Global Adsorbents Market Overview

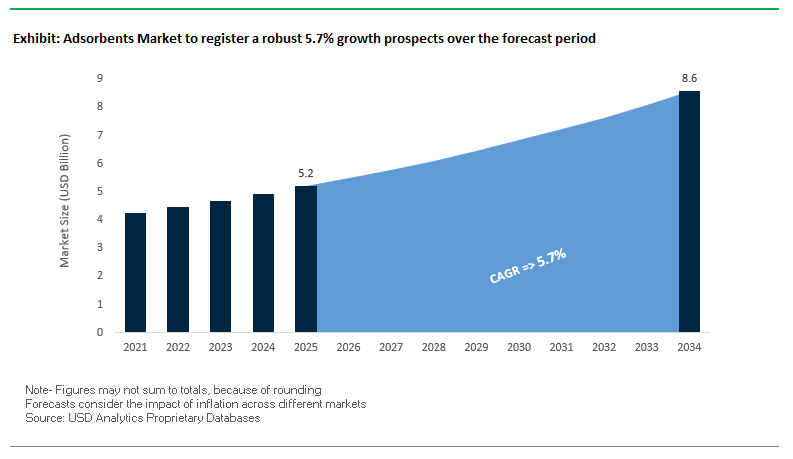

The global adsorbents market is projected to expand from $5.2 billion in 2025 to $8.6 billion by 2034, growing at a CAGR of 5.7%. This growth is driven by the increasing need for industrial process optimization, compliance with environmental regulations, adoption of innovative adsorbent materials, and support for the emerging hydrogen economy. Advanced adsorbents are now essential for purifying gases and liquids in petroleum refining, gas processing, and water treatment, helping protect expensive catalysts and ensuring product quality.

Industry Stakeholders and buyers should note the market’s emphasis on high-performance, sustainable, and low-cost adsorbents, which are being integrated into diverse applications ranging from air purification to hydrogen liquefaction. Technological advancements are enhancing adsorption efficiency, selectivity, and lifecycle management, making adsorbents a critical component of modern industrial and environmental processes.

Key Insights for Industry Stakeholders:

- Industrial Process Optimization: Advanced adsorbents improve gas and liquid purification and protect downstream catalysts.

- Environmental Compliance: Regulations in Asia and North America are driving demand for adsorbents to remove pollutants like SOx, NOx, mercury, and POPs.

- Innovative Materials: Bio-waste-derived and low-cost adsorbents offer sustainable alternatives to traditional materials.

- Hydrogen Economy: Specialized adsorbents are critical for hydrogen purification and liquefaction plants.

- Digital Integration: IoT-enabled sensors and monitoring systems optimize adsorption-based processes.

Market Analysis: Recent Developments in Adsorbents

The adsorbents market has experienced significant technological and strategic developments over 2024–2025. In August 2025, RSE and Siemens signed a Memorandum of Understanding to integrate digital, AI, and automation technologies into modular water treatment systems, signaling cross-industry adoption of smart adsorption processes. Similarly, in July 2025, Halliburton launched its LOGIX™ automated geosteering service, demonstrating how digital advancements are coupled with adsorbent-based fluids for optimized drilling and process control.

In May 2025, BASF partnered with Plug Power to integrate its Purivate™ Pd15 DeOxo catalysts and Sorbead® Air adsorbents into hydrogen liquefaction plants, highlighting the market’s growing role in the clean energy transition. October 2024 marked Clariant AG’s acquisition of BASF’s U.S. Attapulgite assets, strengthening its position in purifying edible oils and renewable fuels. The same month, Adsorbi AB, a Swedish startup, introduced a cellulose-based air purification material derived from renewable sources, reflecting a trend toward sustainable adsorbents.

Additional cross-industry advancements include ABB’s IoT-enabled flowmeters (August 2024) for real-time adsorption monitoring and DuPont’s new membrane technology (January 2024) for PFAS removal, which leverages durable and fouling-resistant materials. These developments underscore the sector’s focus on sustainability, efficiency, and the integration of digital technologies for enhanced process control.

Key Trends Shaping the Global Adsorbents Industry

Rise of Sustainable and Bio-Based Adsorbents

The adsorbents market is witnessing a strong shift toward sustainable and bio-based materials, driven by environmental concerns and the circular economy. Academic studies highlight innovative use of agricultural waste, such as mango and banana peels, to create biosorbents capable of removing heavy metals like lead from industrial wastewater, with removal rates exceeding 90%. Government initiatives, such as the European Union Circular Economy Action Plan, are also promoting the adoption of renewable and eco-friendly adsorbents. This trend is pushing companies to invest in R&D for sustainable adsorbents, offering an environmentally responsible alternative to conventional materials like activated carbon while supporting waste valorization and resource efficiency.

Advancements in Nanotechnology for High-Performance Adsorbents

Nanotechnology is revolutionizing the adsorbents market by enabling materials with enhanced surface area, chemical specificity, and adsorption capacity. Graphene-based materials and metal-organic frameworks (MOFs) are being used for targeted removal of pollutants, including heavy metals, dyes, and pharmaceuticals. Research on Covalent Organic Framework (COF)-coated zeolites demonstrates CO2 uptake of 132 cc/g at 1 bar and 293K, significantly outperforming traditional zeolites. These innovations highlight a growing focus on high-performance adsorbents for precision separation, gas capture, and industrial purification applications, addressing both environmental and industrial performance demands.

Integration of Digital Technology for Adsorbent Optimization

Industry leaders are leveraging digital technologies, AI, and machine learning to optimize adsorbent performance and process efficiency. For instance, Reliance Industries has developed an adsorption-based CO2 capture process integrating an energy-efficient circulating fluidized bed, combining high mechanical strength with superior adsorption capacity. Academic reviews note that AI can predict adsorbent behavior under varying conditions, which is particularly useful for wastewater treatment and industrial processes where pollutant levels fluctuate. This digital integration allows companies to design smarter adsorbents, improve operational efficiency, and reduce environmental footprint, positioning the industry toward data-driven, high-precision solutions.

Emerging Opportunities in Adsorbents Market

The adsorbents market offers significant opportunities across environmental, industrial, and technological applications. The increasing demand for water treatment, gas purification, and CO2 capture is fueling investments in high-performance and bio-based adsorbents. Emerging nanomaterials like MOFs, COFs, and graphene derivatives provide the potential for customized, highly selective adsorption solutions, while digital process optimization opens avenues for AI-assisted adsorbent design and predictive maintenance. Companies that combine sustainability, performance, and digital intelligence are well-positioned to capitalize on the growing market for eco-friendly and efficient adsorbents across multiple industrial sectors.

Market Share Insights of Adsorbents Market

Market Share by Product Type: Activated Carbon Leads, Specialty Materials Grow

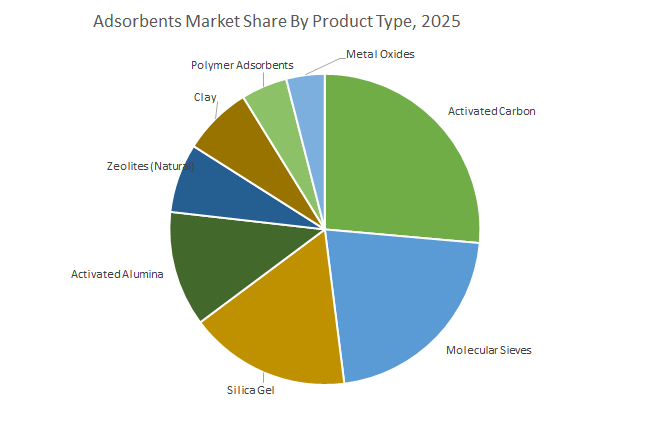

Activated carbon (26.9%) continues to dominate due to its extensive use in water and wastewater treatment, air purification, and food & beverage processing. Molecular sieves (22.5%) hold a high-value position in gas refining, air separation, and petroleum processing, providing precise molecular separation. Silica gel (16.9%) and activated alumina (11.8%) are key volume drivers for moisture control and drying applications, while zeolites, clay, polymer adsorbents, and metal oxides serve niche industrial roles requiring specialized adsorption performance. The segment highlights the balance between high-volume, cost-effective adsorbents and high-value, technically advanced materials.

Market Share by Application: Petroleum Refining Leads, Water Treatment Expands Rapidly

Petroleum refining (22.5%) remains the largest application, essential for fluid catalytic cracking, sulfur removal, and process purification. Chemicals/petrochemicals (16.9%) rely on adsorbents for drying and purifying process streams, while water treatment (16.9%) is the fastest-growing segment, driven by water scarcity and stricter environmental regulations. Gas refining (11.8%) and air separation & drying (11.8%) are crucial for natural gas and industrial gas purification, ensuring compliance with pipeline and process specifications. Smaller but consistent markets include packaging and food & beverage, pharmaceuticals, where adsorbents maintain product quality, shelf-life, and safety. This distribution demonstrates the dual focus on traditional industrial applications and emerging environmental demands, reflecting the evolving market landscape.

Strong U.S. Regulatory Push and Corporate Expansions Driving Adsorbents Adoption

The United States adsorbents market is experiencing significant momentum due to regulatory pressure and large-scale infrastructure funding. The U.S. Environmental Protection Agency (EPA) has enforced stringent air and water quality standards, with the latest legally binding drinking water standards covering six PFAS compounds acting as a major catalyst for the use of advanced adsorbents. These regulations are not only driving municipal water utilities to adopt high-performance filtration systems but also compelling industrial operators to invest in emission control technologies. Further strengthening the market, the Bipartisan Infrastructure Law allocates billions of dollars toward upgrading U.S. water infrastructure, opening vast opportunities for adsorbent-based treatment systems in both municipal and industrial applications. Technological innovation also remains at the forefront Georgia Tech’s February 2025 breakthrough in applying machine learning to identify membrane materials capable of blocking 95% of PFAS within days highlights the U.S. focus on data-driven, rapid-deployment purification solutions. Moreover, corporate consolidation is shaping the competitive landscape, as seen in Hawkins’ April 2025 acquisition of WaterSurplus to expand its advanced filtration portfolio, positioning U.S.-based players as leaders in environmental remediation.

China’s Environmental Regulations and R&D Investments Accelerating Adsorbents Demand

China has emerged as one of the most dynamic markets for adsorbents, with government policies strongly aligned toward environmental protection. Under the 14th Five-Year Plan, China has prioritized stricter air and water quality regulations, compelling industries to adopt high-performance adsorbent technologies for emission control and pollution treatment. Alongside regulatory measures, the country is heavily investing in R&D to produce cost-efficient and energy-saving adsorbents, particularly for advanced applications such as gas separation, catalysis, and industrial wastewater treatment. The petrochemical and refining sectors, which remain critical to China’s industrial backbone, represent key demand drivers as rapid industrialization continues to exacerbate environmental challenges. Corporate strategies are also expanding beyond borders, exemplified by JALON’s completion of its first overseas production base in Thailand in 2021, which strengthens its molecular sieve production for global distribution. With environmental concerns mounting and government mandates tightening, China’s adsorbents market is set for rapid expansion powered by both domestic demand and international growth ambitions.

India’s Urbanization, Infrastructure Growth, and Healthcare Needs Fueling Adsorbents Market

India’s adsorbents market is strongly driven by government-led environmental initiatives, industrial growth, and urgent healthcare requirements. The government has prioritized improving air and water quality, supported by initiatives to boost domestic manufacturing and infrastructure development. A pivotal example came in June 2021 when Honeywell International partnered with India’s DRDO and CSIR-IIP to supply molecular sieve adsorbents for oxygen plants during the pandemic, highlighting the critical role of adsorbents in healthcare and medical oxygen generation. Beyond healthcare, India is investing heavily in refineries and petrochemical complexes, industries that rely on adsorbents for separation and purification processes. With rapid urbanization creating demand for clean air and safe drinking water, the adoption of advanced adsorbent systems across municipal utilities and industries is growing steadily. This dual demand from healthcare and infrastructure positions India as a key growth market for adsorbents in Asia-Pacific.

Germany’s Stricter EU Directives and Corporate Innovations Boosting Adsorbents Market

Germany is at the forefront of Europe’s adsorbents market, with regulations and innovation serving as the twin pillars of growth. The EU’s revised Urban Wastewater Treatment Directive, implemented in January 2025, mandates stricter removal of a wide variety of pollutants, pushing German wastewater treatment plants toward adopting advanced adsorbent-based technologies. Corporate innovation further accelerates the market, with BASF SE’s launch of its PuriCycle portfolio in 2022, offering new catalysts and adsorbents designed for chemical recycling by purifying pyrolysis oils. German research institutions and corporations are also advancing solutions for the removal of micro-pollutants such as PFAS and pharmaceutical residues from water, demonstrating the country’s leadership in applied research. The primary market drivers remain compliance with stringent EU environmental regulations and rising public demand for clean water, ensuring the adoption of adsorbent-based purification systems across both municipal and industrial segments.

Japan’s PFAS Ban and Technological Advancements Creating High Market Potential

Japan’s adsorbents market is being reshaped by recent regulatory shifts and pioneering scientific advancements. In January 2025, the Japanese government introduced a ministerial ordinance under the Chemical Substances Control Law (CSCL) that banned the manufacture, import, and use of 138 PFAS compounds. This decisive move has created an immediate surge in demand for advanced adsorbents in environmental remediation and water treatment. Japanese research institutions, particularly the Institute of Science Tokyo, are spearheading technological breakthroughs, including the development of a membrane distillation system and carbon-based adsorbents capable of removing PFAS with higher energy efficiency and sustainability. The combination of regulatory urgency and innovation-driven solutions makes Japan a pivotal market for next-generation adsorbents, with strong prospects in municipal water utilities, industrial sectors, and environmental restoration projects.

United Kingdom’s Infrastructure Modernization and Circular Economy Approach Supporting Adsorbents Market

The United Kingdom’s adsorbents market is being shaped by regulatory infrastructure reforms and an emphasis on circular economy principles. The implementation of AMP 8 requires water utilities to upgrade systems to reduce environmental risks and safeguard water quality, creating demand for adsorbent-based treatment technologies. In parallel, digital transformation is being integrated into water management, as highlighted by Siemens’ 2024 launch of Water Quality Analytics as a Service (WQAaaS), which provides utilities with real-time data to optimize adsorbent use in treatment plants. On the innovation front, UK companies are increasingly focusing on technologies that regenerate and reuse adsorbents, aligning with the country’s sustainability and resource efficiency goals. The key drivers for the UK market include modernizing aging infrastructure, improving service resilience, and adopting circular approaches that make adsorbent technologies more sustainable and cost-effective for long-term applications.

Competitive Landscape of Adsorbents Market

The global adsorbents market is highly competitive, with key players leveraging innovative materials, strategic partnerships, and digital integration to provide high-performance solutions. Companies differentiate themselves through customized solutions, sustainability initiatives, and global operational reach, ensuring they meet the evolving demands of industrial, environmental, and energy sectors.

BASF SE drives innovation with advanced adsorbent solutions

BASF offers a wide portfolio of adsorbents, including activated alumina, zeolites (molecular sieves), and Sorbead® desiccants. In May 2025, BASF partnered with Plug Power for hydrogen liquefaction applications, while the PuriCycle™ portfolio launched in July 2022 focuses on selective contaminant removal in pyrolysis oils. BASF’s deep R&D capabilities position it as a market leader in high-performance adsorbents.

Calgon Carbon Corporation specializes in granular activated carbon

Calgon Carbon, a Kuraray subsidiary, excels in granular activated carbon (GAC) and end-to-end service solutions. Its FILTERSORB® GAC effectively removes PFAS and other contaminants. The company integrates supply, on-site equipment, and spent carbon reactivation, providing a closed-loop system that enhances operational efficiency and environmental compliance.

Clariant AG strengthens technological leadership with sustainable adsorbents

Clariant leverages specialty clays and activated bleaching earths for purification in edible oils and renewable fuels. The October 2024 acquisition of BASF’s U.S. Attapulgite business expanded its technological capabilities. Products like Tonsil® RNF support sustainable fuels, aligning Clariant with the global clean energy transition.

W. R. Grace & Co. focuses on high-purity adsorbents for demanding applications

Grace provides silica gels and molecular sieves for gas purification, moisture removal, and chromatography. Investments in 2024 enhanced high-purity silica gel and chromatographic media production, catering to pharmaceutical and food industries where precision and purity are critical.

Arkema S.A. innovates with energy-efficient molecular sieves

Arkema delivers molecular sieves for air separation, natural gas treatment, and petroleum refining, focusing on energy-efficient solutions for cryogenic processes. The company emphasizes sustainability, environmental protection, and optimization of gas separation and purification operations.

Purolite International Limited offers polymeric adsorbents with global integration

Purolite, now part of Ecolab, provides polymeric and functionalized resins for water purification, pharmaceuticals, and chemical processing. The 2023 acquisition by Ecolab enhances integration with broader water and hygiene services, offering end-to-end solutions for high-purity applications.

Adsorbents Market Report Scope

Adsorbents Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.2 Billion

|

|

Market Size (2034)

|

$8.6 Billion

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Product Type (Molecular Sieves, Activated Carbon, Silica Gel, Activated Alumina, Clay, Metal Oxides, Polymer Adsorbents, Zeolites), By Application (Petroleum Refining, Chemicals/Petrochemicals, Gas Refining, Water Treatment, Air Separation & Drying, Packaging, Industrial, Other Applications)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Clariant AG, Cabot Corporation, W. R. Grace & Co., Calgon Carbon Corporation (A Subsidiary of Kuraray Co., Ltd.), Honeywell International Inc., Zeochem L.L.C., Arkema S.A., The Dow Chemical Company, Mitsubishi Chemical Group, Axens Group, ICL Group Ltd., DuPont de Nemours, Inc., Sorbead India, Zirax Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Adsorbents Market Segmentation

By Product Type

- Molecular Sieves

- Activated Carbon

- Silica Gel

- Activated Alumina

- Clay

- Metal Oxides

- Polymer Adsorbents

- Zeolites

By Application

- Petroleum Refining

- Chemicals/Petrochemicals

- Gas Refining

- Water Treatment

- Air Separation & Drying

- Packaging

- Industrial

- Other Applications

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Adsorbents Industry include-

- BASF SE

- Clariant AG

- Cabot Corporation

- W. R. Grace & Co.

- Calgon Carbon Corporation (A Subsidiary of Kuraray Co., Ltd.)

- Honeywell International Inc.

- Zeochem L.L.C.

- Arkema S.A.

- The Dow Chemical Company

- Mitsubishi Chemical Group

- Axens Group

- ICL Group Ltd.

- DuPont de Nemours, Inc.

- Sorbead India

- Zirax Limited

*- List not Exhaustive

Research Coverage

The Adsorbents Market Report by USDAnalytics this report investigates how next-gen materials and digital controls are reshaping separations in refining, chemicals, water, and clean-energy value chains; it highlights breakthroughs in MOFs/COFs, bio-derived sorbents, and high-capacity sieves that lift selectivity while lowering lifecycle costs; delivers analysis reviews of adoption barriers, supply security, regeneration strategies, and hydrogen-readiness; and benchmarks performance under real-world contaminants, temperatures, and cycle loads, linking media choice to throughput, catalyst protection, and emissions reduction. By unifying techno-economics with case-evidence from utilities, refineries, and gas processors, this report is an essential resource for operations leaders, process engineers, procurement teams, and ESG stewards planning scalable, compliant adsorption systems through 2034. Scope Includes-

- Segmentation: By product type (molecular sieves, activated carbon, silica gel, activated alumina, clay, metal oxides, polymer adsorbents, zeolites); application (petroleum refining; chemicals/petrochemicals; gas refining; water treatment; air separation & drying; packaging; industrial; other).

- Geographic Scope: “Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.”

- Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies (Profiles of 15+ companies): BASF SE; Clariant AG; Cabot Corporation; W. R. Grace & Co.; Calgon Carbon Corporation (Kuraray); Honeywell International Inc.; Zeochem L.L.C.; Arkema S.A.; The Dow Chemical Company; Mitsubishi Chemical Group; Axens Group; ICL Group Ltd.; DuPont de Nemours, Inc.; Sorbead India; Zirax Limited

Methodology

USDAnalytics triangulates bottom-up shipment and installed-base modeling (by media type, pore class, particle size, and end-use) with top-down spend from public company filings, customs flows, and EPC awards. Primary research spans structured interviews with plant managers, turnaround contractors, catalyst vendors, and OEM skids teams, complemented by pilot logs (breakthrough curves, EBCT, pressure drop), regeneration/React/replace records, and verified OPEX (energy, steam, chemicals, waste). A multi-factor scoring model ranks materials by capacity, selectivity, fouling resistance, regenerability, safety, and supply risk; scenarios incorporate policy tightening, hydrogen ramp-up, and bio-feed penetration. Forecasts (2025–2034) use sensitivity bands for price/availability of key precursors (e.g., alumina, activated carbon, zeolitic powders) and adoption of digital monitoring (IoT/AI) that extends bed life and reduces unplanned downtime.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Adsorbents Market

1. Executive Summary

1.1. Market Highlights & Key Projections

1.2. Global Market Snapshot

1.3. Key Findings

2. Adsorbents Market Overview (2025–2034)

2.1. Introduction

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $5.2 Billion

2.2.2. Forecasted Market Size (2034): $8.6 Billion

2.2.3. Projected Compound Annual Growth Rate (CAGR): 5.7%

2.3. Market Drivers and Challenges

2.3.1. Drivers: Industrial Optimization, Environmental Compliance, and the Hydrogen Economy

2.3.2. Challenges: Raw Material Volatility and High Manufacturing Costs

2.4. Key Insights for Industry Stakeholders

3. Key Market Trends and Recent Developments

3.1. Rise of Sustainable and Bio-Based Adsorbents

3.2. Advancements in Nanotechnology for High-Performance Adsorbents

3.3. Integration of Digital Technology for Adsorbent Optimization

3.4. Recent Developments & Strategic Moves (2024–2025)

3.4.1. Corporate Mergers and Partnerships

3.4.2. Technology and Product Launches

4. Adsorbents Market – Segmentation Insights

4.1. By Product Type

4.1.1. Activated Carbon (26.9% Market Share)

4.1.2. Molecular Sieves (22.5% Market Share)

4.1.3. Silica Gel (16.9% Market Share)

4.1.4. Activated Alumina (11.8% Market Share)

4.1.5. Zeolites

4.1.6. Clay

4.1.7. Polymer Adsorbents

4.1.8. Metal Oxides

4.2. By Application

4.2.1. Petroleum Refining (22.5% Market Share)

4.2.2. Chemicals/Petrochemicals (16.9% Market Share)

4.2.3. Water Treatment (16.9% Market Share)

4.2.4. Gas Refining (11.8% Market Share)

4.2.5. Air Separation & Drying (11.8% Market Share)

4.2.6. Packaging

4.2.7. Industrial

4.2.8. Other Applications

5. Country Analysis and Outlook: Adsorbents Market

5.1. United States: Regulatory Push and Corporate Expansions

5.2. China: Environmental Regulations and R&D Investments

5.3. India: Urbanization, Infrastructure, and Healthcare Needs

5.4. Germany: EU Directives and Corporate Innovations

5.5. Japan: PFAS Ban and Technological Advancements

5.6. United Kingdom: Infrastructure Modernization and Circular Economy Approach

6. Adsorbents Market Size Outlook by Region (2025–2034)

6.1. North America Adsorbents Market Size Outlook to 2034

6.1.1. By Product Type

6.1.2. By Application

6.1.3. By Country (US, Canada, Mexico)

6.2. Europe Adsorbents Market Size Outlook to 2034

6.2.1. By Product Type

6.2.2. By Application

6.2.3. By Country (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

6.3. Asia Pacific Adsorbents Market Size Outlook to 2034

6.3.1. By Product Type

6.3.2. By Application

6.3.3. By Country (China, India, Japan, South Korea, Australia, Rest of Asia)

6.4. South America Adsorbents Market Size Outlook to 2034

6.4.1. By Product Type

6.4.2. By Application

6.4.3. By Country (Brazil, Argentina, Rest of South America)

6.5. Middle East and Africa Adsorbents Market Size Outlook to 2034

6.5.1. By Product Type

6.5.2. By Application

6.5.3. By Country (Saudi Arabia, UAE, South Africa, Egypt, Rest of MEA)

7. Competitive Landscape: Key Companies

7.1. BASF SE

7.1.1. Company Overview

7.1.2. Advanced Adsorbent Solutions

7.2. Calgon Carbon Corporation (A Subsidiary of Kuraray Co., Ltd.)

7.2.1. Company Overview

7.2.2. Granular Activated Carbon Solutions

7.3. Clariant AG

7.4. W. R. Grace & Co.

7.5. Arkema S.A.

7.6. Purolite International Limited

7.7. Other Prominent Companies

7.7.1. Cabot Corporation

7.7.2. Honeywell International Inc.

7.7.3. Zeochem L.L.C.

7.7.4. Axens Group

8. Methodology

8.1. Research Scope

8.2. Market Research Approach

8.3. Data Sources and Validation

8.4. Assumptions and Limitations

9. Appendix

9.1. Acronyms and Abbreviations

9.2. List of Tables

9.3. List of Figures