Global Leachate Treatment Systems Market Overview: Growth Outlook to 2034

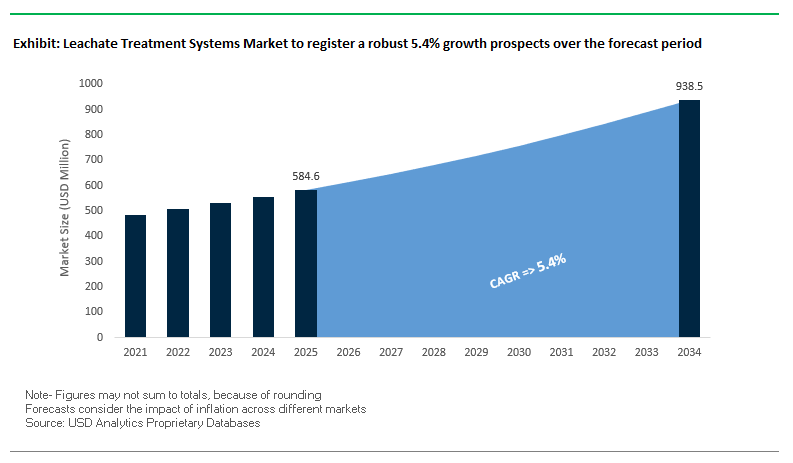

The global leachate treatment systems market is projected to expand from USD 584.6 billion in 2025 to USD 938.5 billion by 2034, registering a steady CAGR of 5.4%. Leachate, the highly polluted liquid generated from landfill waste decomposition, represents one of the most complex wastewater challenges, containing organic matter, ammonia, salts, micropollutants, and heavy metals. As environmental regulations tighten and urbanization accelerates, the demand for effective treatment systems has become a global priority.

The market’s momentum is also shaped by sustainability initiatives, with landfill operators under pressure to reduce off-site disposal and increase on-site treatment capacity. Meanwhile, water-stressed regions such as Asia-Pacific are adopting advanced methods like reverse osmosis, membrane bioreactors, and minimal liquid discharge (MLD) to achieve water reuse and regulatory compliance.

Key Insights for Industry Stakeholders:

- More than 15,000 landfill sites globally generate leachate requiring treatment; 40% already rely on on-site treatment technologies.

- In the U.S., 72% of municipal landfills still use off-site disposal, but state-level regulations are accelerating the shift to localized treatment.

- In Europe, biological nitrification dominates, but stricter discharge standards are pushing adoption of reverse osmosis and advanced oxidation.

- Asia-Pacific is emerging as the fastest-growing market, supported by large-scale government investments in waste management and landfill infrastructure.

Market Analysis: Recent Developments and Industry Dynamics

The leachate treatment systems industry is evolving rapidly, with innovations in membranes, energy-positive systems, and circular water reuse shaping its trajectory. Strategic acquisitions and regulatory reforms are also redefining market dynamics, signaling a shift from compliance-driven investments to long-term sustainability-driven strategies.

In August 2025, DuPont Water Solutions received recognition at the BIG Sustainability Awards for advancements in wastewater reuse and MLD technologies increasingly critical for landfill leachate. The following month, July 2025, Veolia Water Technologies was chosen to equip France’s largest wastewater reuse project in Argelès-sur-Mer, delivering treated water for agriculture, a model for reusing leachate-derived water. In May 2025, Veolia further strengthened its global position by acquiring full ownership of its Water Technologies and Solutions subsidiary, consolidating capabilities in complex effluent treatment. A month earlier, in April 2025, Kurita Water Industries showcased microbial fuel cell technology that generated electricity from wastewater, highlighting a path toward energy-positive landfill treatment.

Policy frameworks are exerting significant influence. In March 2025, the EU’s Urban Wastewater Treatment Directive took effect, requiring pharmaceutical and cosmetic firms to fund the removal of micropollutants, including those in landfill leachate. On the innovation front, January 2025 saw a nanofiber membrane breakthrough for arsenic and lead removal, while December 2024 research confirmed the role of engineered nanoparticles in cost-efficient produced water treatment. In October 2024, China’s Da Tang Industrial Park MLD plant began operations, processing 160,000 m³/day, showcasing scalable solutions that could be replicated in landfill leachate management.

Key Market Trends Shaping Leachate Treatment

Stricter Regulations Driving Advanced Treatment Requirements

Regulatory pressure is a key growth driver for the leachate treatment systems market. The U.S. EPA’s Preliminary Plan #16 (2024) emphasizes the revision of landfill effluent guidelines to address emerging pollutants such as PFAS. In India, the CPCB’s Solid Waste Management Rules mandate proper leachate collection, treatment, and recirculation, ensuring compliance and protecting local water resources. These regulations are pushing landfill operators and municipal authorities to adopt sophisticated treatment systems that go beyond basic containment, driving demand for advanced technologies.

Adoption of Hybrid and Multi-Stage Treatment Technologies

Single-stage treatment is no longer sufficient for the complex composition of modern landfill leachate. Multi-stage treatment trains combining physical-chemical pre-treatment, biological enhancement, and advanced membrane-based systems like Membrane Bioreactors (MBR) and Disc Tube Reverse Osmosis (DTRO) are becoming standard. A case study from Istanbul, Turkey, demonstrated that combining pre-anoxic biological treatment with ultrafiltration (UF) and nanofiltration (NF) achieved 99% removal of both COD and ammonia nitrogen. Such integrated approaches are increasingly recognized as essential for ensuring compliance with stringent effluent standards.

Strategic Focus on Resource Recovery and Energy Generation

Leachate is now seen not only as waste but also as a potential resource. Academic studies highlight the recovery of nitrogen, phosphorus, humic substances, and bioenergy (methane) from leachate streams. Companies like Xylem are developing modular systems capable of flexible resource recovery, including metals and nutrients, demonstrating a clear shift toward a circular economy. This trend turns environmental compliance into a revenue-generating opportunity, incentivizing investment in advanced, customizable treatment technologies.

Leachate Treatment Systems Market Share Insights

By Technology: Membrane Systems Lead, Hybrid Approaches Grow

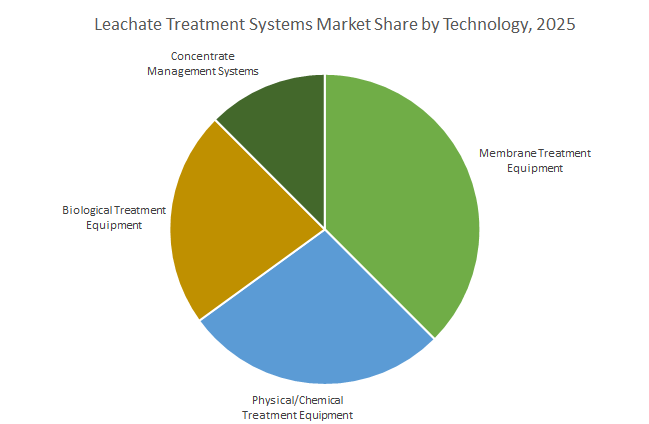

Membrane Treatment Equipment (38%) dominates the market due to its superior performance in removing salts, heavy metals, and persistent organic pollutants. Physical/Chemical Treatment Equipment (26.9%) remains essential as a pre-treatment step to protect downstream systems and enhance overall efficiency. Biological Treatment Equipment (24.6%) is widely used for young leachate with high BOD but is less effective for mature landfill streams. Concentrate Management Systems (11.8%) address the energy-intensive handling of toxic brine from RO systems, highlighting the cost challenges associated with high-purity water production. The market’s technology mix underscores the balance between regulatory compliance, operational efficiency, and long-term sustainability.

By System Configuration: On-Site Systems Dominate

On-Site Treatment Systems (68%) account for the majority of the market, benefiting from economies of scale and the ability to continuously treat large leachate volumes directly at landfill sites. Off-Site Treatment (24.6%) serves smaller landfills, leveraging centralized wastewater treatment facilities to reduce capital expenditure. Mobile & Containerized Systems provide flexible, temporary solutions suitable for pilot testing, emergency response, or closed landfills with diminishing volumes. The configuration mix reflects the logistical and economic considerations of landfill operators alongside the growing demand for scalable and agile solutions.

By Landfill Phase & Leachate Characteristics: Active vs. Mature Landfills

Leachate from Active Landfills (55–60%) contains high biodegradable organic content and emerging contaminants, necessitating robust, continuous treatment systems. Closed or Mature Landfills (44.1%) produce highly concentrated, low-BOD leachate with elevated ammonia and salts, requiring advanced physico-chemical and membrane-based technologies. This split highlights distinct technological requirements across landfill phases and reinforces the long-term market potential driven by post-closure liability and regulatory mandates, ensuring stable demand for operational, maintenance, and upgrade services.

United States: PFAS Regulations and Advanced Leachate Treatment Technologies

In the United States, the leachate treatment systems market is strongly influenced by regulatory policies and government funding. The U.S. Environmental Protection Agency (EPA) enforces long-standing landfill wastewater regulations under 40 CFR Part 445 and is actively developing new effluent guidelines for per- and polyfluoroalkyl substances (PFAS) discharges. This regulatory focus is driving investment in advanced treatment technologies. Under the Bipartisan Infrastructure Law (BIL), over $50 billion is allocated to improve water infrastructure, with a significant portion directed toward decentralized systems capable of handling emerging contaminants like PFAS. Technological advancements in 2024, such as new systems for treating highly mineralized produced water in the Appalachian Basin, have applicability for landfill leachate treatment. Leading companies like Xylem Inc. offer biological, contaminant, and metals removal systems, including mobile and field-erected units for rapid deployment, addressing the increasing demand for efficient leachate management.

China: Government Investment and Forward Osmosis Innovations Enhancing Landfill Leachate Management

China’s leachate treatment systems market is driven by stringent regulations, substantial government investment, and technological innovation. The Ministry of Ecology and Environment (MEE) enforces strict landfill leachate discharge standards, aligned with the 14th Five-Year Plan, targeting 95% wastewater treatment for county-level cities. Researchers from the Chinese Academy of Sciences developed dual-functional reverse osmosis (RO) membranes with antibacterial and anti-adhesion properties, improving heavy metal and contaminant removal efficiency. Corporate initiatives are also notable, with Danish company Aquaporin executing a pilot project using containerized forward osmosis (FO) technology to reduce leachate volume and produce clean water for discharge or reuse. The Chinese government plans to invest $50 billion in wastewater treatment by 2025, supporting large-scale projects that include landfill management and industrial leachate treatment applications.

Germany: EU Directives and Digital Solutions Driving High-Efficiency Leachate Treatment

Germany’s leachate treatment systems market is influenced by EU regulatory frameworks, advanced technology adoption, and corporate innovations. The revised Urban Wastewater Treatment Directive (January 2025) mandates the "4th purification stage" to eliminate micropollutants, encouraging advanced oxidation processes and membrane filtration in leachate treatment. German cities are leveraging AI, digital twins, and advanced monitoring systems to optimize water management, as noted by the Federal Environment Agency (UBA). Key industry players, including H2O GmbH and GEA Group AG, are developing sustainable solutions within ZLD systems for industrial wastewater management, enhancing the efficiency of heavy metal and contaminant removal in landfill leachate.

Australia: Environmental Stewardship and Virtual Curtain Technology in Leachate Treatment

Australia’s leachate treatment systems market is shaped by rigorous environmental policies, innovative technologies, and the country’s extensive mining sector. State environment protection policies, such as SEPP Waters of Victoria, ensure water quality and environmental stewardship. The Commonwealth Scientific and Industrial Research Organisation (CSIRO) developed the "Virtual Curtain" technology, which removes metal contaminants while producing minimal sludge compared to conventional methods. This advancement is significant for landfill leachate treatment, particularly in mining regions. The market is driven by the need for perpetual water treatment solutions to support mine closure and sustainable operations, emphasizing long-term environmental protection.

India: ZLD Mandates and Large-Scale Industrial Leachate Projects Driving Market Adoption

India’s leachate treatment systems market is propelled by regulatory mandates, government initiatives, and corporate expertise. The Central Pollution Control Board (CPCB) and National Green Tribunal (NGT) require Zero Liquid Discharge (ZLD) in water-scarce industrial areas, including landfills. Government programs like the "Jal Jeevan Mission" and "Namami Gange Mission" are accelerating wastewater treatment adoption across urban and rural areas. Companies such as VA Tech Wabag and Xylem Inc. provide large-scale leachate treatment solutions, addressing complex industrial wastewater streams from chemicals, pharmaceuticals, and other regulated products. The market is increasingly focusing on recovery and reuse of valuable metals from industrial and landfill waste streams.

Japan: MBR and Membrane Technology Innovations Enhancing Industrial Leachate Treatment

Japan’s leachate treatment systems market is driven by government initiatives, academic R&D, and technological advancements. The MLIT’s "Advance of Japan Ultimate Membrane bioreactor technology Project (A-JUMP)" promotes widespread adoption of MBR technology for industrial wastewater treatment. Toray Industries Inc. continues to lead in advanced membrane modules, offering high-efficiency separation that doubles filtration performance while reducing clogging. Key applications include nutrient recovery, water reuse, and electrochemical and adsorption methods for heavy metal removal from leachate. Japan’s industrial sector plays a critical role in adopting these advanced systems, reinforcing the country’s position as a leader in efficient landfill and industrial leachate treatment solutions.

Competitive Landscape: Key Companies Shaping the Leachate Treatment Systems Market

The competitive landscape is defined by multinational conglomerates, advanced membrane specialists, and integrated solution providers. Companies are focusing on technology differentiation, geographic expansion, and sustainability-driven strategies to secure market leadership.

Veolia Water Technologies – Integrated Solutions for Complex Leachate Streams

Veolia remains a global leader in ecological transformation, offering biological, membrane, and thermal treatment systems tailored for landfill and industrial leachate. Its May 2025 acquisition of Water Technologies and Solutions strengthens its portfolio, enabling more efficient and sustainable service delivery. Through its GreenUp strategy, Veolia focuses on reducing environmental impact while optimizing resource reuse, making it a preferred partner for governments and landfill operators seeking regulatory compliance and climate resilience.

SUEZ Water Technologies & Solutions – High-Performance ZLD and Digital Integration

SUEZ delivers customized leachate treatment solutions, with a strong foothold in Asia through contracts targeting 100% wastewater recycling. Its expertise lies in biological systems, advanced membranes, and oxidation processes that address the toughest effluents. Beyond hardware, SUEZ deploys predictive analytics and digital platforms to improve operational efficiency, reduce fouling, and optimize chemical usage. This dual approach technological and digital positions it as a frontrunner in resource recovery-oriented landfill operations.

Xylem Inc. – Full Water Cycle Solutions Strengthened by Evoqua Acquisition

Xylem’s 2023 acquisition of Evoqua created a global powerhouse in wastewater treatment, offering pumps, MBRs, advanced oxidation, and monitoring systems. Its comprehensive portfolio addresses the entire water cycle, including landfill leachate, mine effluent, and industrial wastewater. Xylem is heavily investing in digital and IoT-enabled platforms for real-time system monitoring, enabling predictive maintenance and compliance assurance for landfill operators worldwide.

Evoqua Water Technologies – North American Specialist in Mission-Critical Wastewater

Now part of Xylem, Evoqua retains its strong North American presence with 200,000 installations worldwide and more than 38,000 customers. Its solutions span industrial process water, PFAS treatment, and leachate management, supported by a new Sustainability and Innovation Hub in Pittsburgh. Evoqua’s integration into Xylem enhances its ability to deliver comprehensive landfill leachate treatment, combining expertise in filtration, disinfection, and contaminant removal.

DuPont Water Solutions – Membrane Innovation for Advanced Leachate Treatment

DuPont’s FilmTec™ membranes are a global standard in RO and nanofiltration, widely adopted for landfill leachate and high-salinity wastewater. In 2025, it won an R&D 100 Award for its Fortilife™ XC160 Membrane, designed for concentrating high-salinity wastewater and supporting ZLD. Its broader portfolio, including NF, UF, and ion exchange resins, provides integrated solutions for the most complex treatment scenarios. DuPont’s commitment to water circularity and sustainability has established it as a trusted global partner, helping purify over 50 million gallons of water per minute across 112 countries.

Leachate Treatment Systems Market Report Scope

Leachate Treatment Systems Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$584.6 Million

|

|

Market Size (2034)

|

$938.5 Million

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Technology (Biological Treatment Equipment, Physical/Chemical Treatment Equipment, Membrane Treatment Equipment, Concentrate Management Systems), By System Configuration (On-Site, Off-Site Treatment, Mobile & Containerized Treatment), By Landfill Phase & Leachate Characteristics (Active Landfill, Closed/Mature Landfill), By Disposal (Discharge to Surface Water, Discharge to Sewer, Recirculation back into Landfill), By Application (Municipal Landfills, Industrial Landfills, Mining Waste Leachate, Agricultural Waste Sites)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia, SUEZ, Xylem Inc., Evoqua Water Technologies, DuPont de Nemours, Inc., Pentair plc, Toray Industries, Inc., Aquatech International, Kubota Corporation, The Dow Chemical Company, V.A. TECH WABAG Ltd., Mitsubishi Chemical Corporation, Kurita Water Industries Ltd., H2O GmbH, Thermax Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Leachate Treatment Systems Market Segmentation

By Technology

- Biological Treatment Equipment

- Physical/Chemical Treatment Equipment

- Membrane Treatment Equipment

- Concentrate Management Systems

By System Configuration

- On-Site

- Off-Site Treatment

- Mobile & Containerized Treatment

By Landfill Phase & Leachate Characteristics

- Active Landfill

- Closed/Mature Landfill

By Disposal

- Discharge to Surface Water

- Discharge to Sewer

- Recirculation back into Landfill

By Application

- Municipal Landfills

- Industrial Landfills

- Mining Waste Leachate

- Agricultural Waste Sites

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Leachate Treatment Systems Industry include-

- Veolia

- SUEZ

- Xylem Inc.

- Evoqua Water Technologies

- DuPont de Nemours, Inc.

- Pentair plc

- Toray Industries, Inc.

- Aquatech International

- Kubota Corporation

- The Dow Chemical Company

- V.A. TECH WABAG Ltd.

- Mitsubishi Chemical Corporation

- Kurita Water Industries Ltd.

- H2O GmbH

- Thermax Limited

*- List not Exhaustive

Research Coverage

This report investigates the Leachate Treatment Systems Market end-to-end from regulatory catalysts and influent chemistry to deployable treatment trains and lifecycle economics. Compiled by USDAnalytics, it highlights breakthroughs in disc-tube RO (DTRO), high-rejection NF/RO, advanced oxidation, membrane bioreactors, and concentrate management that are redefining compliance and reuse. Our analysis reviews performance benchmarks (ammonia removal, salt rejection, PFAS mitigation), TCO/opex levers, and retrofit pathways for active and mature landfills. It maps competitive positioning, partnership activity, and digital O&M models to 2034 this report is an essential resource for landfill operators, EPCs, utilities, and investors planning scalable, regulation-ready solutions. Scope Includes-

- Segmentation

- By Technology: Biological Treatment Equipment; Physical/Chemical Treatment Equipment; Membrane Treatment Equipment; Concentrate Management Systems

- By System Configuration: On-Site; Off-Site Treatment; Mobile & Containerized Treatment

- By Landfill Phase & Leachate Characteristics: Active Landfill; Closed/Mature Landfill

- By Disposal: Discharge to Surface Water; Discharge to Sewer; Recirculation back into Landfill

- By Application: Municipal Landfills; Industrial Landfills; Mining Waste Leachate; Agricultural Waste Sites

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Horizon: Historic data 2021–2024; forecast 2025–2034.

- Companies (15+ profiles/analysis): Veolia; SUEZ; Xylem Inc.; Evoqua Water Technologies; DuPont de Nemours, Inc.; Pentair plc; Toray Industries, Inc.; Aquatech International; Kubota Corporation; The Dow Chemical Company; V.A. TECH WABAG Ltd.; Mitsubishi Chemical Corporation; Kurita Water Industries Ltd.; H2O GmbH; Thermax Limited.

Methodology

USDAnalytics applied a mixed top-down/bottom-up approach: (i) bottom-up plant inventory of 1,000+ landfill assets by flow, age (young vs mature leachate), and process train (bio-nitritation/MBR, phys-chem, DTRO/NF/RO, AOP/UV, brine/MLD); (ii) triangulation with tender databases, vendor RFQs, and 90+ interviews across operators, OEMs, and regulators; (iii) performance normalization for COD/NH₃-N, chloride/TDS, color, micropollutants/PFAS, and heavy metals, capturing energy (kWh·m⁻³), reagent dose, sludge/brine factors, and recovery %. Market sizing aligns with permitting pipelines, waste-to-landfill trends, and capex/opex curves; scenarios stress-test PFAS rules, sewer-surcharge shifts, power pricing, and reuse mandates to 2034, yielding validated market shares and TCO benchmarks for on-site, off-site, and containerized systems.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Leachate Treatment Systems Market

1. Executive Summary

1.1. Market Highlights and Key Projections

1.2. Key Insights for Industry Stakeholders

1.3. Global Market Snapshot

1.3.1. Current Market Valuation (2025): $584.6 Billion

1.3.2. Projected Market Valuation (2034): $938.5 Billion

1.3.3. Compound Annual Growth Rate (CAGR): 5.4%

2. Market Outlook (2025–2034)

2.1. Introduction: Growth, Drivers, and Key Challenges

2.2. Market Valuation and Growth Projections (2025–2034)

2.3. Key Market Trends Shaping Leachate Treatment

2.3.1. Stricter Regulations Driving Advanced Treatment Requirements

2.3.2. Adoption of Hybrid and Multi-Stage Treatment Technologies

2.3.3. Strategic Focus on Resource Recovery and Energy Generation

3. Innovations and Strategic Developments Redefining the Market

3.1. Market Analysis: Recent Developments and Strategic Shifts

3.1.1. DuPont Water Solutions Recognized for MLD Innovations (August 2025)

3.1.2. Veolia Strengthens Global Leadership with Major Acquisition and Contracts (2025)

3.1.3. Kurita's Breakthrough in Energy-Positive Wastewater Treatment (April 2025)

3.1.4. Nanofiber Membranes and Nanoparticles for Advanced Removal (2024-2025)

3.1.5. Policy Shifts: EU’s Revised Urban Wastewater Treatment Directive (January 2025)

4. Competitive Landscape: Leading Players

4.1. Market Overview: Multinational Leaders and Innovative Specialists

4.2. Strategic Profiles of Key Companies

4.2.1. Veolia Water Technologies: Integrated Solutions for Complex Leachate Streams

4.2.2. SUEZ Water Technologies & Solutions: High-Performance ZLD and Digital Integration

4.2.3. Xylem Inc.: Full Water Cycle Solutions Strengthened by Evoqua Acquisition

4.2.4. Evoqua Water Technologies: North American Specialist in Mission-Critical Wastewater

4.2.5. DuPont Water Solutions: Membrane Innovation for Advanced Leachate Treatment

5. Leachate Treatment Systems Market Segmentation Insights

5.1. By Technology

5.1.1. Biological Treatment Equipment

5.1.2. Physical/Chemical Treatment Equipment

5.1.3. Membrane Treatment Equipment

5.1.4. Concentrate Management Systems

5.2. By System Configuration

5.2.1. On-Site Treatment Systems

5.2.2. Off-Site Treatment

5.2.3. Mobile & Containerized Treatment

5.3. By Landfill Phase & Leachate Characteristics

5.3.1. Active Landfill

5.3.2. Closed/Mature Landfill

5.4. By Disposal

5.4.1. Discharge to Surface Water

5.4.2. Discharge to Sewer

5.4.3. Recirculation back into Landfill

5.5. By Application

5.5.1. Municipal Landfills

5.5.2. Industrial Landfills

5.5.3. Mining Waste Leachate

5.5.4. Agricultural Waste Sites

6. Country Analysis and Outlook

6.1. United States: PFAS Regulations and Advanced Leachate Treatment Technologies

6.2. China: Government Investment and Forward Osmosis Innovations

6.3. Germany: EU Directives and Digital Solutions

6.4. Australia: Environmental Stewardship and Virtual Curtain Technology

6.5. India: ZLD Mandates and Large-Scale Industrial Leachate Projects

6.6. Japan: MBR and Membrane Technology Innovations

6.7. Other Countries Analyzed

6.7.1. North America (Canada, Mexico)

6.7.2. Europe (UK, France, Spain, Italy, Russia, Rest of Europe)

6.7.3. Asia Pacific (South Korea, South East Asia, Rest of Asia)

6.7.4. South America (Brazil, Argentina, Rest of South America)

6.7.5. Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

7. Market Size Outlook by Region (2025-2034)

7.1. North America Leachate Treatment Systems Market Size Outlook to 2034

7.1.1. By Technology

7.1.2. By System Configuration

7.1.3. By Landfill Phase & Leachate Characteristics

7.1.4. By Disposal

7.1.5. By Application

7.2. Europe Leachate Treatment Systems Market Size Outlook to 2034

7.2.1. By Technology

7.2.2. By System Configuration

7.2.3. By Landfill Phase & Leachate Characteristics

7.2.4. By Disposal

7.2.5. By Application

7.3. Asia Pacific Leachate Treatment Systems Market Size Outlook to 2034

7.3.1. By Technology

7.3.2. By System Configuration

7.3.3. By Landfill Phase & Leachate Characteristics

7.3.4. By Disposal

7.3.5. By Application

7.4. South America Leachate Treatment Systems Market Size Outlook to 2034

7.4.1. By Technology

7.4.2. By System Configuration

7.4.3. By Landfill Phase & Leachate Characteristics

7.4.4. By Disposal

7.4.5. By Application

7.5. Middle East and Africa Leachate Treatment Systems Market Size Outlook to 2034

7.5.1. By Technology

7.5.2. By System Configuration

7.5.3. By Landfill Phase & Leachate Characteristics

7.5.4. By Disposal

7.5.5. By Application

8. Company Profiles: Leading Players in Leachate Treatment Systems Market

8.1. Veolia

8.2. SUEZ

8.3. Xylem Inc.

8.4. Evoqua Water Technologies

8.5. DuPont de Nemours, Inc.

8.6. Pentair plc

8.7. Toray Industries, Inc.

8.8. Aquatech International

8.9. Kubota Corporation

8.10. The Dow Chemical Company

8.11. V.A. TECH WABAG Ltd.

8.12. Mitsubishi Chemical Corporation

8.13. Kurita Water Industries Ltd.

8.14. H2O GmbH

8.15. Thermax Limited

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures