Green Water Treatment Chemicals Market: Sustainable Growth Analysis and Value Forecast to 2034

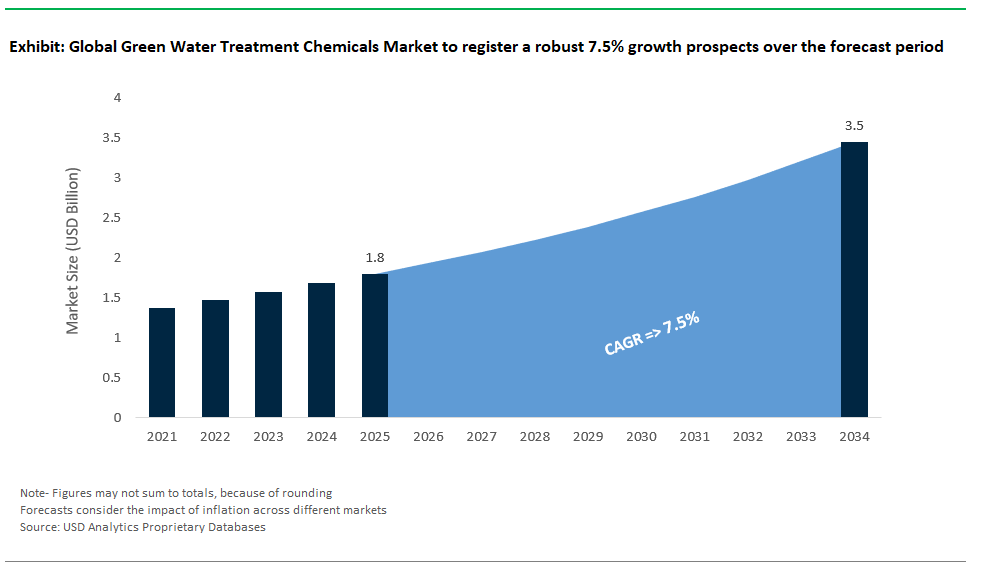

The green water treatment chemicals market is valued at $1.8 billion in 2025 and is projected to reach $3.5 billion by 2034, demonstrating a robust CAGR of 7.5%. This sector is gaining strategic momentum as industrial and municipal operators seek environmentally preferable alternatives that meet both performance and regulatory thresholds without relying on traditional petrochemical-based formulations. Plant-derived coagulants such as Moringa oleifera extracts have emerged as viable substitutes for alum and ferric salts in turbidity control applications, delivering 80–90% turbidity reduction at 50–150 mg/L dosing comparable to alum at 100 mg/L, but with the added benefits of lower sludge volume and improved biodegradability, as demonstrated in recent trials.

In the realm of biofouling control, enzymatic biofilm disruptors specifically protease and polysaccharide hydrolase blends are becoming a compelling alternative to oxidative or surfactant-based cleaners. At concentrations as low as 0.1–1.0 mg/L, these enzymatic agents can achieve a 3-log reduction in extracellular polymeric substances (EPS), effectively dismantling biofilms without the material compatibility issues associated with halogenated or acid-based cleaners. The market is also witnessing adjacent innovations that reduce or eliminate chemical input, notably through electrochemical water conditioning systems. Enzyme blends have also been increasingly field-validated in membrane systems since 2023.

Pulsed electromagnetic or electrostatic field devices have demonstrated >70% scale suppression in heat exchangers and boiler circuits without chemical additives, positioning them as zero-discharge-compatible technologies (AWWA Research Foundation). However, chemical products marketed under the “green” label are increasingly scrutinized for verifiable environmental attributes. Under OECD 301 protocols, only those achieving >60% biodegradation in 28 days qualify, making third-party validation and formulation transparency key differentiators in this segment. As ESG-linked procurement gains ground, particularly among Fortune 500 manufacturers and utilities with net-zero water goals, the green water treatment chemicals market is moving beyond niche status.

Regulatory Pressures and Sustainability Commitments Accelerate Growth in the Green Water Treatment Chemicals Market

Market Trend: Surge in Bio-Based Disinfectants and Scale Inhibitors Reshapes the Future of Water Treatment

The green water treatment chemicals market is experiencing a decisive pivot toward bio-based and non-toxic formulations as regulatory crackdowns and corporate sustainability commitments converge. Traditional treatment chemistries such as PFAS-laced surfactants, phosphonates, and chlorine derivatives are being phased out under intensifying scrutiny. The European Union’s 2024 PFAS restrictions and the U.S. EPA’s expansion of the Safer Choice Standard are creating immediate market urgency to eliminate persistent, toxic, and bioaccumulative compounds from water treatment protocols. In parallel, global multinationals such as Coca-Cola, Nestlé, and Unilever are tightening supplier requirements demanding proof of USDA BioPreferred® certifications or equivalent ecolabels for all incoming water-related chemicals. This regulatory-commercial alignment has catalyzed a wave of innovation in green chemistries. Ecolab’s EnviroTru®, a lactic acid-based sanitizer, has successfully replaced chlorine in bottling plants, cutting chemical residues by 80% while ensuring compliance with FDA and WHO potable reuse guidelines. In the scaling segment, BASF’s Sokalan® Bio series has demonstrated superior sludge volume reduction compared to legacy phosphonates, with enhanced compatibility across closed-loop cooling systems. These advancements reflect a broader shift from “greenwashing” to performance-verified, regulation-aligned green water treatment cementing bio-based formulations as essential tools for future-ready water management in industrial, municipal, and commercial sectors.

Market Opportunity: Circular Water Solutions and ESG Integration Create Premium Value for Green Treatment Providers

The most transformative opportunity in the green water treatment chemicals market lies in enabling circular water systems for ESG-focused industries where water reuse, regulatory compliance, and carbon tracking converge to deliver both sustainability and financial returns. Industries adopting Zero Liquid Discharge (ZLD) and water-positive models are not just avoiding penalties they are monetizing their environmental performance. Heineken’s Brewery of the Future in the Netherlands is a model example: using enzyme-based cleaners and electrochemical oxidation, the facility recycles 99% of its process water, achieving $1.2 million in annual water cost savings while marketing its products under the Alliance for Water Stewardship (AWS) certification translating into a 5–7% premium in conscious consumer markets. In the mining sector, Rio Tinto’s lithium operations leverage plant-based flocculants to extract critical minerals with wastewater reuse cutting freshwater procurement costs in water-stressed geographies like the Atacama. Textile manufacturers partnering with brands like H&M are adopting bio-coagulants and non-toxic defoamers, cutting effluent treatment costs by 30% while remaining compliant with global buyer mandates. The opportunity extends beyond water savings: Veolia’s ReUse™ platform enables customers to track and monetize the carbon savings from avoided chlorine production and transport, generating verified carbon credits ($15–$50/tonne) through Scope 3 accounting. Chemical suppliers such as Ecolab and Solenis are capitalizing on this shift by offering “Chemical-as-a-Service” models, bundling green formulations, sensor analytics, and performance guarantees under pay-per-use contracts accelerating adoption while locking in long-term clients. With ROI on circular water systems dropping below 18 months by 2030, the business case for green water treatment chemicals has moved from aspirational to essential.

Competitive Landscape: Green Water Treatment Chemicals Market

The green water treatment chemicals market is changing significantly as sustainability becomes important in regulations, customer buying standards, and investor evaluation. Instead of relying on performance or pricing, competition now hinges on a company’s ability to reduce environmental impacts while ensuring reliable processes. This change is creating a new order of players. The leaders are those that incorporate biodegradable, bio-based, low-toxicity, and resource-efficient products into complete water treatment programs, often supported by digital tools and life cycle transparency.

A key feature of the competitive landscape is the rise of multi-dimensional solutions that blend green chemistry with process improvement and digital management. Many global water solution providers are integrating green principles directly into their platform strategies. They use life cycle assessment (LCA), smart dosing systems, and energy-chemical-water nexus metrics to reshape product performance. These companies are creating high-purity bio-based polymers, phosphate- and nitrogen-free inhibitors, biodegradable chelants, and enzyme-based controls for scale or microbes, all designed to reduce sludge, cut down on residues, and support water reuse or zero liquid discharge compliance.

Innovation pipelines are increasingly focused on cradle-to-cradle design. They prefer raw materials that are less persistent, do not bioaccumulate, and have lower ecotoxicity. Suppliers that produce upstream building blocks, such as bio-derived solvents, natural chelants, or low-carbon footprint monomers, are becoming essential in the value chain. Their technologies are crucial for downstream formulators aiming for green certifications, food-grade compliance, or reduced environmental hazards. At the same time, regional specialists in water-scarce areas are making progress by offering minimal-chemical and chemical-free solutions like electrocoagulation, advanced oxidation, and ion exchange, often tailored to meet local water reuse or discharge regulations.

Digitalization also sets companies apart. Providers that use smart water platforms can optimize chemical use in real time, track sustainability metrics, and ensure regulatory compliance, all while improving cost efficiency. The combination of green chemistry with AI-driven control is especially important for industrial clients wanting to balance environmental, social, and governance (ESG) goals with reliable operations. Furthermore, sustainability reporting and transparency are now essential. Leading companies publish detailed impact assessments, set climate goals, and engage in global standard-setting projects, positioning themselves as leaders in environmental responsibility.

Green Water Treatment Chemicals Market – Segmentation Insights (2025–2034)

By Type: Green Coagulants Lead the Market While Membrane Antiscalants Grow Fastest

Green coagulants and flocculants represent the largest share in the green water treatment chemicals market, accounting for approximately 28.7% of the market in 2025. This leadership is driven by rising environmental and health concerns surrounding conventional aluminum- and synthetic-based coagulants. Natural alternatives such as chitosan (from crustacean shells) and tannins (from plant bark) are gaining traction across municipal and industrial treatment systems due to their biodegradability, lower toxicity, and minimal sludge generation. In contrast, green membrane antiscalants are experiencing the fastest growth, expanding at a remarkable 8.6% CAGR between 2025 and 2034. This surge is fueled by the global expansion of reverse osmosis (RO) and desalination infrastructure, which demands eco-friendly antiscaling agents compatible with membranes and regulatory limits. Green biocides and disinfectants are also on the rise, as natural antimicrobials such as thyme oil and neem extract disrupt traditional chlorine- and bromine-based disinfection markets. Meanwhile, green corrosion and scale inhibitors are becoming popular for cooling towers and closed-loop systems, offering sustainable protection without heavy metals or phosphonates. Defoamers, pH adjusters and Softeners, and sludge conditioners, though niche, continue to find adoption in green-certified water treatment projects worldwide.

By Source of Raw Material: Plant-Based Sources Dominate; Waste-Derived Inputs Grow Most Rapidly

Plant-based raw materials dominate the green water treatment chemicals market, capturing around 44.3% of total share in 2025. The widespread use of agricultural byproducts such as starch, lignin, and guar gum positions plant-based chemicals as the preferred choice for formulators looking to reduce dependence on petrochemicals while ensuring performance. These bio-sourced materials are readily available, cost-effective, and support a cleaner chemical lifecycle, aligning with ESG mandates and green building certifications. However, the fastest-growing segment is waste-derived substances, projected to grow at a staggering 9.2% CAGR through 2034. Innovations in utilizing brewery waste, fruit peels, and food processing residues are creating new circular economy opportunities for water treatment chemicals, especially in developing markets aiming to reduce waste disposal burdens and enhance resource efficiency. Microbial-based materials, such as polyhydroxyalkanoates (PHAs) and bacterial extracts, are also gaining popularity due to their high functionality and biodegradability, particularly in high-performance membrane and disinfection applications. Mineral-based raw materials, though stable and familiar, grow at a slower pace due to limitations in renewability and environmental impact.

.png)

United States Catalyzes Green Water Treatment Chemicals Market with Infrastructure Investment and Sustainable Innovation

The United States is a key growth engine in the green water treatment chemicals market, driven by unprecedented federal infrastructure spending and an intensified focus on sustainability. The Infrastructure Investment and Jobs Act has allocated over $50 billion to the EPA for nationwide water system upgrades, with a special emphasis on tackling emerging contaminants such as PFAS. This is spurring rapid commercialization of non-toxic, biodegradable, and eco-friendly water treatment solutions that meet both regulatory and consumer demand for safer, greener products. Leading U.S. companies and academic partnerships are advancing novel chemistries, including bio-based coagulants and flocculants from renewable resources, as well as advanced technologies that eliminate bio-toxins without creating new environmental risks.

The EPA’s Clean Water Technology Center is providing a national platform for research and funding, helping to accelerate the adoption of green treatment solutions at the state and municipal level. The U.S. market is now defined by a collaborative approach between regulators, technology providers, and communities, resulting in a pipeline of sustainable water treatment innovations poised to set global benchmarks.

China Accelerates Green Water Treatment Chemicals Market with Policy-Driven Innovation and Circular Economy Focus

China’s green water treatment chemicals market is expanding rapidly, fueled by state-led investment in environmental protection and an ambitious circular economy agenda. Government policy has made water resource protection a cornerstone of national development, supporting a surge in technological innovation and patent activity around eco-friendly treatment materials. In 2025, Chinese firms secured patents for advanced polyacrylamide and water reuse systems, reflecting the nation’s emphasis on increasing industrial water efficiency and reducing chemical consumption.

China is diversifying its green water treatment portfolio, moving beyond legacy chemicals to high-performance, environmentally friendly products that support strict wastewater discharge limits for municipal and industrial sectors. Major industries including papermaking, mining, and manufacturing are integrating these solutions to reduce pollution, increase resource reuse, and align with evolving regulatory mandates. The strategic emphasis on science-based, green chemistry is establishing China as a leading innovator and adopter in the global green water treatment market.

Germany Leads Green Water Treatment Chemicals Market with Compliance-Driven R&D and Smart Water Integration

Germany is at the forefront of the green water treatment chemicals market, leveraging strict environmental regulations and a strong R&D culture to drive adoption of sustainable solutions. The implementation of the revised EU Drinking Water Directive in German law is prompting a shift toward advanced, eco-friendly chemistries such as biodegradable coagulants and phosphate-free corrosion inhibitors capable of addressing pollutants like arsenic, chromium, and lead at reduced concentration levels. Leading German companies are heavily investing in R&D for new formulations that combine efficacy with a minimal environmental footprint.

The rise of digital water management is further enhancing the efficiency of green chemicals through real-time data integration, optimized dosing, and waste reduction. Germany’s industrial landscape including pharmaceuticals, power, and food and beverage is rapidly embracing these sustainable solutions to comply with both EU standards and consumer expectations for environmental responsibility.

India Expands Green Water Treatment Chemicals Market with National Water Missions and Localized Innovation

India’s green water treatment chemicals market is undergoing robust expansion, propelled by landmark government initiatives and new regulatory standards for water reuse. The Ministry of Jal Shakti’s “Catch the Rain – 2025” campaign and stricter Central Pollution Control Board (CPCB) discharge norms are accelerating demand for sustainable, effective treatment solutions. Incentives such as tax benefits and green bonds are catalyzing investment in advanced technologies, making it easier for both cities and industry to upgrade to eco-friendly water treatment systems.

Innovative modular and decentralized solutions, like SUSBIO ECOTREAT, are addressing India’s diverse water challenges with energy-efficient, green chemistries tailored for urban and rural contexts. The market is further buoyed by community participation programs and growing industrial awareness of the long-term benefits of sustainable water management, positioning India as a fast-rising player in the global green water treatment chemicals industry.

Japan Pioneers High-Purity, Sustainable Green Water Treatment Chemicals for Advanced Applications

Japan’s green water treatment chemicals market is marked by advanced technological expertise and a pioneering approach to both terrestrial and extraterrestrial applications. Japanese companies are developing breakthrough solutions such as polyglutamic acid-based bio-flocculants, which have delivered clean water to millions worldwide and set new standards for effectiveness and sustainability. Collaboration with lunar exploration firms to test water purification on the Moon is expanding the boundaries of what green treatment can achieve, with direct implications for earth-based applications.

Sustainability is embedded in Japanese corporate culture, with beverage and manufacturing sectors launching dedicated water stewardship ventures and offering consultancy on best practices. New commercial wastewater treatments for agriculture and livestock further showcase Japan’s commitment to cleaner rivers and groundwater through innovative, green chemistry.

Brazil Advances Green Water Treatment Chemicals Market through Sanitation Reform and Nature-Based Solutions

Brazil’s green water treatment chemicals market is experiencing significant growth, driven by regulatory reform and ambitious national goals for universal water access and sustainability. The 2020 sanitation law is ushering in large-scale private investment and an upgrade of water treatment infrastructure, with the National Water and Sanitation Agency (ANA) setting high performance and efficiency standards. Nature-based and “green infrastructure” solutions are increasingly being used to supplement conventional chemical treatments, creating new demand for eco-friendly chemicals that fit within circular and closed-loop systems especially in the country’s extensive agricultural sector.

With a focus on both water reuse and environmental compliance, Brazil is on track to become a regional leader in sustainable water treatment, supported by an active policy environment and a growing market for green chemical solutions.

United Kingdom Champions Green Water Treatment Chemicals Market with Environmental Legislation and Circular Economy

The United Kingdom is rapidly evolving its green water treatment chemicals market under the guidance of the Environment Act 2021 and the national “Plan for Water.” Water companies are now required to meet stringent quality targets using advanced, environmentally friendly treatment chemistries. There is a coordinated industry push to address contaminants such as PFAS and microplastics, with ongoing research supporting the development and adoption of new green chemical technologies.

The UK’s commitment to a circular economy is also evident in wastewater treatment practices, where the recovery of phosphorus and other resources for agricultural reuse demands the use of specific, sustainable chemicals. The integration of policy, research, and market innovation is positioning the UK as a leading advocate for green chemistry in the global water sector.

France Accelerates Green Water Treatment Chemicals Market with National Water Plan and Digital Transformation

France is making rapid progress in the green water treatment chemicals market, guided by the 2023–2030 national water management plan that emphasizes water reuse and sustainable resource management. Government funding such as the issuance of blue bonds to support water protection and restoration projects has unlocked hundreds of millions of euros for research, digital infrastructure, and sustainable technology upgrades. French water utilities are investing heavily in automation and AI, targeting 80% process automation by 2025, which enhances the precision and effectiveness of green chemical dosing.

Collaborations between large water companies and innovative startups are resulting in miniaturized, high-performance treatment systems tailored for urban environments, with sustainability at the core of product development. France’s dual focus on digitalization and green chemistry is setting a high bar for the European and global water treatment industry.

Green Water Treatment Chemicals Market Report Scope

Green Water Treatment Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.8 Billion

|

|

Market Size (2034)

|

$3.5 Billion

|

|

Market Growth Rate

|

7.5%

|

|

Segments

|

By Type (Green Coagulants and Flocculants, Green Corrosion and Scale Inhibitors, Green Biocides and Disinfectants, Green pH Adjusters and Softeners, Green Defoamers and Antifoaming Agents, Green Sludge Conditioners, Green Membrane Performance Enhancers/Antiscalants), By Source of Raw Material (Plant-Based, Microbial-Based, Mineral-Based, Waste-Derived Substances), By Application (Primary Treatment, Secondary Treatment, Tertiary Treatment and Advanced Treatment, Pre-treatment for Membrane Systems, Disinfection and Sanitation, Boiler Water Treatment, Cooling Water Treatment, Wastewater Treatment, Process Water Treatment), By End-User Industry (Municipal, Industrial, Commercial, Residential

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Kemira Oyj (Finland), Veolia (France), Ecolab (U.S.), Kurita Water Industries Ltd. (Japan), Solenis (U.S.), BASF SE (Germany), Thermax Global (India), Nouryon (The Netherlands), SNF Floerger (France), Green Water Treatment Solutions (UAE),

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Green Water Treatment Chemicals Market Segmentation

By Type

- Green Coagulants and Flocculants

- Green Corrosion and Scale Inhibitors

- Green Biocides and Disinfectants

- Green pH Adjusters and Softeners

- Green Defoamers and Antifoaming Agents

- Green Sludge Conditioners

- Green Membrane Performance Enhancers/Antiscalants

By Source of Raw Material

- Plant-Based

- Microbial-Based

- Mineral-Based

- Waste-Derived Substances

By Application

- Primary Treatment

- Secondary Treatment

- Tertiary Treatment and Advanced Treatment

- Pre-treatment for Membrane Systems

- Disinfection and Sanitation

- Boiler Water Treatment

- Cooling Water Treatment

- Wastewater Treatment

- Process Water Treatment

By End-User Industry

- Municipal

- Drinking Water Treatment Plants

- Municipal Wastewater Treatment Plants

- Industrial

- Food and Beverage

- Pulp and Paper

- Oil and Gas

- Power Generation

- Chemical and Petrochemical

- Mining and Metallurgy

- Textile

- Pharmaceutical

- Agriculture

- Other Manufacturing and Process Industries

- Commercial

- Residential

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Green Water Treatment Chemicals Market

- Kemira Oyj (Finland)

- Veolia (France)

- Ecolab (U.S.)

- Kurita Water Industries Ltd. (Japan)

- Solenis (U.S.)

- BASF SE (Germany)

- Thermax Global (India)

- Nouryon (The Netherlands)

- SNF Floerger (France)

- Green Water Treatment Solutions (UAE)

* List Not Exhaustive

Research Coverage

This report investigates the green water treatment chemicals market, providing in-depth analysis reviews, critical breakthroughs in sustainable chemistry, and strategic insights on regulatory trends, ESG integration, and market expansion. Drawing on USDAnalytics’ proprietary research, this report highlights the transition from petrochemical-based to bio-based and waste-derived chemicals, and underscores how digital water management, regulatory alignment, and circular economy solutions are reshaping water treatment for industrial, municipal, and commercial sectors. The report is an essential resource for manufacturers, utilities, technology providers, policymakers, and investors seeking clarity on growth opportunities, innovation pipelines, and competitive dynamics across more than 25 countries worldwide.

Scope Highlights:

- Segmentation:

- By Type: Green Coagulants and Flocculants, Green Corrosion and Scale Inhibitors, Green Biocides and Disinfectants, Green pH Adjusters and Softeners, Green Defoamers and Antifoaming Agents, Green Sludge Conditioners, Green Membrane Performance Enhancers/Antiscalants

- By Source of Raw Material: Plant-Based, Microbial-Based, Mineral-Based, Waste-Derived Substances

- By Application: Primary Treatment, Secondary Treatment, Tertiary Treatment and Advanced Treatment, Pre-treatment for Membrane Systems, Disinfection and Sanitation, Boiler Water Treatment, Cooling Water Treatment, Wastewater Treatment, Process Water Treatment

- By End-User Industry: Municipal, Industrial, Commercial, Residential

- Geographic Scope: Covers 25+ countries across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

- Data Coverage: Historic data from 2021 to 2024 and forecasts from 2025 to 2034.

- Key Players: Kemira Oyj (Finland), Veolia (France), Ecolab (U.S.), Kurita Water Industries Ltd. (Japan), Solenis (U.S.), BASF SE (Germany), Thermax Global (India), Nouryon (The Netherlands), SNF Floerger (France), Green Water Treatment Solutions (UAE).

Methodology

USDAnalytics employs a rigorous, multi-step research methodology combining expert interviews, real-world plant and project data, and cross-referenced secondary research from technical journals, regulatory filings, and industry databases. Market estimates and forecasts are built using proprietary analytics, comparative trend mapping, and scenario analysis to ensure accuracy. Each market segment is evaluated for qualitative and quantitative trends, providing actionable insights and trustworthy intelligence for all stakeholders in the green water treatment chemicals market.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements