Bioremediation Agents in Industrial Wastewater Treatment Market Analysis: Growth Overview and Forecast to 2034

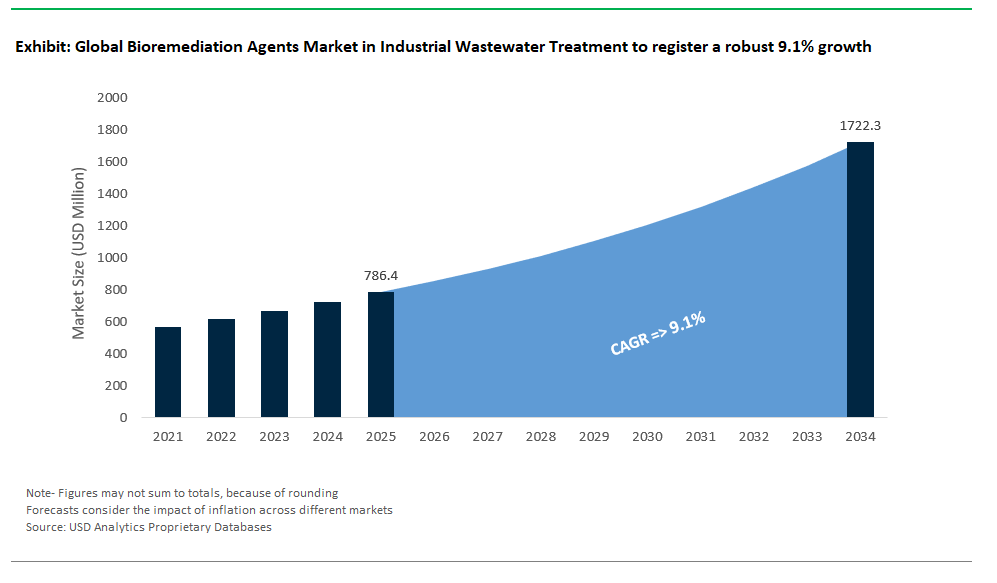

The bioremediation agents market for industrial wastewater is valued at $786.4 million in 2025 and projected to reach $1,722.1 million by 2034, with a CAGR of 9.1%. The market is advancing rapidly as industries confront rising costs and tightening regulations associated with physicochemical treatment methods. Biologically mediated solutions ranging from live microbial cultures to enzymatic additives and biosorbents are being increasingly deployed to tackle persistent organics, nutrient loads, and heavy metals across a wide spectrum of industrial effluents. Bioaugmentation with nitrifying bacteria is a common strategy for ammonia management in industries with nitrogen-rich waste streams. These cultures, typically comprising Nitrosomonas and Nitrobacter species, achieve ammonium removal rates of 0.5–2.0 g/m³/h at temperatures between 10–30°C, aligning with operational envelopes of aeration basins and moving bed biofilm reactors (WEF MOP OM-9).

For oxidative degradation of phenolic and other aromatic pollutants, enzymatic agents particularly fungal laccases have gained traction for their high catalytic turnover rates, enabling selective degradation under mild process conditions without generating secondary sludge (Bioresour. Technol.). In denitrification applications, especially post-nitrification zones or anoxic polishing reactors, glycerol-based electron donors offer precise stoichiometric control. At C/N ratios of 2.0–3.0, these carbon supplements enable over 90% nitrate removal within hydraulic retention times of 4–8 hours, offering a safer and more controllable alternative to methanol or acetate (Water Sci. Tech.).

Addressing the inorganic load, particularly toxic metals like lead, is another frontier where biosorption using non-viable fungal biomass (e.g., Aspergillus spp.) is demonstrating commercial viability. These biosorbents exhibit adsorption capacities of 50–150 mg Pb/g under mildly acidic conditions (pH ~5), making them suitable for pre-polishing or tertiary metal removal stages (J. Hazard. Mater.). As the bioremediation market matures, the emphasis is shifting toward agent stability, metabolic robustness under industrial toxicity profiles, and compatibility with existing treatment infrastructure. Vendors offering strain optimization, enzyme immobilization, and integrated dosing systems are expected to lead in a market increasingly defined by biological precision and cost-to-removal efficiency.

Engineered Bioremediation Agents and Sector-Specific Growth Opportunities in Industrial Wastewater Treatment

Market Trend: Bioaugmentation with Engineered Microbes for Complex Contaminants

The industrial wastewater sector is rapidly shifting toward bioremediation agents, especially engineered microbial consortia, as industries face intensifying regulation and rising costs for conventional treatment methods. In 2024, the introduction of Novozymes’ EnviroFix PF, a genetically modified Pseudomonas strain capable of degrading PFOA and PFOS up to 100 times faster than natural microbes, marked a significant leap in PFAS treatment technology. Piloted at 3M’s Cottage Grove site, it showed real-world effectiveness in handling recalcitrant contaminants. Complementing this innovation, the EPA’s fast-track permitting pathway for genetically engineered microbes under Superfund programs reduces regulatory delays to just six months accelerating adoption in highly contaminated sites. In heavy metal remediation, LanzaTech’s MetalRex, an algae-yeast hybrid, has demonstrated 95% removal of cadmium and arsenic while generating bioethanol a true circular solution deployed in Chilean copper mining operations. Globally, regulatory bodies such as the EU’s 2024 Industrial Emissions Directive require biological treatment for certain classes of priority pollutants, further validating microbial solutions. The economic case is equally compelling: bioaugmentation can reduce treatment costs by 40–60%, according to U.S. Department of Energy case studies. Moreover, recovered metals like cobalt and nickel from biologically treated biomass can command resale values exceeding $30,000/tonne, converting liabilities into revenue. As environmental liabilities and sustainability pressures converge, engineered bioremediation agents are becoming essential in treating contaminants that chemicals alone cannot address offering a potent combination of compliance, circularity, and cost-efficiency.

Growth Opportunity: Petrochemical & Textile Wastewater Biotreatment

The bioremediation agents market is poised for rapid expansion in Petrochemical & Textile Wastewater sectors where legacy pollutants such as hydrocarbons, synthetic dyes, and pharmaceutical residues are prevalent particularly in petrochemical refining and textile manufacturing. In refinery sludge management, Shell’s BioClean+, a microbial consortium that degrades diesel-range hydrocarbons, is converting over 10,000 tons/year of oily sludge into biogas at a pilot site in Singapore. This not only reduces hazardous waste but generates carbon credits BP’s bioremediation-based offsets are earning $25/ton CO₂-equivalent. In the textile sector, dominated by water-intensive dyeing operations, Archroma’s EcoFix B, a fungal-bacterial blend, has enabled fivefold faster decolorization of azo dyes compared to traditional UV/H₂O₂ treatment. Adopted by Bangladesh’s DBL Group, this bio-solution is gaining traction as global brands like Levi’s enforce ZDHC-mandated biological dye removal by 2025. The pharmaceutical industry, facing growing scrutiny over antibiotic resistance genes (ARGs) in effluents, is also turning to bioremediation. Merck’s BioARG-X, a CRISPR-edited strain, effectively eliminates tetracycline-resistance markers in Indian pharma discharges, a critical milestone backed by WHO’s AMR fund. First movers in this space enjoy competitive advantages across IP and finance. BASF’s BioSorb™ platform with patents on metal-binding algae has become a licensing engine for circular remediation. Furthermore, successful remediation projects are qualifying for ESG-linked bonds, such as Chevron’s $300 million issuance for bioremediated Superfund zones. With rising investor scrutiny, green bond access, and decarbonization-linked supplier mandates, bioremediation is no longer niche it’s core to future-proof industrial water treatment strategies.

Competitive Landscape: Bioremediation Agents in Industrial Wastewater Treatment

The industrial bioremediation market for wastewater treatment is evolving into a specialized segment. Bioaugmentation, enzymatic systems, and biological carriers are key tools for managing complex waste streams. The competitive environment focuses on integrating microbial groups with digital control systems. Companies must provide cost-effective solutions in difficult industrial settings and keep up with changing environmental regulations, especially regarding nutrients, organics, and new contaminants like PFAS precursors and pharmaceuticals.

Global leaders like Ecolab and Veolia represent the high end of the market with well-integrated solutions. Ecolab’s Nalco Water division uses biological agents, including microbial blends and enzyme-nutrient systems, within its TRASAR™ digital platform. This setup allows for continuous improvement across industries like food and beverage, pulp and paper, and light industrial processing. The company is also investing in next-generation biologics aimed at breaking down hard-to-degrade compounds, utilizing data-driven feedback loops and targeted group designs.

Veolia, on the other hand, focuses on biological treatment technologies such as Biostyr™, Biothelys®, and AnoxKaldnes™ MBBR systems. These are paired with proprietary bioaugmentation cultures that enhance nitrification, break down FOG, and stabilize biological loads under changing influent conditions. Veolia’s solutions are especially effective in large-scale industrial or hybrid municipal-industrial environments, where anaerobic digestion and biogas recovery are significant benefits.

In the mid-tier and regionally focused landscape, companies like Kurita, Xylem (through Evoqua), and SUEZ offer strong process integration along with specialized microbial agents. Kurita’s KURIVER™ lineup is designed for nitrification, reducing BOD loads, and resisting system inhibition, particularly in high-tech manufacturing in Asia. Its use of bioagents with AI-based controls (Kurita Brain) shows the shift toward biology enhanced by automation. After merging, Xylem combined Evoqua’s BioMag® and BioPortz® portfolios with its digital monitoring tools and aeration systems, focusing on retrofit and upgrade projects in North America. SUEZ combines biological formulations (Biopur®, Biobed®) with anaerobic treatment and biogas-to-energy systems, especially in Europe’s food and chemical sectors.

Emerging companies in India, such as Organica Biotech and Team One Biotech, are gaining industrial market share with affordable microbial blends tailored for local waste streams in textiles, distilleries, and agro-processing. These companies excel at customizing solutions for smaller industrial units that lack advanced physical-chemical infrastructure. Team One also addresses more complex degradation issues like hydrocarbons, heavy metals, and dyes, often incorporating enzymes and biostimulants for better treatment near contaminated areas.

Innovation appears in niche specialists like Tidal Vision (using chitosan), Probiosphere (controlling odors and sludge with natural microbes), and Regenesis (anaerobically degrading chlorinated solvents). Regenesis is more recognized in the remediation space, but its electron donor and microbial systems have potential uses in industrial wastewater, particularly in pump-and-treat scenarios facing similar soil and groundwater issues. Likewise, Biorem primarily targets air pollution control with biofiltration but occasionally overlaps with wastewater treatment when dealing with volatilized organics that need pre-treatment or combined air-water solutions.

Overall, the competitive landscape is shifting toward resilient microbial systems that can handle shock loads, temperature changes, and chemical inhibitors. Successful companies not only provide effective consortia but also integrate them into advanced treatment processes and digital platforms, whether for small decentralized plants or large industrial sites. As regulatory oversight tightens and client environmental and social governance goals increase, biological agents are becoming essential elements of broader wastewater improvement strategies.

Bioremediation Agents Market in Industrial Wastewater Treatment – Segmentation Insights (2025–2034)

By Treatment Method: Bioaugmentation Leads While Fungal Remediation Grows Fastest

Bioaugmentation holds the largest market share in the bioremediation agents market for industrial wastewater treatment, accounting for approximately 34.1% in 2025. This method leverages specialized microbial consortia such as Pseudomonas, Bacillus, and Rhodococcus engineered or selected for their capacity to degrade specific industrial contaminants like hydrocarbons, phenols, and surfactants. Bioaugmentation is particularly valued for its adaptability across oil & gas, chemical, and pharmaceutical industries where effluents contain high loads of toxic compounds. In contrast, fungal remediation is the fastest-growing segment, projected to expand at a 10.9% CAGR through 2034. The exceptional enzymatic capabilities of ligninolytic fungi (e.g., Phanerochaete chrysosporium) in breaking down recalcitrant compounds such as dyes, active pharmaceutical ingredients (APIs), and endocrine disruptors are fueling its adoption, especially in textile and pharmaceutical wastewater applications. Bioreactors such as Moving Bed Biofilm Reactors (MBBRs) and Anaerobic Membrane Bioreactors (AnMBRs) are also gaining traction with a projected CAGR of 9.8%, driven by their efficiency in high-rate biological treatment and compact design. Biostimulation remains a critical strategy to enhance native microbial activity via nutrient or oxygen addition, while phytoremediation and land-based treatments continue to serve niche or supplemental roles in integrated remediation systems.

.png)

By End-User Industry: Oil & Gas Leads While Pharmaceutical Industry Grows Fastest

The oil & gas sector represents the largest end-user of bioremediation agents, contributing approximately 28.9% of market share in 2025. This leadership is fueled by the sector’s ongoing need to treat hydrocarbon-laden produced water and refinery wastewater, where bioaugmentation and bioreactor technologies are widely applied to reduce chemical oxygen demand (COD), total petroleum hydrocarbons (TPH), and aromatic compounds. However, the pharmaceutical industry is the fastest-growing segment, advancing at a 11.1% CAGR through 2034. Growing pressure to comply with emerging regulations including the EU Water Framework Directive’s Watch List for APIs and endocrine disruptors is pushing pharmaceutical manufacturers to integrate bioremediation strategies capable of degrading complex, low-concentration contaminants. The textile and dyeing industry is also showing rapid adoption, particularly of fungal remediation techniques to break down persistent azo dyes and aromatic sulfonates. The chemical and petrochemical sectors continue to invest in microbial solutions for toxic organics and nitrification, while pulp and paper facilities apply bio-based treatment to handle lignin, chlorinated compounds, and volatile organic residues. Mining and metallurgy facilities, though smaller in volume, increasingly utilize targeted bioleaching and biosorption approaches for heavy metals and cyanide remediation.

United States Leads Industrial Wastewater Bioremediation with Advanced Microbial Innovation

The United States remains a powerhouse in the global bioremediation agents market for industrial wastewater treatment, underpinned by rigorous regulation and a commitment to biotechnology advancement. The U.S. Environmental Protection Agency (EPA) enforces strict industrial discharge rules under the Clean Water Act, compelling industries to adopt next-generation bioremediation solutions capable of addressing persistent pollutants, including chlorinated solvents and heavy metals. American innovation is particularly evident in the development of genetically engineered microorganisms designed to degrade complex organic pollutants resistant to traditional biological methods.

A significant trend in the U.S. market is bioaugmentation, where specific microbial consortia are introduced to contaminated sites to accelerate the breakdown of challenging contaminants. The oil and gas industry is a major adopter, relying on bio-based agents to treat produced water and remediate spills. Companies are also investing in specialized bioremediation systems, including advanced bioreactors that optimize nutrient supply, aeration, and pH ensuring that microbial agents work at peak efficiency. The United States’ leadership in developing both microbes and supporting technologies makes it a primary destination for industrial bioremediation investment and innovation.

China Drives Growth in Bioremediation for Sustainable Industrial Wastewater Management

China’s bioremediation agents market is expanding at a rapid pace, fuelled by government policy, environmental imperatives, and research leadership. The Chinese government’s large-scale investment in upgrading wastewater treatment plants, as part of its environmental protection strategy, is generating robust demand for biological treatment solutions in a wide range of industries. Chinese researchers and companies are at the vanguard of bioremediation, developing solutions like biochar from agricultural waste to absorb industrial dyes demonstrating the synergy between bioremediation and material science.

China’s “War on Pollution” campaign targets emissions from sectors such as pharmaceuticals, textiles, and chemicals, driving the need for microbial agents that can degrade complex industrial contaminants. There is strong market momentum behind hybrid technologies, with plants employing membrane bioreactors (MBRs) that use custom microbes to treat effluents and recover energy as methane. The drive for innovation and sustainability is positioning China as a global hub for scalable, eco-friendly bioremediation in industrial wastewater treatment.

Germany Champions Mobile and Fungal Solutions in Bioremediation for Industrial Wastewater

Germany is setting the standard in sustainable water management with a strong focus on advanced bioremediation technologies. The market is shaped by the EU Water Framework Directive and Germany’s dedication to the circular economy, resulting in widespread adoption of environmentally sound treatment methods. German innovation includes mobile treatment plants equipped with bioremediation capabilities, offering a flexible response to high-contamination industrial sites. These mobile solutions are particularly effective for rapid deployment in areas with urgent remediation needs.

A notable development is the rise of “mycoremediation,” using fungi to break down a broad spectrum of industrial pollutants. This method complements the push for a “fourth purification stage” in sewage treatment plants, which specifically targets pharmaceuticals and emerging contaminants. Germany’s integrated approach combining policy, mobility, and cutting-edge biology continues to drive the bioremediation agents market forward as a model for Europe and beyond.

India Accelerates Industrial Bioremediation with Regulatory Innovation and Indigenous Microbes

India is emerging as a dynamic market for bioremediation agents in industrial wastewater, propelled by pioneering regulation and an emphasis on low-cost, indigenous solutions. The introduction of strict standards for antibiotic discharge from pharmaceutical factories by the Ministry of Environment, Forest and Climate Change (MoEF&CC) is a world first forcing the adoption of biological agents to degrade these persistent contaminants. The Central Pollution Control Board (CPCB) further mandates advanced treatment, including biological processes, across major industrial sectors.

Indian research institutions are leveraging local bacteria and fungi to tackle pollutants such as heavy metals and dyes in textile effluents, aligning cost-effectiveness with sustainability. A key trend is the application of microbial agents to detoxify and decolorize wastewater from the country’s extensive textile industry, making treated water suitable for reuse. With rapid growth in both regulatory oversight and R&D, India is well-positioned to lead in accessible, scalable bioremediation for complex industrial effluents.

Japan Integrates Bioremediation with Technological Sophistication for Industrial Wastewater

Japan’s market for bioremediation agents is distinguished by its focus on high-tech, innovative treatment solutions and water conservation. Japanese researchers are advancing the use of photocatalytic and microbial techniques to break down pollutants such as PFAS a growing concern in industrial waste. In high-tech industries like electronics and semiconductors, bioremediation is integral to achieving the ultra-pure water quality required for manufacturing, supplementing traditional physical and chemical purification methods.

Government policy supports the expansion of green technologies for both land and water applications, further encouraging the uptake of biological solutions in industrial and coastal remediation. Japanese companies and research centers are developing specialized microbial strains and treatment processes tailored to the unique challenges of industrial wastewater, solidifying Japan’s status as a leader in precision, sustainable water treatment.

Brazil Taps Bioremediation for Industrial Water Reuse and Sanitation Reform

Brazil’s industrial bioremediation agents market is gaining momentum, driven by a new national sanitation framework and the need for cost-effective, sustainable wastewater solutions. The focus on universal sanitation has sparked a wave of infrastructure investment, especially in private sector wastewater treatment. Brazilian researchers are exploring combined bioremediation methods to target veterinary antibiotics and other persistent contaminants in industrial effluents.

The agricultural and industrial sectors offer a robust local supply of biomass for bio-based agent production, providing economic and environmental advantages. The oil and gas industry is a significant user, relying on bioremediation to manage produced water and meet stricter environmental standards. As Brazil continues to modernize its water management systems, bioremediation agents are becoming a central component of strategies for water reuse and pollution control.

United Kingdom Advances Bioremediation with Policy Support and Focus on Micropollutants

The United Kingdom is rapidly modernizing its industrial wastewater treatment sector in response to ambitious environmental policies and rising public scrutiny. The “Plan for Water” and the Environment Act 2021 have set higher benchmarks for pollution reduction and water company accountability, fueling investment in bioremediation agents to meet new compliance targets. UK researchers and companies are actively pursuing the use of biological agents to tackle micropollutants and other emerging contaminants in both municipal and industrial water streams.

There is also growing market interest in using bioremediation and biodegradable additives to reduce sludge volume and toxicity key to improving the environmental impact of treatment processes. With ongoing government funding and research support, the UK is poised to increase adoption of innovative bioremediation solutions across the industrial landscape.

South Korea Forges Ahead in Automated, High-Tech Bioremediation for Industrial Effluents

South Korea’s market for bioremediation agents is driven by rapid industrialization, advanced automation, and a strong focus on water reuse and smart infrastructure. Major manufacturing, chemical, and electronics sectors are embracing biological treatment to meet high regulatory and sustainability standards. South Korea’s investments in water reuse and desalination projects hinge on robust pre-treatment with advanced bioremediation agents.

Automation and smart controls are hallmarks of Korean wastewater treatment plants, enabling real-time monitoring and data-driven optimization of microbial activity for pollutant removal. Ongoing research is delivering novel bioremediation agents tailored to the specific needs of textile and food processing industries. With strong technological capacity and a commitment to environmental stewardship, South Korea is setting new standards in automated, efficient bioremediation for industrial wastewater.

Bioremediation Agents Market in Industrial Wastewater Treatment Report Scope

Bioremediation Agents Market in Industrial Wastewater Treatment

|

Parameter

|

Details

|

|

Market Size (2025)

|

$786.4 Million

|

|

Market Size (2034)

|

$1722.1 Million

|

|

Market Growth Rate

|

9.1%

|

|

Segments

|

By Type of Bioremediation Agent (Microbial Agents, Biostimulants/Nutrient Additives, Enzyme-based Formulations, Other Bio-derived Materials), By Application (Pollutant Type) (Organic Contaminants, Inorganic Contaminants, Mixed Contaminants), By Treatment Method (Bioaugmentation, Biostimulation, Bioreactors, Phytoremediation, Fungal Remediation, Land-based Treatments), By End-User Industry (Oil and Gas, Chemical and Petrochemical, Pharmaceutical, Pulp and Paper, Textile and Dyeing, Food and Beverage, Mining and Metallurgy, Automotive, Electronics and Semiconductors, Leather, Agriculture, Waste Management, Power Generation, Other Manufacturing Industries

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ecolab Inc. (U.S.), Veolia Water Technologies (France), Organica Biotech Pvt. Ltd. (India), Team One Biotech (India), Kurita Water Industries Ltd. (Japan), Xylem Inc. (U.S.), Evoqua Water Technologies LLC (U.S.), SUEZ SA (France), Newterra Ltd. (Canada), Probiosphere, Inc. (U.S.), Regenesis Corporation (U.S.), Biorem Technologies Inc. (Canada),

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Bioremediation Agents Market in Industrial Wastewater Treatment Market Segmentation

By Type of Bioremediation Agent

- Microbial Agents

- Bacteria-based

- Fungi-based

- Algae-based

- Genetically Engineered Microorganisms (GEMs)

- Biostimulants/Nutrient Additives

- Enzyme-based Formulations

- Other Bio-derived Materials

By Application (Pollutant Type)

- Organic Contaminants

- Hydrocarbons

- Pesticides and Herbicides

- Phenols

- Chlorinated Compounds

- Dyes and Pigments

- Pharmaceutical and Personal Care Products (PPCPs)

- Surfactants

- Xenobiotics

- High BOD/COD Wastewater

- Inorganic Contaminants

- Heavy Metals

- Nitrates and Phosphates

- Sulfides

- Mixed Contaminants

By Treatment Method

- Bioaugmentation

- Biostimulation

- Bioreactors

- Phytoremediation

- Fungal Remediation

- Land-based Treatments

By End-User Industry

- Oil and Gas

- Chemical and Petrochemical

- Pharmaceutical

- Pulp and Paper

- Textile and Dyeing

- Food and Beverage

- Mining and Metallurgy

- Automotive

- Electronics and Semiconductors

- Leather

- Agriculture

- Waste Management

- Power Generation

- Other Manufacturing Industries

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Bioremediation Agents Market in Industrial Wastewater Treatment

- Ecolab Inc. (U.S.)

- Veolia Water Technologies (France)

- Organica Biotech Pvt. Ltd. (India)

- Team One Biotech (India)

- Kurita Water Industries Ltd. (Japan)

- Xylem Inc. (U.S.)

- Evoqua Water Technologies LLC (U.S.)

- SUEZ SA (France)

- Newterra Ltd. (Canada)

- Probiosphere, Inc. (U.S.)

- Regenesis Corporation (U.S.)

- Biorem Technologies Inc. (Canada)

* List Not Exhaustive

Research Coverage

This report provides a comprehensive analysis of the Bioremediation Agents Market in Industrial Wastewater Treatment, delivering insights into growth drivers, regulatory dynamics, and the adoption of advanced microbial and enzymatic solutions across diverse industrial sectors. The study focuses on emerging technologies such as bioaugmentation, fungal remediation, enzyme-based systems, and genetically engineered microorganisms (GEMs) designed to treat complex organic and inorganic contaminants in industrial effluents. It evaluates key trends including the commercialization of engineered strains for PFAS degradation, the role of hybrid bioreactors, and the monetization of resource recovery through circular economy initiatives.

Scope Highlights:

- Segmentation Scope:

- By Type of Bioremediation Agent: Microbial Agents (Bacteria-based, Fungi-based, Algae-based, GEMs), Biostimulants/Nutrient Additives, Enzyme-based Formulations, Other Bio-derived Materials

- By Application (Pollutant Type): Organic Contaminants (Hydrocarbons, Pesticides, Phenols, Chlorinated Compounds, Pharmaceutical Residues), Inorganic Contaminants (Heavy Metals, Nitrates, Sulfides), Mixed Contaminants

- By Treatment Method: Bioaugmentation, Biostimulation, Bioreactors, Phytoremediation, Fungal Remediation, Land-based Treatments

- By End-User Industry: Oil & Gas, Chemical & Petrochemical, Pharmaceutical, Textile & Dyeing, Food & Beverage, Pulp & Paper, Mining & Metallurgy, Automotive, Electronics & Semiconductors, Agriculture, Waste Management, Power Generation, Other Manufacturing

- Geographic Scope: Covers 25+ countries across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

- Data Coverage: Historic data from 2021 to 2024 and forecasts from 2025 to 2034.

- Companies Profiled: Ecolab Inc. (U.S.), Veolia Water Technologies (France), Organica Biotech (India), Team One Biotech (India), Kurita Water Industries Ltd. (Japan), Xylem Inc. (U.S.), Evoqua Water Technologies (U.S.), SUEZ SA (France), Regenesis Corporation (U.S.), Probiosphere Inc. (U.S.), and others.

Methodology

The analysis is based on a hybrid research methodology, integrating primary interviews with industry stakeholders, environmental scientists, and technology innovators with extensive secondary research from peer-reviewed journals, regulatory reports, and global industry databases. Data triangulation was applied to validate market estimates, involving supply-side modeling (production, capacity, cost trends) and demand-side metrics (end-user adoption, regulatory compliance, sustainability initiatives). Forecasting employed time-series analysis, scenario modeling, and technology diffusion curves, ensuring precision across base-case and optimistic adoption scenarios. The methodology incorporates regulatory impact analysis for emerging contaminants like PFAS, antibiotics, and heavy metals and includes LCA-based benchmarking to evaluate environmental benefits of bioremediation compared to conventional chemical treatments. This comprehensive approach ensures reliable and actionable insights for decision-makers navigating the evolving industrial wastewater treatment landscape.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements