Global Heavy Metal Removal Systems Market Overview: Market Value, Growth Outlook

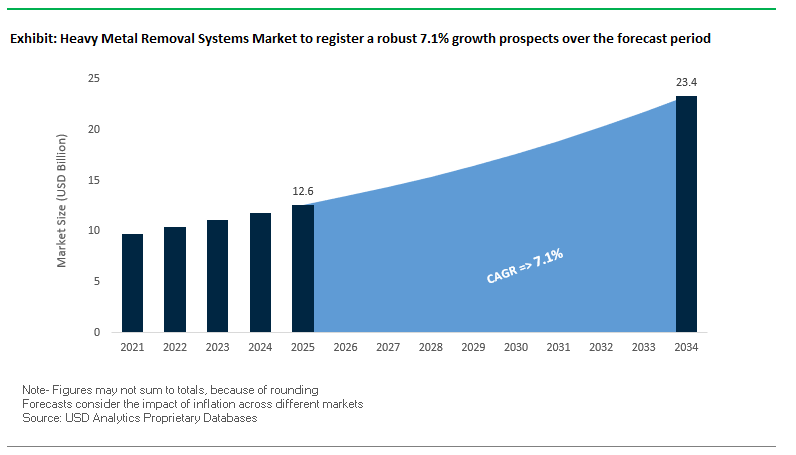

The global heavy metal removal systems market is projected to expand from USD 12.6 billion in 2025 to USD 23.4 billion by 2034, reflecting a strong CAGR of 7.1%. This growth is fueled by rapid industrialization, rising water stress, and stringent environmental regulations requiring industries to mitigate toxic discharges. Heavy metals such as lead, mercury, cadmium, and arsenic are among the most hazardous contaminants, with long-term implications for public health, agriculture, and ecosystems. Industrial and mining effluents are the largest contributors, creating demand for advanced systems capable of treating acid mine drainage (AMD), high-salinity wastewater, and effluent streams from manufacturing.

Key Insights for Industry Stakeholders:

- Industrial and mining sectors are the dominant sources of heavy metal contamination, creating long-term demand for treatment technologies.

- Asia-Pacific is the fastest-growing region, with China and India enforcing stricter regulations and promoting water reuse initiatives.

- Mining operations, particularly lithium and copper extraction, face critical challenges with water usage and heavy metal effluents.

- Water reuse and zero liquid discharge systems are becoming standard in industrial clusters, creating opportunities for integrated solutions providers.

Market Analysis: Recent Developments and Industry Shifts

The heavy metal removal systems market is undergoing rapid transformation, shaped by technological advancements, regulatory reforms, and corporate consolidation. A steady stream of breakthroughs in membranes, ion-exchange resins, advanced oxidation, and nanomaterials is redefining how industrial wastewater is treated. Moreover, sustainability frameworks particularly in the EU and Asia are increasing the responsibility of industries to internalize treatment costs.

A closer look at the last 12 months reveals several important developments. In August 2025, DuPont Water Solutions was recognized in the BIG Sustainability Awards for innovations in wastewater reuse and MLD, reinforcing its position as a leader in sustainable treatment. In July 2025, Veolia Water Technologies secured France’s largest treated wastewater reuse project, marking a milestone in large-scale reclamation for agriculture. Meanwhile, in May 2025, Veolia finalized its acquisition of full ownership of Water Technologies and Solutions from CDPQ, consolidating its global footprint in water technology for mining and manufacturing. Another highlight came in April 2025, when Kurita Water Industries demonstrated a microbial fuel cell that generates electricity from wastewater, signaling a shift toward energy-positive treatment systems.

Policy changes are also reshaping the market. In March 2025, the European Union’s Urban Wastewater Treatment Directive introduced Extended Producer Responsibility (EPR), requiring pharmaceutical and cosmetic companies to fund the removal of micropollutants including heavy metals from wastewater. On the innovation front, January 2025 saw the introduction of a nanofiber membrane effective in arsenic and lead removal, while December 2024 brought forward scientific validation of engineered nanoparticles for produced water treatment. Notably, in October 2024, China launched a large-scale MLD wastewater plant in Foshan, with a treatment capacity of 160,000 m³/day, offering a blueprint for other industrial regions facing water scarcity and contamination challenges.

Key Market Trends Shaping Heavy Metal Removal

Stricter Regulations and Intensified Regulatory Scrutiny

Regulatory frameworks are a primary growth driver in the heavy metal removal systems market. The U.S. Environmental Protection Agency (EPA) continues to strengthen Effluent Guidelines for industries such as metal finishing and electroplating, targeting emerging contaminants like PFAS linked to chromium emissions (Preliminary Plan #16, 2024). Similarly, India’s Central Pollution Control Board (CPCB) has mandated heavy metal and antibiotic residue monitoring for pharmaceutical and metal-processing facilities. These regulations, combined with mandatory Zero Liquid Discharge (ZLD) initiatives, compel industries to adopt advanced treatment systems, driving substantial market expansion.

Adoption of Advanced and Selective Treatment Technologies

The market is witnessing a shift toward sophisticated technologies capable of selective heavy metal removal. Capacitive deionization (CDI) devices, leveraging machine learning and X-ray analysis, have demonstrated highly efficient lead removal, highlighting the move toward precision treatment. Additionally, membrane filtration systems (ultrafiltration, nanofiltration, reverse osmosis) and adsorption with novel media are widely applied for high-purity water production. Emerging technologies like photocatalysis further offer simultaneous removal of organic pollutants and metals, signaling a trend toward multi-functional, cost-effective treatment solutions.

Integration of Resource Recovery and Circular Economy Principles

Mining and industrial companies are increasingly focusing on recovering valuable metals from wastewater streams. Case studies from South American mining operations highlight investments exceeding $20 million in facilities designed to treat acidic effluents while recovering zinc and copper for reintroduction into production cycles. Biosorption, utilizing algae, fungi, and other biological materials, is gaining traction as an eco-friendly, low-cost solution with potential for metal recovery and chemical sludge minimization. These initiatives demonstrate the growing importance of integrating sustainability and profitability in heavy metal removal strategies.

Heavy Metal Removal Systems Market Share Insights

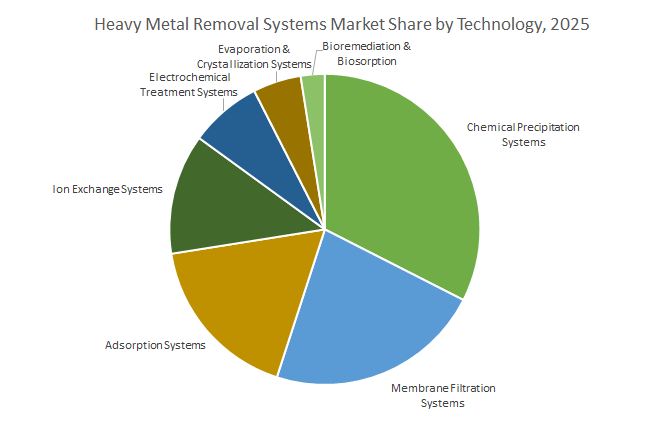

By Technology: Chemical Precipitation Dominates, Membrane and Adsorption Growing

Chemical Precipitation Systems (32.8%) remain the largest segment due to their cost-effectiveness, high capacity, and reliability in treating industrial wastewater containing high metal loads. Membrane Filtration Systems (24.6%) are the fastest-growing segment, driven by stringent discharge limits and high-purity water reuse applications. Adsorption Systems (16.9%) provide effective polishing for low-concentration metals, while Ion Exchange Systems (11.8%) are valued for selective removal of specific metals like chromium (VI) and nickel. Electrochemical Treatment and Evaporation & Crystallization represent a niche, eco-friendly segment for targeted applications. The technology mix reflects a balance between cost-efficiency, operational scalability, and strategic resource recovery.

By Heavy Metal Treated: Lead and Arsenic Drive Market Focus

Lead (Pb) (24.6%) dominates due to severe neurotoxic impacts and extensive investment in municipal drinking water remediation. Arsenic (As) (21.2%) is a critical groundwater contaminant, particularly in South Asia and the Americas, driving large-scale municipal treatment projects. Mercury (Hg) (17.3%) and Chromium (Cr) (14.8%) are primarily regulated in industrial discharges, including coal-fired power plants, metal plating, and chemical manufacturing. Copper (Cu) & Zinc (Zn) are common in industrial wastewater streams, often treated together via precipitation, while Cadmium (Cd) & Nickel (Ni) are targeted for specialized industrial applications like electroplating and battery manufacturing. The distribution emphasizes how public health concerns, regulatory requirements, and industrial prevalence guide the allocation of market resources.

China: Stringent Regulations and Advanced Membrane Technologies Driving Market Growth

China’s heavy metal removal systems market is strongly influenced by strict regulatory policies and government initiatives aimed at controlling industrial wastewater discharge. The Ministry of Ecology and Environment (MEE) enforces stringent standards, with the 14th Five-Year Plan targeting 95% wastewater treatment for all county-level cities, creating substantial demand for biological treatment infrastructure. Technological advancements are led by the Chinese Academy of Sciences, which developed a dual-functional reverse osmosis (RO) membrane with enhanced antibacterial and anti-adhesion properties, optimizing heavy metal removal in pharmaceutical and industrial wastewater. Government investments of $50 billion by 2025 across chemicals, steel, and pharmaceutical sectors are further accelerating market adoption. Key applications include membrane filtration and adsorption systems for municipal and industrial wastewater treatment projects focused on high-efficiency heavy metal removal with compact footprints.

United States: PFAS Regulations and ZLD Technologies Boost Heavy Metal Treatment

In the United States, the heavy metal removal systems market is driven by government funding, regulatory oversight, and corporate innovation. The Bipartisan Infrastructure Law allocates over $50 billion to the EPA for improving water infrastructure, including treatment of emerging contaminants like PFAS, often coupled with heavy metal-laden waste streams. The National Alliance for Water Innovation (NAWI) is developing new membranes to reduce energy costs for waste-brine and ZLD systems in industrial facilities. Companies such as Veolia Water Technologies and Evoqua Water Technologies are deploying biological treatment solutions and membrane-based systems to ensure regulatory compliance. The market emphasizes recovery and reuse of valuable metals from complex wastewater streams in chemical, pharmaceutical, and industrial production.

India: ZLD Mandates and Government Missions Fuel Industrial Wastewater Solutions

India’s heavy metal removal systems market is shaped by strict regulatory frameworks, government programs, and corporate projects. The Central Pollution Control Board (CPCB) and National Green Tribunal (NGT) have mandated Zero Liquid Discharge (ZLD) for water-scarce industrial regions, particularly in chemical and pharmaceutical sectors. Government initiatives like the "Jal Jeevan Mission," "Namami Gange Mission," and "Smart Cities Mission" are driving widespread deployment and modernization of wastewater treatment plants. Companies such as VA Tech Wabag are implementing large-scale industrial wastewater solutions domestically and abroad. Technological advancements under the Department of Pharmaceuticals’ RPTUAS program support high-efficiency treatment of wastewater containing heavy metals from APIs, bulk drugs, and formulations.

Germany: EU Directives and Digital Water Management Propel Advanced Heavy Metal Removal

Germany’s heavy metal removal systems market benefits from strict EU regulations, technological innovation, and corporate expertise. The revised Urban Wastewater Treatment Directive (January 2025) mandates a "4th purification stage," encouraging adoption of advanced oxidation and membrane filtration techniques to eliminate heavy metals. German firms such as H2O GmbH and GEA Group AG are leading in ZLD solutions, while Veolia’s technologies have transformed pharmaceutical wastewater plants, achieving significant carbon emissions reductions. The Federal Environment Agency (UBA) highlights widespread adoption of AI-driven monitoring, digital twins, and climate-adaptive water management, which optimize heavy metal removal processes. The chemical and pharmaceutical industries remain key drivers for the market, demanding high-efficiency wastewater treatment solutions.

Australia: Environmental Stewardship and Virtual Curtain Technology Enhance Heavy Metal Removal

Australia’s heavy metal removal systems market is defined by stringent environmental policies and innovative water treatment technologies. State environment protection policies, such as the SEPP Waters of Victoria, establish strict guidelines to maintain water quality and protect beneficial uses. CSIRO developed the "Virtual Curtain" technology, which uses hydrotalcites to remove metal contaminants while producing minimal sludge compared to conventional methods. The market’s key applications focus on mining operations, particularly iron ore, coal, and precious metals, emphasizing perpetual water treatment solutions for mine closure and long-term environmental stewardship.

Japan: MBR and Advanced Membrane Technologies Leading Industrial Wastewater Treatment

Japan’s heavy metal removal systems market is driven by government initiatives, academic and corporate R&D, and technological advancements. The MLIT’s "Advance of Japan Ultimate Membrane bioreactor technology Project (A-JUMP)" promotes full-scale MBR penetration for industrial wastewater treatment. Toray Industries Inc. continues to innovate with high-efficiency separation membrane modules that double filtration performance while reducing clogging, making them ideal for pharmaceutical and industrial effluents. Key applications focus on nutrient recovery, water reuse, and electrochemical and adsorption methods for heavy metal removal, reinforcing Japan’s role as a leader in advanced industrial wastewater treatment technologies.

Competitive Landscape: Leading Players in Heavy Metal Removal Systems

The heavy metal removal systems market is defined by intense competition between multinational leaders, regional specialists, and emerging innovators. Companies are expanding portfolios, securing acquisitions, and investing in R&D to address the growing complexity of industrial effluents. Below is an overview of leading players shaping this market.

DuPont Water Solutions – Membrane Innovation Driving Advanced Heavy Metal Removal

DuPont leverages decades of expertise in materials science and membranes, positioning its FilmTec™ range as a benchmark in reverse osmosis (RO) and nanofiltration technologies. In 2025, DuPont’s FilmTec™ Fortilife™ XC160 Membrane won an R&D 100 Award for its ability to handle high-salinity wastewater, a common challenge in mining. Its portfolio, spanning RO, NF, ultrafiltration (UF), and ion exchange resins, enables integrated solutions for industries grappling with acid mine drainage and ZLD requirements. The company’s focus on sustainability and water circularity ensures that its technologies are embedded in over 112 countries, purifying more than 50 million gallons of water per minute.

Veolia Water Technologies – Expanding Global Leadership Through Integrated Solutions

Veolia is a global leader in ecological transformation, with comprehensive offerings from filtration to thermal crystallizers. Its May 2025 acquisition of Water Technologies and Solutions reflects its commitment to consolidating its technological leadership, especially in mining-heavy geographies. Veolia’s “GreenUp” strategy directly supports industries seeking sustainable, low-carbon wastewater treatment, while its expertise in design, construction, and O&M contracts strengthens long-term partnerships with industrial customers. Its role in France’s largest water reuse project in July 2025 highlights its strength in scaling sustainable water solutions.

SUEZ Water Technologies & Solutions – Customization and Digital Integration in Industrial Wastewater

SUEZ has built a reputation for tailored industrial wastewater treatment systems, with a strong emphasis on ZLD and micropollutant removal. Recent contract wins in Asia, including a major Chinese plant aiming for 100% wastewater recycling, highlight its competitive edge in emerging markets. Its portfolio blends biological, membrane, and oxidation technologies with predictive analytics platforms that optimize plant performance. By combining hardware with digital intelligence, SUEZ lowers fouling risks, reduces chemical use, and delivers measurable OPEX savings, positioning itself as a go-to provider for resource recovery-focused industries.

Evoqua Water Technologies LLC (Now Part of Xylem) – Strengthening North American Presence

Evoqua specializes in mission-critical water treatment, serving more than 38,000 customers worldwide. Its 2023 integration with Xylem has created a stronger combined entity with expanded capabilities for mining, municipal, and industrial sectors. Evoqua’s strength lies in industrial process water treatment and contaminant removal, and its new Sustainability and Innovation Hub in Pittsburgh is driving next-generation solutions for PFAS, heavy metals, and emerging contaminants. With 200,000 installations globally, Evoqua’s credibility in large-scale deployments remains unmatched in North America.

Kurita Water Industries – Chemical Expertise and Energy-Positive Wastewater Innovations

Kurita combines chemical solutions with equipment expertise, addressing difficult wastewater streams with advanced agents and customized treatment processes. In June 2024, it launched Kurita AquaChemie India Private Limited to tap into the rapidly growing Indian market for heavy metal removal. Notably, in April 2025, it showcased microbial fuel cell technology that generates power from wastewater, an innovation that blends energy recovery with water treatment. Kurita’s sustainability mission centers on minimizing discharges and improving water reuse efficiency, making it a trusted partner for industrial clients pursuing environmental compliance.

Heavy Metal Removal Systems Market Report Scope

Heavy Metal Removal Systems Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$12.6 Billion

|

|

Market Size (2034)

|

$23.4 Billion

|

|

Market Growth Rate

|

7.1%

|

|

Segments

|

By Technology (Chemical Precipitation Systems, Ion Exchange Systems, Membrane Filtration Systems, Adsorption Systems, Electrochemical Treatment Systems, Bioremediation & Biosorption Systems, Evaporation & Crystallization Systems), By Heavy Metal Treated (Arsenic, Lead, Mercury, Cadmium, Chromium, Nickel, Copper & Zinc), By Application (Municipal Drinking Water Treatment, Industrial Wastewater Treatment, Groundwater & Contaminated Site Remediation, Power Generation & Energy Sector, Food & Beverage Processing, Pharmaceutical & Biotechnology), By Treatment Mode (On-Site, Mobile, Centralized)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia, SUEZ, Xylem Inc., Evoqua Water Technologies, DuPont de Nemours, Inc., Pentair plc, Toray Industries, Inc., Aquatech International, Kubota Corporation, The Dow Chemical Company, V.A. TECH WABAG Ltd., Mitsubishi Chemical Corporation, Kurita Water Industries Ltd., Nalco Water (An Ecolab Company), Thermax Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Heavy Metal Removal Systems Market Segmentation

By Technology

- Chemical Precipitation Systems

- Ion Exchange Systems

- Membrane Filtration Systems

- Adsorption Systems

- Electrochemical Treatment Systems

- Bioremediation & Biosorption Systems

- Evaporation & Crystallization Systems

By Heavy Metal Treated

- Arsenic

- Lead

- Mercury

- Cadmium

- Chromium

- Nickel, Copper & Zinc

By Application

- Municipal Drinking Water Treatment

- Industrial Wastewater Treatment

- Groundwater & Contaminated Site Remediation

- Power Generation & Energy Sector

- Food & Beverage Processing

- Pharmaceutical & Biotechnology

By Treatment Mode

- On-Site

- Mobile

- Centralized

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Heavy Metal Removal Systems Industry include-

- Veolia

- SUEZ

- Xylem Inc.

- Evoqua Water Technologies

- DuPont de Nemours, Inc.

- Pentair plc

- Toray Industries, Inc.

- Aquatech International

- Kubota Corporation

- The Dow Chemical Company

- V.A. TECH WABAG Ltd.

- Mitsubishi Chemical Corporation

- Kurita Water Industries Ltd.

- Nalco Water (An Ecolab Company)

- Thermax Limited

*- List not Exhaustive

Research Coverage

This report investigates the Heavy Metal Removal Systems Market from demand drivers to deployable treatment trains, and analysis reviews vendor capabilities, retrofit economics, and compliance pathways across municipal, industrial, and mining use cases. Compiled by USDAnalytics, it highlights breakthroughs in selective ion exchange, high-recovery membranes, electrochemical polishing, advanced oxidation, and resource-recovery adsorbents, while mapping the regulatory catalysts reshaping CAPEX/OPEX decisions. The study quantifies market sizing to 2034, benchmarks performance (removal efficiencies, brine ratios, sludge indices), and synthesizes purchase criteria for AMD, high-salinity, and mixed-contaminant effluents this report is an essential resource for utilities, EHS leaders, EPCs, investors, and OEMs planning resilient water strategies. Scope Includes-

- Segmentation

- By Technology: Chemical Precipitation Systems; Ion Exchange Systems; Membrane Filtration Systems; Adsorption Systems; Electrochemical Treatment Systems; Bioremediation & Biosorption Systems; Evaporation & Crystallization Systems

- By Heavy Metal Treated: Arsenic; Lead; Mercury; Cadmium; Chromium; Nickel, Copper & Zinc

- By Application: Municipal Drinking Water Treatment; Industrial Wastewater Treatment; Groundwater & Contaminated Site Remediation; Power Generation & Energy Sector; Food & Beverage Processing; Pharmaceutical & Biotechnology

- By Treatment Mode: On-Site; Mobile; Centralized

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Frame: Historic data 2021–2024 and forecasts 2025–2034.

- Companies (15+ profiles/analysis): Veolia; SUEZ; Xylem Inc.; Evoqua Water Technologies; DuPont de Nemours, Inc.; Pentair plc; Toray Industries, Inc.; Aquatech International; Kubota Corporation; The Dow Chemical Company; V.A. TECH WABAG Ltd.; Mitsubishi Chemical Corporation; Kurita Water Industries Ltd.; Nalco Water (An Ecolab Company); Thermax Limited.

Methodology

USDAnalytics integrates a bottom-up model of installed and planned systems (by flow, influent chemistry, and process train) with a top-down calibration to discharge permits, reuse targets, and sector output indices. We compiled pricing and performance from vendor RFQs, tenders, and 90+ expert interviews (utilities, miners, OEMs, EPCs, regulators). Tech benchmarking normalizes removal efficiency for Pb/As/Hg/Cr/Ni-Cu-Zn, specific energy (kWh·m⁻³), reagent dose, sludge yield, brine factor, media life, and recovery %. Scenario analysis stress-tests ZLD mandates, PFAS co-treatment, reagent/energy inflation, and water-stress indices to 2034, producing triangulated market sizes, shares, and TCO curves for greenfield, brownfield, and mobile deployments.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Heavy Metal Removal Systems Market

1. Executive Summary

1.1. Market Highlights and Key Projections

1.2. Key Insights for Industry Stakeholders

1.3. Global Market Snapshot

1.3.1. Current Market Valuation (2025): $12.6 Billion

1.3.2. Projected Market Valuation (2034): $23.4 Billion

1.3.3. Compound Annual Growth Rate (CAGR): 7.1%

2. Market Outlook (2025–2034)

2.1. Introduction: Growth, Drivers, and Key Challenges

2.2. Market Valuation and Growth Projections (2025–2034)

2.3. Key Market Trends Shaping Heavy Metal Removal

2.3.1. Stricter Regulations and Intensified Regulatory Scrutiny

2.3.2. Adoption of Advanced and Selective Treatment Technologies

2.3.3. Integration of Resource Recovery and Circular Economy Principles

3. Innovations and Strategic Developments Redefining the Market

3.1. Market Analysis: Recent Developments and Strategic Shifts

3.1.1. DuPont Water Solutions Recognized for MLD Innovations (August 2025)

3.1.2. Veolia Strengthens Global Leadership with Major Acquisition and Contracts (2025)

3.1.3. Kurita's Breakthrough in Energy-Positive Wastewater Treatment (April 2025)

3.1.4. Nanofiber Membranes and Nanoparticles for Advanced Removal (2024-2025)

3.1.5. Policy Shifts: EU's Revised Urban Wastewater Treatment Directive (January 2025)

4. Competitive Landscape: Leading Players

4.1. Market Overview: Multinational Leaders and Innovative Specialists

4.2. Strategic Profiles of Key Companies

4.2.1. DuPont Water Solutions: Membrane Innovation Driving Advanced Removal

4.2.2. Veolia Water Technologies: Expanding Global Leadership Through Integrated Solutions

4.2.3. SUEZ Water Technologies & Solutions: Customization and Digital Integration

4.2.4. Evoqua Water Technologies LLC (Now Part of Xylem): Strengthening North American Presence

4.2.5. Kurita Water Industries: Chemical Expertise and Energy-Positive Wastewater Innovations

5. Heavy Metal Removal Systems Market Segmentation Insights

5.1. By Technology

5.1.1. Chemical Precipitation Systems: Dominant Segment (32.8% Market Share)

5.1.2. Membrane Filtration Systems: Fastest Growing Segment (24.6% Market Share)

5.1.3. Adsorption Systems (16.9% Market Share)

5.1.4. Ion Exchange Systems (11.8% Market Share)

5.1.5. Electrochemical Treatment Systems

5.1.6. Bioremediation & Biosorption Systems

5.1.7. Evaporation & Crystallization Systems

5.2. By Heavy Metal Treated

5.2.1. Lead (24.6% Market Share) & Arsenic (21.2% Market Share)

5.2.3. Mercury (17.3% Market Share) & Chromium (14.8% Market Share)

5.2.4. Nickel, Copper & Zinc

5.2.5. Cadmium

5.3. By Application

5.3.1. Municipal Drinking Water Treatment

5.3.2. Industrial Wastewater Treatment

5.3.3. Groundwater & Contaminated Site Remediation

5.3.4. Power Generation & Energy Sector

5.3.5. Food & Beverage Processing

5.3.6. Pharmaceutical & Biotechnology

5.4. By Treatment Mode

5.4.1. On-Site

5.4.2. Mobile

5.4.3. Centralized

6. Country Analysis and Outlook

6.1. China: Stringent Regulations and Advanced Membrane Technologies

6.2. United States: PFAS Regulations and ZLD Technologies

6.3. India: ZLD Mandates and Government Missions

6.4. Germany: EU Directives and Digital Water Management

6.5. Australia: Environmental Stewardship and Virtual Curtain Technology

6.6. Japan: MBR and Advanced Membrane Technologies

6.7. Other Countries Analyzed

6.7.1. North America (Canada, Mexico)

6.7.2. Europe (UK, France, Spain, Italy, Russia, Rest of Europe)

6.7.3. Asia Pacific (South Korea, South East Asia, Rest of Asia)

6.7.4. South America (Brazil, Argentina, Rest of South America)

6.7.5. Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

7. Market Size Outlook by Region (2025-2034)

7.1. North America Heavy Metal Removal Systems Market Size Outlook to 2034

7.1.1. By Technology

7.1.2. By Heavy Metal Treated

7.1.3. By Application

7.1.4. By Treatment Mode

7.2. Europe Heavy Metal Removal Systems Market Size Outlook to 2034

7.2.1. By Technology

7.2.2. By Heavy Metal Treated

7.2.3. By Application

7.2.4. By Treatment Mode

7.3. Asia Pacific Heavy Metal Removal Systems Market Size Outlook to 2034

7.3.1. By Technology

7.3.2. By Heavy Metal Treated

7.3.3. By Application

7.3.4. By Treatment Mode

7.4. South America Heavy Metal Removal Systems Market Size Outlook to 2034

7.4.1. By Technology

7.4.2. By Heavy Metal Treated

7.4.3. By Application

7.4.4. By Treatment Mode

7.5. Middle East and Africa Heavy Metal Removal Systems Market Size Outlook to 2034

7.5.1. By Technology

7.5.2. By Heavy Metal Treated

7.5.3. By Application

7.5.4. By Treatment Mode

8. Company Profiles: Leading Players in Heavy Metal Removal Systems Market

8.1. Veolia

8.2. SUEZ

8.3. Xylem Inc.

8.4. Evoqua Water Technologies

8.5. DuPont de Nemours, Inc.

8.6. Pentair plc

8.7. Toray Industries, Inc.

8.8. Aquatech International

8.9. Kubota Corporation

8.10. The Dow Chemical Company

8.11. V.A. TECH WABAG Ltd.

8.12. Mitsubishi Chemical Corporation

8.13. Kurita Water Industries Ltd.

8.14. Nalco Water (An Ecolab Company)

8.15. Thermax Limited

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures