Water Purification Adsorbents Market: Growth Analysis and Value Forecast

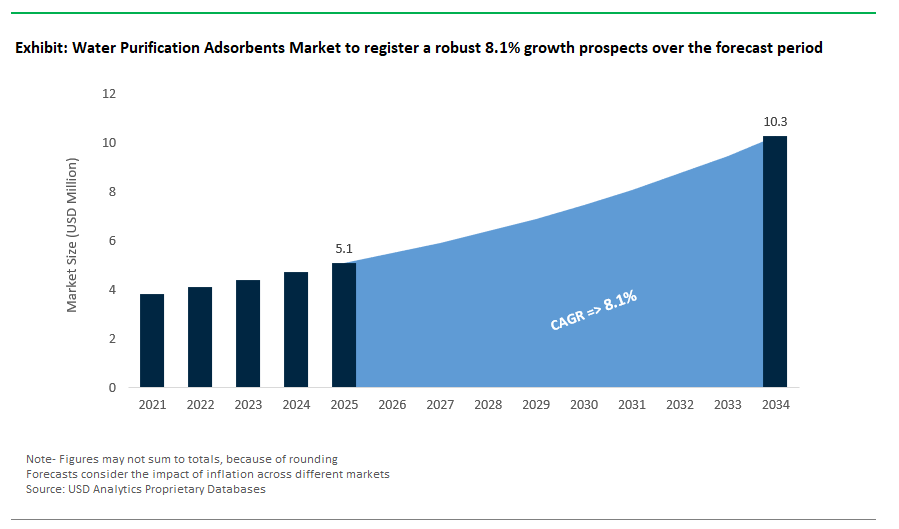

The global market for adsorbents in water purification is evolving rapidly, reaching a value of $5.1 billion in 2025 and projected to double to $10.3 billion by 2034, supported by a robust CAGR of 8.1%. This momentum is underpinned by the urgent need to address emerging contaminants, regulatory tightening, and the limitations of legacy treatment technologies. Activated carbon, particularly granular activated carbon (GAC), remains the cornerstone of industrial and municipal purification systems due to its high surface area (1,000–1,500 m²/g as per ASTM D3860) and strong micropore volume performance (0.25–0.5 cm³/g), especially in removing volatile organic compounds and legacy pollutants.

However, long-standing dependence on thermal regeneration methods recovering only 70–85% of sorption capacity with 10–15% structural degradation per cycle continues to present operational cost and sustainability challenges, especially in high-throughput industrial settings. GAC’s removal efficiency for persistent PFAS compounds, such as PFOA and PFOS, remains high at 90–99% for low ppb concentrations, yet breakthrough times vary significantly across influent matrices, raising design complexity for utilities aiming for multi-contaminant compliance.

The competitive dynamics of the market are beginning to shift, with advanced adsorbents such as metal-organic frameworks (MOFs) entering pilot stages. For instance, MIL-101 variants have demonstrated high arsenate adsorption capacities, offering a path forward for utilities struggling with trace metal remediation in decentralized applications. This pivot toward next-gen materials is not just driven by performance metrics but also by a need for scalability, selectivity, and lower regeneration energy inputs. As global water security challenges intensify across South Asia, Sub-Saharan Africa, and the drought-prone western U.S., adsorbent-based purification systems are expected to play a more central role in treatment infrastructure, driving innovation and capital flows across both established and experimental material classes.

Major Shifts and Emerging Opportunities in the Adsorbents Market

Market Trend: Rise of Next-Generation Adsorbents MOFs and Engineered Biochar Challenge Activated Carbon Dominance

The Adsorbents for Water Purification market is undergoing a decisive shift away from traditional activated carbon toward high-performance, engineered materials such as Metal-Organic Frameworks (MOFs) and functionalized biochar. This trend is being driven by the convergence of tightening global regulations especially around emerging contaminants like PFAS, arsenic, and phosphate and the growing limitations of legacy carbon technologies. MOFs, once considered purely academic due to water instability and scalability concerns, have reached commercial viability, with firms like BASF deploying MOF-based systems in EU industrial wastewater treatment to remove heavy metals like mercury and cadmium. In parallel, MOFs like Zr-TCA from UC Berkeley have demonstrated 99% PFAS removal at a fraction of the energy cost, offering a compelling alternative to granular activated carbon (GAC), which struggles with shorter lifespans and poor selectivity. On the biochar front, USDA-funded trials and utility-scale pilots in California are validating the cost and performance benefits of iron-coated and aluminum-modified biochar, especially for nutrient removal and arsenic mitigation. Regulatory tailwinds, such as the EPA’s 2024 PFAS threshold of 4 ppt, are making traditional GAC-based systems increasingly obsolete for municipal and industrial operators. Moreover, biochar derived from sewage sludge and agri-waste is aligning with circular economy mandates, cutting adsorbent procurement costs by up to 50% while reducing landfill burden. As water utilities and industrial processors demand contaminant-specific solutions with longer service lives and greater sustainability, the dominance of activated carbon is giving way to modular, tunable adsorbents designed for precision remediation.

Market Opportunity: Mining Sector Emerges as High-Value Application for MOF and Biochar Adsorbents

A significant untapped opportunity for adsorbent manufacturers lies in the intersection of critical mineral extraction and water reuse in the mining industry. As regulatory and ESG pressures escalate, mining companies are seeking integrated solutions that enable both resource recovery and wastewater purification. Advanced adsorbents especially MOF-based systems and functionalized biochar are showing breakthrough potential in recovering lithium, boron, rare earth elements (REEs), and even radioactive contaminants from mining effluents. For instance, EnergyX’s 2024 demonstration plant uses MOF-functionalized membranes to recover over 98% lithium from South American brine sources while purifying the residual water for reuse an innovation directly targeting the water-intensive nature of battery metal extraction. Likewise, Chile’s SQM and Malaysia’s Lynas Rare Earths are actively testing aluminum-grafted biochar and phosphonate-modified MOFs to selectively adsorb boron, thorium, and uranium from high-salinity or acid mine drainage (AMD) streams. These developments signal a dual-value proposition: not only can mining operators lower their freshwater procurement costs by up to 60% (as per USGS estimates), but they can also monetize previously wasted effluent through critical mineral recovery. For adsorbent suppliers, this opens a new frontier of high-margin industrial applications where performance, specificity, and reusability outweigh bulk cost setting the stage for rapid adoption of engineered materials over commodity GAC. With global investment in rare earths and lithium processing expected to surge amid clean energy transitions, this vertical represents a high-growth, strategic pivot point for the adsorbents market.

Competitive Landscape: Adsorbents Market for Water Purification

The global adsorbents market for water purification is led by a combination of large chemical companies with varied portfolios and smaller companies focusing on specific contaminants. Activated carbon is still the main product type, especially in granular and powdered forms. Specialty adsorbents like zeolites, polymeric resins, activated alumina, and silica gels are becoming more popular for applications that require targeted contaminant removal.

Calgon Carbon (Kuraray) is a leader in activated carbon adsorbents for drinking water, wastewater, and groundwater. Their proprietary products include Filtrasorb® and Centaur®. Mitsubishi Chemical also has a strong presence with its Diahope™ and Shirasagi™ activated carbon lines for drinking and process water. Clariant is a key supplier of activated alumina for removing arsenic and fluoride from drinking water.

W. R. Grace and Honeywell UOP are well-known for synthetic zeolites and silica gel-based systems for industrial process water. BASF, Evonik, and Cabot provide specialized or functionalized adsorbents aimed at removing trace organics or serving as support media. JALON has created a cost-effective position in industrial-grade zeolites and activated alumina. At the same time, Arkema has limited direct involvement in core adsorbents but contributes to water treatment through related chemical technologies.

Competition in this market is driven by proven removal efficiencies, cost-performance ratios, reusability or reactivation capabilities, and the ability to handle regulated contaminants like PFAS, arsenic, and VOCs.

Adsorbents Market for Water Purification – Segmentation Insights (2025–2034)

Activated Carbon Dominates Adsorbent Types, Bio-based Adsorbents Exhibit Fastest Growth

Activated carbon commands the largest market share among adsorbent types, accounting for 42.3% of the adsorbents market for water purification in 2025. Its prominent position is driven by stringent regulations mandating the effective removal of contaminants such as PFAS and pharmaceuticals from drinking water. Activated carbon’s high adsorption efficiency, scalability, and proven effectiveness across various purification applications significantly bolster its market presence. Meanwhile, bio-based adsorbents, encompassing innovative materials like biochar and chitosan, are experiencing the fastest growth at a notable 9.3% CAGR. This rapid expansion results from an increased global emphasis on sustainability and environmentally responsible water treatment solutions. Other significant adsorbents include zeolites, growing at a healthy pace primarily due to their efficacy in ammonium and radionuclide removal (10% CAGR), activated alumina for fluoride and arsenic removal, polymer-based adsorbents witnessing rising adoption for specialized contaminant targeting, silica gel favored for moisture-sensitive purification, and traditional clay & mineral adsorbents maintaining steady use in cost-sensitive applications.

.png)

Polishing/Tertiary Treatment Holds Largest Functional Share, Wastewater Resource Recovery Fastest Growing

In the adsorbents market segmented by function, polishing or tertiary treatment occupies the leading position with a market share of 34.2% in 2025. This dominance reflects heightened global initiatives aimed at micropollutant elimination particularly pharmaceuticals, pesticides, and industrial contaminants resulting in widespread adoption across municipal and industrial water treatment sectors. In contrast, the wastewater resource recovery segment exhibits the fastest growth, achieving a robust CAGR of 9.7% during 2025–2034. Its growth trajectory is closely linked to increasing implementation of circular economy strategies, targeting the recovery of valuable nutrients such as phosphorus and nitrogen for reuse. Additionally, Point-of-Use (POU) systems show significant momentum driven by rising consumer awareness around PFAS contamination and preference for personalized filtration solutions at household levels. Meanwhile, primary treatment remains integral for initial contaminant reduction, while Point-of-Entry (POE) systems continue steady expansion, particularly in residential and commercial infrastructures demanding comprehensive water purification solutions at entry points.

United States Leads Adsorbents Market with Federal Funding and PFAS Innovation

The United States stands as a central driver of the global adsorbents market for water purification, propelled by unprecedented federal investments and a relentless focus on emerging contaminants such as PFAS. The Infrastructure Investment and Jobs Act, the largest federal commitment to water infrastructure in U.S. history, has earmarked over $50 billion to the EPA for upgrading the nation’s drinking water, wastewater, and stormwater networks. A landmark $15 billion allocation specifically targets the Drinking Water State Revolving Fund to replace aging lead service lines, catalyzing demand for advanced adsorbent solutions that effectively capture heavy metals and toxicants. Additionally, $4 billion is channeled towards addressing “emerging contaminants” notably PFAS or “forever chemicals” which is fueling a surge in the development and deployment of next-generation adsorbents engineered for selectivity, durability, and environmental compliance.

The EPA’s strategic promotion of innovative and alternative wastewater treatment technologies, showcased in its Wastewater Treatment Clearinghouse, is accelerating the adoption of adsorbent-based water purification systems across municipalities. As utilities modernize aging infrastructure, the integration of smart, high-capacity, and regenerable adsorbent materials is becoming an essential component of long-term water quality assurance in the United States. The ongoing transformation, underpinned by government funding and regulatory mandates, positions the U.S. as a frontrunner in the commercialization and innovation of water purification adsorbents, setting standards for the global industry.

China Accelerates Advanced Materials and Bio-Based Adsorbents for Sustainable Water Purification

China’s rapid industrial growth and urbanization are fundamentally reshaping the country’s water purification adsorbents market. The competitive landscape is moving decisively beyond conventional activated carbon, with leading Chinese enterprises and research institutions investing in advanced adsorbent technologies such as zeolites, graphene, and metal-organic frameworks (MOFs) for highly selective contaminant removal. In response to escalating environmental regulations, there is a pronounced shift toward sustainable and cost-efficient adsorbent feedstocks including rice husks, bamboo, and sugarcane bagasse positioning China as a key innovator in the development of bio-based adsorbents.

Sustainability is driving not only materials selection but also process innovation. The growing focus on regenerable media, although requiring upfront capital for infrastructure, promises long-term operational cost savings and improved lifecycle sustainability. China’s municipal water sector is an especially vibrant market for ion-exchange zeolites, prized for their efficiency and cost-effectiveness in ammonia and heavy metal removal. These trends underscore China’s dual emphasis on environmental stewardship and advanced materials science, cementing its role as a major player in the global adsorbents market.

India Champions Affordable, Sustainable Adsorbents with Breakthrough Nanomaterial Technologies

India is fast emerging as an epicenter for innovation in the adsorbents market, with a focus on affordable, scalable, and sustainable solutions for both urban and rural water purification needs. Pioneering research at the Indian Institute of Technology (IIT) Madras has led to the development of AMRIT (Anion and Metal Removal by Indian Technology), a breakthrough nanomaterial-based adsorbent platform for arsenic, fluoride, and multi-contaminant removal. The AMRIT technology, rolled out across diverse applications from household purifiers to large-scale community systems demonstrates India’s ability to deliver high-impact, low-maintenance water treatment solutions at scale.

A standout feature is the maintenance-free iron removal unit, eliminating the need for backwashing and sludge handling a persistent challenge in traditional water treatment. Cross-border collaborations, such as the Indo-US Science and Technology Endowment Fund’s project in West Bengal, further underscore India’s leadership in deploying innovative in-situ adsorbent generation for localized water challenges. By integrating advanced materials with community-centric delivery models, India is driving a new paradigm of affordable and sustainable water purification.

Germany Advances Green Adsorbents and Surface-Modified Materials for Superior Water Quality

Germany continues to set global benchmarks in adsorbents research and development, emphasizing the transition toward green, sustainable, and high-efficiency water purification materials. Leading academic and industrial R&D initiatives are advancing the use of renewable and biodegradable materials such as starch, chitosan, and nanoscale structures including zeolites and MOFs as the foundation for next-generation inorganic adsorbents. A core research focus lies in surface modification techniques, which are significantly enhancing the adsorption capacity and regenerative performance of various adsorbents.

Germany’s “green adsorbents” strategy is anchored in the valorization of agricultural and forestry waste streams, with biochar derived from forestry waste showing removal efficiencies above 69% for heavy metals in wastewater. This sustainability-first approach, combined with world-class engineering and regulatory rigor, is positioning Germany as a leader in the development of eco-friendly, high-performance adsorbents. The country’s commitment to R&D in sustainable water treatment technologies is shaping both European and global standards in water purification.

Canada Tightens PFAS Regulations and Drives Advanced Adsorbent Adoption

Canada’s regulatory landscape is rapidly evolving, making it one of the most dynamic markets for advanced water purification adsorbents. The federal government’s dramatic reduction in PFAS limits to just 30 nanograms per liter across 25 compounds represents one of the strictest regulatory stances worldwide, compelling water utilities and municipalities to invest in next-generation adsorbent materials and processes. This move is supported by a broader “source-to-tap” water quality approach, with enhanced guidelines for a wide array of microbiological and chemical parameters, including aluminum and antimony.

As municipal water providers assess contaminant levels and plan for extensive treatment upgrades, demand is surging for specialized adsorbents capable of meeting these stringent standards. Canada’s proactive regulatory measures are creating both legal and economic incentives for the rapid adoption of advanced adsorbent technologies. The country’s rigorous policies are not only transforming domestic water treatment but also setting influential precedents for global best practices in adsorbents deployment and water quality management.

Japan Drives Global Impact with Deployable Adsorbent Innovations and International Outreach

Japan distinguishes itself in the global adsorbents market through its emphasis on deployable, user-friendly technologies and international development partnerships. Nippon Poly-Glu Co., Ltd. exemplifies this with the invention of PGα21Ca a polyglutamic acid-based water purification “magic powder” derived from fermented soybeans, engineered to aggregate and remove impurities swiftly and efficiently. This technology, designed for easy use and local management, has been deployed in nearly 80 countries, improving water access for 18 million people and creating over 1,500 jobs globally.

Japan’s government, through robust Official Development Assistance (ODA), has historically invested billions into international water and sanitation projects, reinforcing its reputation as a leader in humanitarian and infrastructure-focused water solutions. By combining technological ingenuity with capacity-building and sustainability, Japan is catalyzing the global adoption of simple, scalable, and community-empowering adsorbent technologies.

France Pioneers Energy-Positive Wastewater Plants and Digital Water Solutions

France is carving a unique position in the adsorbents market through its leadership in sustainable infrastructure and the digital transformation of water management. Industry leaders such as SUEZ are developing innovative approaches to water resource protection, from large-scale wastewater reuse and desalination to the deployment of decentralized, off-grid purification systems. A notable example is the energy-positive wastewater treatment plant in Nice, designed to generate four times the energy it consumes, setting a new standard for sustainability in municipal infrastructure.

The French market is also at the forefront of integrating digital technologies for leak detection, predictive maintenance, and infrastructure optimization. EU-funded pilots, like the solar-powered, self-sufficient purification project in Côte d'Azur, showcase France’s commitment to combining renewable energy with cutting-edge adsorbent systems. These initiatives are driving both industrial and community-level innovation, positioning France as a hub for future-ready, digitally integrated water purification solutions.

United Kingdom Ramps Up Water Sustainability with Smart Infrastructure and Stewardship Programs

The United Kingdom is intensifying its efforts in water sustainability through a combination of ambitious government targets, infrastructure modernization, and private-sector collaboration. With a national goal to halve water leakage by 2050, the UK is investing heavily in the adoption of smart sensors, predictive analytics, and advanced adsorbent technologies for leak detection and water savings. Regulatory initiatives also aim to cut per capita water consumption from 143 to 110 liters per day by 2050, supported by standards review and extensive public engagement.

Private-sector partnerships, such as the Strategic Panel’s Market Improvement Fund with Yorkshire Water, are fostering the implementation of water stewardship programs that equip businesses with practical tools for sustainable water use. The “Plan for Water” integrates policies to restore water bodies, curb pollution, and boost supply resilience all of which drive demand for innovative adsorbents and next-generation treatment technologies. The UK’s holistic, data-driven approach is positioning it as a leader in advanced water sustainability and resource management.

Adsorbents Market for Water Purification Report Scope

Adsorbents Market for Water Purification

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.1 Billion

|

|

Market Size (2034)

|

$10.3 Billion

|

|

Market Growth Rate

|

8.1%

|

|

Segments

|

By Adsorbent Type (Activated Carbon, Zeolites, Silica Gel, Activated Alumina, Clay and Minerals, Metal Oxides, Polymer-based Adsorbents, Bio-based Adsorbents), By Application (Organic Contaminant Removal, Inorganic Contaminant Removal, Emerging Contaminant Removal, Color and Odor Removal, Desalination Support), By Function (Primary Treatment, Polishing/Tertiary Treatment, Point-of-Use (POU) Systems, Point-of-Entry (POE) Systems, Wastewater Resource Recovery), By End-User Industry (Municipal Water Treatment, Industrial Water Treatment, Food and Beverage, Pharmaceuticals, Textiles and Leather, Pulp and Paper, Mining and Metals, Residential/Household, Commercial), By Form (Granules/Extrudates, Powders, Pellets, Beads/Spheres, Fabrics/Non-wovens

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE (Germany), Calgon Carbon Corporation (Kuraray Co., Ltd.) (U.S.), W. R. Grace and Co.-Conn. (U.S.), Clariant (Switzerland), Evonik Industries AG (Germany), Cabot Corporation (U.S.), Mitsubishi Chemical Corporation (Japan), Arkema SA (France), Honeywell International Inc. (U.S.), JALON (China)

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Adsorbents Market for Water Purification Market Segmentation

By Adsorbent Type

- Activated Carbon

- Granular Activated Carbon (GAC)

- Powdered Activated Carbon (PAC)

- Activated Carbon Fibers (ACF)

- Zeolites

- Silica Gel

- Activated Alumina

- Clay and Minerals

- Metal Oxides

- Polymer-based Adsorbents

- Bio-based Adsorbents

- Chitosan

- Lignin

- Cellulose

- Agricultural Waste

By Application

- Organic Contaminant Removal

- Pesticides/Herbicides

- Pharmaceuticals and Personal Care Products (PPCPs)

- Organic Solvents

- Natural Organic Matter (NOM)

- Inorganic Contaminant Removal

- Heavy Metals (Arsenic, Lead, Mercury, Cadmium)

- Fluoride

- Nitrates/Nitrites

- Ammonia

- Emerging Contaminant Removal

- Per- and Polyfluoroalkyl Substances (PFAS)

- Microplastics

- Endocrine Disruptors

- Color and Odor Removal

- Desalination Support

By Function

- Primary Treatment

- Polishing/Tertiary Treatment

- Point-of-Use (POU) Systems

- Point-of-Entry (POE) Systems

- Wastewater Resource Recovery

By End-User Industry

- Municipal Water Treatment

- Drinking Water Plants

- Wastewater Treatment Plants (WWTPs)

- Industrial Water Treatment

- Food and Beverage

- Pharmaceuticals

- Textiles and Leather

- Pulp and Paper

- Mining and Metals

- Residential/Household

- Commercial

By Form

- Granules/Extrudates

- Powders

- Pellets

- Beads/Spheres

- Fabrics/Non-wovens

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Adsorbents Market for Water Purification

- BASF SE (Germany)

- Calgon Carbon Corporation (Kuraray Co., Ltd.) (U.S.)

- W. R. Grace and Co.-Conn. (U.S.)

- Clariant (Switzerland)

- Evonik Industries AG (Germany)

- Cabot Corporation (U.S.)

- Mitsubishi Chemical Corporation (Japan)

- Arkema SA (France)

- Honeywell International Inc. (U.S.)

- JALON (China)

* List Not Exhaustive

Research Coverage

This report offers a focused analysis of the global adsorbents market for water purification, highlighting key breakthroughs, market drivers, and in-depth segmentation by adsorbent type, application, function, end-user industry, and form. It reviews the transition to advanced materials—including metal-organic frameworks, engineered biochar, and sustainable bio-based adsorbents—while examining adoption trends across major geographies and end-use sectors. With strategic insights and data-backed reviews, this report is an essential resource for industry professionals navigating regulatory changes, sustainability mandates, and new opportunities in water purification. USDAnalytics delivers the clarity and actionable intelligence needed for forward-thinking decision-makers.

Scope Highlights:

- Segmentation:

- By Adsorbent Type: Activated Carbon, Zeolites, Silica Gel, Activated Alumina, Clay and Minerals, Metal Oxides, Polymer-based Adsorbents, Bio-based Adsorbents

- By Application: Organic Contaminant Removal, Inorganic Contaminant Removal, Emerging Contaminant Removal, Color and Odor Removal, Desalination Support

- By Function: Primary Treatment, Polishing/Tertiary Treatment, Point-of-Use (POU) Systems, Point-of-Entry (POE) Systems, Wastewater Resource Recovery

- By End-User Industry: Municipal Water Treatment (Drinking Water, Wastewater Plants), Industrial Water Treatment, Food and Beverage, Pharmaceuticals, Textiles and Leather, Pulp and Paper, Mining and Metals, Residential/Household, Commercial

- By Form: Granules/Extrudates, Powders, Pellets, Beads/Spheres, Fabrics/Non-wovens

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Data Coverage: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Key Players: BASF SE, Calgon Carbon Corporation (Kuraray Co., Ltd.), W. R. Grace and Co.-Conn., Clariant, Evonik Industries AG, Cabot Corporation, Mitsubishi Chemical Corporation, Arkema SA, Honeywell International Inc., JALON (China) (list not exhaustive)

Methodology

USDAnalytics applies a robust, multi-stage research methodology for the Adsorbents Market for Water Purification, integrating primary interviews with market participants and extensive secondary research from technical literature, patents, and regulatory databases. Market sizing and forecasting rely on proprietary modeling, triangulated with verified historical data (2021–2024) and scenario-based projections to 2034. Each market segment is mapped for performance, adoption rates, and regulatory drivers, with special emphasis on emerging technologies and material innovations. All analysis undergoes peer review and sensitivity checks to ensure credible, actionable insights for industry professionals and strategic decision-makers.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements