Biological Wastewater Treatment Market Overview: Growth Outlook and Key Insights

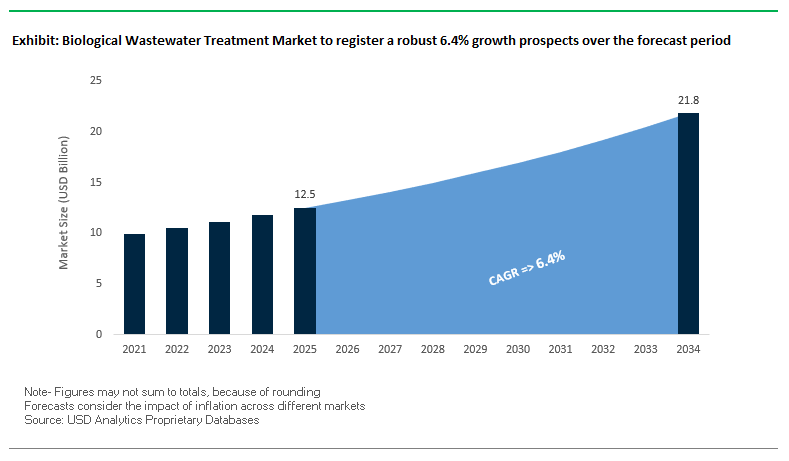

The Biological Wastewater Treatment Market is projected to grow from $12.5 billion in 2025 to $21.8 billion by 2034, registering a CAGR of 6.4%. This growth trajectory underscores the increasing demand for sustainable wastewater treatment solutions driven by rapid urbanization, industrial expansion, and stringent environmental regulations. Biological processes, particularly activated sludge systems, anaerobic digesters, and advanced membrane bioreactors (MBRs), are at the forefront of this expansion, offering cost-efficient and eco-friendly alternatives to conventional chemical treatment.

Key Insights for Decision-Makers:

- Energy Efficiency: Advanced biological systems can lower operational energy costs by 20–30% compared to conventional methods.

- Industrial Adoption: Food & beverage, pharmaceuticals, and chemicals industries are leading adopters due to stricter discharge standards.

- Technology Shifts: Membrane bioreactors (MBRs) are gaining traction for municipal and industrial wastewater reuse due to high effluent quality.

- Geographical Demand: Asia-Pacific dominates the market with growing investments in municipal infrastructure, while North America focuses on plant upgrades and regulatory compliance.

Market Analysis: Recent Developments Shaping the Sector

The biological wastewater treatment industry is evolving rapidly, with innovation and strategic partnerships driving the adoption of advanced systems. A series of high-impact developments since late 2024 reflect how technology suppliers and utilities are aligning to meet sustainability targets and optimize wastewater reuse.

In August 2025, DuPont Water Solutions earned recognition with the BIG Sustainability Award for its FilmTec™ Fortilife™ membranes, designed to support wastewater reuse in retrofitted industrial facilities. Just a month earlier, in July 2025, SUEZ partnered with AgriTech startup Seabex to explore agricultural applications of biochar, reinforcing the shift towards integrated waste-to-value solutions in wastewater treatment.

Veolia Water Technologies made headlines in May 2025 by acquiring full ownership of its Water Technologies and Solutions subsidiary, a move aimed at streamlining operations and accelerating its wastewater infrastructure upgrade portfolio. Meanwhile, Toray Industries launched a next-generation reverse osmosis membrane in March 2025, boasting double chemical resistance and reduced replacement frequency an advancement particularly relevant for retrofitting biological treatment plants.

Earlier in February 2025, Kovalus Separation Solutions announced a $20 million investment in Mexico to expand spiral membrane production capacity by 50%, a direct response to the growing demand for retrofit-friendly systems in North America and Latin America.

Looking back to late 2024, strategic milestones also shaped the industry’s trajectory. At COP29 in November 2024, Nitto Denko Corporation unveiled its carbon-negative membrane solutions for CO₂ capture from industrial exhaust gases demonstrating how biological treatment can be paired with environmental remediation technologies. Similarly, in October 2024, Veolia secured a contract in San Francisco to deploy its MemGas™ membrane technology, converting wastewater biogas into renewable natural gas, underscoring the integration of biological treatment with circular economy solutions.

Key Trends Driving the Biological Wastewater Treatment Market

Advanced Biological Processes for Nutrient and Micropollutant Removal

Technological innovation is reshaping treatment efficiency with systems capable of handling complex pollutants. For instance, research published in Energies has shown that Microbial Fuel Cells (MFCs) can simultaneously treat wastewater and generate electricity, with a pilot project in Dhaka achieving a theoretical recovery of 478.4 MWh/day from 100,000 cubic meters of effluent. Commercially, Alfa Laval’s Membrane Bioreactor (MBR) systems highlight the industry’s pivot toward advanced processes capable of reducing suspended solids to less than 1 mg/L, enabling treated water reuse. This trend underscores how nutrient and micropollutant removal is becoming the new benchmark for high-quality effluent standards worldwide.

The Push for Decentralized and Modular Biological Systems

Decentralized wastewater treatment is emerging as a game-changer, especially for regions without centralized infrastructure. Fluence Corporation’s projects in India demonstrate how modular plants can address wastewater challenges in rapidly urbanizing and remote geographies. According to the India Brand Equity Foundation, nearly 49% of India’s wastewater systems already rely on biological processes, paving the way for advanced, flexible, and modular solutions that reduce the dependence on expensive large-scale networks. This trend is particularly relevant for developing economies and industrial clusters where agility and scalability are paramount.

Industrial Sector Investment in Sustainable Effluent Management

Industries are increasingly integrating biological wastewater treatment into their sustainability frameworks. Oriental Weavers’ new facility treating 1,250 m³/day of wastewater and the Ilim Group’s investment in Russia for its kraftliner mill highlight how large-scale industrial players are embedding biological solutions within core operations. This reflects a global movement where wastewater management is no longer a regulatory burden but a competitive differentiator. Industrial wastewater treatment investments are particularly critical in high-consumption sectors such as pulp & paper, textiles, and food & beverage, where closed-loop systems enhance both compliance and resource efficiency.

Emerging Opportunities in the Biological Wastewater Treatment Market

The opportunities in this market are closely tied to the convergence of sustainability goals and technological progress. The resource recovery potential of anaerobic treatment systems is opening avenues for energy-positive wastewater plants, especially in industries with high-strength effluents. Growing demand for decentralized modular systems offers suppliers and integrators the chance to penetrate underserved markets, particularly in Asia-Pacific, Africa, and Latin America. Moreover, advanced nutrient removal technologies are enabling utilities and municipalities to comply with tightening nutrient discharge limits, creating opportunities for providers of hybrid and upgraded systems. Another major opportunity lies in bioaugmentation solutions, which offer tailored microbial consortia to treat specialized industrial waste streams helping plants address increasingly diverse and toxic pollutant loads. Collectively, these opportunities reinforce biological wastewater treatment as not just a compliance solution but a driver of circular economy integration, water reuse, and industrial sustainability.

Market Share Analysis of the Biological Wastewater Treatment Market

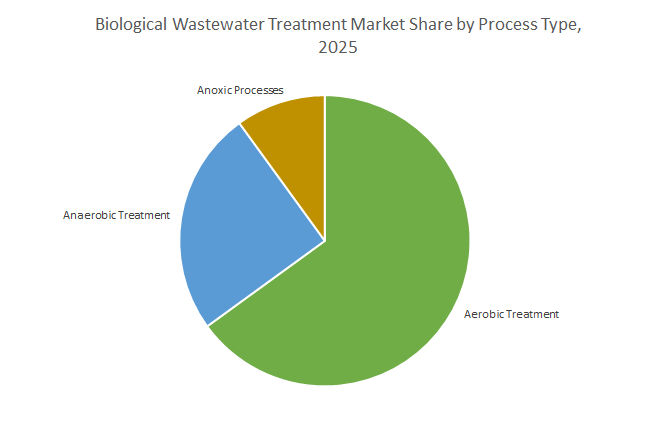

Market Share by Process Type

The biological wastewater treatment market is heavily dominated by aerobic processes, accounting for 65% of global installations, primarily due to their effectiveness in handling municipal effluents and industrial discharges of moderate strength. Conventional activated sludge systems remain the backbone of municipal treatment, offering a reliable and standardized approach. However, anaerobic treatment, with a 25% market share, is gaining momentum in industrial settings such as distilleries, pulp & paper, and food processing, where energy recovery from biogas is shifting plants toward energy-neutral operations. The 10% share of anoxic processes highlights their role as essential complements in nutrient removal, particularly for nitrogen, reinforcing the complexity of integrated modern systems. While aerobic methods dominate today, anaerobic and hybrid approaches are expected to capture greater share as industries prioritize sustainability and energy efficiency.

Market Share by Technology

By technology, the market continues to be anchored by Conventional Activated Sludge (CAS) systems, which hold a 50% market share due to entrenched municipal infrastructure. However, the fastest growth lies in advanced Biological Nutrient Removal (BNR) systems, representing 25% of the market, as utilities globally face tighter nitrogen and phosphorus discharge limits. Hybrid systems such as MBBR, MBR, and IFAS, with a 15% market share, are carving a strong niche where land is scarce and higher performance is needed. Meanwhile, natural systems (5%) such as constructed wetlands remain vital for small communities, offering low-energy alternatives. Bioaugmentation technologies (5%) play a strategic role in specialized industrial cases, allowing tailored microbial enhancement for unique pollutants. The overall technology mix indicates a transition away from conventional CAS toward nutrient-focused and hybrid systems, aligning with stricter global regulations and circular economy models.

Market Share by Application

In terms of application, the municipal wastewater treatment sector accounts for 70% of the global biological treatment demand, reflecting large-scale public investment, growing urban populations, and the urgent need to modernize aging infrastructure. This dominance is reinforced by the need for public health safeguards and environmental compliance, making municipal projects the cornerstone of market growth. On the other hand, the industrial wastewater treatment segment holds 30%, but is considered the most innovation-driven segment. With industries adopting wastewater recycling, anaerobic digestion, and customized bioaugmentation, industrial applications are increasingly setting the pace for next-generation solutions. The industrial share is expected to grow faster than municipal, driven by corporate sustainability goals, rising regulatory scrutiny, and the economic benefits of resource recovery from effluents.

China: Regulatory-Driven Expansion and Advanced MBR Adoption

China’s biological wastewater treatment market is strongly influenced by stringent regulatory policies and large-scale government investments. The Ministry of Ecology and Environment (MEE) enforces rigorous industrial wastewater discharge standards, driving the adoption of advanced treatment technologies. The 14th Five-Year Plan emphasizes water reuse and aims to achieve 95% wastewater treatment coverage in all county-level cities, creating massive demand for biological treatment infrastructure. In 2024, researchers from the Chinese Academy of Sciences developed dual-functional RO membranes with enhanced antibacterial and anti-adhesion properties for use downstream of biological treatment systems, boosting overall system efficiency. With planned investments of $50 billion by 2025 in sectors like textiles, steel, and pharmaceuticals, China is rapidly expanding its deployment of membrane bioreactors (MBRs) for municipal wastewater treatment, enabling higher treatment efficiency and smaller plant footprints.

United States: Government Funding and Corporate Deployment Drive MBR Growth

In the U.S., biological wastewater treatment growth is propelled by significant government funding and innovative technologies. The Bipartisan Infrastructure Law allocates over $50 billion to the EPA for water infrastructure improvements, including tackling emerging contaminants like PFAS, which require advanced biological and membrane-based treatment. Public-private partnerships such as the National Alliance for Water Innovation (NAWI) support research and development to lower desalination costs and improve energy efficiency. Leading corporations including Veolia Water Technologies, Evoqua Water Technologies, and Koch Separation Solutions are deploying modular MBR systems that allow retrofitting of existing facilities while meeting regulatory standards. Biological treatment is increasingly applied in the food and beverage sector, with strong emphasis on resource recovery and bioenergy generation, further driving market expansion.

India: Government Missions and Infrastructure Investment Accelerate Treatment Adoption

India’s biological wastewater treatment market is shaped by national initiatives and infrastructure investments. Programs like the Jal Jeevan Mission, Namami Gange Mission, and Smart Cities Mission are accelerating new plant deployment and modernization of existing facilities. Under AMRUT, the government has allocated over INR 77,640 crores (approximately USD 10 billion) for water supply and wastewater treatment infrastructure, often implemented through public-private partnerships. Technological adoption is increasing, with sequencing batch reactors (SBR) and membrane bioreactors (MBR) used to achieve higher treatment efficiency. Industrial sectors such as power generation, chemicals, and textiles are driving demand for wastewater reuse solutions, reducing environmental impact while ensuring regulatory compliance.

Germany: Advanced Regulatory Environment and Containerized Biological Systems

Germany remains a global leader in biological wastewater treatment due to strict environmental regulations and advanced technology adoption. The German Federal Wastewater Charges Act incentivizes investment in treatment systems, promoting retrofits and expansion with modern biological technologies. Nitrification and denitrification are standard practices, with over 95% of treated wastewater employing these methods. German companies such as PPU Umwelttechnik are innovating with containerized membrane systems, which can be installed in both new and existing tanks, providing cost-effective and scalable solutions for retrofitting older facilities and enhancing municipal and industrial wastewater management.

Japan: Legacy of Johkasou Systems and MBR Innovation

Japan’s market for biological wastewater treatment benefits from a legacy of advanced on-site systems and active corporate-academic collaboration. The Johkasou decentralized systems treat both blackwater and greywater, reflecting decades of innovation in biological treatment. The A-JUMP project (Advance of Japan Ultimate Membrane bioreactor technology Project) promotes MBR adoption for medium- to large-scale sewage plants requiring upgrades, highlighting the strategic focus on retrofitting. In 2025, Toray Industries announced high-efficiency separation membrane modules for biopharmaceutical processes, demonstrating Japan’s leadership in integrating advanced membrane technologies with biological treatment, ensuring higher throughput and reduced operational costs.

Saudi Arabia: Strategic Investment in MBR Systems for Water Reuse

Saudi Arabia is investing heavily in advanced biological wastewater treatment to address water scarcity and promote sustainable reuse. The Saudi Water Partnership Company (SWPC) is inviting bids for six new wastewater treatment projects under public-private partnerships in 2024, emphasizing membrane bioreactor (MBR) technology. MBR systems provide higher-quality effluent than conventional treatment, enabling reuse in non-potable municipal, industrial, and agricultural applications. These initiatives align with the Kingdom’s strategy to optimize water resources, reduce freshwater dependence, and adopt sustainable, energy-efficient biological treatment technologies.

Competitive Landscape: Leading Innovators in Biological Wastewater Treatment

The competitive landscape of the biological wastewater treatment market is shaped by global leaders and innovators focusing on retrofits, energy efficiency, and advanced system integration. Companies are differentiating through R&D investments, sustainable product portfolios, and digital technologies that enhance plant reliability and compliance.

DuPont Water Solutions – Driving Membrane Integration in Biological Systems

DuPont’s strength lies in its FilmTec™ membrane portfolio, which has become a benchmark for biological wastewater treatment retrofits. With FilmTec™ Fortilife™ membranes recognized in August 2025 for industrial reuse applications, DuPont is positioned as a leader in sustainability-driven upgrades. Its strategy emphasizes total cost of ownership (TCO) reduction, delivering membranes that extend system life, cut chemical use, and reduce energy intensity factors critical for industries upgrading biological plants.

SUEZ – Comprehensive Water and Wastewater Retrofitting Expertise

SUEZ has established itself as a full-spectrum service provider, from biological system design to long-term operations. With strategic collaborations like the Seabex biochar project (July 2025) and its CNRS partnership (April 2025), the company is reinforcing its focus on sustainable wastewater treatment and advanced retrofits. Its ability to integrate digital predictive analytics with physical infrastructure makes it a preferred choice for municipalities and industries seeking optimized biological treatment.

Veolia Water Technologies – Global Leader in Wastewater Infrastructure Upgrades

Veolia continues to dominate the retrofit space with large-scale projects and flexible solutions such as mobile water services for temporary plant upgrades. Its MemGas™ project in San Francisco (October 2024) highlighted how biological wastewater systems can be integrated with energy recovery. The May 2025 acquisition of its Water Technologies subsidiary demonstrates its commitment to strengthening its portfolio for long-term market leadership in biological treatment retrofits.

Kurita Water Industries Ltd. – Specialized Membrane Treatment and Cleaning Expertise

Kurita leverages decades of expertise in membrane cleaning chemicals, antiscalants, and process optimization to extend the performance of existing biological treatment systems. Its merger with Avista Technologies (April 2025) significantly expanded its North American presence, enhancing its retrofit-focused solutions. Kurita’s CSV (Creating Shared Value) business model aligns with industry demand for sustainable, efficiency-driven upgrades.

Toray Industries, Inc. – Innovation in High-Performance RO Membranes for Retrofits

Toray stands out for its strong foundation in synthetic polymer chemistry, enabling it to develop membranes that directly enhance retrofitted biological wastewater systems. The March 2025 launch of its advanced RO membrane represents a key milestone in improving chemical resistance and operational life, directly lowering costs for biological treatment operators. Its Water Treatment Technology Center in Saudi Arabia further positions Toray as a regional leader in addressing water scarcity with advanced retrofitting solutions.

Biological Wastewater Treatment Market Report Scope

Biological Wastewater Treatment Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$12.5 Billion

|

|

Market Size (2034)

|

$21.8 Billion

|

|

Market Growth Rate

|

6.4%

|

|

Segments

|

By Process Type (Aerobic Treatment, Anaerobic Treatment, Anoxic Processes), By Technology (Conventional Activated Sludge Systems, Advanced Biological Nutrient Removal (BNR), Hybrid Biological Treatment, Bioaugmentation & Specialized Microbial Consortia, Natural Systems), By Application (Municipal Wastewater Treatment, Industrial Wastewater Treatment), By Plant Configuration (Centralized Wastewater Treatment Plants, Decentralized & Onsite Systems), By End-User (Municipal Authorities, Industrial Facilities, Commercial Establishments, Residential Complexes)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia, SUEZ, Xylem Inc., Evoqua Water Technologies, Pentair plc, DuPont de Nemours, Inc., Toray Industries, Inc., Aquatech International, Kubota Corporation, The Dow Chemical Company, V.A. TECH WABAG Ltd., Mitsubishi Chemical Corporation, Kuraray Co., Ltd., Ion Exchange (India) Ltd., Thermax Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Biological Wastewater Treatment Market Segmentation

By Process Type

- Aerobic Treatment

- Activated Sludge Process (ASP)

- Sequencing Batch Reactors (SBR)

- Moving Bed Biofilm Reactor (MBBR)

- Membrane Bioreactors (MBR)

- Trickling Filters

- Rotating Biological Contactors (RBCs)

- Anaerobic Treatment

- Upflow Anaerobic Sludge Blanket (UASB)

- Anaerobic Digesters

- Anaerobic Filters

- Expanded/Fluidized Bed Reactors

- Anoxic Processes

- Denitrification Systems

- Combined Anoxic–Aerobic Treatment

By Technology

- Conventional Activated Sludge Systems

- Advanced Biological Nutrient Removal (BNR)

- Hybrid Biological Treatment

- Bioaugmentation & Specialized Microbial Consortia

- Natural Systems

By Application

- Municipal Wastewater Treatment

- Domestic Sewage

- Community Treatment Plants

- Industrial Wastewater Treatment

- Food & Beverage Processing

- Pharmaceuticals & Biotechnology

- Pulp & Paper Mills

- Chemicals & Petrochemicals

- Oil & Gas & Refining

- Textiles & Dyeing

- Power Generation & Utilities

By Plant Configuration

- Centralized Wastewater Treatment Plants

- Decentralized & Onsite Systems

By End-User

- Municipal Authorities

- Industrial Facilities

- Commercial Establishments

- Residential Complexes

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Biological Wastewater Treatment Industry include-

- Veolia

- SUEZ

- Xylem Inc.

- Evoqua Water Technologies

- Pentair plc

- DuPont de Nemours, Inc.

- Toray Industries, Inc.

- Aquatech International

- Kubota Corporation

- The Dow Chemical Company

- V.A. TECH WABAG Ltd.

- Mitsubishi Chemical Corporation

- Kuraray Co., Ltd.

- Ion Exchange (India) Ltd.

- Thermax Limited

*- List not Exhaustive

Research Coverage

This report investigates the global Biological Wastewater Treatment Market, delivering analysis reviews on demand drivers, regulatory inflection points, and technology breakthroughs that are redefining nutrient removal, energy balance, and reuse economics. Produced by USDAnalytics, this report is an essential resource for municipal authorities, industrial operators, EPCs, and technology providers seeking decision-ready insight into upgrade pathways, CAPEX/OPEX trade-offs, and circular-economy integration. It highlights how advanced activated sludge, anaerobic digestion, hybrid biofilm systems, and membrane bioreactors converge with digital controls to stabilize effluent quality, unlock biogas valorization, and compress footprints offering clear strategic highlights for compliance roadmaps, decarbonization targets, and resilience planning through 2034. Scope Includes-

- Segmentation:

- By Process Type: Aerobic (ASP, SBR, MBBR, MBR, Trickling Filters, RBCs); Anaerobic (UASB, Anaerobic Digesters, Anaerobic Filters, Expanded/Fluidized Bed Reactors); Anoxic (Denitrification Systems, Combined Anoxic–Aerobic).

- By Technology: Conventional Activated Sludge; Advanced BNR; Hybrid Biological Treatment; Bioaugmentation & Specialized Microbial Consortia; Natural Systems.

- By Application: Municipal Wastewater Treatment (Domestic Sewage, Community Plants); Industrial Wastewater Treatment (Food & Beverage; Pharmaceuticals & Biotechnology; Pulp & Paper; Chemicals & Petrochemicals; Oil & Gas & Refining; Textiles & Dyeing; Power Generation & Utilities).

- By Plant Configuration: Centralized Plants; Decentralized & Onsite Systems.

- By End-User: Municipal Authorities; Industrial Facilities; Commercial Establishments; Residential Complexes.

- Geographic Scope: “Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.”

- Data Coverage: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies (Profiles of 15+ companies): Veolia; SUEZ; Xylem Inc.; Evoqua Water Technologies; Pentair plc; DuPont de Nemours, Inc.; Toray Industries, Inc.; Aquatech International; Kubota Corporation; The Dow Chemical Company; V.A. TECH WABAG Ltd.; Mitsubishi Chemical Corporation; Kuraray Co., Ltd.; Ion Exchange (India) Ltd.; Thermax Limited.

Methodology

USDAnalytics employs a mixed-methods framework combining bottom-up market sizing by process, technology, application, configuration, and end-user across each country with top-down triangulation using utility capex, industrial water intensity, urbanization rates, and regulatory timetables. Primary research includes structured interviews with utility managers, plant engineers, EPCs, and technology vendors to validate throughput, energy use, nutrient limits, upgrade costs, and payback periods. Secondary inputs span environmental statutes, tender/PPP databases, academic literature, and vendor specifications to benchmark KPIs (effluent TN/TP, MLSS/MLVSS, SOTE, energy kWh/m³, SRT/HRT, biogas yield). Scenario modeling stress-tests sensitivities to energy prices, sludge-handling costs, membrane adoption, and nutrient standards, producing robust 2025–2034 forecasts with defensible confidence bands.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Biological Wastewater Treatment Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Insights for Decision-Makers

1.3. Global Market Snapshot

1.3.1. Current Market Size (2025): $12.5 Billion

1.3.2. Forecasted Market Size (2034): $21.8 Billion

1.3.3. Projected Compound Annual Growth Rate (CAGR): 6.4%

2. Biological Wastewater Treatment Market Outlook (2025–2034)

2.1. Introduction: Increasing Demand for Sustainable Solutions

2.2. Market Valuation and Growth Projections (2025–2034)

2.3. Key Trends Driving the Market

2.3.1. Advanced Biological Processes for Nutrient and Micropollutant Removal

2.3.2. The Push for Decentralized and Modular Biological Systems

2.3.3. Industrial Sector Investment in Sustainable Effluent Management

2.3.4. Emerging Opportunities in Resource Recovery and Bioaugmentation

3. Innovations and Strategic Developments Redefining the Market

3.1. Market Analysis: Recent Developments Shaping the Sector

3.1.1. DuPont Water Solutions Wins Sustainability Award (August 2025)

3.1.2. SUEZ Partners with AgriTech Startup for Biochar Applications (July 2025)

3.1.3. Veolia Acquires Water Technologies and Solutions Subsidiary (May 2025)

3.1.4. Toray Industries Launches Next-Generation RO Membrane (March 2025)

3.1.5. Kovalus Separation Solutions Invests in Mexico (February 2025)

3.1.6. Nitto Denko Showcases Carbon-Negative Membrane Technology at COP29 (November 2024)

3.1.7. Veolia Secures Biogas-to-Energy Project in San Francisco (October 2024)

4. Competitive Landscape: Biological Wastewater Treatment Market

4.1. Market Overview: Leading Innovators Focusing on Energy Efficiency and Integration

4.2. Profiles of Top Players

4.2.1. DuPont Water Solutions

4.2.2. SUEZ

4.2.3. Veolia Water Technologies

4.2.4. Kurita Water Industries Ltd.

4.2.5. Toray Industries, Inc.

5. Biological Wastewater Treatment Market – Segmentation Insights (2025–2034)

5.1. By Process Type

5.1.1. Aerobic Treatment: Largest Segment (65% Share)

5.1.2. Anaerobic Treatment: Gaining Momentum (25% Share)

5.1.3. Anoxic Processes

5.2. By Technology

5.2.1. Conventional Activated Sludge Systems (CAS): Backbone of the Market (50% Share)

5.2.2. Advanced Biological Nutrient Removal (BNR): Fastest Growing Segment (25% Share)

5.2.3. Hybrid Biological Treatment

5.2.4. Bioaugmentation & Specialized Microbial Consortia

5.2.5. Natural Systems

5.3. By Application

5.3.1. Municipal Wastewater Treatment: Largest Segment (70% Share)

5.3.2. Industrial Wastewater Treatment: Most Innovation-Driven Segment (30% Share)

5.4. By Plant Configuration

5.4.1. Centralized Wastewater Treatment Plants

5.4.2. Decentralized & Onsite Systems

5.5. By End-User

5.5.1. Municipal Authorities

5.5.2. Industrial Facilities

5.5.3. Commercial Establishments

5.5.4. Residential Complexes

6. Country Analysis and Outlook: Biological Wastewater Treatment Market

6.1. China: Regulatory-Driven Expansion and Advanced MBR Adoption

6.2. United States: Government Funding and Corporate Deployment Drive MBR Growth

6.3. India: Government Missions and Infrastructure Investment Accelerate Treatment Adoption

6.4. Germany: Advanced Regulatory Environment and Containerized Biological Systems

6.5. Japan: Legacy of Johkasou Systems and MBR Innovation

6.6. Saudi Arabia: Strategic Investment in MBR Systems for Water Reuse

6.7. Other Countries Analyzed

6.7.1. North America (Canada, Mexico)

6.7.2. Europe (UK, France, Spain, Italy, Russia, Rest of Europe)

6.7.3. Asia Pacific (South Korea, Australia, South East Asia, Rest of Asia)

6.7.4. South America (Brazil, Argentina, Rest of South America)

6.7.5. Middle East and Africa (UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

7. Biological Wastewater Treatment Market Size Outlook by Region (2025-2034)

7.1. North America Market Size Outlook to 2034

7.1.1. By Process Type

7.1.2. By Technology

7.1.3. By Application

7.2. Europe Market Size Outlook to 2034

7.2.1. By Process Type

7.2.2. By Technology

7.2.3. By Application

7.3. Asia Pacific Market Size Outlook to 2034

7.3.1. By Process Type

7.3.2. By Technology

7.3.3. By Application

7.4. South America Market Size Outlook to 2034

7.4.1. By Process Type

7.4.2. By Technology

7.4.3. By Application

7.5. Middle East and Africa Market Size Outlook to 2034

7.5.1. By Process Type

7.5.2. By Technology

7.5.3. By Application

8. Company Profiles: Leading Players in Biological Wastewater Treatment Industry

8.1. Veolia

8.2. SUEZ

8.3. Xylem Inc.

8.4. Evoqua Water Technologies

8.5. Pentair plc

8.6. DuPont de Nemours, Inc.

8.7. Toray Industries, Inc.

8.8. Aquatech International

8.9. Kubota Corporation

8.10. The Dow Chemical Company

8.11. V.A. TECH WABAG Ltd.

8.12. Mitsubishi Chemical Corporation

8.13. Kuraray Co., Ltd.

8.14. Ion Exchange (India) Ltd.

8.15. Thermax Limited

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures