Bio-based Flocculants and Coagulants in Water Treatment Market Overview: Growth Outlook, Analysis, and Forecast to 2034

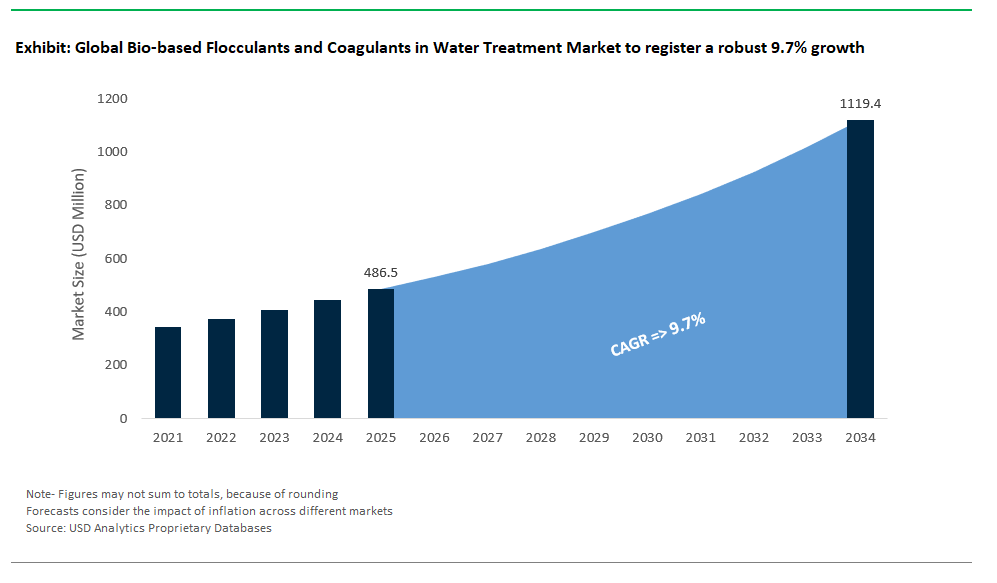

The bio-based flocculants and coagulants in water treatment market is valued at $486.5 million in 2025 and projected to reach $1,119.3 million by 2034, registering a CAGR of 9.7%. The market is emerging as a compelling response to the dual imperatives of process efficacy and environmental responsibility, particularly in water treatment sectors where sludge generation, chemical residuals, and regulatory scrutiny are intensifying. Plant-derived coagulants such as Moringa oleifera seed extracts have demonstrated strong turbidity removal, achieving 85–95% reduction at doses of 50–100 mg/L, rivalling or surpassing conventional alum, which typically requires 100–150 mg/L for equivalent performance.

The coagulant activity is attributed to the seed’s protein content, with thresholds above 30% protein composition proving essential for consistent charge neutralization and particle destabilization. Beyond plant extracts, microbial polysaccharides like chitosan derived from crustacean shell waste are gaining ground for their cationic density and performance across a broad pH range. With charge densities between 4–6 meq/g, chitosan exhibits strong affinity for negatively charged particulates, notably in algae-laden waters at low operational doses.

From an end-of-pipe perspective, these biopolymers far outperform synthetic polyacrylamides in environmental metrics, achieving over 90% biodegradation in 28 days under OECD 301B protocols, compared to less than 50% degradation for their petroleum-based counterparts. This dramatic difference in downstream persistence is influencing regulatory frameworks and public procurement preferences, particularly in Europe and select U.S. jurisdictions pushing for green procurement in water utilities.

As demand grows for circular, non-toxic, and low-carbon water treatment strategies, the market is shifting from experimental adoption to strategic implementation. The challenge ahead lies in standardizing performance across raw material sources, scaling fermentation or extraction processes, and integrating these bio-based agents into existing jar testing, automation, and sludge dewatering protocols. Suppliers capable of delivering batch consistency, application-specific blends, and third-party biodegradability validation will define the future of this rapidly maturing segment.

Evolving Market Dynamics and Growth Opportunities in Coagulation and Flocculation Solutions

Market Trend: Rapid Shift Toward Sustainable and Circular Solutions in Coagulation & Flocculation

The global water treatment industry is undergoing a structural transition from metal-based and synthetic polymeric coagulants toward bio-based and waste-derived alternatives, driven by escalating regulatory, environmental, and economic pressures. This shift is supported by the EU’s regulations on aluminum-based coagulants in ecologically sensitive watersheds triggering over $500 million in new demand for natural alternatives. Pioneers like Kemira and Corbion are commercializing next-generation formulations derived from industrial and marine waste streams. Kemira’s BioFloc™, made from lignin waste from pulp mills, demonstrated 90% turbidity removal in Brazilian municipal trials while halving dosing requirements versus aluminum sulfate. Meanwhile, Corbion’s chitosan-based solution derived from shrimp shells, shows high PFAS removal efficiency in EU drinking water validations, outperforming traditional polymers without introducing microplastic residues. These bio-coagulants not only reduce toxicity risks and residual heavy metals but also help utilities meet Scope 3 emission reduction targets, with Life Cycle Assessments showing 50% lower carbon footprints. Economically, maturing supply chains have closed the cost gap chitosan is marketed at comparable costs to many synthetic polyDADMAC or polyacrylamide variants. The U.S. EPA’s PFAS Strategic Roadmap and landfill leachate treatment policies are further accelerating the move toward green, non-toxic flocculation solutions. As regulatory and ESG scrutiny intensifies globally, especially from institutional investors and corporate buyers, utilities and industrial users are pivoting fast toward biodegradable, circular chemistry with high removal efficiency and long-term compliance confidence.

Growth Opportunity: Industrial Wastewater Valorization with Bio-Based Flocculants

Bio-based flocculants are unlocking transformative opportunities in industrial wastewater valorization, particularly across mining, F&B, and textile sectors, where both regulatory burden and circular economy pressure are highest. In mining, chitosan-metal complexes are enabling dual benefits of clarification and resource recovery as seen in Rio Tinto’s lithium brine operations, where chitosan captured rare earth elements from spent brine, while concurrently producing reusable water for further extraction. This approach contributes to a $5,000/tonne lithium carbonate yield and reduces chemical intensity in tailings management. Glencore’s cobalt operations incorporate lignin-derived flocculants to transform sludge into recoverable battery materials, creating new revenue streams while aligning with EU battery passport requirements. In the food and beverage industry, PepsiCo’s Mexico plant utilized okra polysaccharide-based coagulants to treat high-COD, starch-rich effluents from snack production, enabling annual savings of over $1 million. These agri-waste flocculants not only qualify for USDA BioPreferred® labeling but also meet corporate circularity KPIs. Meanwhile, in the textile sector, H&M’s suppliers in Bangladesh deployed plant-based coagulants to slash COD loads by 40%, ensuring ZDHC compliance and unlocking access to premium buyers. Early movers benefit from multiple levers carbon credits ($10–$50/tonne CO₂), IP monetization, and premium positioning in green procurement systems. As water-intensive sectors look to decarbonize and monetize waste, bio-flocculants will evolve from compliance tools into strategic enablers of industrial circularity.

Competitive Landscape: Bio-based Flocculants & Coagulants in Water Treatment Market

The competitive dynamics of the bio-based flocculants and coagulants market revolve around polymer innovation, sustainability-driven research and development, and integration into wider water treatment ecosystems. Leading companies are adopting different strategies to market bio-derived alternatives to traditional synthetic products. They aim to ensure similar performance, regulatory acceptance, and cost efficiency.

A key focus for top manufacturers is the shift to renewable feedstocks like starches, chitosan, tannins, and bio-based acrylamides. Companies such as SNF Floerger are using their global reach and polymerization infrastructure to create bio-based polyacrylamides from renewable monomers sourced from plant sugars. Their strategy highlights equal performance and a reduction in lifecycle carbon, which supports larger goals in circular chemistry. Similarly, Kemira has made strides in the market with its commercial BioGrip® product line, which includes tannin-based coagulants and polysaccharide flocculants certified by programs like the USDA BioPreferred initiative. Their attention to municipal and industrial sludge dewatering applications has set a standard for measurable sustainability metrics and lower greenhouse gas emissions.

Upstream chemical producers like BASF may not directly create flocculants, but they play an essential supporting role. By providing bio-based polyacrylic acid precursors and modified starches through its “Biomass Balance” program, BASF helps others develop greener alternatives. Ecolab takes a different approach by acting as a systems integrator, incorporating bio-based coagulants and flocculants from outside partners into comprehensive water management platforms. Their use of these materials within data-driven systems like 3D TRASAR shows that bio-based solutions are being validated not only through lab tests but also through real-world results tied to client environmental, social, and governance (ESG) performance.

Companies like Solenis and Kurita are advancing natural polymer chemistry. Solenis invests in high-performance biodegradable flocculants aimed at industries sensitive to effluent quality and sludge handling. Kurita uses enzyme modification on starches and chitosan to improve floc strength, settleability, and biodegradability. These innovations show how traditional performance trade-offs in bio-based systems are being gradually tackled through biochemical engineering.

The market also includes niche innovators like Tidal Vision, which has launched high-purity chitosan solutions made from crab shell waste. Its CYCLOSORB-CHT™ platform stresses traceable sourcing, consistent viscosity, and effectiveness in heavy metal removal addressing rising demands for sustainability and functional specialization. Other companies, like Buckman and Feralco, are building hybrid systems that mix conventional chemistries like ferric salts or celluloses with renewable components to improve performance while lessening environmental impact. Distributors such as Accepta Ltd. help by providing technical guidance and product selection that align with changing EU regulations and customer needs.

Bio-based Flocculants and Coagulants in Water Treatment Market – Segmentation Insights (2025–2034)

By Type of Bio-based Chemical: Plant-Based Leads the Market While Microbial Bioflocculants Grow Fastest

Plant-based bio-flocculants and coagulants account for the largest market share, approximately 44.3% in 2025, driven by their wide availability, cost-effectiveness, and alignment with circular economy goals. Materials like tannins, starch derivatives, lignin, and guar gum are increasingly sourced from agricultural and forestry byproducts, making them attractive to both public utilities and industries seeking sustainable treatment solutions. Their compatibility with existing treatment systems and biodegradability further support their widespread adoption. In contrast, microbial-based bioflocculants derived from strains such as Bacillus, Aspergillus, and Rhizobium represent the fastest-growing category, with a projected 10.8% CAGR through 2034. These bioflocculants exhibit superior performance in removing heavy metals, organic matter, and dyes, especially in high-contaminant industrial streams. Modified or grafted bio-based polymers such as chitosan-grafted polyacrylamide (chitosan-g-PAM) are also gaining ground as they combine natural biopolymer properties with enhanced flocculation performance, helping bridge the gap between green alternatives and synthetic polymers. Animal-based flocculants, typically derived from shellfish or gelatin, remain niche but continue to find use in sensitive applications like food processing due to their high protein content and strong charge density.

By End-User Industry: Municipal Water Sector Leads While Textile Industry Grows Fastest

Municipal water and wastewater plants dominate end-use adoption, holding approximately 37.8% of the market share in 2025. Their leadership stems from tightening global regulations particularly in Europe under the EU Green Deal that push municipalities to phase out synthetic polymers in favor of bio-based alternatives. These regulations are driving upgrades in coagulation and flocculation systems to accommodate natural and biodegradable materials while maintaining performance standards. Meanwhile, the textile industry is the fastest-growing end-user, projected to expand at a 11.2% CAGR through 2034. The shift toward organic-certified and environmentally friendly processing chemicals is prompting textile manufacturers to adopt bio-based flocculants to replace conventional polyacrylamides used in dye and COD removal. The food and beverage sector is also witnessing strong growth, fueled by increasing demand for organic-label certification and clean-label processing aids. Pulp and paper mills, with a long history of using natural polymers, continue steady integration of bio-based coagulants, while the mining and metallurgy sector is increasingly deploying microbial flocculants for tailings clarification and metal recovery. Other industries, including pharmaceuticals and cosmetics, are exploring niche uses for bio-based water treatment agents as part of broader green transition strategies.

.png)

India Champions Circular Economy in Bio-based Flocculants and Coagulants Market

India is rapidly positioning itself as a global leader in the bio-based flocculants and coagulants market for water treatment, leveraging innovative government policies and extensive academic research. Central to this momentum is the GOBARdhan initiative, which drives the transformation of agricultural and cattle waste into high-value resources, perfectly aligning with the circular economy ethos. This framework not only supports waste-to-resource conversion but also underpins the development of next-generation bio-based water treatment solutions. India’s National Water Policy further accelerates market growth by advocating widespread water recycling and reuse, spurring innovation in green, non-toxic chemical formulations.

Cutting-edge research by Indian scientists highlights the efficacy of indigenous materials such as papaya seeds, tamarind seeds, neem leaves, and orange peels as potent, plant-based coagulants offering an affordable and biodegradable alternative to conventional chemicals. Companies like SUSBIO ECOTREAT are responding with advanced dual-process treatment systems, tapping into available government incentives and positioning themselves at the intersection of economic and environmental sustainability. With native plant-based solutions and a strong focus on cost-effectiveness and safety, India is emerging as a key player in the global market for bio-based water treatment chemicals.

United States Advances Bio-based Water Treatment with Regulatory and Technological Leadership

The United States remains at the forefront of the bio-based flocculants and coagulants market, propelled by stringent environmental regulations, industry innovation, and a robust investment climate. The Clean Water Act and other federal initiatives are pressuring industries to shift away from metal-based coagulants known for generating toxic sludge toward biodegradable, low-toxicity alternatives. This shift is particularly evident in advanced industrial sectors such as semiconductors, pharmaceuticals, and mining, where compliance is non-negotiable.

Leading innovators like Gradiant are rolling out platforms such as CURE Chemicals, delivering new-generation coagulants tailored for the most demanding applications. U.S. academic and private-sector research is producing breakthroughs in chitosan- and starch-based flocculants, while AI-driven dosing technologies are revolutionizing efficiency and waste reduction across water treatment facilities. The U.S. investment community’s growing prioritization of sustainable water technologies is further accelerating market adoption, making the country a trendsetter for green water treatment solutions globally.

Germany Sets Sustainability Benchmarks in Bio-based Coagulants and Flocculants for Water Treatment

Germany’s bio-based flocculants and coagulants market is defined by world-class sustainability standards, green chemistry, and an unwavering commitment to the circular economy. The German government’s active collaboration with research institutions is producing innovative, biodegradable water treatment technologies that meet the strict requirements of the EU Water Framework Directive. German firms, such as Veolia, are spearheading the development of plant-based coagulants that slash sludge volume by up to 50%, making them particularly attractive for sectors like food and beverage processing.

Sustainability isn’t just a regulatory requirement but a market differentiator in Germany. The focus is on delivering high-performance, low-impact solutions that facilitate resource recovery and minimize environmental burden. By prioritizing green water treatment practices and the adoption of circular economy models, Germany stands out as a reference point for responsible and efficient bio-based water treatment chemistry.

Brazil Leverages Native Resources and Sanitation Reform to Fuel Bio-based Flocculants Growth

Brazil’s bio-based flocculants and coagulants market is surging, energized by a transformative sanitation regulatory framework and the nation’s abundant natural resources. With universal clean water and sanitation as national goals, Brazil is experiencing substantial investment in municipal and industrial water treatment, driving demand for eco-friendly solutions. Local academic research, particularly in the use of native plant extracts like Moringa oleifera seeds, is demonstrating exceptional turbidity and contaminant removal, positioning Brazil as a hub for cost-effective, sustainable water purification.

Brazil’s agricultural sector provides a rich, local supply chain for the production of bio-based chemicals, giving the country a natural advantage. The mining industry and other heavy water users are adopting these green alternatives to improve environmental performance and regulatory compliance. This strategic blend of policy, research, and natural resources is making Brazil a fast-growing market for bio-based water treatment solutions in Latin America.

China Drives Bio-based Water Treatment Innovation with Circular Economy Focus

China is emerging as a key force in the development and commercialization of bio-based flocculants and coagulants, aligning national policy with rapid technological advancement. The government’s green technology mandate and support for pollution control are driving large-scale research into biodegradable and high-performance water treatment chemicals. Chinese scientists are pioneering the conversion of agricultural waste and microbial byproducts into next-generation flocculants, supporting national goals to reduce chemical imports and close resource loops.

The textile and food sectors are early adopters of these bio-based solutions, seeking to minimize sludge generation and handle complex organic loads more sustainably. Innovation is evident in the creation of hybrid materials that merge natural polymers with inorganics, delivering superior treatment outcomes with a lower environmental impact. China’s focus on both industrial efficiency and ecological protection positions it as a front-runner in the global bio-based water treatment chemicals market.

South Korea Pioneers High-Tech Biodegradable Flocculants and Coagulants for Water Treatment

South Korea’s market for bio-based flocculants and coagulants is distinguished by advanced materials science, a strong industrial user base, and relentless R&D. Korean companies and research centers are investing in the development of next-generation polymer membranes, nanocellulose, and other bio-based compounds for a variety of water treatment applications. This innovation is closely tied to the country’s electronics and chemical sectors, which demand high-performance, sustainable water treatment solutions to meet both operational and regulatory objectives.

Academic research is also exploring the use of renewable materials for new flocculation and coagulation processes. South Korea’s commitment to high-tech manufacturing and its clean energy agenda ensure continued demand for innovative, environmentally friendly water treatment chemicals, further strengthening its competitive edge in Asia-Pacific.

United Kingdom Responds to Environmental Policy with Bio-based Water Treatment Innovation

The United Kingdom is actively reshaping its water treatment chemicals market in response to evolving environmental targets and increased regulatory scrutiny. The Environment Act 2021 and the "Plan for Water" are key policy drivers, setting stricter standards for pollution reduction and the management of micropollutants. UK research institutions and water companies are exploring bio-based flocculants to enhance the removal of emerging contaminants from both drinking water and wastewater streams.

Market demand is shifting toward biodegradable, low-toxicity chemicals that can minimize sludge volume and ecological impact. Funding for green innovation is on the rise, with government support for R&D programs in sustainable water treatment technologies. As environmental accountability becomes a core expectation for water companies, the UK is expected to see a rapid uptick in the adoption of bio-based water treatment solutions.

Japan Integrates High-Performance Bio-based Flocculants into Water Reuse and Conservation Strategies

Japan’s technologically mature water treatment sector is leading the way in integrating advanced bio-based flocculants and coagulants to meet its stringent water quality and conservation goals. The country’s electronics and pharmaceutical industries require ultra-pure water, spurring investment in high-purity, bio-based chemicals that are both efficient and environmentally benign. Japanese researchers are at the cutting edge, developing novel membranes and hybrid treatment processes that harness bio-based materials to improve treatment outcomes and system longevity.

Japan’s water reuse initiatives, underpinned by a national commitment to the circular economy, are creating new opportunities for sustainable treatment chemicals. These solutions play a critical role in reducing freshwater demand and supporting the country’s long-term sustainability agenda. With strong policy backing and a reputation for technological innovation, Japan remains a global benchmark for green water treatment chemistry.

Bio-based Flocculants and Coagulants in Water Treatment Market Report Scope

Bio-based Flocculants and Coagulants in Water Treatment Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$486.5 Million

|

|

Market Size (2034)

|

$1119.3 Million

|

|

Market Growth Rate

|

9.7%

|

|

Segments

|

By Type of Bio-based Chemical (Plant-based, Microbial-based (Bioflocculants - BFs), Animal-based, Modified/Grafted Bio-based Polymers), By Application (Water Treatment, Wastewater Treatment, Other Applications), By End-User Industry (Municipal Water and Wastewater Treatment Plants, Food and Beverage, Pulp and Paper, Mining and Metallurgy, Textile, Chemical and Petrochemical, Pharmaceutical, Oil and Gas, Agriculture, Other Manufacturing Industries

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

SNF Floerger (France), Kemira Oyj (Finland), BASF SE (Germany), Ecolab Inc. (U.S.), Solenis LLC (U.S.), Kurita Water Industries Ltd. (Japan), Tidal Vision (U.S.), Feralco AB (Sweden), Buckman (U.S.), Accepta Ltd. (UK),

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Bio-based Flocculants and Coagulants in Water Treatment Market Segmentation

By Type of Bio-based Chemical

- Plant-based

- Moringa Oleifera

- Tannins/Lignin

- Starch-based

- Cellulose-based

- Chitosan

- Gums

- Other Plant Extracts

- Microbial-based (Bioflocculants - BFs)

- Polysaccharides

- Proteins

- Glycoproteins

- Lipopolysaccharides

- Nucleic acids

- Specific microbial strains

- Animal-based

- Modified/Grafted Bio-based Polymers

By Application

- Water Treatment

- Drinking Water Purification

- Raw Water Clarification

- Sedimentation Enhancement

- Wastewater Treatment

- Municipal Wastewater Treatment

- Industrial Wastewater Treatment

- Nutrient Removal

- Heavy Metal Removal

- Color Removal

- Oil and Grease Removal

- COD/BOD Reduction

- Other Applications

By End-User Industry

- Municipal Water and Wastewater Treatment Plants

- Food and Beverage

- Pulp and Paper

- Mining and Metallurgy

- Textile

- Chemical and Petrochemical

- Pharmaceutical

- Oil and Gas

- Agriculture

- Other Manufacturing Industries

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Bio-based Flocculants and Coagulants in Water Treatment Market

- SNF Floerger (France)

- Kemira Oyj (Finland)

- BASF SE (Germany)

- Ecolab Inc. (U.S.)

- Solenis LLC (U.S.)

- Kurita Water Industries Ltd. (Japan)

- Tidal Vision (U.S.)

- FeralcAB (Sweden)

- Buckman (U.S.)

- Accepta Ltd. (UK)

* List Not Exhaustive

Research Coverage

This report investigates the global Bio-based Flocculants and Coagulants Market, delivering detailed analysis reviews of emerging green chemistries, regulatory mandates, and advanced solutions reshaping coagulation and flocculation practices. USDAnalytics highlights major breakthroughs in plant-based, microbial-based, and modified bio-polymers that are driving sustainable water treatment across municipal and industrial sectors. The study emphasizes technological innovation, industrial adoption, and strategic opportunities linked to the circular economy and low-carbon water management. This report is an essential resource for utilities, industrial operators, policymakers, and solution providers seeking actionable intelligence on market dynamics, growth prospects, and eco-friendly chemical integration from 2025 to 2034.

Scope Highlights:

- Segmentation:

- By Type of Bio-based Chemical: Plant-based (Moringa Oleifera, Tannins/Lignin, Starch-based, Cellulose-based, Chitosan, Gums, Other Plant Extracts), Microbial-based (Polysaccharides, Proteins, Glycoproteins, Lipopolysaccharides, Nucleic acids, Specific microbial strains), Animal-based, Modified/Grafted Bio-based Polymers

- By Application: Water Treatment (Drinking Water Purification, Raw Water Clarification, Sedimentation Enhancement), Wastewater Treatment (Municipal, Industrial, Nutrient Removal, Heavy Metal Removal, Color Removal, Oil and Grease Removal, COD/BOD Reduction), Other Applications

- By End-User Industry: Municipal Water & Wastewater Treatment Plants, Food & Beverage, Pulp & Paper, Mining & Metallurgy, Textile, Chemical & Petrochemical, Pharmaceutical, Oil & Gas, Agriculture, Other Manufacturing Industries

- Geographic Scope: Covers 25+ countries across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

- Data Coverage: Historic data from 2021 to 2024 and forecasts from 2025 to 2034.

- Companies Profiled: SNF Floerger (France), Kemira Oyj (Finland), BASF SE (Germany), Ecolab Inc. (U.S.), Solenis LLC (U.S.), Kurita Water Industries Ltd. (Japan), Tidal Vision (U.S.), FeralcAB (Sweden), Buckman (U.S.), Accepta Ltd. (UK).

Methodology

The research methodology is based on a combination of primary interviews with industry experts and secondary data sourced from trusted databases, regulatory reports, and scientific publications. USDAnalytics applies advanced modeling techniques, demand-supply analysis, and scenario-based forecasting to deliver accurate projections. This approach integrates market dynamics, pricing trends, and adoption patterns across end-use industries while factoring in sustainability metrics and regulatory frameworks. Our methodology ensures reliable, data-driven insights for strategic decision-making in the bio-based water treatment chemicals sector.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements