U.S. Municipal Water Treatment Chemicals Market Value Analysis and Forecast

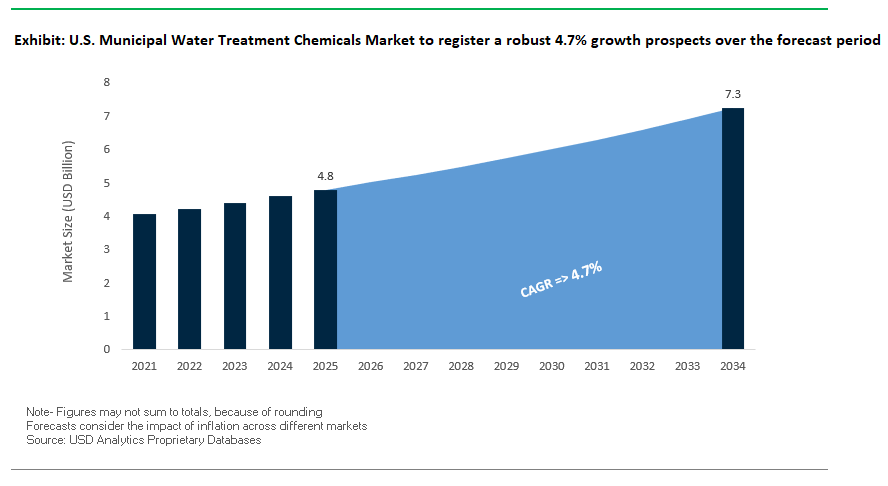

The U.S. Municipal Water Treatment Chemicals Market Size is estimated at $4.8 Billion in 2025 and is forecast to register an annual growth rate (CAGR) of 4.7% to reach $7.3 Billion by 2034.

The U.S. municipal water treatment chemicals market is undergoing a transformative phase driven by stricter federal mandates, advanced treatment goals, and innovation in green and digital technologies. Coagulation and flocculation continue to be foundational, with polyaluminum chloride (PACl) replacing traditional alum in many plants due to its ability to reduce sludge generation and deliver effluent turbidities.

Organic polymers such as cationic polyDADMAC are widely used for TSS removal efficiencies >90%, while bio-based alternatives like chitosan are gaining NSF/ANSI 60 certification for sustainable, biodegradable performance (AWWA Journal 2023). Corrosion control remains critical, especially in light of the updated Lead and Copper Rule Improvements (LCRI 2024), which mandates full replacement of lead service lines by 2037.

Orthophosphate inhibitors dosed at 0.5–1.5 mg/L can reduce lead leaching to <3 µg/L, with zinc orthophosphate showing enhanced efficacy in soft water systems (AWWA C815). Silicate inhibitors at 4–8 mg/L also offer protection by limiting corrosion to <0.1 mm/year (ASTM G199). Emerging contaminant regulation is reshaping treatment priorities: PFAS removal is rapidly scaling through high-capacity anion exchange resins and electrochemical oxidation technologies capable of >99% PFAS destruction at 15–25 kWh/kg (EPA ETV).

Meanwhile, enhanced coagulation using PACl and polymers can remove over 85% of microplastics in the 1–5 µm range (ASCE 68-21). Regulatory momentum is strong PFAS maximum contaminant levels (MCLs) were set at 4.0 ppt in 2024, intensifying demand for GAC and AOP systems. In response, utilities are embracing green chemistry, with on-site electrochemical hypochlorite generation reducing transport-related emissions by 40% (NSF/ANSI 61). Digital innovations are also reshaping dosing strategies, as AI-driven systems using real-time UV₂₅₄ monitoring cut chemical use by 15–25%, in line with findings from the USGS Integrated Monitoring & Research Program.

Market Trend: PFAS Remediation and Chlorine-Free Disinfection Redefine U.S. Municipal Water Treatment Priorities

The U.S. municipal water treatment chemicals market is undergoing a fundamental reorientation as utilities race to comply with the EPA’s 2024 PFAS National Primary Drinking Water Regulation (NPDWR), which enforces a 4 parts per trillion (ppt) maximum contaminant level for PFOA and PFOS. With over 3,000 water systems affected, demand is soaring for high-performance, PFAS-selective adsorbents and ion exchange resins, such as Calgon Carbon’s PFAS-Select™, which outperforms traditional activated carbon under low-concentration conditions. Backed by $10 billion in Bipartisan Infrastructure Law (BIL) PFAS funding, with half earmarked for small and rural systems, municipalities are rapidly replacing outdated chlorine-centric regimes. A parallel trend is the transition away from chloramine, due to disinfection byproduct (DBP) risks and public backlash. Los Angeles’ Hyperion 2030 Plan exemplifies this shift, replacing chloramines with UV and advanced oxidation processes (AOPs) that eliminate trace organics and carcinogens, while cities like Miami-Dade are deploying 3M’s ElectroChlor™ for safer, on-site chlorine generation. Sustainability pressures are intensifying: 30+ states offer incentives for carbon-neutral, non-toxic treatment solutions, driving adoption of AI-driven chemical optimization systems like Xylem’s Visenti™, which reduce alum dosing by up to 20% and save utilities hundreds of thousands annually. With PFAS lawsuits topping $15 billion and ESG mandates shaping utility procurement, chemical suppliers are being forced to pivot rapidly offering not just compliance but digital, safe, and climate-aligned innovation.

Growth Opportunity: Smart Infrastructure and Nutrient Recovery Create Multi-Billion Dollar Demand Surge

The next frontier of growth in the U.S. municipal water treatment chemicals market lies in intelligent infrastructure modernization and circular economy solutions, enabled by robust policy backing and tech readiness. Lead contamination remediation is a top priority: the BIL allocates $15 billion for lead service line (LSL) replacements, and utilities like Chicago are deploying orthophosphate inhibitors to prevent lead leaching during infrastructure transition generating a $200 million+ opportunity for corrosion control chemicals alone. Simultaneously, phosphorus recovery is emerging as a lucrative segment. Utilities like DC Water’s Blue Plains Advanced Wastewater Treatment Plant are commercializing recovered struvite a slow-release fertilizer sold at $500/ton through technologies like Ostara’s Pearl®, with Wisconsin’s 2025 mandate requiring P-recovery for plants exceeding 1 MGD. Decentralized systems also represent a breakout market: solar-powered RO and chitosan-based prefilters in tribal and remote communities (e.g., Navajo Nation) deliver arsenic reduction and potable reuse at a fraction of centralized treatment costs. Strategic advantages abound: utilities that integrate sustainable chemicals and smart dosing qualify for 15% additional BIL grant support, while carbon credits for struvite recovery offer up to $15 per ton CO₂e under the Climate Action Reserve. As firms like American Water (NYSE: AWK) commit to net-zero operations by 2030, early movers in green chemistry, AI integration, and nutrient monetization will command premium contracts, ESG leadership, and policy-aligned growth for the decade ahead.

Competitive Landscape: U.S. Municipal Water Treatment Chemicals Market

The U.S. municipal water treatment chemicals market is mature but highly competitive. A few global companies hold over half the market share while numerous regional firms and tech startups are evolving specific niches. Tier 1 companies like Ecolab, Solenis, Kemira, and BASF together account for about 55% of the market. They benefit from strong technology portfolios, nationwide distribution, and solid municipal contracts. Ecolab is notable for its integrated 3D TRASAR platform and a recent $400 million smart water management contract with Chicago. This reinforces its lead in tracking compliance through IoT. Solenis relies on deep relationships from long-term operation and maintenance contracts and specializes in advanced polymers and PFAS-removing agents like FloPam PF. Kemira, recognized for its low-carbon and phosphate-free chemicals, aims to be a regulatory leader as EPA mandates tighten. Meanwhile, BASF is moving strongly toward sustainability, with innovations such as chitosan-based coagulants and silicate inhibitors, meeting the needs of utilities looking for greener options.

A second competitive tier includes USALCO, Chemtrade, Carus Group, and PVS Chemicals, which together control about 30% of the market. These firms focus on high-volume, cost-effective commodity products and thrive by serving regional areas with customized delivery. USALCO, the largest alum supplier in the country, has a local delivery model across the Northeast and Midwest. Chemtrade is vertically integrated in chlorine supply and is actively pursuing work under the SECURE Water Act. Carus Group, a key player in permanganates, is increasingly focused on lead pipe replacement as regulations require municipalities to replace millions of outdated service lines. PVS Chemicals specializes in on-site generation and serves emergency response and flood-prone urban areas in the Great Lakes region.

The third tier consists of digital-first startups and application-specific innovators, many funded by venture capital or federal infrastructure grants. AquaHawk leads this group with AI-powered chemical dosing platforms designed for mid-sized utilities. It recently secured $28 million in Series C funding. Other companies like ClearAqua are developing electrochemical disinfection methods for regions affected by PFAS, while Nexom provides phosphate-free inhibitors financed by state revolving funds. Though these disruptors hold a small market share (~15%), they are changing procurement models and promoting chemical-as-a-service concepts, aligning product development with requirements for climate resilience.

From a technology standpoint, the market is shifting from traditional products to digitally optimized and environmentally friendly chemistries. Polyaluminum chloride remains the leading product with a 40% market share. However, companies like Kemira and USALCO are creating low-total organic carbon versions to cut down on disinfection byproducts. Sodium hypochlorite, making up 25% of the market, continues to see demand sustained through on-site generation systems pioneered by Chemtrade and PVS, improving safety and logistics. Orthophosphates and chloramines, once stable niches, are now under regulatory pressure, leading to next-generation reformulations. BASF is working on phosphate alternatives while Solenis is developing stabilized blends.

Competition is heating up in three main areas: PFAS mitigation, lead service line replacement, and climate resilience. The U.S. government allocated $6 billion for PFAS remediation, spurring competition among companies such as Kemira, with its activated alumina systems, and Ecolab, offering chemical destruction platforms. Additionally, the 2030 deadline to replace 15 million lead pipes opens up significant opportunities for corrosion control vendors like Carus and BASF. On the climate front, FEMA's funding for flood-ready infrastructure is fostering collaborations like BASF’s disaster resilience programs and AquaHawk’s adaptive dosing linked to weather forecasts.

Digital transformation and sustainability are essential for survival in this market. Ecolab’s cloud-based monitoring, Kemira’s AI sludge optimization, and AquaHawk’s real-time leak-adjusted dosing show how the industry is shifting toward smart water solutions. Sustainability initiatives are evident in carbon-neutral production processes, such as Kemira's biogas-powered plants, circular solutions like BASF’s alum recovery program, and Solenis’ focus on bio-based products to help utilities obtain LEED credits. Lastly, emerging business models like Chemical-as-a-Service, performance-based contracts, and resilience funding partnerships are altering how chemicals are acquired, priced, and used. Together, these trends highlight a market driven by regulatory demands, climate urgency, and digital innovation.

U.S. Municipal Water Treatment Chemicals Market – Segmentation Insights (2025–2034)

By Type of Chemical: Coagulants Dominate, Adsorbents Surge Amid PFAS Regulations

In the United States municipal water treatment chemicals market, coagulants and flocculants are projected to hold the highest market share in 2025 at around 36.2%, driven by their essential role in turbidity and organic matter removal. Widely used coagulants like alum and polyDADMAC are standard across drinking water plants for sedimentation and clarifying processes. Compliance with the EPA’s Surface Water Treatment Rule and rising turbidity levels due to stormwater events are reinforcing their use across both small and large municipal systems.

However, the adsorbents category is set to expand at the fastest pace, with a projected CAGR of 6.7% through 2034, propelled by stringent federal PFAS regulations. The EPA's finalized Maximum Contaminant Levels (MCLs) for perfluorinated compounds set at below 4 parts per trillion are compelling utilities to deploy activated carbon and ion exchange resins at an accelerated rate. These advanced materials are increasingly used for targeted removal of PFAS, pesticides, and pharmaceutical residues in both source water and effluent polishing stages.

Biocides and disinfectants, accounting for nearly 27.7% of the market, remain crucial for residual disinfection, especially in chloramine-based treatment systems preferred for minimizing disinfection by-products (DBPs). Meanwhile, corrosion and scale inhibitors are gaining renewed importance amid the Lead and Copper Rule Revisions (LCRR), which mandate corrosion control optimization for lead service line mitigation.

.png)

By Application: Drinking Water Dominates as Compliance Tightens on Lead and Emerging Contaminants

Drinking water treatment constitutes the largest share of the U.S. municipal water treatment chemicals market, estimated at 58.1% in 2025, with stable growth supported by compliance with the Safe Drinking Water Act (SDWA) and increased federal funding through the Bipartisan Infrastructure Law. Utilities across the country are investing in chemical treatment solutions such as coagulants, corrosion inhibitors, and disinfectants to address challenges tied to source water variability, lead contamination, and new PFAS standards.

A particularly strong driver is the implementation of the Lead and Copper Rule Revisions (LCRR), which place a renewed emphasis on corrosion control optimization and service line inventory tracking. These regulatory shifts are prompting a rise in demand for phosphate-based corrosion inhibitors, pH control chemicals, and advanced monitoring technologies.

On the other hand, municipal wastewater treatment accounts for roughly 44.7% of market share, with growing emphasis on nutrient removal (especially nitrogen and phosphorus) and control of contaminants of emerging concern (CECs). Utilities are adopting adsorbents, advanced coagulants, and bioaugmentation strategies to improve effluent quality in alignment with Clean Water Act permits and Total Maximum Daily Load (TMDL) requirements. As U.S. municipalities aim to enhance sustainability and resilience, chemical treatment remains a cornerstone of safe and compliant public water infrastructure.

U.S. Municipal Water Treatment Chemicals Market Report Scope

U.S. Municipal Water Treatment Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.8 Billion

|

|

Market Size (2034)

|

$7.3 Billion

|

|

Market Growth Rate

|

4.7%

|

|

Segments

|

By Type of Chemical (Coagulants and Flocculants, Flocculants, Biocides and Disinfectants, pH Adjusters and Neutralizers, Corrosion and Scale Inhibitors, Adsorbents, Other Specialty Chemicals), By Application (Drinking Water Treatment, Municipal Wastewater Treatment), By End-User (Public Water Systems (PWSs), Publicly Owned Treatment Works (POTWs)), By Form of Chemical (Liquid, Powder/Solid, Gas

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ecolab Inc. (U.S.), Solenis LLC (U.S.), Kemira Oyj (Finland), SNF Holding Company (U.S.), BASF SE (Germany), Veolia Water Technologies (France), SUEZ Water Technologies and Solutions (France), The Dow Chemical Company (U.S.), Kurita Water Industries Ltd. (Japan), ChemTreat, Inc. (U.S.), Hawkins, Inc. (U.S.), USALCO (U.S.)

|

U.S. Municipal Water Treatment Chemicals Market Segmentation

By Type of Chemical

- Coagulants and Flocculants

- Inorganic Coagulants

- Organic Coagulants

- Flocculants

- Biocides and Disinfectants

- Oxidizing Biocides

- Non-Oxidizing Biocides

- pH Adjusters and Neutralizers

- Corrosion and Scale Inhibitors

- Phosphates

- Silicates.

- Zinc compounds

- Adsorbents

- Other Specialty Chemicals

By Application

- Drinking Water Treatment

- Raw Water Clarification

- Filtration Aids.

- Primary and Secondary Disinfection

- Taste and Odor Control

- Corrosion Control in Distribution Systems

- PFAS and Lead Removal

- Municipal Wastewater Treatment

- Primary Treatment

- Secondary (Biological) Treatment support.

- Tertiary Treatment

- Sludge Treatment and Dewatering

- Odor Control.

- Wastewater Reuse and Recycling

By End-User

- Public Water Systems (PWSs)

- Publicly Owned Treatment Works (POTWs)

By Form of Chemical

Top Companies in U.S. Municipal Water Treatment Chemicals Market

- Ecolab Inc. (U.S.)

- Solenis LLC (U.S.)

- Kemira Oyj (Finland)

- SNF Holding Company (U.S.)

- BASF SE (Germany)

- Veolia Water Technologies (France)

- SUEZ Water Technologies and Solutions (France)

- The Dow Chemical Company (U.S.)

- Kurita Water Industries Ltd. (Japan)

- ChemTreat, Inc. (U.S.)

- Hawkins, Inc. (U.S.)

- USALC(U.S.)

* List Not Exhaustive

Research Coverage

This USDAnalytics report provides a comprehensive and data-driven analysis of the U.S. Municipal Water Treatment Chemicals Market, focusing on growth dynamics, technological advancements, and regulatory influences shaping the industry. The coverage spans critical chemical categories—coagulants and flocculants, corrosion and scale inhibitors, biocides, adsorbents, and specialty chemicals—aligned with the evolving regulatory landscape under EPA mandates and the Bipartisan Infrastructure Law.

The report highlights key market trends such as PFAS remediation, chlorine-free disinfection, bio-based formulations, and AI-driven dosing optimization. Special attention is given to sustainability-driven innovations, nutrient recovery systems (e.g., struvite recovery), and digital transformation in chemical dosing, all of which are becoming essential for utility modernization and compliance with federal funding requirements.

Scope Includes:

- Segmentation

- By Type of Chemical: Coagulants & Flocculants, Biocides & Disinfectants, Corrosion & Scale Inhibitors, Adsorbents, Specialty Chemicals.

- By Application: Drinking Water Treatment, Municipal Wastewater Treatment, Advanced PFAS & Lead Removal, Nutrient Recovery.

- By End-User: Public Water Systems (PWSs), Publicly Owned Treatment Works (POTWs).

- By Form: Liquid, Powder/Solid, Gas.

- Geographic Focus: United States with regional dynamics impacting procurement and technology adoption.

- Study Period: Historic data from 2021–2024 and forecast data from 2025–2034.

- Top Companies Covered: Ecolab Inc., Solenis LLC, Kemira Oyj, BASF SE, SNF Holding Company, Veolia Water Technologies, SUEZ Water Technologies, The Dow Chemical Company, Kurita Water Industries, ChemTreat Inc., Hawkins Inc., and USALCO.

Methodology

The methodology for this report leverages primary and secondary research for robust market intelligence:

- Primary Research: In-depth interviews with water utility directors, municipal engineers, chemical suppliers, and environmental regulators, focusing on PFAS mitigation strategies, corrosion control, and chemical optimization technologies.

- Secondary Research: Extensive analysis of EPA regulatory frameworks (LCRI, NPDWR), AWWA standards, utility infrastructure plans, government databases, and company financial disclosures.

- Data Modeling:

- Bottom-Up Approach: Estimation of market size based on chemical dosing rates, treatment plant capacities, and application-specific chemical consumption patterns across municipal segments.

- Forecasting Technique: Time-series analysis integrated with macroeconomic indicators, infrastructure investment pipelines, and regulatory compliance timelines.

- Validation: Triangulation using multiple data sources, cross-verification with utility financial reports, and benchmarking against peer-reviewed technical literature.

- Scenario Modeling: Evaluating impact scenarios for PFAS regulations, AI-enabled dosing adoption, and nutrient recovery incentives on market demand by 2034.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements