PFAS Filtration Chemicals Market: Rapid Growth Analysis and Value Forecast to 2034

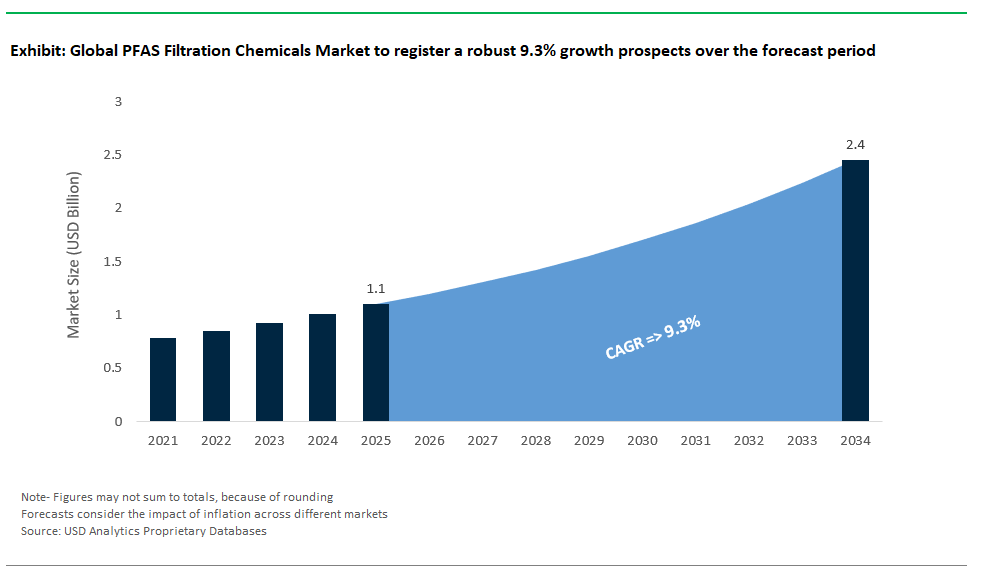

The PFAS filtration chemicals market is valued at $1.1 billion in 2025 and projected to reach $2.4 billion by 2034, demonstrating a high CAGR of 9.3%. The market is currently experiencing significant growth and specialization, driven by increasing regulatory actions and the urgent need to reduce per- and polyfluoroalkyl substances (PFAS) in water. The U.S. EPA has set Maximum Contaminant Levels (MCLs) for PFOA and PFOS at an extremely low 4.0 parts per trillion (ppt), effective in 2031, creating major compliance challenges for utilities and industrial dischargers.

Strong base anion (SBA) exchange resins are a common solution, providing PFAS uptake capacities of 0.5–1.5 mmol/g for long-chain compounds under various conditions (USEPA, 2024). However, these resins tend to lose efficiency during regeneration, typically recovering only 10–20% of their initial capacity after 10,000 bed volumes. This makes life-cycle costs an important factor for large-scale use.

As the focus shifts to sustainable methods of destroying PFAS instead of merely separating it, destructive chemical technologies are becoming more popular. Supercritical water oxidation (SCWO) operates at 450–650°C and 220–300 bar and consistently achieves over 99.99% PFAS mineralization. This positions it as a scalable technology for handling spent media and high-strength residuals. Plasma-based treatment systems are also emerging from the lab, with pilot-scale reactors showing energy yields of 10–50 g PFAS destroyed per kWh. This raises the possibility of decentralized, on-site chemical oxidation that does not produce secondary waste.

While granular activated carbon (GAC) and powdered carbon are still used in temporary applications, their limitations in dealing with breakthrough rates and short-chain PFAS have spurred demand for better resins and oxidants that address the complex nature of these contaminants. The market is increasingly shaped not just by traditional filtration capabilities, but by how well these solutions integrate with downstream destruction technologies and their ability to meet safety exposure standards at both low levels and high flow rates. New technologies, such as UV/plasma and sound wave methods, are being developed as destructive techniques. As funding shifts toward PFAS reduction due to bipartisan infrastructure and state initiatives, chemical suppliers that can provide effective, cost-efficient, and compliant solutions will likely lead the market.

Regulatory Shifts and Destruction Technologies Redefine the PFAS Filtration Chemicals Market

Market Trend: From Capture to Destruction- Strategies shaping market outlook

The PFAS filtration chemicals market is undergoing a major shift as regulatory, legal, and economic pressures lead to the decline of traditional capture-and-dispose methods. Instead, there is a move toward regenerable materials and destruction technologies. In 2024, the U.S. EPA set enforceable MCLs of 4 ppt for PFOA and PFOS in drinking water. This compels utilities and industries to adopt treatment methods that offer high selectivity and minimal residual risk. Because of this change, single-use granular activated carbon (GAC) and conventional ion exchange (IX) resins are becoming both financially unfeasible and environmentally problematic, especially as incineration of waste media faces bans or public opposition. Battelle’s Annihilator™, a supercritical water oxidation (SCWO) system, is leading the change, operating at over 20 U.S. military bases and achieving 99.99% PFAS destruction at a cost of $2–5 per gallon. This is about half the cost of thermal incineration and avoids releasing harmful airborne emissions. Cyclopure’s DEXSORB® polymer is also making waves in municipal and industrial settings. It can be regenerated and reused multiple times, cutting down disposal volumes by 70%. Evoqua’s Regenesis system uses electrochemical regeneration for IX resins, extending their lifespan by up to 5 times and significantly reducing operational costs in landfill leachate treatment, which is a major expense for municipal solid waste operations. Regulatory and legal risks make this shift even more urgent, as facilities storing PFAS-laden waste face potential liability under CERCLA amendments. As the industry moves toward sustainable, closed-loop filtration systems that allow for on-site regeneration or total PFAS degradation, the focus is shifting from sorption capacity to minimizing liability, controlling costs, and ensuring environmental impact.

Market Opportunity: Industrial Wastewater & Decentralized Drinking Water presents robust prospects for new entrants

The greatest business opportunity for PFAS filtration chemicals lies in the growing intersection of high-load industrial wastewater treatment and decentralized drinking water purification. Both fields face unique challenges but share a rising need for cost-effective, scalable PFAS solutions. In industrial settings, textile and dye manufacturing has emerged as a key area. For example, Shaw Industries’ Georgia plant uses plasma-enhanced cerium oxide filtration to remove PFAS from dye baths. This allows for water reuse during the process and results in annual savings of $1.2 million. As countries like Vietnam set national PFAS limits by 2026, over 1,000 textile mills are expected to adopt treatment systems, creating a pressing retrofit market in Southeast Asia. At the same time, U.S. Department of Defense firefighting training locations are priorities under the PFAS Fast Track Initiative, which has allocated $250 million to install supercritical water oxidation units at over 50 military sites. This presents a clear opportunity for turnkey destruction solutions. In addition to industrial applications, modular PFAS treatment is gaining traction in rural and underserved areas. Xylem’s Sentry™ containerized systems combine detection, capture, and destruction into one unit. These systems are already deployed in Maine and Michigan to comply with the Safe Drinking Water Act while enabling carbon monetization. Vermont’s Combined Sewer Overflow (CSO) program rewards $50 per pound of PFAS destroyed. This financial incentive is expected to roll out nationally under proposed PFAS Clean-Up Tax Credit bills. Furthermore, the market for retrofitting legacy AFFF (aqueous film-forming foam) storage sites following 3M’s switch to fluorine-free foam is valued at $800 million. This creates considerable demand for regenerable or in-situ destruction technologies. Chemical companies, equipment manufacturers, and engineering firms that bundle effective PFAS treatments with analytics, validation, and regulatory support stand to thrive in a landscape where mere removal is insufficient complete elimination is now the standard.

Competitive Landscape: PFAS Filtration Chemicals Market

The PFAS filtration chemicals market is changing quickly due to increasing regulatory pressures, technological progress, and the urgent demand for scalable solutions in municipal, industrial, and remediation settings. The competitive landscape includes both established water treatment leaders and new innovators, each focusing on different parts of the value chain, including media supply, system integration, service, and destruction technologies.

Activated carbon is still the foundation of PFAS removal, especially in municipal drinking water applications. Calgon Carbon (Kuraray) leads this global market, providing specialized PFAS-targeting grades such as CENTAUR® PFAS, supported by a solid reactivation infrastructure that improves lifecycle economics. Their leadership comes from a strong history in large-scale installations and proven performance under various site conditions. Other companies like Veolia and Xylem (through Evoqua) also use granular activated carbon (GAC) in integrated treatment systems, often combined with clarification or pre-treatment steps for efficiency.

Ion exchange (IX) resins are becoming a complementary or alternative technology, particularly for short-chain PFAS where carbon-based methods may not work as well. LANXESS and DuPont (with their Lewatit® and Amberlite™/Ambersep™ product lines) are major global suppliers of PFAS-selective resins, mainly serving engineering firms and OEMs. After acquiring Evoqua, Xylem has expanded its IX offerings, now providing complete systems that combine both GAC and IX for greater flexibility.

Specialty adsorbents are increasingly filling performance gaps, particularly in difficult industrial waters, landfill leachate, and point-of-use (POU) settings. 3M’s Perfluorosorb™ and Cyclopure’s DEXSORB+® (a cyclodextrin-based polymer) offer new chemistries with high selectivity and fast response times. Cyclopure, in particular, focuses on decentralized and household-scale solutions, responding to rising public health concerns and local regulations. Mineral Technologies Inc. (MTI) adds another angle with engineered mineral-based adsorbents like RemBind® and PFASorb®, originally designed for soil but now used in liquid treatment where irreversible binding is needed.

Companies like Veolia (and the now-integrated SUEZ) and Xylem stand out as system integrators offering complete PFAS treatment systems. These include not only media-based technologies like GAC and IX but also advanced biological and oxidation methods, such as Veolia’s Actiflo® Carb system and Xylem’s Wedeco ultraviolet oxidation, for thorough water management. Their ability to design and operate full-scale treatment plants sets them apart in both the municipal and industrial sectors.

Consulting and engineering firms, such as AECOM, play an important role in the value chain by connecting technology providers with end-users. Their services cover site assessment, pilot testing, and the integration of suitable media and systems from various suppliers. In highly regulated or technically complex situations, firms like Battelle are key contributors, developing advanced destruction technologies (like supercritical water oxidation) and validating media performance in real-world conditions. This research and development support is vital for progressing from adsorption to closed-loop solutions that manage PFAS waste streams.

The competitive dynamics focus on three main technology areas: GAC is the leading method in installed base and cost per treated gallon; IX resins provide better selectivity for certain PFAS types, particularly short chains; and new adsorbents aim to offer niche benefits in selectivity, regenerability, or size. At the same time, destruction technologies, though still in development, are gaining traction as regulations start demanding complete PFAS elimination instead of mere containment.

Market segmentation helps clarify where players stand. Municipal utilities make up the largest volume of treated water, where performance, cost-effectiveness, and compliance with EPA Maximum Contaminant Levels (MCLs) are crucial. Industrial treatment, including PFAS-rich wastewater and landfill leachate, involves more complex mixtures that require customized systems and often involve multiple media stages. Smaller-scale and decentralized systems (like private wells and mobile units) represent a growth area, particularly for point-of-entry and point-of-use systems using new adsorbents.

The market’s future will focus on capturing short-chain PFAS, media regenerability, and on-site destruction capabilities, all under tighter global regulations. Suppliers that can prove lifetime value, regulatory compliance, and adaptability across different treatment contexts are likely to have an advantage as utilities and industries work to future-proof their water systems.

PFAS Filtration Chemicals Market – Segmentation Insights (2025–2034)

By Type of Chemical: Granular Activated Carbon Leads While Specialty Adsorbents Grow Fastest

Granular Activated Carbon (GAC) holds the largest share in the PFAS filtration chemicals market, accounting for approximately 47.3% of total market demand in 2025. GAC remains the most widely adopted solution due to its well-documented performance in removing long-chain PFAS compounds, relatively low capital costs, and ease of integration into existing municipal and industrial filtration systems. Its high surface area and regenerability make it ideal for continuous and large-volume water treatment operations. However, the market is rapidly shifting toward more advanced materials, with Specialty/Proprietary Adsorbents growing at the fastest rate of 11.2% CAGR through 2034. These next-generation materials including functionalized silica for short-chain PFAS, engineered biochar composites, and molecularly imprinted polymers (MIPs) offer superior selectivity, adsorption capacity, and regeneration potential, making them ideal for complex remediation scenarios. Ion Exchange Resins (IX) are also witnessing significant growth, particularly in high-throughput systems where selective PFAS removal and lower breakthrough volumes are critical. Other chemical categories, including hybrid filtration blends and emerging sorbents, continue to support niche and experimental PFAS control solutions.

.png)

By Application: Water Treatment Dominates While Soil Remediation Expands Most Rapidly

Water treatment is the largest application for PFAS filtration chemicals, capturing approximately 69.2% of the market in 2025. This segment is driven by the surge in global regulatory mandates, particularly from the U.S. EPA and European agencies, requiring stringent PFAS limits in municipal drinking water and industrial wastewater discharges. Applications span municipal water utilities, firefighting foam runoff containment, and compliance-driven retrofits in chemical manufacturing zones. Technologies such as GAC and IX are commonly deployed for their proven efficacy in treating both surface and groundwater contaminated with PFAS. Meanwhile, soil remediation is the fastest-growing application segment, projected to expand at a 10.6% CAGR through 2034. This growth is fueled by rising environmental concerns over PFAS accumulation in soil near airfields, landfills, and manufacturing sites. Innovative in-situ stabilization techniques using specialty adsorbents and ex-situ remediation methods combining chemical filtration with thermal destruction are accelerating demand in this space. Other applications, including landfill leachate treatment and air emissions control, continue to evolve, contributing to a diversified PFAS mitigation strategy across environmental media.

United States Sets Global Benchmark for PFAS Filtration Chemicals Market with Regulatory Action and Technology Investment

The United States is at the forefront of the PFAS filtration chemicals market, experiencing the fastest growth globally due to historic regulatory and financial commitments. The April 2024 EPA rule introducing the first-ever national, legally enforceable drinking water standard for PFAS has triggered a wave of investment in advanced chemical filtration systems across the country. With $2 billion earmarked under the Infrastructure Investment and Jobs Act, municipalities are rapidly upgrading facilities to comply with these strict mandates, driving robust demand for granular activated carbon (GAC), ion exchange resins, and novel filtration agents.

The EPA’s designation of PFOA and PFOS as hazardous substances under Superfund legislation further accelerates cleanup efforts, empowering the agency to hold polluters accountable and fund state-of-the-art remediation projects. Industry trends include the adoption of AI-optimized GAC systems for operational efficiency and a rapid shift toward ion exchange resins, which provide higher selectivity and longer lifespan for PFAS removal in both municipal and industrial water treatment settings.

Germany Drives PFAS Filtration Chemicals Market with Strict Limits and Pilot-Driven Technology Selection

Germany stands as the European leader in the PFAS filtration chemicals market, propelled by stringent national limits on PFAS in water and a proactive regulatory stance. Notably, regions like North Rhine-Westphalia have seen rapid implementation of certified filtration solutions following high-profile contamination events. German water utilities and industrial users are investing heavily in pilot programs led by consortiums like Life CASCADE to identify the most effective treatment combinations for removing both long- and short-chain PFAS, as well as microplastics.

Advanced ion exchange resins are increasingly favored due to their high efficiency, while companies such as De Nora offer pilot testing to determine the optimal mix of GAC, ion exchange, or hybrid approaches for local compliance. Germany’s strong regulatory framework and culture of industrial innovation ensure it remains a critical testing ground and growth market for PFAS filtration chemicals in Europe.

China Advances PFAS Filtration Chemicals Market with Green Technology and Industrial Policy

China’s PFAS filtration chemicals market is witnessing steady momentum, with a growing emphasis on green technology, industrial emissions control, and emerging regulatory frameworks. The government’s evolving “Standards for Drinking Water Quality” already set limit values for PFOS and PFOA, laying a foundation for stricter future regulations. In 2024, MIT researchers introduced a breakthrough natural silk-cellulose filtration material in China, promoting a new generation of sustainable, high-efficiency PFAS remediation solutions for both industrial and municipal applications.

Chinese authorities are increasing research and development efforts to map PFAS contamination, especially near industrial and agricultural zones, and are supporting the commercialization of eco-friendly water treatment products. As regulatory clarity and public pressure grow, China is poised to expand its role as both a technology developer and a major end-user in the global PFAS filtration chemicals market.

Canada Accelerates PFAS Filtration Chemicals Adoption with New Guidelines and National Monitoring

Canada is undergoing rapid transformation in its PFAS filtration chemicals market, as federal and provincial governments introduce strict guidelines and step up enforcement. The new Canadian Drinking Water Objective, released in August 2024, sets a temporary limit of 30 ng/L for the sum of 25 PFAS compounds prompting municipal water utilities to upgrade treatment systems and invest in advanced filtration chemistries. The planned inclusion of most PFAS (excluding fluoropolymers) as toxic substances under CEPA will expand the regulatory net, requiring broader testing, monitoring, and remediation across the country.

Data-driven regulation is a key trend, with Section 71 Notices mandating reporting from PFAS manufacturers and users to support a comprehensive national risk assessment. Researchers and public health advocates are pushing for enforceable standards and greater investment in systematic testing near known contamination sites, further boosting demand for innovative, high-performance PFAS filtration chemicals and systems.

India Prepares for PFAS Filtration Chemicals Growth with Research and Regulatory Foundations

India’s market for PFAS filtration chemicals is in its infancy but is primed for growth as research, awareness, and policy recommendations gain traction. While India currently lacks dedicated PFAS standards, growing recognition of contamination risks especially in industrial groundwater has sparked calls for national guidelines and a coordinated monitoring network. Recent BIS and CPCB initiatives suggest that regulatory oversight may soon strengthen, laying the groundwork for mandatory PFAS testing and future filtration requirements.

Academic and policy circles are advocating for targeted investments in water treatment technologies, with a focus on affordable, scalable filtration solutions suitable for India’s vulnerable and rural communities. As regulatory momentum builds, demand for PFAS filtration chemicals and pilot projects is set to rise sharply across both public utilities and industrial sites.

Japan Innovates PFAS Filtration Chemicals Market with Comprehensive Ban and Advanced Degradation Technology

Japan’s PFAS filtration chemicals market is experiencing rapid change, led by stringent new chemical bans and technological innovation. The 2025 prohibition of 138 PFAS compounds as Class I Specified Chemical Substances is driving major investments in advanced filtration and degradation technologies for both industry and municipalities. Japanese researchers are making breakthroughs, such as the development of a photocatalytic process that fully degrades PFAS at room temperature using visible light signaling a shift from conventional capture-based filtration to destruction-based treatment.

Japan’s regulatory framework, which includes the “polluter pays” principle, is incentivizing industries to implement robust remediation measures, especially at sites impacted by firefighting foams. As a result, the Japanese market is quickly moving toward comprehensive, multi-stage PFAS treatment solutions that combine physical filtration and chemical degradation.

United Kingdom Adopts PFAS Filtration Chemicals Market Reforms with Environmental Targets and Infrastructure Investment

The United Kingdom’s PFAS filtration chemicals market is evolving as new environmental targets and risk-based regulations take hold. The Drinking Water Inspectorate’s tiered guidelines require water utilities to implement advanced blending and filtration techniques to reduce PFAS concentrations, while the national “Plan for Water” and recent Ofwat-approved investment plan are directing substantial new resources toward tackling micropollutants in water and sewage infrastructure.

A growing public debate over PFAS in water sources and sewage sludge is catalyzing a more comprehensive approach to emerging contaminants. The market is poised for further growth as utilities and industries are required to upgrade treatment systems, adopt new chemical solutions, and enhance monitoring to comply with both domestic and EU standards.

France Advances PFAS Filtration Chemicals Market with Legislative Action and Water Reuse Strategy

France is leading in the PFAS filtration chemicals market with a strong legislative push and innovative water management strategies. The March 2025 law banning PFAS in multiple product categories and instituting a “polluters tax” has generated significant funding for upgrading municipal water treatment systems. High-profile contamination incidents, such as in Saint-Louis, have raised public awareness and prompted immediate government and industry action to deploy advanced filtration and remediation technologies.

France’s new national water plan mandates mandatory control and phased elimination of PFAS releases into water by 2030 surpassing current EU requirements. The country’s emphasis on water reuse and unconventional sources requires best-in-class PFAS filtration chemicals to guarantee safety standards. The combination of regulatory urgency and technological investment makes France a pivotal market for innovation and expansion in the global PFAS filtration chemicals sector.

PFAS Filtration Chemicals Market Report Scope

PFAS Filtration Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.1 Billion

|

|

Market Size (2034)

|

$2.4 Billion

|

|

Market Growth Rate

|

9.3%

|

|

Segments

|

By Type of Chemical (Granular Activated Carbon (GAC), Ion Exchange Resins (IX), Specialty/Proprietary Adsorbents, Others), By Application (Water Treatment, Soil Remediation, Other Applications), By End-User (Municipal, Industrial, Chemical Manufacturing, Oil and Gas, Power Generation, Electronics and Semiconductors, Textile Industry, Pulp and Paper, Aerospace, Automotive, Mining, Waste Management (landfills, hazardous waste treatment facilities), Commercial, Residential, Government and Military), By Place of Treatment (Ex-situ Treatment, In-situ Treatment

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Calgon Carbon Corporation (Kuraray Co., Ltd.) (U.S.), Veolia Water Technologies (France), Evoqua Water Technologies LLC (U.S.), LANXESS AG (Germany), DuPont de Nemours, Inc. (U.S.), 3M Company (U.S.), Xylem Inc. (U.S.), AECOM (U.S.), Battelle Memorial Institute (U.S.), SUEZ SA (Veolia) (France), Mineral Technologies Inc. (U.S.), Cyclopure, Inc. (U.S.),

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

PFAS Filtration Chemicals Market Segmentation

By Type of Chemical

- Granular Activated Carbon (GAC)

- Ion Exchange Resins (IX)

- Specialty/Proprietary Adsorbents

- Others

By Application

- Water Treatment

- Soil Remediation

- Other Applications

By End-User

- Municipal

- Industrial

- Chemical Manufacturing

- Oil and Gas

- Power Generation

- Electronics and Semiconductors

- Textile Industry

- Pulp and Paper

- Aerospace

- Automotive

- Mining

- Waste Management (landfills, hazardous waste treatment facilities)

- Commercial

- Residential

- Government and Military

By Place of Treatment

- Ex-situ Treatment

- In-situ Treatment

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in PFAS Filtration Chemicals Market

- Calgon Carbon Corporation (Kuraray Co., Ltd.) (U.S.)

- Veolia Water Technologies (France)

- Evoqua Water Technologies LLC (U.S.)

- LANXESS AG (Germany)

- DuPont de Nemours, Inc. (U.S.)

- 3M Company (U.S.)

- Xylem Inc. (U.S.)

- AECOM (U.S.)

- Battelle Memorial Institute (U.S.)

- SUEZ SA (Veolia) (France)

- Mineral Technologies Inc. (U.S.)

- Cyclopure, Inc. (U.S.)

* List Not Exhaustive

Research Coverage

This report by USDAnalytics investigates the PFAS Filtration Chemicals Market, offering an extensive analysis of market dynamics, emerging trends, and future growth prospects. It highlights breakthroughs in adsorption and destruction technologies, from granular activated carbon (GAC) and ion exchange resins to advanced specialty adsorbents and supercritical water oxidation (SCWO) systems. The analysis reviews regulatory drivers, sustainability initiatives, and technology innovations shaping compliance strategies worldwide. This report is an essential resource for professionals seeking strategic insights into PFAS mitigation solutions across municipal, industrial, and environmental remediation applications.

Scope Highlights

- Segmentation:

- By Type of Chemical: Granular Activated Carbon (GAC), Ion Exchange Resins (IX), Specialty/Proprietary Adsorbents, Others

- By Application: Water Treatment, Soil Remediation, Other Applications

- By End-User: Municipal, Industrial, Chemical Manufacturing, Oil and Gas, Power Generation, Electronics and Semiconductors, Textile, Pulp & Paper, Aerospace, Automotive, Mining, Waste Management, Commercial, Residential, Government & Military

- By Place of Treatment: Ex-situ Treatment, In-situ Treatment

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historic Data: 2021–2024; Forecast Data: 2025–2034

- Companies Covered: Calgon Carbon (Kuraray), Veolia Water Technologies, Evoqua Water Technologies LLC, LANXESS AG, DuPont, 3M Company, Xylem Inc., AECOM, Battelle Memorial Institute, SUEZ (Veolia), Mineral Technologies Inc., Cyclopure Inc.

Methodology

The study follows a hybrid research methodology combining primary interviews with key stakeholders and secondary analysis from credible sources, including regulatory reports, patents, and company disclosures. Advanced market modeling using both top-down and bottom-up approaches ensures robust segment-level forecasts. Historical data is validated through statistical triangulation, while forward-looking estimates incorporate scenario modeling and technology adoption curves. Qualitative insights are supplemented by expert panel reviews, making the analysis highly actionable and reliable for strategic decisions.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements