Biocides and Disinfectants

- Dechlorinators/Oxygen Scavengers

- pH Adjusters

- Specialty Chemicals for Wastewater Treatment

By Application

- Ultra-Pure Water (UPW) Generation

- Rinsing and Cleaning Processes

- Etching Processes

- Process Water Production

- Wastewater Treatment

- Sludge Treatment

By Manufacturing Segment

- Semiconductor Manufacturing

- Printed Circuit Board (PCB) Manufacturing

- Flat Panel Display (FPD) Manufacturing

- Solar Photovoltaic (PV) Manufacturing

- Other Electronic Component Manufacturing

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Water Treatment Chemicals Market in Data Centers and Electronics Manufacturing

- Ecolab Inc. (U.S.)

- Veolia Water Technologies (France)

- Kurita Water Industries Ltd. (Japan)

- Solenis LLC (U.S.)

- BASF SE (Germany)

- The Dow Chemical Company (U.S.)

- Xylem Inc. (U.S.)

- Kemira Oyj (Finland)

- ChemTreat, Inc. (U.S.)

- Ion Exchange (India) Ltd. (India)

* List Not Exhaustive

Research Coverage

This report provides a comprehensive analysis of the Water Treatment Chemicals Market in Data Centers and Electronics Manufacturing, focusing on high-purity chemical formulations and advanced dosing technologies essential for mission-critical operations. USDAnalytics highlights the integration of ultra-pure water (UPW) systems in semiconductor fabs, specialized corrosion inhibitors for liquid cooling loops, and emerging chemistries targeting PFAS and lithium-ion contaminants in hyperscale data centers. Coverage spans chemical categories such as corrosion inhibitors, scale inhibitors, biocides, antiscalants, and membrane cleaners tailored for both electronics manufacturing and large-scale data infrastructure. The report also evaluates innovations in smart dosing systems, regulatory frameworks impacting ZLD (Zero Liquid Discharge) adoption, and sustainability-driven chemical strategies.

Scope Highlights:

- Segmentation:

- Data Centers

- By Type of Chemical: Corrosion Inhibitors, Scale Inhibitors, Biocides and Disinfectants, pH Adjusters, Dispersants, Filter Aids/Coagulants

- By Application: Cooling Tower Water Treatment, Chilled Water Systems, Closed-Loop Cooling Systems, Evaporative Cooling Systems, Direct Liquid Cooling Systems, Make-up Water Pre-treatment, Wastewater Treatment

- By Data Center Size/Type: Hyperscale Data Centers, Colocation Data Centers, Enterprise Data Centers, Edge Data Centers

- Electronics Manufacturing

- By Type of Chemical: Ion Exchange Resins, Coagulants and Flocculants, Membrane Cleaning Chemicals, Antiscalants, Biocides, Dechlorinators/Oxygen Scavengers, pH Adjusters, Specialty Chemicals for Wastewater Treatment

- By Application: UPW Generation, Rinsing and Cleaning, Etching, Process Water Production, Wastewater Treatment, Sludge Treatment

- By Manufacturing Segment: Semiconductor Manufacturing, PCB Manufacturing, Flat Panel Display Manufacturing, Solar PV Manufacturing, Other Components

- Geographic Scope: Includes 25+ countries across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa.

- Companies Covered: Ecolab, Veolia, Kurita Water Industries, Solenis, BASF, Dow Chemical, Xylem, Kemira, ChemTreat, Ion Exchange India.

- Data Coverage: Historic data (2021–2024), forecast (2025–2034).

Methodology

The research methodology combines primary interviews with water treatment chemical suppliers, electronics manufacturing engineers, and data center facility operators, supported by secondary research from regulatory databases (SEMI Standards, EU Water Framework Directive, U.S. EPA), trade journals, and company financial reports. Market sizing and forecasts were developed using a bottom-up approach, aggregating segment-level demand from data centers and electronics manufacturing, validated through top-down triangulation against macroeconomic indicators and capex trends in semiconductor and hyperscale data infrastructure. Forecasting incorporates factors like ZLD adoption, IoT-driven dosing integration, and ESG compliance mandates, applying scenario-based sensitivity analysis to capture the impact of emerging regulations and AI-enabled dosing platforms on chemical consumption trends.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements