Anaerobic Wastewater Treatment Systems Market Overview: Growth Outlook to 2034

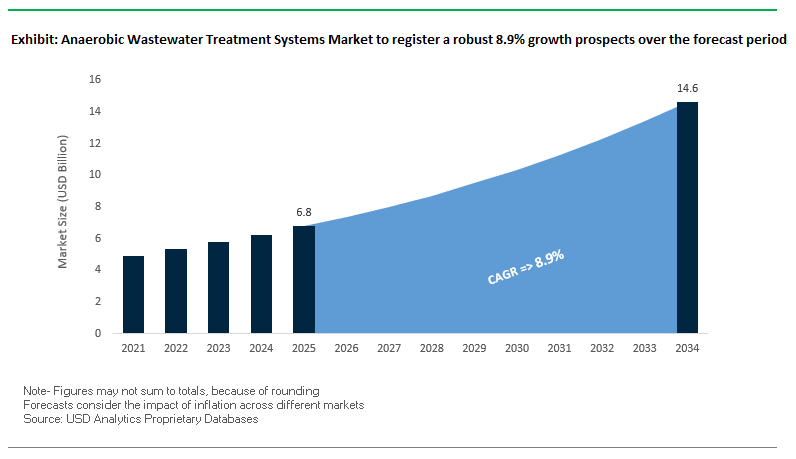

The anaerobic wastewater treatment systems market is projected to grow from USD 6.8 billion in 2025 to USD 14.6 billion by 2034, registering a robust CAGR of 8.9%. This high growth trajectory reflects the increasing global demand for energy-efficient, resource-recovering wastewater treatment technologies. Unlike conventional aerobic methods, anaerobic processes convert organic pollutants into biogas, offering a sustainable solution for industries with high-strength effluents, such as food and beverage, pulp and paper, and textiles.

Key Insights for Industry Stakeholders:

- Anaerobic digestion consistently reduces COD loads by over 90%, making it a proven technology for treating high-strength industrial wastewater.

- The food and beverage industry is the single largest adopter, using biogas recovery to offset a substantial share of onsite energy demand.

- Compared with aerobic methods, anaerobic processes generate up to 80% less sludge, drastically cutting disposal and handling costs.

- A single large-scale digester can produce biogas equivalent to the electricity needs of thousands of households, making it an attractive solution for industrial decarbonization and circular economy initiatives.

Market Analysis- Recent Market Developments Shaping the Outlook

The anaerobic wastewater treatment systems market is entering a transformative phase, driven by a convergence of sustainability imperatives, technological innovation, and regulatory compliance pressures. Industry leaders are increasingly integrating digital monitoring tools, advanced membrane technologies, and resource recovery pathways into conventional anaerobic processes, positioning wastewater not as waste but as a valuable resource for water reuse, energy generation, and zero liquid discharge (ZLD) initiatives. This evolution reflects a broader industrial paradigm shift where anaerobic systems are central to achieving operational efficiency, environmental stewardship, and cost-effective treatment solutions.

Strategic and Technological Milestones Shaping the Market

- DuPont Water Solutions – Leadership in Minimal Liquid Discharge: In August 2025, DuPont Water Solutions was recognized as part of the “Sustainability Squad” at the BIG Sustainability Awards, highlighting its leadership in advanced wastewater reuse and minimal liquid discharge (MLD) technologies. This accolade underscores the growing emphasis on integrating environmentally responsible technologies into industrial wastewater systems to reduce liquid waste and enhance sustainability reporting.

- Veolia Water Technologies – Expansion in Industrial Reuse: Veolia has strengthened its market presence through multiple strategic developments. In July 2025, the company was selected to supply equipment for France’s largest treated wastewater reuse project in Argelès-sur-Mer, where reclaimed water is directed toward agricultural irrigation, demonstrating the critical role of anaerobic systems in circular water economy models. Earlier, in May 2025, Veolia completed a full acquisition of its Water Technologies and Solutions subsidiary, consolidating its position as a global leader in sustainable industrial water treatment and signaling growing industry consolidation for scale and innovation.

- Kurita Water Industries – Pioneering Energy-Positive Treatment: In April 2025, Kurita Water Industries showcased the generation of electricity through microbial fuel cells powered by wastewater, marking a significant step toward energy-positive treatment plants. This milestone highlights the dual role of anaerobic systems in wastewater treatment and renewable energy production, offering industries both environmental and financial benefits.

- BIOFerm – Expanding Operations & Maintenance Services: BIOFerm expanded its portfolio in April 2025 with new Operations & Maintenance (O&M) services, facilitating broader adoption of anaerobic digestion technologies for both energy recovery and waste management. The move reflects the increasing demand for end-to-end service models that enhance system reliability, reduce operational downtime, and maximize resource recovery.

- Breakthroughs in Advanced Membranes and Nanotechnology: Academic and industrial research is driving innovations in membrane-based and nanoparticle-enabled treatments. In January 2025, the Journal of Membrane Science reported advanced nanofiber membranes capable of removing arsenic and lead, a breakthrough that enhances the safety and scalability of industrial wastewater reuse. Complementing this, December 2024 research demonstrated the use of engineered nanoparticles for cost-efficient heavy metal removal from produced water, providing scalable solutions for industries with complex effluents.

- Global Infrastructure Expansion – Scaling MLD Facilities: In October 2024, China’s Da Tang Industrial Park inaugurated a minimal liquid discharge facility treating 160,000 m³/day of textile wastewater, emphasizing the centrality of anaerobic processes in sustainable manufacturing and large-scale industrial water management. This reflects the trend of leveraging anaerobic technologies as foundational components in high-volume, resource-efficient wastewater treatment strategies.

Market Trends Shaping Anaerobic Wastewater Treatment Systems

Policy and Financial Incentives for Resource Recovery

The anaerobic wastewater treatment systems market is increasingly influenced by government-led policies and financial incentives that emphasize resource recovery. In India, the implementation of the Liquid Waste Management Rules from 2025 expands regulatory coverage to industrial and commercial wastewater generators, promoting treatment and reuse. Complementary policies such as the National Water Policy and financial mechanisms like the Hybrid Annuity Model (HAM) for sewage projects help de-risk capital-intensive anaerobic system investments. In Europe, reports from the European Biogas Association highlight that industrial wastewater treatment enables biogas production, supporting climate neutrality goals by 2050. These regulatory frameworks and incentive structures are driving modernization and replacement of conventional wastewater plants, creating significant opportunities for environmentally sustainable and energy-efficient anaerobic systems.

Emergence of Advanced and Hybrid Reactor Technologies

Innovation in reactor technologies is redefining the anaerobic wastewater treatment market. Anaerobic Membrane Bioreactors (AnMBRs), as highlighted in a 2024 MDPI Water journal study, combine anaerobic biological treatment with membrane filtration to produce high-quality effluent while minimizing sludge output. These compact systems are highly suitable for urban and decentralized applications where space is limited. Academic publications from IWA Publishing in 2024 further reinforce that high-rate and membrane reactor technologies are making anaerobic processes viable in colder climates and for dilute wastewater streams. The adoption of such advanced and hybrid technologies is positioning anaerobic treatment as a competitive and sustainable solution for modern wastewater challenges.

Corporate Investment in Biogas and Biofertilizer Production

Corporate initiatives are increasingly leveraging anaerobic wastewater treatment for resource recovery and revenue generation. For instance, Jordan Dairy in Massachusetts partners with local food companies to co-digest organics, generating 2.24 million kWh annually enough to power the farm and hundreds of homes. Similarly, Gills Onions saves approximately US$700,000 yearly by utilizing biogas from its wastewater. Municipal wastewater plants are also following this trend; the Greater Lawrence Sanitary District invested in an additional digester to co-digest food waste with sludge, aiming to produce 3.2 MW of electricity and biofertilizers for sale. These examples demonstrate how anaerobic systems are being integrated into commercial and municipal operations, offering both economic and environmental returns.

Market Share Analysis of Anaerobic Wastewater Treatment Systems

UASB Leads While High-Rate and Hybrid Reactors Gain Traction

In 2025, Upflow Anaerobic Sludge Blanket (UASB) reactors are projected to dominate the market with 32.8% share, thanks to their simplicity, proven reliability, and adaptability to a wide range of wastewater streams. High-rate technologies, including Expanded Granular Sludge Bed (EGSB) and Internal Circulation (IC) reactors, are capturing increasing market share at 22.5% and 16.9%, respectively, driven by compact designs and high organic loading capacity that suit modern industrial installations. Other technologies such as Anaerobic Filters (AF), Covered Anaerobic Lagoons (CAL), Anaerobic Baffled Reactors (ABR), and Anaerobic Sequencing Batch Reactors (ASBR) serve niche applications including high-solids wastewater, low-cost large-volume treatment, decentralized setups, and variable-flow wastewater highlighting the need for tailored reactor solutions across diverse operational environments.

Industrial Applications Dominate While Municipal and Agricultural Segments Expand

By application, industrial wastewater treatment dominates with 68% share, leveraging high-strength organic effluents from food & beverage, pulp & paper, and chemical industries that are ideal for anaerobic digestion and biogas recovery. Municipal wastewater treatment, accounting for 22.5%, focuses on sludge stabilization, with growing use for mainstream treatment in warmer climates where microbial activity supports higher efficiency. The agricultural segment, projected at 8–12%, offers significant opportunities by treating livestock manure and agro-processing wastewater, generating renewable energy and biofertilizers, and transforming waste streams into sustainable resources for the circular economy.

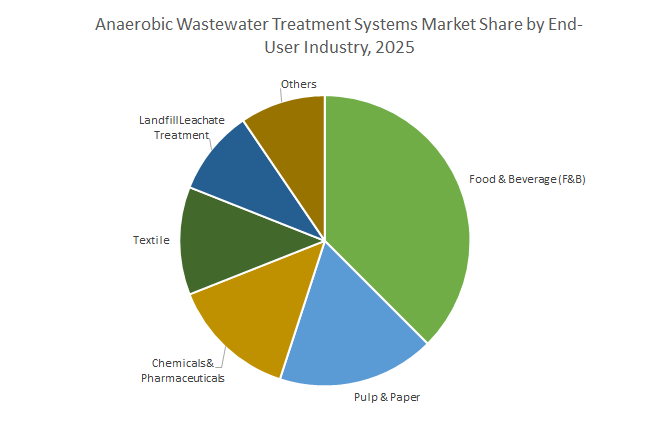

Food & Beverage Anchors Market While Specialized Industries Present High-Value Opportunities

Among end-user industries, Food & Beverage leads with 35.7% share, driven by high COD/BOD, biodegradable wastewater streams that deliver high biogas yields and operational savings. Pulp & Paper (16.9%) and Landfill Leachate Treatment are well-established sectors utilizing anaerobic systems for efficient wastewater stabilization and energy recovery. Chemicals & Pharmaceuticals (12–16%) and Textile (10–14%) represent complex but high-value markets, requiring specialized pre-treatment and advanced reactor technologies, yet offering substantial benefits in energy recovery, operational efficiency, and regulatory compliance.

China: Policy-Driven Adoption of High-Rate Anaerobic Reactors

China’s anaerobic wastewater treatment market is witnessing robust growth, driven by stringent government regulations, large-scale infrastructure investments, and technological advancements. The Ministry of Ecology and Environment (MEE) enforces strict industrial wastewater discharge standards, motivating industries to adopt high-efficiency anaerobic digestion systems. The 14th Five-Year Plan emphasizes water reuse, targeting 95% wastewater treatment coverage in county-level cities, which has created strong demand for anaerobic technologies capable of handling high-strength industrial waste. Significant government investment in wastewater infrastructure, often structured through Public-Private-Partnership (PPP) models, supports large-scale deployment. Technological advancements include high-rate anaerobic reactors and integrated membrane solutions, coupled with global leadership in sewage sludge reuse. Key applications focus on treating high-organic-load wastewater from food and beverage, pulp and paper, and pharmaceutical industries while producing renewable biogas for energy recovery.

United States: Government Grants and Industrial Energy Recovery Boost Market Expansion

The United States market for anaerobic wastewater treatment systems is fueled by government funding, regulatory oversight, and corporate initiatives. The EPA supports expansion of anaerobic digester capacity to reduce food waste, while USDA’s Rural Energy for America Program (REAP) provides grants and loan guarantees for on-farm digester installations. Emerging regulations targeting PFAS discharges are complementing AOP technologies, with anaerobic digestion serving as an essential pretreatment for complex industrial waste streams. Corporate innovations, such as the Evoqua Water Technologies-Xylem merger, have broadened the U.S. market’s anaerobic capabilities. Projects like the East County Advanced Water Purification facility in Santee, California, illustrate large-scale applications where anaerobic digestion converts sludge into renewable biogas, supporting energy self-sufficiency and sustainable wastewater management. Key applications include high-strength industrial effluent treatment, energy recovery, and landfill diversion programs.

India: Mission-Driven Growth in Anaerobic Wastewater Management

India’s anaerobic wastewater treatment systems market is expanding due to government initiatives, regulatory mandates, corporate expertise, and technological advancements. National programs like Jal Jeevan Mission, Namami Gange, and Swachh Bharat Mission-Urban (SBM-U 2.0) are driving the adoption of advanced wastewater treatment technologies, including anaerobic digestion. Regulatory enforcement by CPCB and SPCBs has mandated Zero Liquid Discharge (ZLD) in industrial clusters, with over 400 ZLD systems installed by 2023, many utilizing anaerobic modules. Corporates such as VA Tech Wabag lead large-scale municipal and industrial projects, while Ion Exchange (India) Ltd., in partnership with TERI, has commercialized advanced oxidation technologies often integrated with anaerobic processes for enhanced performance. Key applications focus on treating high-strength industrial wastewater, improving municipal sewage management, and enabling energy recovery from organic waste streams.

Germany: EU Regulations and AI-Enabled Operations Driving Anaerobic Adoption

Germany’s anaerobic wastewater treatment market is influenced by strict EU regulations, technological innovation, and corporate leadership. The revised EU Urban Wastewater Treatment Directive (January 2025) requires the "4th purification stage" in wastewater treatment plants, creating opportunities for anaerobic digestion as an effective pretreatment step. Cities are increasingly adopting AI, digital twins, and advanced monitoring systems for optimized operations of anaerobic digesters. Companies like H2O GmbH and GEA Group AG are pivotal in ZLD and industrial wastewater management, offering sustainable solutions that include anaerobic processes. Key applications focus on treating complex effluents from the food, beverage, and chemical industries while meeting stringent environmental standards.

Brazil: Integrated River Basin Planning Enhances Anaerobic Treatment Potential

Brazil’s anaerobic wastewater treatment market is evolving due to policy shifts, infrastructure investments, and resource recovery opportunities. The government promotes integrated river basin planning approaches, moving beyond isolated solutions to sustainable, resilient systems. Development banks such as the World Bank support initiatives that enhance wastewater treatment capacity while leveraging organic waste for energy recovery. Key applications include treatment of industrial wastewater, particularly from food and beverage sectors, and the generation of renewable biogas, positioning anaerobic digestion as a strategic component of Brazil’s energy and environmental strategy.

Japan: MBR Integration and Biogas Reuse Expand Market Opportunities

Japan’s anaerobic wastewater treatment market is propelled by academic research, corporate R&D, and government programs. The MLIT’s "Advance of Japan Ultimate Membrane bioreactor technology Project (A-JUMP)" promotes widespread adoption of MBRs, forming the foundation for anaerobic membrane bioreactors (AnMBRs). Companies like Toray Industries Inc. lead innovation in membrane technologies integrated with anaerobic processes, enhancing treatment efficiency for industrial and municipal wastewater. The market also emphasizes the beneficial reuse of biogas generated through anaerobic digestion, including applications in natural gas-powered vehicles. Key applications include high-strength industrial effluent management, municipal wastewater treatment, and renewable energy generation from organic waste streams.

Competitive Landscape: Key Companies in the Anaerobic Wastewater Treatment Systems Market

The competitive dynamics of the anaerobic wastewater treatment systems industry are defined by global leaders, niche technology providers, and innovators leveraging advanced science for sustainability. Companies are competing not only on treatment efficiency but also on their ability to enable biogas recovery, ZLD compliance, and digital optimization for industrial clients. Below is a detailed look at leading market players:

Paques B.V. – Pioneering High-Rate Anaerobic Technologies

Paques is a recognized pioneer in biological wastewater treatment with a legacy of more than six decades. Its flagship technology, BIOPAQ®IC, is widely adopted for treating industrial effluents with high organic loads. With over 3,400 installations in 60+ countries, Paques is trusted for its compact, energy-efficient systems. Recently, the company has advanced into resource recovery by exploring polyhydroxyalkanoates (PHA) production from wastewater, aligning with the circular economy. Its strategic vision, “Resource Tomorrow,” positions Paques as a leader in reclaiming biogas and nutrients while reducing environmental footprints.

Veolia Water Technologies – Driving Large-Scale Industrial Adoption

Veolia is a global leader in ecological transformation, offering end-to-end wastewater solutions across industries. Its strength lies in integrating advanced anaerobic systems such as Sparthane® technology with broader water reuse and MLD platforms. In May 2025, Veolia strengthened its position by acquiring full ownership of its Water Technologies and Solutions business, allowing streamlined delivery of sustainable systems worldwide. Veolia’s strategic plan, “GreenUp,” reflects its commitment to decarbonization, water reuse, and climate resilience, making it one of the most influential players in this space.

SUEZ Water Technologies & Solutions – Customized Resource Recovery Solutions

SUEZ specializes in delivering customized anaerobic digestion systems tailored for both industrial and municipal sectors. Its Degremont brand technologies are globally recognized for excellence in water and wastewater treatment. The company is actively executing contracts in Asia, including a large-scale facility in China targeting 100% wastewater recycling. By integrating predictive analytics and digital control, SUEZ enhances plant efficiency, lowers fouling, and reduces operational costs. Its focus on turning sewage sludge into renewable energy reflects a strong commitment to resource recovery and circular economy practices.

Xylem Inc. – Integrated Water Solutions with Digital Edge

Xylem is a global water technology powerhouse with a comprehensive portfolio spanning pumps, biological treatment, analytics, and controls. The company’s landmark acquisition of Evoqua in 2023 expanded its capabilities in anaerobic wastewater treatment and reuse. Xylem’s solutions cover the full water cycle, making it a preferred partner for municipalities and industries alike. Its ongoing investments in IoT and predictive maintenance platforms provide customers with real-time insights, boosting performance and ensuring system reliability during peak events such as stormwater surges.

DuPont Water Solutions – Innovating with Advanced Membranes

DuPont applies its materials science expertise to develop high-performance membranes that support water reuse and wastewater concentration. Its FilmTec™ brand remains the industry benchmark for reverse osmosis and nanofiltration membranes. In 2025, DuPont received the prestigious R&D 100 Award for its FilmTec™ Fortilife™ XC160 Membrane, designed to enable more sustainable concentration of wastewater streams. By combining membranes, ultrafiltration, and ion exchange resins, DuPont delivers integrated solutions that help industries achieve water circularity, lower carbon footprints, and compliance with stricter reuse standards.

Anaerobic Wastewater Treatment Systems Market Report Scope

Anaerobic Wastewater Treatment Systems Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.8 Billion

|

|

Market Size (2034)

|

$14.6 Billion

|

|

Market Growth Rate

|

8.9%

|

|

Segments

|

By Technology/Reactor Type (Upflow Anaerobic Sludge Blanket, Expanded Granular Sludge Bed, Anaerobic Filters, Anaerobic Baffled Reactor, Internal Circulation Reactor, Anaerobic Sequencing Batch Reactor, Covered Anaerobic Lagoon), By Application (Industrial Wastewater Treatment, Municipal Wastewater Treatment, Agricultural Wastewater Treatment), By End-User Industry (Food & Beverage, Pulp & Paper, Chemicals & Pharmaceuticals, Textile, Landfill Leachate Treatment), By System Capacity (Small-scale, Medium-scale, Large-scale), By Offering (Engineering, Design, and Construction, Treatment Systems & Reactors, Biogas Recovery & Utilization Systems, Operation & Maintenance Services)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia, SUEZ, Xylem Inc., Evoqua Water Technologies, DuPont de Nemours, Inc., Alfa Laval, Toray Industries, Inc., Aquatech International, Kubota Corporation, The Dow Chemical Company, VA Tech Wabag Ltd., Mitsubishi Chemical Corporation, Kurita Water Industries Ltd., Anaergia Inc., Fluence Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Anaerobic Wastewater Treatment Systems Market Segmentation

By Technology/Reactor Type

- Upflow Anaerobic Sludge Blanket (UASB)

- Expanded Granular Sludge Bed (EGSB)

- Anaerobic Filters (AF)

- Anaerobic Baffled Reactor (ABR)

- Internal Circulation (IC) Reactor

- Anaerobic Sequencing Batch Reactor (ASBR)

- Covered Anaerobic Lagoon (CAL)

By Application

- Industrial Wastewater Treatment

- Municipal Wastewater Treatment

- Agricultural Wastewater Treatment

By End-User Industry

- Food & Beverage

- Sugar & Ethanol

- Breweries & Distilleries

- Dairy

- Starch & Glucose

- Meat & Poultry Processing

- Pulp & Paper

- Chemicals & Pharmaceuticals

- Textile

- Landfill Leachate Treatment

By System Capacity

- Small-scale (< 100 m³/day)

- Medium-scale (100 - 10,000 m³/day)

- Large-scale (> 10,000 m³/day)

By Offering

- Engineering, Design, and Construction

- Treatment Systems & Reactors

- Biogas Recovery & Utilization Systems

- Operation & Maintenance Services

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Anaerobic Wastewater Treatment Systems Industry include-

- Veolia

- SUEZ

- Xylem Inc.

- Evoqua Water Technologies

- DuPont de Nemours, Inc.

- Alfa Laval

- Toray Industries, Inc.

- Aquatech International

- Kubota Corporation

- The Dow Chemical Company

- VA Tech Wabag Ltd.

- Mitsubishi Chemical Corporation

- Kurita Water Industries Ltd.

- Anaergia Inc.

- Fluence Corporation

*- List not Exhaustive

Research Coverage – USDAnalytics

This report investigates the global anaerobic wastewater treatment systems market, highlighting its evolution as a sustainable and energy-positive solution across industrial, municipal, and agricultural applications. The report offers an in-depth analysis of market breakthroughs, including cutting-edge hybrid reactor technologies, policy-driven adoption trends, and real-world use cases showcasing biogas recovery and operational efficiency. It reviews recent developments from companies such as Veolia, SUEZ, Xylem, DuPont, Kurita, and Anaergia, placing them within the context of evolving regulatory landscapes and circular economy initiatives. This report is an essential resource for decision-makers, technology providers, and environmental engineers seeking to align with the next generation of zero-liquid discharge (ZLD) systems and decentralized wastewater management. With rich data insights and expert analysis, USDAnalytics provides a complete strategic outlook for stakeholders aiming to capture opportunities in biogas production, membrane bioreactor integration, and sludge minimization via anaerobic treatment. Scope Includes-

- Segmentation: By Technology (UASB, EGSB, ABR, etc.), Application (Industrial, Municipal, Agricultural), End-Use (Food & Beverage, Pulp & Paper, Chemicals, etc.), System Capacity, and Offering

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Frame: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies Covered: Analysis/profiles of 15+ companies, including Veolia, SUEZ, Xylem Inc., DuPont, Evoqua, Alfa Laval, Toray, Kubota, Dow, VA Tech Wabag, Mitsubishi Chemical, Kurita, Anaergia, Fluence, and Aquatech.

Methodology

The research methodology applied in this report by USDAnalytics integrates primary and secondary data collection, market triangulation, and advanced forecasting techniques. Primary insights were gathered from structured interviews with industry experts, technology developers, EPC contractors, and utility managers. Secondary research involved the analysis of government policy documents (e.g., EU Urban Wastewater Directive, India’s Jal Jeevan Mission), academic journals (e.g., MDPI, Journal of Membrane Science), and company reports. Market estimates and projections from 2025 to 2034 are developed using bottom-up modeling, adjusted for regional policy scenarios, technological adoption rates, and sectoral investment flows. A special focus was placed on segment-specific demand drivers, competitive benchmarking, and regional case studies to validate our models and ensure accurate, actionable insights.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Anaerobic Wastewater Treatment Systems Market

1. Executive Summary

1.1. Market Highlights and Key Projections

1.2. Key Insights for Industry Stakeholders

1.3. Global Market Snapshot

1.3.1. Current Market Valuation (2025): USD 6.8 Billion

1.3.2. Projected Market Valuation (2034): USD 14.6 Billion

1.3.3. Compound Annual Growth Rate (CAGR): 8.9%

2. Market Outlook (2025–2034)

2.1. Introduction: Growth, Drivers, and Key Challenges

2.2. Market Valuation and Growth Projections (2025–2034)

2.3. Key Market Trends Driving Anaerobic System Adoption

2.3.1. Policy and Financial Incentives for Resource Recovery

2.3.2. Emergence of Advanced and Hybrid Reactor Technologies (e.g., AnMBRs)

2.3.3. Corporate and Municipal Investment in Biogas and Biofertilizer Production

2.3.4. Integration of Digital Twins and AI for Optimized Operations

3. Innovations and Strategic Developments Redefining the Market

3.1. Market Analysis: Recent Developments and Strategic Shifts

3.1.1. Strategic Acquisitions and Consolidation (Veolia, Xylem)

3.1.2. Pioneering Energy-Positive Treatment (Kurita Water Industries)

3.1.3. Expansion of Operations & Maintenance Services (BIOFerm)

3.1.4. Breakthroughs in Advanced Membranes and Nanotechnology

3.1.5. Large-Scale Infrastructure Expansion (China's Da Tang Industrial Park)

3.1.6. Global Infrastructure Expansion and Project Announcements (EnviTec Biogas, Xylem)

4. Competitive Landscape: Leading Companies

4.1. Market Overview: Global Leaders and Innovative Specialists

4.2. Strategic Profiles of Key Companies

4.2.1. Paques B.V.: Pioneering High-Rate Anaerobic Technologies

4.2.2. Veolia Water Technologies: Driving Large-Scale Industrial Adoption

4.2.3. SUEZ Water Technologies & Solutions: Customized Resource Recovery Solutions

4.2.4. Xylem Inc.: Integrated Water Solutions with a Digital Edge

4.2.5. DuPont Water Solutions: Innovating with Advanced Membranes

4.2.6. Kurita Water Industries Ltd.

4.2.7. VA Tech Wabag Ltd.

4.2.8. Anaergia Inc.

4.2.9. Fluence Corporation

5. Anaerobic Wastewater Treatment Market Segmentation Insights

5.1. By Technology/Reactor Type

5.1.1. Upflow Anaerobic Sludge Blanket (UASB)

5.1.2. Expanded Granular Sludge Bed (EGSB)

5.1.3. Internal Circulation (IC) Reactor

5.1.4. Anaerobic Filters (AF)

5.1.5. Anaerobic Baffled Reactor (ABR)

5.1.6. Anaerobic Sequencing Batch Reactor (ASBR)

5.1.7. Covered Anaerobic Lagoon (CAL)

5.2. By Application

5.2.1. Industrial Wastewater Treatment

5.2.2. Municipal Wastewater Treatment

5.2.3. Agricultural Wastewater Treatment

5.3. By End-User Industry

5.3.1. Food & Beverage

5.3.2. Pulp & Paper

5.3.3. Chemicals & Pharmaceuticals

5.3.4. Textile

5.3.5. Landfill Leachate Treatment

5.4. By System Capacity

5.4.1. Small-scale (< 100 m³/day)

5.4.2. Medium-scale (100 - 10,000 m³/day)

5.4.3. Large-scale (> 10,000 m³/day)

5.5. By Offering

5.5.1. Engineering, Design, and Construction

5.5.2. Treatment Systems & Reactors

5.5.3. Biogas Recovery & Utilization Systems

5.5.4. Operation & Maintenance Services

6. Country Analysis and Outlook

6.1. China: Policy-Driven Adoption of High-Rate Anaerobic Reactors

6.2. United States: Government Grants and Industrial Energy Recovery

6.3. India: Mission-Driven Growth in Anaerobic Wastewater Management

6.4. Germany: EU Regulations and AI-Enabled Operations

6.5. Brazil: Integrated River Basin Planning and Policy Shifts

6.6. Japan: MBR Integration and Biogas Reuse

6.7. Other Countries Analyzed

6.7.1. North America (Canada, Mexico)

6.7.2. Europe (UK, France, Spain, Italy, Russia, Rest of Europe)

6.7.3. Asia Pacific (South Korea, Australia, South East Asia, Rest of Asia)

6.7.4. South America (Argentina, Rest of South America)

6.7.5. Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

7. Market Size Outlook by Region (2025-2034)

7.1. North America Market Size Outlook to 2034

7.1.1. By Technology

7.1.2. By Application

7.1.3. By End-User Industry

7.2. Europe Market Size Outlook to 2034

7.2.1. By Technology

7.2.2. By Application

7.2.3. By End-User Industry

7.3. Asia Pacific Market Size Outlook to 2034

7.3.1. By Technology

7.3.2. By Application

7.3.3. By End-User Industry

7.4. South America Market Size Outlook to 2034

7.4.1. By Technology

7.4.2. By Application

7.4.3. By End-User Industry

7.5. Middle East and Africa Market Size Outlook to 2034

7.5.1. By Technology

7.5.2. By Application

7.5.3. By End-User Industry

8. Company Profiles: Leading Players

8.1. Veolia

8.2. SUEZ

8.3. Xylem Inc.

8.4. DuPont de Nemours, Inc.

8.5. Paques B.V.

8.6. Kurita Water Industries Ltd.

8.7. VA Tech Wabag Ltd.

8.8. Anaergia Inc.

8.9. Fluence Corporation

8.10. Evoqua Water Technologies

8.11. Trojan Technologies

8.12. H2O GmbH

8.13. Other Prominent Players

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures