H₂S Scavengers in Oil & Gas Market Analysis: Growth Outlook and Forecast

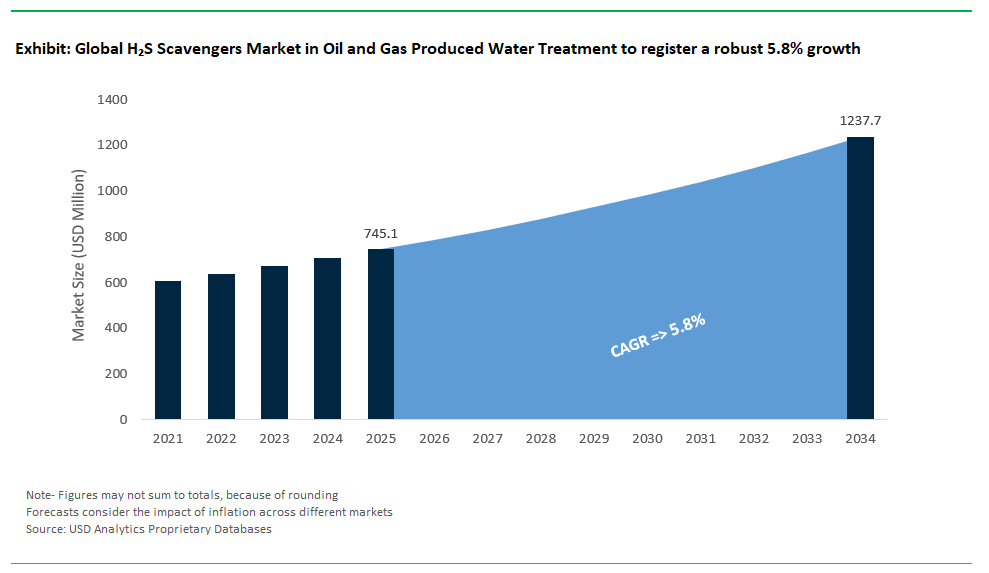

The Hydrogen Sulfide scavengers market in oil and gas operations is valued at $745.1 million in 2025 and projected to reach $1,237.6 million by 2034, registering a CAGR of 5.8%. This sector remains a technically demanding and economically sensitive domain, where performance, compatibility, and residue control are tightly scrutinized. Hydrogen sulfide (H₂S) not only poses severe toxicity and corrosion risks across upstream, midstream, and produced water systems but also threatens regulatory compliance and equipment lifespan.

Triazine-based scavengers, particularly hexahydro-1,3,5-tris(hydroxyethyl)-s-triazine (THEED), remain the dominant formulation due to their well-established reactivity and low capex requirements. At operational temperatures around 50°C, reaction kinetics are favorable, with typical application rates ranging from 100–300 ppm per ppm of H₂S, depending on residence time and brine composition (NACE SP21430-2023). However, residual monomeric byproducts such as formaldehyde and MEA derivatives must be managed carefully NORSOK M-001 compliance, for instance, caps these residues at <15 ppm to protect downstream metallurgy and meet discharge quality standards.

In response to regulatory tightening and the operational need for lower toxicity profiles, non-triazine scavengers such as metal carboxylates are gaining share. These alternatives offer rapid kinetics often reducing H₂S to <0.1 ppm within 5 minutes while retaining efficacy in hypersaline environments exceeding 250,000 ppm TDS, making them highly suitable for deepwater or produced water reinjection systems.

Key Trends and Emerging Opportunities in the H₂S Scavengers Market for Oil & Gas

Market Trend: Shift Toward Non-Toxic, Regenerable, and Smart H₂S Mitigation Solutions

The H₂S scavengers market in the oil & gas industry is undergoing a pivotal transformation driven by the convergence of environmental regulations, operational efficiency goals, and digital innovation. The 2024 enforcement of the U.S. EPA’s revised hazardous air pollutant (HAP) standards has accelerated a market-wide pivot toward non-toxic and biodegradable scavenging chemistries. Technologies using iron-based nanoparticles that can be electrochemically regenerated represent a major step toward circular, low-waste operations already showing 60% reductions in chemical consumption at scale in Permian Basin deployments. Complementing this green shift, Ecolab’s EnviroScav™ provides a bio-based alternative to triazine with zero formaldehyde byproducts, meeting both air quality and ESG compliance standards. In parallel, the digitalization of H₂S mitigation combines real-time H₂S sensors with AI-based dosing algorithms enables chemical savings in tight gas fields like Eagle Ford. Meanwhile, Chevron’s net-zero mandate for 2030, which includes a focus on reducing emissions from chemical treatments, reinforces long-term demand for these next-generation scavengers. As regulatory and investor scrutiny tighten, the market is quickly realigning around low-carbon, smart, and regenerable H₂S scavenging systems as the new industry standard.

Growth Opportunity: Offshore & Tight Gas Applications

The strongest growth potential for H₂S scavengers lies in offshore sour gas fields, tight gas basins, and carbon capture-linked operations, where traditional treatments struggle with cost, reliability, and emissions compliance. In deepwater operations, such as Shell’s Vito Floating Production Unit in the Gulf of Mexico, the deployment of non-emulsifying scavengers has proven critical in maintaining gas-liquid separator stability saving over $5 million annually in downtime and production losses. Similarly, in Brazil’s ultra-deep Búzios pre-salt field, high-pressure scavenger formulations enable production of sales gas with <1 ppm H₂S, a key requirement for pipeline-grade output. In shale plays, where gas is becoming increasingly sour, operators like EQT are deploying nanoparticle-based scavengers at the wellhead, eliminating the need for centralized sweetening infrastructure. Additionally, the rise of carbon capture and storage (CCS) projects creates a new use case for integrated scavenging. The opportunity is further amplified by carbon credits, with bio-based scavengers qualifying for $10–$30/ton of CO₂e avoided under Verra and Gold Standard schemes. With an expected $500M+ market potential by 2030, driven by souring fields and sustainability mandates, the H₂S scavengers market is poised for strong growth through tailored, intelligent, and low-impact chemical solutions.

Competitive Landscape: H₂S Scavengers in Produced Water Treatment

As oil and gas operators face more environmental scrutiny and challenges in handling produced water, controlling hydrogen sulfide (H₂S) has become crucial within production chemistry strategies. The market for H₂S scavengers is shifting from traditional triazines to solutions that provide better safety, compatibility with reinjection systems, and cost-effective treatment in high-pressure, high-temperature (HPHT) and high-total dissolved solids (TDS) conditions.

Triazine Dominance and Evolution Toward Non-Triazine Formulations

- Triazine-based scavengers continue to be the standard for bulk H₂S removal, especially in onshore and offshore produced water and gas treatment operations. However, concerns about sludge formation, emulsion stability, and formaldehyde byproducts are pushing the development of non-triazine alternatives with better safety and environmental profiles.

- SLB (Schlumberger) and Baker Hughes have extensive H₂S scavenger portfolios, including triazines, aldehyde condensates, and metal-based products. SLB’s integration of the GasTreat and ScavConnect series into real-time monitored chemical programs such as IROPS™ allows for dose optimization and reduced byproduct formation. Both companies are investing in low-dosage, high-efficiency non-triazine products to decrease disposal costs.

- Clariant, Lubrizol, and Dorf Ketal remain strong in triazine formulations, but they are also moving toward hybrid or metal-organic options. Clariant focuses on zinc-based scavengers (Zetane™) that provide higher loading capacities to reduce waste volume while keeping treatment efficacy. Dorf Ketal works on optimizing cost and performance in Middle Eastern and Indian fields, adapting to high H₂S and saline conditions.

- Ecolab/Nalco Water is gaining popularity with its Focus™ SC series, which includes formaldehyde-free and low-toxicity aldehyde-based products. With a strong emphasis on health, safety, and environmental (HSE) practices and reinjection compatibility, Ecolab matches its offerings with operators’ sustainability goals and regulatory needs.

Metal-Based and Redox Scavenging for Long-Term or High-Capacity Operations

- While triazines are commonly used in wellhead and separator applications, metal-based and redox systems are preferred for continuous or large-volume H₂S treatment, especially in vapor and high-gas-content produced waters.

- Merichem Technologies offers LO-CAT® and SulfaTreat®, which enable efficient bulk removal through liquid redox and solid-bed sponge iron systems. These technologies are suitable for sour gas co-treatment and handling produced water vapor-phase, particularly where H₂S levels are high and continuous operations are essential.

- Q2 Technologies introduces a vapor-phase innovation with Q2 Treat™, designed to prevent top-of-line corrosion and address H₂S in tank vapor spaces, pipelines, and light hydrocarbons. Its focus on vapor-phase scavenging specifically targets corrosion and safety risks in storage and transport systems.

System-Level Integration and Modular Water Treatment Approaches

- Companies experienced in water treatment infrastructure are incorporating H₂S scavengers into modular, end-to-end solutions. These systems often combine scavengers with filtration, deoxygenation, and chemical conditioning.

- Veolia Water Technologies and Solutions uses its expertise in produced water system design to dose scavengers alongside membrane or thermal treatment units. This is particularly effective in offshore and large-scale onshore facilities where H₂S post-primary polishing is necessary before discharge or reinjection.

- Genesis Water Technologies, while not specifically listed, follows this systems-driven approach in other settings. This trend involves pairing scavengers with advanced separation and recovery technologies.

Amine and Aldehyde Chemistry for Multiphase and Gas-Focused Operations

- For producers working across gas-liquid interfaces or in multiphase environments, amine-based scavengers are essential, especially for gas sweetening and liquid hydrocarbon treatment.

- Dow provides Ucarsol™ and Glytron™ scavengers that utilize MEA, DEA, and MDEA chemistry. With deep expertise in gas processing, Dow keeps improving its amine formulations to reduce foaming, lower corrosion risk, and enhance phase compatibility.

- BASF, through its SulfaScav® range, balances triazine and non-triazine formulations while focusing on stability in high TDS and hardness environments. Product development here aligns with the realities of the field improving safety, storage, and performance across different chemistries.

Regional Players Tailoring for Local Conditions and Regulations

- Smaller or regionally focused companies are meeting specific geographic needs by offering cost-effective, compliant, and temperature-adapted scavengers.

- Vink Chemicals serves European and North African markets with triazine-based scavengers that have improved biodegradability. Their expertise in low-temperature formulations helps meet regulatory and operational demands in the North Sea and Mediterranean.

- Dorf Ketal, with its strong regional presence in India and the Middle East, customizes its SCAVET™ series to fit the salinity, H₂S concentration, and infrastructure limitations in these markets. It provides both triazine and non-triazine options, emphasizing affordability and effective chemical logistics.

Hydrogen Sulfide (H₂S) Scavengers Market in Oil & Gas Produced Water Treatment– Segmentation Insights (2025–2034)

By Type of H₂S Scavenger: Non-Regenerative Leads, Regenerative Gains with Sustainability Focus

In 2025, non-regenerative scavengers are projected to hold a 73.2% market share, dominating the H₂S scavengers market in produced water treatment. Their widespread use is attributed to low capital requirements, ease of injection, and rapid deployment in upstream operations. Common types include triazine-based scavengers (e.g., MEA triazine), which react irreversibly with hydrogen sulfide to form stable byproducts. These are preferred in shale plays, marginal wells, and temporary production setups where speed and flexibility are prioritized over regeneration.

However, regenerative H₂S scavengers are emerging as the faster-growing segment, with a projected CAGR of 6.7% from 2025 to 2034. These include amine-based solutions, electrochemical scavenging units, and liquid redox systems that offer long-term operating cost savings and environmental compliance by minimizing chemical consumption and reducing waste volumes. Increasing demand for sustainable solutions and circular chemical reuse in EOR and water reinjection workflows is expected to drive their adoption, especially in large-scale offshore and Middle Eastern fields. Oil & gas operators are also turning to hybrid scavenger systems that integrate regenerative and non-regenerative chemistry, depending on the gas loading and water quality profile, aligning with broader ESG mandates and asset life-cycle optimization.

By Application Point: Treatment Facilities Dominate, Water Injection and Downhole Gain Ground

Produced water treatment facilities including separators, hydrocyclones, and centralized chemical treatment systems are expected to command the largest market share at 35.2% in 2025. These facilities are often the first point of H₂S removal before water discharge or reuse, driven by strict disposal regulations such as the U.S. EPA Effluent Limitation Guidelines (ELGs) and OSPAR standards in Europe. The widespread need to neutralize H₂S before reinjection or disposal underpins the dominance of this segment.

Water injection systems and downhole injection points are witnessing steady growth, with projected CAGRs of 7.1% and 6.5%, respectively. In regions such as the Permian Basin and North Sea, injecting scavengers downhole prevents souring of the reservoir and protects the integrity of casing and tubing. Water injection setups, especially those treating partially treated or recycled produced water, require scavenging to avoid scaling and microbial activity in the reservoir. Storage tanks and pipelines also utilize H₂S scavengers to ensure safe handling of sour fluids and prevent vapor release. Though sludge and solids treatment currently hold a smaller share, growing attention to tail-end waste remediation and chemical residual management is expected to bolster growth.

Scavengers Market in Oil & Gas Produced Water Treatment By Application Point (2025).png)

United States: Regulatory Pressure and Innovation in Biodegradable H2S Scavenger Solutions

The U.S. market is a global leader in hydrogen sulfide scavengers for oil and gas produced water treatment, driven by strict federal and state regulations and strong technological innovation. The U.S. Environmental Protection Agency (EPA) and Bureau of Ocean Energy Management (BOEM) require operators to mitigate H₂S risks to protect workers, infrastructure, and the environment. Compliance with the Clean Water Act and other mandates fuels demand for advanced scavenger chemicals in both offshore and onshore operations.

A major trend in the U.S. is the shift from traditional triazine-based scavengers to non-triazine, environmentally friendly alternatives. These new formulations reduce solids deposition and equipment fouling, improving operational efficiency. Companies like Streamline Innovations are pioneering biodegradable solutions that treat dissolved sulfides with scalable, cost-effective dosing systems. Additionally, biological treatments are gaining momentum, with firms such as Q2 Technologies introducing bio-nutrient systems that disrupt sulfate-reducing bacteria (SRB) activity, thereby preventing H₂S generation at the source. The growing focus on produced water reuse for hydraulic fracturing and enhanced oil recovery further accelerates the demand for high-performance scavenger technologies in the U.S.

Saudi Arabia: High Sour Gas Volumes and Vision 2030 Drive Sustainable H₂S Scavenger Adoption

Saudi Arabia remains a critical market for hydrogen sulfide scavengers due to its large-scale oil and gas production, particularly from sour crude and gas fields with high H₂S concentrations. Saudi Aramco’s extensive upstream and midstream infrastructure relies heavily on scavenger technologies to prevent pipeline corrosion and safeguard personnel in hazardous operating conditions. The country’s energy sector is also prioritizing water injection for enhanced oil recovery, creating significant demand for scavenger solutions that control SRB-related H₂S formation in injection water.

Under the Vision 2030 framework, Saudi Arabia is advancing sustainability goals, prompting oilfield chemical providers to develop biodegradable and non-toxic scavengers. These innovations not only ensure compliance with environmental regulations but also reduce operational risks and maintenance costs. With megaprojects in offshore and onshore fields, the Saudi market continues to set the benchmark for large-scale deployment of advanced H₂S scavenger solutions.

China: Policy-Driven Growth and Hybrid Scavenger Technologies

China is rapidly emerging as a major market for hydrogen sulfide scavengers, supported by national initiatives such as the “War on Pollution” campaign, which enforces stringent industrial wastewater discharge standards. This regulatory shift compels oil and gas operators to adopt high-efficiency H₂S removal chemicals to treat produced water before discharge or reuse.

Chinese companies and research institutions are actively developing cost-effective, eco-friendly scavenger formulations, including GLDA-based and other plant-derived chemistries. Additionally, hybrid treatment technologies combining chemical scavenging with membrane filtration and biological remediation are gaining traction for large-scale operations. The ongoing expansion of sour gas fields to meet domestic energy demand is another growth driver, as natural gas projects require reliable scavenger systems to maintain water quality and infrastructure integrity.

Brazil: Offshore Pre-Salt Production and Real-Time Scavenger Dosing

Brazil’s H₂S scavenger market is expanding in tandem with its booming offshore oil and gas sector, particularly in the pre-salt basin, where high-pressure reservoirs produce large volumes of sour water. Compliance with the new national sanitation and environmental frameworks has intensified the adoption of advanced produced water treatment technologies, including efficient H₂S scavengers.

State-owned Petrobras is spearheading investments in real-time monitoring and automated dosing systems that optimize scavenger application, reducing chemical waste and operational costs. The shift toward environmentally friendly scavengers aligns with Brazil’s sustainability targets, making the market favorable for companies offering low-toxicity, high-performance products. These advancements are critical for deepwater projects, where operational reliability and corrosion control are paramount.

Norway: Stringent Offshore Regulations Fuel Demand for Low-Toxicity Scavengers

Norway is a highly regulated market for oil and gas chemicals, with the Norwegian Petroleum Directorate (NPD) enforcing some of the strictest environmental and safety standards globally. These regulations drive demand for biodegradable, non-triazine H₂S scavengers suitable for offshore platforms, where equipment fouling and environmental discharge compliance are critical concerns.

Leading service providers are introducing next-generation scavengers that reduce solids formation and improve system efficiency. Additionally, Norway’s leadership in subsea processing and enhanced oil recovery amplifies the need for scavenger formulations capable of operating under extreme conditions while minimizing environmental risks. This sustainability-driven approach positions Norway as a model for green chemistry adoption in offshore oil operations.

India: Expanding Domestic Production and Cost-Effective H₂S Treatment Solutions

India’s hydrogen sulfide scavenger market is growing rapidly as the country ramps up domestic oil and gas production to reduce import dependency. National oil companies like ONGC are prioritizing produced water management, creating strong demand for cost-effective and high-performance scavenger solutions.

Emerging technologies include bio-based scavengers and bioremediation agents designed to degrade H₂S and related contaminants, offering a sustainable alternative for onshore fields and aging infrastructure. These solutions are particularly valuable for land reuse projects in agricultural zones, where treated produced water can be repurposed safely. Coupled with government initiatives promoting water conservation and environmental compliance, India represents a significant growth opportunity for innovative H₂S scavenger suppliers.

United Kingdom: Energy Transition and Offshore Water Management Drive Scavenger Use

The UK oil and gas sector, primarily in the North Sea, is upgrading its water treatment capabilities in line with net-zero emissions goals and stricter environmental policies. Operators are deploying high-efficiency, low-toxicity H₂S scavengers to enhance produced water quality and minimize the environmental impact of offshore discharges.

Recent developments include the integration of digital monitoring systems for real-time scavenger dosing, improving process control and reducing chemical consumption. The UK market is also exploring green alternatives to triazine-based scavengers to align with sustainability mandates. With growing pressure from both regulators and environmental groups, companies operating in the UK are accelerating their shift toward eco-friendly, performance-driven water treatment chemicals.

Australia: Environmental Protection and Offshore Project Growth Propel Market Expansion

Australia’s hydrogen sulfide scavenger market is expanding due to the country’s offshore oil and gas development and its stringent environmental regulations for produced water discharge. Operators in the Browse Basin and Northwest Shelf are implementing advanced scavenger technologies to meet compliance standards while reducing environmental risks.

There is a strong focus on automation and smart chemical dosing systems, which optimize scavenger application and enhance safety in offshore environments. The country’s push for sustainable oilfield operations and its commitment to protecting marine ecosystems are prompting companies to adopt biodegradable scavenger solutions over conventional chemicals. As offshore projects increase in scale, demand for advanced, environmentally friendly scavenger systems is set to accelerate.

Hydrogen Sulfide Scavengers Market in Oil and Gas Produced Water Treatment Report Scope

Hydrogen Sulfide Scavengers Market in Oil and Gas Produced Water Treatment

|

Parameter

|

Details

|

|

Market Size (2025)

|

$745.1 Million

|

|

Market Size (2034)

|

$1237.6 Million

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Type of H2S Scavenger (Non-Regenerative Scavengers, Regenerative Scavengers), By Physical Form/Solubility (Water-soluble Scavengers, Oil-soluble Scavengers, Solid Scavengers), By Application Point/System (Downhole Injection, Produced Water Separators/Treatment Facilities, Water Injection Systems, Storage Tanks and Vessels, Pipelines, Sludge and Solids Treatment), By End-User (Upstream, Midstream, Downstream

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

SLB (Schlumberger Limited) (U.S.), Baker Hughes Company (U.S.), Ecolab Inc. (U.S.), Veolia Water Technologies and Solutions (France), BASF SE (Germany), The Dow Chemical Company (U.S.), Clariant AG (Switzerland), The Lubrizol Corporation (U.S.), Dorf Ketal Chemicals I Pvt. Ltd. (India), Merichem Technologies (U.S.), Vink Chemicals GmbH and Co. KG (Germany), Q2 Technologies (U.S.),

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Hydrogen Sulfide Scavengers in Oil & Gas Produced Water Treatment Market Segmentation

By Type of H2S Scavenger

- Non-Regenerative Scavengers

- Regenerative Scavengers

By Physical Form/Solubility

- Water-soluble Scavengers

- Oil-soluble Scavengers

- Solid Scavengers

By Application Point/System

- Downhole Injection

- Produced Water Separators/Treatment Facilities

- Water Injection Systems

- Storage Tanks and Vessels

- Pipelines

- Sludge and Solids Treatment

By End-User

- Upstream

- Onshore Oil and Gas Fields

- Offshore Oil and Gas Platforms

- Shale Gas and Tight Oil Operations

- Midstream

- Downstream

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Hydrogen Sulfide Scavengers Market in Oil and Gas Produced Water Treatment

- SLB (Schlumberger Limited) (U.S.)

- Baker Hughes Company (U.S.)

- Ecolab Inc. (U.S.)

- Veolia Water Technologies and Solutions (France)

- BASF SE (Germany)

- The Dow Chemical Company (U.S.)

- Clariant AG (Switzerland)

- The Lubrizol Corporation (U.S.)

- Dorf Ketal Chemicals I Pvt. Ltd. (India)

- Merichem Technologies (U.S.)

- Vink Chemicals GmbH and Co. KG (Germany)

- Q2 Technologies (U.S.)

* List Not Exhaustive

Research Coverage

This report investigates the Hydrogen Sulfide (H₂S) Scavengers Market in Oil and Gas Produced Water Treatment, providing an in-depth analysis of market dynamics, chemical innovations, and emerging regulatory trends. USDAnalytics delivers comprehensive insights into both triazine-based and next-generation non-triazine formulations, highlighting their application in upstream, midstream, and offshore systems. The report reviews breakthroughs in low-toxicity and regenerative scavenger technologies, examines integration with smart chemical dosing, and evaluates market opportunities across geographies. This analysis is an essential resource for industry professionals seeking to align operational efficiency with environmental compliance in the evolving oilfield water treatment landscape.

Scope Highlights:

- Segmentation:

- By Type of H₂S Scavenger: Non-Regenerative Scavengers, Regenerative Scavengers

- By Physical Form/Solubility: Water-soluble Scavengers, Oil-soluble Scavengers, Solid Scavengers

- By Application Point/System: Downhole Injection, Produced Water Separators/Treatment Facilities, Water Injection Systems, Storage Tanks and Vessels, Pipelines, Sludge and Solids Treatment

- By End-User: Upstream (Onshore Oil and Gas Fields, Offshore Oil and Gas Platforms, Shale Gas and Tight Oil Operations), Midstream, Downstream

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Data Coverage: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies Covered: SLB (Schlumberger), Baker Hughes, Ecolab, Veolia Water Technologies and Solutions, BASF SE, Dow Chemical Company, Clariant AG, Lubrizol Corporation, Dorf Ketal, Merichem Technologies, Vink Chemicals, Q2 Technologies.

Methodology

USDAnalytics applies a rigorous research methodology combining primary interviews with oilfield chemical experts, produced water treatment engineers, and procurement managers, along with extensive secondary research from NACE, API, and industry publications. Market estimates are derived using top-down and bottom-up approaches validated through data triangulation. Scenario-based forecasting incorporates variables such as sour gas development, offshore project pipelines, regulatory shifts, and adoption of regenerative scavenger systems, ensuring reliable projections for 2025–2034.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements