Industry Outlook and Value Growth: Forecasting the Future of Agricultural Wastewater Treatment Chemicals

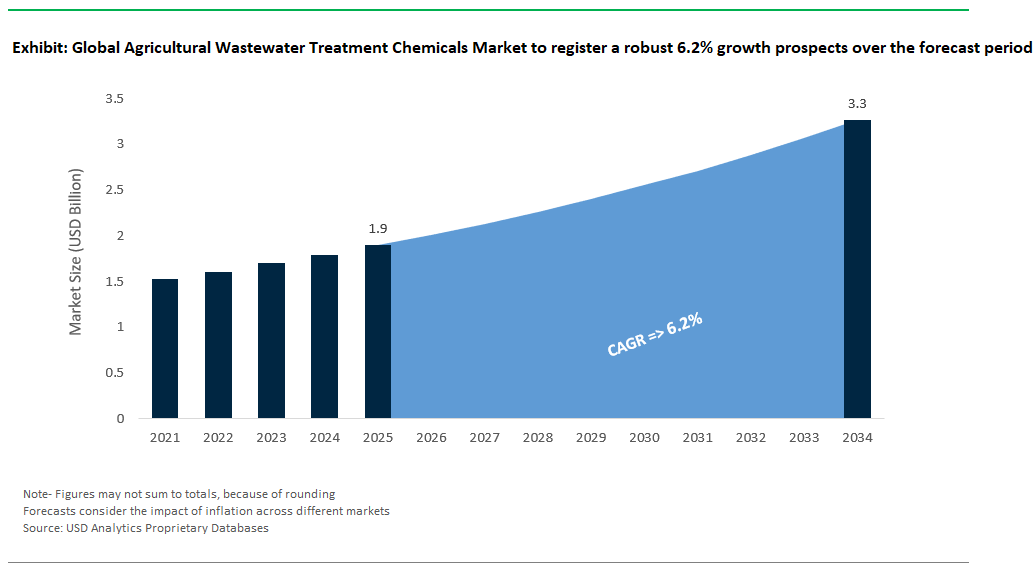

The agricultural wastewater treatment chemicals market is valued at $1.9 billion in 2025 and projected to rise to $3.3 billion by 2034, growing at a CAGR of 6.2%. The sector is undergoing a paradigm shift as nutrient recovery, pesticide degradation, and zero-discharge imperatives redefine how runoff and effluent streams are managed in both intensive and extensive farming systems. With phosphorus and nitrogen regulations tightening globally, chemical solutions that support nutrient valorization are gaining traction. Struvite precipitation, for example, has become a commercially viable pathway for phosphorus recovery, enabling 85–95% capture of P as magnesium ammonium phosphate at pH ranges of 8.5–9.0, transforming a once-problematic pollutant into a slow-release fertilizer. Advancements such as electrocatalytic nitrate removal technology further support the market outlook.

On the nitrogen front, electrocatalytic reduction methods have emerged as a promising chemical-electrical hybrid route within decentralized or grid-backed installations. Meanwhile, pesticide oxidation dynamics continue to dictate chemical selection and dosing strategies. Ozone-based treatments display highly compound-specific degradation kinetics, with reaction rates ranging from 6 M⁻¹s⁻¹ for atrazine to an impressive 2.4×10⁶ M⁻¹s⁻¹ for glyphosate, underscoring the need for precision oxidation chemistry in field runoff and collection basins.

As agribusinesses move toward environmental stewardship frameworks and as ESG metrics start influencing fertilizer subsidies and irrigation licenses, the role of chemical interventions is becoming less reactive and more integrated. Suppliers are responding by offering modular chemical platforms that blend oxidants, nutrient capture agents, and pH buffers for site-specific treatment goals. This market is thus increasingly defined not just by pollutant removal efficiency but by circularity, compliance alignment, and energy adaptability, making chemical solutions a critical lever in agricultural water sustainability strategies.

Major Trends and Strategic Opportunities in the Agricultural Wastewater Treatment Chemicals Market

Market Trend: Rise of Bio-Based and AI-Optimized Formulations Redefines Agricultural Wastewater Treatment

The agricultural wastewater treatment chemicals market is moving decisively beyond conventional inorganic coagulants toward bio-based, biodegradable, and precision-engineered solutions. This shift is being driven by a combination of sludge disposal costs, environmental regulations, and increasing scrutiny of chemical residues in soil and water. Bio-based coagulants derived from agricultural and marine biomass particularly lignin and chitosan are proving to be not only eco-friendlier but also more efficient under real-world agricultural runoff conditions. BASF’s Sokalan® AQ 6800, a lignin-derived coagulant, has demonstrated 90% phosphate removal at half the dosage compared to alum while reducing sludge volumes by 40%, a significant operational advantage in large-scale crop production systems like Brazilian sugarcane farms. Simultaneously, chitosan extracted from crustacean shells is finding traction in Southeast Asian rice paddy irrigation, showing 75% pesticide residue reduction compared to polyaluminum chloride. This bio-based transition is being reinforced by the adoption of precision chemical dosing platforms, exemplified by Netafim’s SmartFloc system. Integrated with IoT sensors and machine learning, SmartFloc dynamically adjusts polyacrylamide dosages in real time based on turbidity and total suspended solids (TSS), resulting in 20% lower chemical usage across California’s dairy and feedlot operations. Together, these developments reflect a broader market trend: treatment chemicals in agriculture are no longer chosen solely for bulk cost they must meet performance, biodegradability, and automation criteria to stay relevant in an increasingly regulated, resource-constrained environment.

Market Opportunity: Nutrient Recovery Technologies Open Profit-Driven Model for Agricultural Wastewater Management

A high-value opportunity in the agricultural wastewater treatment chemicals market lies in the convergence of nutrient recovery and circular agribusiness models. Fertilizer-grade nutrient extraction from livestock and crop waste streams is emerging as both a compliance mechanism and a revenue-generating solution. Technologies like struvite precipitation are transforming phosphorus-laden livestock effluents into marketable slow-release fertilizers. Ostara’s Pearl® system, for example, has enabled Iowa hog farms to recover 85% of wastewater phosphorus, converting it into crystalline struvite that fetches $500/tonne in specialty fertilizer markets effectively turning a $200/tonne waste disposal liability into a profitable output. Similarly, Europe’s Phos4You initiative has demonstrated the viability of transforming millions of tons of dairy manure into dual outputs: struvite and reclaimed water. In crop-centric geographies, biochar-filtered reuse systems are gaining traction. Spain’s AZUD PhytoFilter uses pyrolyzed olive pits to remove nitrates and pesticide residues from farm effluent, enabling cost-effective irrigation reuse at just $0.03/m³ one-fifth the cost of conventional reverse osmosis. Meanwhile, modular electrocoagulation units are making chemical treatment viable for smallholder farms. Solar-powered and engineered for low TCO, these systems process over 1 million liters/day of pesticide-laden runoff with 60% lower OPEX than traditional hauling and central treatment. With legislative mandates such as California’s SB 1383 requiring 100% livestock wastewater recycling by 2030, nutrient recovery solutions are not merely compliance tools they are redefining wastewater treatment as a profit center, particularly in high-value crops and protein production zones. For chemical suppliers and treatment technology vendors, this represents a $400M+ emerging opportunity tied directly to agronomic returns, sustainability metrics, and decarbonization goals.

Competitive Landscape, Agricultural Wastewater Treatment Chemicals

The market for agricultural wastewater treatment chemicals has various players addressing multiple challenges. These challenges include high organic loads, nutrient pollution, particularly nitrogen and phosphorus, pathogens, suspended solids, and trace pesticides or herbicides. The market includes chemical types like coagulants, flocculants, pH control agents, disinfectants, nutrient precipitants, and biological additives.

Multinational companies such as BASF, Kemira, Solenis, and SNF Floerger provide high-performance flocculants and coagulants designed for dewatering manure and agricultural processing sludge. Ecolab, through its Nalco Water division, offers integrated chemical solutions focused on phosphorus removal, odor control, and remote monitoring using 3D TRASAR™ systems. Veolia and SUEZ work on full-scale treatment plants where chemicals are part of a larger solution that may involve nutrient recovery and water reuse.

Kurita supplies specialized bioaugmentation and odor control chemicals for digestate and animal waste streams. Meanwhile, Dow and DuPont focus on advanced treatment methods using membranes, ion exchange resins, and protective chemicals, mainly for agricultural processors. Companies differentiate themselves based on their effectiveness in dealing with complex effluents, adherence to discharge regulations, chemical safety for possible irrigation reuse, and the level of technical support provided to agricultural operations.

Agricultural Wastewater Treatment Chemicals Market – Segmentation Insights (2025–2034)

Coagulants & Flocculants Dominate Chemical Types; Adsorbents Show Highest Growth

In the Agricultural Wastewater Treatment Chemicals market, Coagulants & Flocculants hold the largest market share, capturing approximately 38.2% in 2025. Their market leadership is primarily driven by their essential role in the effective removal of suspended solids and turbidity from farm runoff, significantly reducing sedimentation and nutrient loads entering natural waterways. Additionally, these chemicals efficiently aid in the clarification process, making them indispensable across agricultural wastewater management practices. Conversely, adsorbents represent the fastest-growing chemical category, expanding at an impressive 7.8% CAGR during 2025–2034. Growth in adsorbents, notably activated carbon and biochar, is fueled by their heightened efficacy in the targeted removal of pesticides and herbicides from agricultural discharge, addressing rising environmental and regulatory concerns. Nutrient Removal Chemicals, particularly alum-based solutions for phosphorus and nitrate reduction, also maintain steady growth driven by tightening environmental regulations, while oxidizing agents like chlorine and ozone increasingly find applications in pathogen control within livestock wastewater treatment.

.png)

Secondary Treatment Leads Process Types; Tertiary Treatment Registers Fastest Expansion

By treatment process, Secondary Treatment emerges as the leading segment, commanding approximately 39.1% market share in 2025. This dominance stems from the widespread adoption of biological treatment methods, notably activated sludge and anaerobic digestion, which effectively reduce organic loads and biological oxygen demand (BOD) in agricultural wastewater. Secondary treatment is widely regarded as a standard and cost-effective solution, achieving regulatory compliance across diverse agricultural operations, from livestock to crop processing. Meanwhile, Tertiary or Advanced Treatment processes register the fastest growth, with a robust 8.2% CAGR projected through 2034. The rising demand for high-quality treated water, driven by increasing environmental standards and water reuse strategies, accelerates adoption of advanced filtration technologies, including membrane filtration and advanced chemical polishing methods such as UV/H₂O₂ oxidation. Sludge Treatment and Conditioning also experience notable growth due to the necessity for efficient sludge dewatering and safe disposal solutions, frequently employing coagulants like ferric chloride. Primary treatment continues as a foundational treatment stage, crucial for preliminary solids removal in agricultural wastewater systems.

United States Strengthens Agricultural Wastewater Treatment Chemicals Market with Regulatory Push and Water Reuse

The United States is a frontrunner in the agricultural wastewater treatment chemicals market, driven by tightening environmental regulations and a strategic focus on water reuse. The U.S. Environmental Protection Agency (EPA) has escalated efforts to tackle agricultural runoff particularly nutrient pollution from fertilizers and pesticides prompting the adoption of advanced chemical treatment solutions nationwide. As regulatory scrutiny intensifies, including new mandates for reporting water use and setting strict effluent discharge limits, state governments in key agricultural regions are enforcing compliance, further stimulating demand for high-performance treatment chemicals.

A surge in concern over "emerging contaminants" such as PFAS in agricultural runoff is spurring innovation in specialized treatment processes and next-generation chemical formulations. The U.S. agricultural sector is also leading the shift to closed-loop systems, where treated wastewater is recycled for irrigation and livestock, requiring reliable, high-quality chemical treatments to ensure water safety and regulatory adherence. These combined pressures and innovations position the U.S. as a trendsetter in sustainable, regulatory-driven wastewater treatment for agriculture.

China Accelerates Agricultural Wastewater Treatment with Policy, Investment, and Technology Expansion

China’s agricultural wastewater treatment chemicals market is expanding rapidly, underpinned by aggressive government policies and major investments in environmental protection. The Chinese government has made cleaning up agricultural runoff a national priority, introducing policies that set new fertilizer usage standards and fund massive rural water treatment infrastructure upgrades. This has triggered a significant uptick in demand for chemical solutions tailored to nutrient-rich runoff and rural water reuse.

Rural and peri-urban regions are a particular focus, with the 13th Five-Year Plan allocating substantial funding for new wastewater treatment facilities, extending chemical treatment technology into previously underserved communities. As China continues to industrialize its agriculture, the demand for both traditional and innovative chemical treatments capable of meeting strict pollution prevention standards continues to grow. By fostering a robust market for cleaning and recycling water technology, China is cementing its position as a leader in the deployment and scaling of agricultural wastewater solutions.

India Drives Agricultural Wastewater Chemical Market Growth with Policy Mandates and Technology Pilots

India’s agricultural wastewater treatment chemicals market is surging, fueled by landmark national policies promoting water recycling and the adoption of innovative, cost-effective technologies. The Ministry of Jal Shakti’s mandate for increased water reuse is accelerating demand for treatment chemicals across both municipal and rural applications. Progressive states like Gujarat, Maharashtra, and Karnataka are enforcing policies that require the use of treated wastewater in agriculture and industry with Gujarat setting a bold target for 100% reuse by 2030.

The National Green Tribunal’s active enforcement and financial penalties for non-compliance are compelling local governments and utilities to adopt efficient wastewater treatment chemicals. India is also a hotbed for technology innovation, with advanced systems like TERI’s “TADOX” UV-Photocatalysis technology being piloted under flagship programs to address agricultural runoff. These regulatory and technological advances are enabling scalable, effective, and economically viable treatment for India’s diverse agricultural sector.

Brazil Advances Agricultural Wastewater Treatment with Large-Scale Infrastructure and Biological Technologies

Brazil is establishing itself as a vital market for agricultural wastewater treatment chemicals, responding to the complexities of managing waste from its vast industrial-scale farms. Leading companies such as Xylem and ACCIONA are spearheading the construction and modernization of wastewater treatment facilities designed for regions with intensive agriculture. The emphasis in Brazil is on deploying advanced biological treatment technologies such as intermittent cycle extended aeration systems (ICEAS) that combine energy efficiency with the ability to handle nutrient-rich agricultural effluents.

Large-scale government and private investments in new treatment plants and expansive sewerage networks are strengthening Brazil’s capacity to manage both agricultural and rural wastewater. As the agricultural sector intensifies and sustainability standards rise, Brazil’s market is expected to see continued growth in demand for sophisticated chemical and biological treatment solutions that support regulatory compliance and environmental stewardship.

Netherlands Champions Resource Recovery and Circular Economy in Agricultural Wastewater Treatment

The Netherlands stands as a global benchmark for innovation in agricultural wastewater treatment, pioneering technologies and circular economy approaches that maximize resource recovery. Dutch regulators and private companies are rolling out advanced systems for treating agricultural runoff, designed to adapt to both climate change and evolving EU directives. A signature trend is phosphorus recovery through crystallization reactors, converting waste into valuable struvite for reuse as fertilizer simultaneously lowering nutrient discharge and supporting sustainable agriculture.

The high cost of water in the Netherlands incentivizes manufacturers to invest in zero-liquid discharge systems, leveraging real-time digital platforms to optimize chemical dosing and energy consumption. Plants in North Brabant and Friesland exemplify the integration of smart technology and chemical treatments, setting a global standard for water efficiency, resource reuse, and sustainability in the agri-food sector.

Australia Focuses on Drought Resilience and Sustainable Growth in Agricultural Wastewater Treatment

Australia’s approach to agricultural wastewater treatment chemicals is directly shaped by its need for water security and long-term agricultural productivity. The Australian government is allocating substantial funding for water resource management projects particularly in the critical Murray–Darling Basin to support regional industries and enhance river health. This national agenda is prompting greater adoption of treatment chemicals to meet higher environmental standards for effluent discharge and water recycling.

Investments in land management and on-farm biodiversity initiatives are creating new demand for efficient wastewater treatment systems. Australia’s ambitious plan to reach $100 billion in farm production by 2030 includes integrating advanced chemicals and technologies to ensure sustainable, compliant, and productive agricultural practices, especially in drought-prone regions.

Israel Sets Global Standard for Agricultural Water Reuse and Treatment Technology

Israel is recognized worldwide for its leadership in water reuse and cutting-edge agricultural wastewater treatment technology. Nearly 90% of the country’s wastewater is recycled for agricultural irrigation an achievement made possible through coordinated regulatory reform, infrastructure investment, and institutional support. Israel’s expertise is showcased at the Shafdan Water Recycling Facility, which deploys extensive tertiary and aquifer-based treatments as a model for safe, high-quality water reuse.

Israel’s policies and technology have garnered global interest, with the U.S. Environmental Protection Agency (EPA) signing a Memorandum of Understanding (MOU) with Israel’s Ministry of Environmental Protection to collaborate on water reuse strategies. Through knowledge-sharing, research, and international delegations, Israel is actively shaping global best practices for agricultural wastewater treatment and advanced chemical applications.

United Kingdom Embraces Circular Economy and Advanced Treatment Alternatives for Agricultural Wastewater

The United Kingdom is advancing agricultural wastewater treatment through collaborative research, ambitious government policy, and a commitment to resource recovery. Projects led by Cranfield University and major water utilities are pioneering thermochemical processes such as pyrolysis and hydrothermal oxidation (HTO) to target PFAS and microplastics in sewage sludge applied to farmland. The government’s “Plan for Water” sets a comprehensive agenda to restore water quality, tackle agricultural runoff, and implement integrated water management strategies.

The UK water industry is investing in the identification and evaluation of sustainable, less chemical-intensive alternatives, while also promoting the recovery of valuable nutrients like phosphorus and ammonia for agricultural reuse. By embedding circular economy principles and technological innovation, the UK is charting a path toward sustainable, resilient, and resource-efficient agricultural water management.

Agricultural Wastewater Treatment Chemicals Market Report Scope

Agricultural Wastewater Treatment Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.9 Billion

|

|

Market Size (2034)

|

$3.3 Billion

|

|

Market Growth Rate

|

6.2%

|

|

Segments

|

By Chemical Type (Coagulants and Flocculants, pH Adjusters and Neutralizers, Disinfectants and Biocides, Oxidizing and Reducing Agents, Adsorbents, Nutrient Removal Chemicals, Anti-foaming Agents (Defoamers)), By Wastewater Source (Livestock and Animal Husbandry, Crop Production and Horticulture, Agro-industrial Operations), By Treatment Process (Primary Treatment, Secondary Treatment, Tertiary/Advanced Treatment, Sludge Treatment and Conditioning

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE (Germany), Ecolab (U.S.), Kemira Oyj (Finland), SUEZ SA (France), Veolia Water Technologies (France), Solenis (U.S.), Kurita Water Industries Ltd. (Japan), The Dow Chemical Company (U.S.), DuPont de Nemours Inc. (U.S.), SNF Floerger (France),

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Agricultural Wastewater Treatment Chemicals Market Segmentation

By Chemical Type

- Coagulants and Flocculants

- Inorganic

- Organic Polymers

- pH Adjusters and Neutralizers

- Disinfectants and Biocides

- Oxidizing and Reducing Agents

- Potassium Permanganate

- Hydrogen Peroxide

- Adsorbents

- Nutrient Removal Chemicals

- Anti-foaming Agents (Defoamers)

By Wastewater Source

- Livestock and Animal Husbandry

- Dairy Farms

- Poultry Operations

- Piggeries/Swine Farms

- Feedlots

- Aquaculture

- Crop Production and Horticulture

- Pesticide and Herbicide Runoff

- Fertilizer Runoff

- Vegetable and Fruit Washing/Processing

- Agro-industrial Operations

- Wineries

- Slaughterhouses

- Food and Beverage Processing

By Treatment Process

- Primary Treatment

- Secondary Treatment

- Tertiary/Advanced Treatment

- Sludge Treatment and Conditioning

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Agricultural Wastewater Treatment Chemicals Market

- BASF SE (Germany)

- Ecolab (U.S.)

- Kemira Oyj (Finland)

- SUEZ SA (France)

- Veolia Water Technologies (France)

- Solenis (U.S.)

- Kurita Water Industries Ltd. (Japan)

- The Dow Chemical Company (U.S.)

- DuPont de Nemours Inc. (U.S.)

- SNF Floerger (France)

* List Not Exhaustive

Research Coverage

This report provides a comprehensive review of the Agricultural Wastewater Treatment Chemicals Market, highlighting market size, growth drivers, and in-depth segmentation by chemical type, wastewater source, and treatment process. It examines the rapid adoption of bio-based, AI-optimized formulations, nutrient recovery technologies, and advanced oxidation processes driven by tightening nutrient regulations, water reuse mandates, and sustainability goals. The analysis covers key trends across livestock, crop production, and agro-industrial wastewater streams, with strategic insights on the circular economy, resource recovery, and regulatory impacts. USDAnalytics delivers actionable, data-backed intelligence to guide industry professionals, technology providers, and policymakers through the evolving landscape of agricultural water sustainability.

Scope Highlights:

- Segmentation:

- By Chemical Type: Coagulants & Flocculants (Inorganic, Organic Polymers), pH Adjusters & Neutralizers (Acids, Bases), Disinfectants & Biocides (Chlorine, Peracetic Acid, Ozone), Oxidizing & Reducing Agents (Potassium Permanganate, Hydrogen Peroxide), Adsorbents, Nutrient Removal Chemicals, Anti-foaming Agents

- By Wastewater Source: Livestock & Animal Husbandry (Dairy, Poultry, Swine, Feedlots, Aquaculture), Crop Production & Horticulture (Pesticide/Herbicide Runoff, Fertilizer Runoff, Vegetable/Fruit Processing), Agro-industrial Operations (Wineries, Slaughterhouses, Food/Beverage Processing)

- By Treatment Process: Primary, Secondary, Tertiary/Advanced, Sludge Treatment & Conditioning

- Geographic Scope: Analysis spans 25+ countries in North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

- Data Coverage: Historic data from 2021 to 2024 and forecasts from 2025 to 2034.

- Key Players: BASF SE, Ecolab, Kemira Oyj, SUEZ SA, Veolia Water Technologies, Solenis, Kurita Water Industries, The Dow Chemical Company, DuPont de Nemours, SNF Floerger (list not exhaustive)

Methodology

USDAnalytics employs a robust, multi-phase methodology for the Agricultural Wastewater Treatment Chemicals Market. The approach integrates primary interviews with global suppliers, regulators, and end users, alongside exhaustive secondary research from scientific publications, patents, and government sources. Market sizing and forecasts leverage proprietary modeling techniques, triangulated with historic data (2021–2024) and scenario-driven projections to 2034. Each segment is evaluated for market share, growth drivers, technology adoption, and regulatory trends, with a special focus on nutrient recovery, bio-based innovations, and compliance. Peer review and sensitivity analysis ensure the findings are both credible and actionable for stakeholders seeking strategic clarity in this evolving sector.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements