Pharmaceutical Wastewater Treatment Systems Market Size, Growth Outlook to 2034

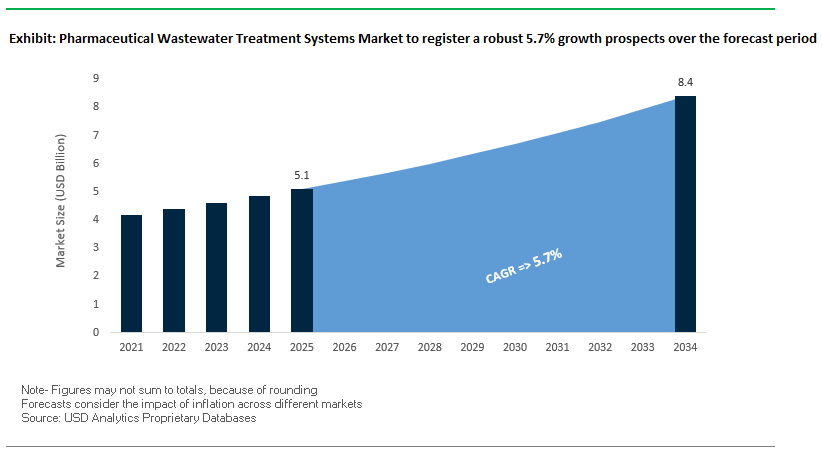

The pharmaceutical wastewater treatment systems market is projected to grow from $5.1 billion in 2025 to $8.4 billion by 2034, registering a healthy CAGR of 5.7%. This growth is underpinned by rising environmental regulations, the need for advanced treatment technologies, and increasing pharmaceutical manufacturing across Asia-Pacific and Europe.

The industry is under immense pressure to manage complex effluents containing APIs, solvents, and micropollutants, which cannot be effectively treated with conventional systems. Technologies such as advanced oxidation processes (AOPs), membrane filtration, and biological treatment are becoming central to compliance and sustainability goals.

Key Insights Driving Market Expansion

- Pharmaceuticals & chemicals remain top end-users of biological wastewater treatment, requiring robust and specialized solutions.

- According to the European Commission, over 90% of pharmaceutical micropollutants in urban wastewater come from medicinal and cosmetic residues, forcing stricter regulatory action.

- Asia-Pacific is the fastest-growing regional market, fueled by rapid industrialization, strong government mandates, and the expansion of pharmaceutical manufacturing hubs in China and India.

- Advanced Oxidation Processes (AOPs) are proven effective in degrading APIs and micropollutants, highlighting their increasing role in tertiary wastewater treatment.

Market Analysis: Recent Developments Reshaping Pharmaceutical Wastewater Treatment

The pharmaceutical wastewater treatment industry is undergoing rapid innovation, strategic partnerships, and regulatory shifts. Companies are not only improving wastewater treatment efficiency but also integrating resource recovery, AI-driven monitoring, and minimal liquid discharge (MLD) systems.

In August 2025, DuPont Water Solutions was recognized at the BIG Sustainability Awards for advancements in wastewater reuse and MLD for pharmaceuticals. Similarly, in July 2025, Veolia Water Technologies secured a major contract to equip France’s largest treated wastewater reuse project in Argelès-sur-Mer, showcasing its strength in large-scale water reclamation.

The regulatory landscape also shifted in March 2025 when the European Union’s Urban Wastewater Treatment Directive introduced Extended Producer Responsibility (EPR), holding pharmaceutical companies accountable for micropollutant removal costs. However, in February 2025, the European Federation of Pharmaceutical Industries and Associations (EFPIA) announced plans to challenge this directive in court, signaling potential industry pushback.

Technological innovation remains strong. bioMérieux launched its WATCHFIRE™ PCR solution in April 2025, enabling virus and bacteria detection in pharmaceutical effluent. Meanwhile, Kurita Water Industries validated microbial fuel cells in December 2024, using wastewater to generate electricity. Strategic programs like Veolia’s GreenUp 24-27 (announced in September 2024) further emphasize investment in reuse, resource recovery, and next-gen water technologies.

Key Market Trends Shaping the Pharmaceutical Wastewater Treatment Systems Industry

Advanced Oxidation Processes (AOPs) for Degrading Micropollutants

Advanced Oxidation Processes (AOPs) such as UV-H₂O₂ have emerged as critical technologies for pharmaceutical wastewater treatment. A 2024 study published in MDPI demonstrates that AOPs can achieve near-complete removal of persistent APIs resistant to biological treatment. Research from ResearchGate in early 2025 highlights hybrid systems where AOPs serve as a post-treatment polishing step, complementing biological treatment to remove residual micropollutants. This trend reflects the increasing regulatory focus on emerging contaminants and the need for technologically advanced solutions.

Growing Adoption of Zero Liquid Discharge (ZLD) Systems

ZLD systems are gaining traction in the pharmaceutical sector to manage high-salinity and high-strength wastewater. Jubilant Pharmova’s Nanjangud plant exemplifies the feasibility of ZLD, achieving a 90% reduction in cooling tower blowdown and complete elimination of wastewater discharge. The Indian Central Pollution Control Board classifies pharmaceutical production as a “red category” industry, driving mandatory ZLD adoption in water-stressed regions. This regulatory push is accelerating investments in sophisticated treatment technologies such as multi-effect evaporators and reverse osmosis, ensuring long-term sustainability and operational resilience.

Corporate Investment in On-Site Water Management

Pharma companies increasingly outsource wastewater management to specialized partners to maintain focus on core operations. Veolia Water Technologies has over 100 global reference projects providing design, engineering, and operational support for pharmaceutical wastewater. On-site water management not only ensures regulatory compliance but also optimizes resource efficiency. Case studies reveal that implementing advanced ZLD and AOP solutions reduces water consumption and operating costs, creating a compelling business case beyond environmental compliance.

Pharmaceutical Wastewater Treatment Systems Market Share Insights

Market Share by Type: Advanced/Tertiary Treatment Dominates

Tertiary/Advanced Treatment (40%) leads the market due to the need for complex technologies such as MBR, RO, AOPs, and ozonation to remove micropollutants and APIs. Secondary (Biological) Treatment (30%) remains critical for bulk organic removal, with upgrades increasingly favoring MBR over conventional activated sludge systems. Pre-Treatment & Primary Treatment (22%) maintains a stable share for screening, flow equalization, and clarification. The market demonstrates a clear shift toward integrating secondary and tertiary processes to meet stricter discharge standards and retrofit aging plants for compliance.

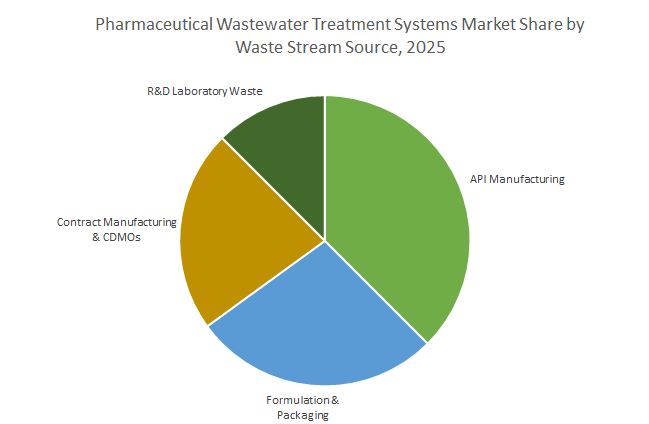

Market Share by Waste Stream Source: API Manufacturing Holds the Largest Share

API Manufacturing (38%) generates the most complex, high-strength, and variable wastewater, necessitating sophisticated treatment systems and making it the largest segment. Formulation & Packaging (26.9%) produces lower-strength but high-volume effluents, while Contract Manufacturing & CDMOs represent the fastest-growing segment due to diverse product portfolios and high compliance requirements. R&D Laboratory Waste is niche but critical for risk mitigation, requiring specialized point-source treatment before discharge. The complexity of wastewater directly drives investment and technology adoption across these segments.

Market Share by System Configuration: End-of-Pipe Still Dominant but Point-Source Growing

End-of-Pipe Treatment (68%) remains the traditional and most practical approach for centralized plants handling combined wastewater streams. Point-Source Treatment (32%) is a fast-growing strategy, focusing on high-strength or hazardous streams at their origin. This approach reduces load and toxicity for the main treatment plant, supports solvent recovery, enables water reuse, and aligns with circular water economy goals. Regulatory frameworks increasingly incentivize manufacturers to adopt point-source strategies to minimize environmental impact and enhance operational efficiency.

India: ZLD Mandates and API Manufacturing Boost Demand for Advanced Treatment Systems

India’s pharmaceutical wastewater treatment systems market is driven by stringent regulations and government initiatives supporting domestic drug production. The Central Pollution Control Board (CPCB) and National Green Tribunal (NGT) have mandated Zero Liquid Discharge (ZLD) in water-scarce regions, particularly for the discharge of active pharmaceutical ingredients (APIs) and antibiotics. Government programs like the “Scheme for Promotion of Bulk Drug Parks” and the Production Linked Incentive (PLI) Scheme are fostering the establishment of new pharmaceutical manufacturing facilities, creating demand for advanced wastewater treatment systems compliant with environmental standards. Technological advancements under the Revamped Pharmaceutical Technology Upgradation Assistance Scheme (RPTUAS) provide financial support for technology upgrades, including state-of-the-art MBR and membrane filtration systems. Corporations such as VA Tech Wabag have demonstrated expertise in executing large-scale projects, including industrial wastewater treatment for pharmaceutical facilities abroad. Key applications focus on the treatment of complex wastewater streams from APIs, bulk drugs, and formulations, emphasizing compliance, sustainability, and operational efficiency.

China: Regulatory Pressure and RO Membrane Innovation Drive Market Expansion

China’s pharmaceutical wastewater treatment market is experiencing significant growth due to regulatory mandates, government investments, and technological innovation. The Ministry of Ecology and Environment (MEE) enforces strict industrial wastewater discharge regulations, focusing on mitigating antibiotic resistance by reducing pharmaceutical effluents. The Chinese government plans to invest $50 billion in wastewater treatment infrastructure by 2025, with significant allocation to heavy-polluting industries, including pharmaceuticals. Technological advancements include dual-functional reverse osmosis (RO) membranes with enhanced antibacterial and anti-adhesion properties developed by the Chinese Academy of Sciences, which improve system efficiency in pharmaceutical wastewater treatment. Biological membrane bioreactors (MBRs) are increasingly adopted in municipal and industrial projects, providing higher treatment performance with a smaller footprint. These innovations position China as a key market for advanced pharmaceutical wastewater solutions.

United States: PFAS Regulations and Renewable-Powered MABR Solutions Stimulate Market Growth

The U.S. pharmaceutical wastewater treatment systems market is driven by regulatory oversight, research innovation, and corporate deployment of advanced technologies. The U.S. EPA’s PFAS Maximum Contaminant Levels and 2021 PFAS Strategic Roadmap are prompting immediate retrofitting of water treatment facilities with membrane technologies. Research by the National Alliance for Water Innovation (NAWI) is advancing new membranes for waste-brine treatment and renewable-powered desalination, supporting ZLD applications in pharmaceutical plants. Companies such as Veolia Water Technologies, Evoqua Water Technologies, and DuPont are deploying MABR and membrane-based solutions to achieve high-purity effluent for biopharmaceutical production. Key applications focus on treating complex wastewater streams and achieving stringent discharge standards, particularly in facilities producing highly regulated pharmaceuticals and biologics.

Germany: Advanced Oxidation, MBR Expansion, and Private Investment Propel Market Development

Germany’s pharmaceutical wastewater treatment systems market benefits from strict EU directives, innovation in treatment technology, and private-sector investment. The revised Urban Wastewater Treatment Directive (January 2025) requires a "4th purification stage" to eliminate micropollutants, encouraging adoption of advanced oxidation processes and membrane filtration systems. Infrastructure investments include support for startups like Membion, which received €5 million to expand MBR module production for retrofitting existing plants. Leading companies such as H2O GmbH, GEA Group AG, and Veolia are developing ZLD systems for pharmaceutical wastewater, exemplified by Veolia’s transformation of Roche’s Penzberg plant, reducing annual carbon emissions by 950 metric tons. Key applications focus on high-purity effluent management for pharmaceutical production, ensuring compliance with strict environmental regulations and sustainability targets.

Saudi Arabia: Vision 2030 and PPP Projects Encourage Advanced Wastewater Treatment Deployment

Saudi Arabia’s pharmaceutical wastewater treatment systems market is advancing due to government-led initiatives and public-private partnerships (PPP). The Saudi Water Partnership Company (SWPC) continues to launch projects incorporating advanced reverse osmosis and membrane technologies to enable water reuse. VA Tech Wabag secured a major contract in Riyadh in 2025, supporting pharmaceutical manufacturing under the National Water Strategy, which aims to reuse 1.8 billion cubic meters of treated water by 2030. Treated wastewater is primarily used for non-potable municipal and industrial applications, including pharmaceutical plant operations, and agricultural irrigation. These developments are key drivers for investment in advanced wastewater recycling technologies and sustainable water management solutions.

Japan: MBR Innovation and Biopharmaceutical Focus Enhance Market Potential

Japan’s pharmaceutical wastewater treatment systems market is shaped by advanced membrane technology, corporate sustainability initiatives, and academic research. The Ministry of Land, Infrastructure, Transport and Tourism (MLIT) launched the “Advance of Japan Ultimate Membrane bioreactor technology Project (A-JUMP)” to expand MBR adoption in pharmaceutical wastewater treatment. Toray Industries Inc., a leading Japanese manufacturer, has developed high-efficiency separation membrane modules for biopharmaceutical production, doubling filtration performance and reducing clogging compared to conventional systems. Key applications include nutrient recovery, water reuse, and treatment of complex pharmaceutical effluents. Japan’s focus on sustainable wastewater management in the pharmaceutical industry drives demand for high-performance, environmentally compliant treatment systems.

Competitive Landscape: Leading Players in Pharmaceutical Wastewater Treatment

The competitive landscape of the pharmaceutical wastewater treatment systems market is dominated by global leaders, regional innovators, and specialized technology providers. These companies differentiate themselves through advanced treatment portfolios, digital integration, and sustainability-driven strategies.

DuPont Water Solutions: Driving Innovation in Membrane Filtration

DuPont is a pioneer in high-performance membranes and its FilmTec™ RO and NF technologies are widely adopted in pharmaceutical wastewater treatment. In 2025, DuPont won an R&D 100 Award for its FilmTec™ Fortilife™ XC160 Membrane, engineered to concentrate pharmaceutical effluents and enable efficient water reuse and MLD. Its integrated solutions including RO, NF, ultrafiltration, and ion exchange resins are helping pharma facilities achieve water circularity and reduce operational costs.

Veolia Water Technologies: Leader in Large-Scale Pharmaceutical Wastewater Projects

Veolia is a global leader in ecological transformation, with expertise across DAF, activated sludge systems, and membrane bioreactors (MBR) tailored for pharmaceutical wastewater. Following its May 2025 acquisition of Water Technologies and Solutions, Veolia strengthened its ability to deliver integrated, full-cycle solutions. With over 100 pharmaceutical wastewater projects globally, it remains a preferred partner for compliance-driven, large-scale facilities.

SUEZ Water Technologies & Solutions: Advanced Micropollutant Treatment Specialist

SUEZ delivers customized, high-performance wastewater treatment systems for pharmaceutical and chemical industries. Its strengths lie in MBR systems, advanced oxidation, and nutrient removal technologies. Recent contracts in Asia, including a 100% wastewater recycling plant in China, demonstrate SUEZ’s ZLD (Zero Liquid Discharge) capabilities. By integrating predictive analytics and digital plant monitoring, SUEZ optimizes operational efficiency and cost savings for pharmaceutical clients.

Xylem Inc.: IoT-Enabled Wastewater Treatment Solutions

Xylem offers end-to-end water treatment technologies, including biological systems, oxidation processes, pumps, and MBRs. Its acquisition of Evoqua in 2023 expanded its pharmaceutical portfolio, combining complementary expertise. Xylem’s IoT-enabled monitoring and predictive maintenance tools are crucial for pharmaceutical plants aiming to meet compliance standards while lowering operating expenses.

Kurita Water Industries: Sustainable, Energy-Positive Wastewater Solutions

Kurita combines chemical treatment expertise with advanced wastewater equipment. In June 2024, it expanded into India through Kurita AquaChemie India Pvt. Ltd., tapping into Asia’s fast-growing pharmaceutical market. Its offerings range from membrane cleaning agents to microbial fuel cells capable of generating electricity from wastewater. Kurita’s sustainability strategy focuses on maximizing water reuse, minimizing discharges, and supporting clients’ carbon reduction goals.

Pharmaceutical Wastewater Treatment Systems Market Report Scope

Pharmaceutical Wastewater Treatment Systems Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.1 Billion

|

|

Market Size (2034)

|

$8.4 Billion

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Type (Pre-Treatment & Primary Treatment, Secondary (Biological) Treatment, Tertiary/Advanced Treatment), By Waste Stream Source (API Manufacturing, Formulation & Packaging Wastewater, Contract manufacturing & CDMOs, R&D Laboratory Waste), By System Configuration (End-of-Pipe Treatment, Point-Source Treatment), By Capacity (Micro, Small, Medium, Large, Very Large), By Pollutant (High-strength organic API streams, Active pharmaceutical ingredients, Antibiotics / cytotoxics / endocrine-active compounds, Solvent-laden streams, Saline / high TDS streams, Heavy metals, catalysts, chlorinated organics, Pathogen risk)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia, SUEZ, Xylem Inc., Evoqua Water Technologies, DuPont de Nemours, Inc., Alfa Laval, Toray Industries, Inc., Aquatech International, Kubota Corporation, The Dow Chemical Company, V.A. TECH WABAG Ltd., Mitsubishi Chemical Corporation, Kuraray Co., Ltd., H2O GmbH, Thermax Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Pharmaceutical Wastewater Treatment Systems Market Segmentation

By Type

- Pre-Treatment & Primary Treatment

- Secondary (Biological) Treatment

- Tertiary/Advanced Treatment

By Waste Stream Source

- API Manufacturing

- Formulation & Packaging Wastewater

- Contract manufacturing & CDMOs

- R&D Laboratory Waste

By System Configuration

- End-of-Pipe Treatment

- Point-Source Treatment

By Capacity

- Micro

- Small

- Medium

- Large

- Very Large

By Pollutant

- High-strength organic API streams

- Active pharmaceutical ingredients

- Antibiotics / cytotoxics / endocrine-active compounds

- Solvent-laden streams

- Saline / high TDS streams

- Heavy metals, catalysts, chlorinated organics

- Pathogen risk

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Pharmaceutical Wastewater Treatment Systems Industry include-

- Veolia

- SUEZ

- Xylem Inc.

- Evoqua Water Technologies

- DuPont de Nemours, Inc.

- Alfa Laval

- Toray Industries, Inc.

- Aquatech International

- Kubota Corporation

- The Dow Chemical Company

- V.A. TECH WABAG Ltd.

- Mitsubishi Chemical Corporation

- Kuraray Co., Ltd.

- H2O GmbH

- Thermax Limited

*- List not Exhaustive

Research Coverage

This report investigates the Pharmaceutical Wastewater Treatment Systems Market with analysis reviews of demand fundamentals, regulatory inflection points, and plant-level economics; it highlights technology breakthroughs in AOPs, MBR/RO trains, ZLD/MLD integration, and point-source controls that are redefining compliance and reuse strategies. Produced by USDAnalytics, the study maps growth across API, formulation, CDMO, and R&D streams; benchmarks removal performance for APIs, solvent-laden and saline effluents; and evaluates vendor capabilities, cost curves, and retrofit pathways under EU EPR rules and Asia-Pacific build-out. By unifying market sizing with engineering metrics (energy, chemicals, cleaning intervals, brine handling) and procurement best practices, this report is an essential resource for EHS leaders, utilities managers, process engineers, OEMs/EPCs, and investors planning resilient water strategies through 2034. Scope Includes-

- Segmentation

- By Type: Pre-Treatment & Primary; Secondary (Biological); Tertiary/Advanced

- By Waste Stream Source: API Manufacturing; Formulation & Packaging; Contract Manufacturing & CDMOs; R&D Laboratory Waste

- By System Configuration: End-of-Pipe; Point-Source

- By Capacity: Micro; Small; Medium; Large; Very Large

- By Pollutant: High-strength organic API streams; Active pharmaceutical ingredients; Antibiotics/cytotoxics/endocrine-active compounds; Solvent-laden streams; Saline/high TDS; Heavy metals/catalysts/chlorinated organics; Pathogen risk

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Frame: Historic data 2021–2024; Forecasts 2025–2034.

- Companies (15+ profiles/analysis): Veolia; SUEZ; Xylem Inc.; Evoqua Water Technologies; DuPont de Nemours, Inc.; Alfa Laval; Toray Industries, Inc.; Aquatech International; Kubota Corporation; The Dow Chemical Company; V.A. TECH WABAG Ltd.; Mitsubishi Chemical Corporation; Kuraray Co., Ltd.; H2O GmbH; Thermax Limited.

Methodology

USDAnalytics employs a triangulated approach: bottom-up audits of installed capacities and equipment shipments by stream type and configuration; top-down allocation from pharma output, CapEx/Opex budgets, and discharge permits; and 100+ expert interviews spanning EHS leaders, OEMs/EPCs, and regulators. Technical validation draws on pilot and full-scale data for AOPs (UV-H₂O₂/ozone), MBR, UF/NF/RO, evaporators/crystallizers, and solvent recovery capturing BOD/COD reduction, API/micropollutant removal, kWh·m⁻³, chemical dose, cleaning cycles, and brine yields. We build levelized cost models and stress-test forecasts to 2034 under scenarios for EU EPR, ZLD mandates, PFAS/PPCP limits, energy price volatility, and water-scarcity indices, producing defensible market sizes and vendor share estimates.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Pharmaceutical Wastewater Treatment Systems Market

1. Executive Summary

1.1. Market Highlights and Key Projections

1.2. Key Insights: Regulatory Pressure, Micropollutant Removal, and Asia-Pacific Growth

1.3. Global Market Snapshot

1.3.1. Current Market Valuation (2025): $5.1 Billion

1.3.2. Projected Market Valuation (2034): $8.4 Billion

1.3.3. Compound Annual Growth Rate (CAGR): 5.7%

2. Market Outlook (2025–2034)

2.1. Introduction: Market Drivers and Growth Forecast

2.2. Market Valuation and Growth Projections (2025–2034)

2.3. Key Trends and Emerging Opportunities

2.3.1. Advanced Oxidation Processes (AOPs) for Degrading Micropollutants

2.3.2. Growing Adoption of Zero Liquid Discharge (ZLD) Systems

2.3.3. Corporate Investment in On-Site Water Management

3. Innovations and Strategic Developments

3.1. Market Analysis: Recent Developments Reshaping the Industry

3.1.1. DuPont Water Solutions Recognized with Sustainability Awards (August 2025)

3.1.2. Veolia Secures Major Water Reuse Contracts in France (July 2025)

3.1.3. European Regulatory Shifts and Industry Pushback (March 2025)

3.1.4. Technological Innovations: New Detection and Energy Generation Systems (2024–2025)

3.1.5. Strategic Corporate Programs for Ecological Transformation

4. Competitive Landscape: Leading Companies

4.1. Competitive Overview: Global Leaders and Regional Innovators

4.2. Strategic Profiles of Key Companies

4.2.1. DuPont Water Solutions: Driving Innovation in Membrane Filtration

4.2.2. Veolia Water Technologies: Leader in Large-Scale Pharmaceutical Wastewater Projects

4.2.3. SUEZ Water Technologies & Solutions: Advanced Micropollutant Treatment Specialist

4.2.4. Xylem Inc.: IoT-Enabled Wastewater Treatment Solutions

4.2.5. Kurita Water Industries: Sustainable, Energy-Positive Wastewater Solutions

5. Market Segmentation Insights

5.1. By Type

5.1.1. Tertiary/Advanced Treatment (40% Market Share)

5.1.2. Secondary (Biological) Treatment (30% Market Share)

5.1.3. Pre-Treatment & Primary Treatment (22% Market Share)

5.2. By Waste Stream Source

5.2.1. API Manufacturing (38% Market Share)

5.2.2. Formulation & Packaging

5.2.3. Contract Manufacturing & CDMOs

5.2.4. R&D Laboratory Waste

5.3. By System Configuration

5.3.1. End-of-Pipe Treatment (68% Market Share)

5.3.2. Point-Source Treatment (32% Market Share)

5.4. By Capacity

5.4.1. Micro

5.4.2. Small

5.4.3. Medium

5.4.4. Large

5.4.5. Very Large

5.5. By Pollutant

5.5.1. High-Strength Organic API Streams

5.5.2. Active Pharmaceutical Ingredients

5.5.3. Antibiotics / Cytotoxics / Endocrine-Active Compounds

5.5.4. Solvent-Laden Streams

5.5.5. Saline / High TDS Streams

5.5.6. Heavy Metals, Catalysts, Chlorinated Organics

5.5.7. Pathogen Risk

6. Country Analysis and Outlook

6.1. India: ZLD Mandates and API Manufacturing

6.2. China: Regulatory Pressure and RO Membrane Innovation

6.3. United States: PFAS Regulations and Advanced Solutions

6.4. Germany: Advanced Oxidation and MBR Expansion

6.5. Saudi Arabia: Vision 2030 and PPP Projects

6.6. Japan: MBR Innovation and Biopharmaceutical Focus

6.7. Other Countries Analyzed

6.7.1. North America (Canada, Mexico)

6.7.2. Europe (UK, France, Spain, Italy, Russia, Rest of Europe)

6.7.3. Asia Pacific (South Korea, Australia, South East Asia, Rest of Asia)

6.7.4. South America (Brazil, Argentina, Rest of South America)

6.7.5. Middle East and Africa (UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

7. Company Profiles

7.1. Veolia

7.2. SUEZ

7.3. Xylem Inc.

7.4. Evoqua Water Technologies

7.5. DuPont de Nemours, Inc.

7.6. Alfa Laval

7.7. Toray Industries, Inc.

7.8. Aquatech International

7.9. Kubota Corporation

7.10. The Dow Chemical Company

7.11. V.A. TECH WABAG Ltd.

7.12. Mitsubishi Chemical Corporation

7.13. Kuraray Co., Ltd.

7.14. H2O GmbH

7.15. Thermax Limited

8. Methodology

8.1. Research Scope

8.2. Market Research Approach

8.3. Market Sizing and Forecasting Model

8.4. Research Coverage

8.5. Data Horizon

8.6. Deliverables

9. Appendix

9.1. Acronyms and Abbreviations

9.2. List of Tables

9.3. List of Figures