Coagulants and Flocculants Market in Water and Wastewater Treatment Outlook: Value Forecast and Strategic Growth Analysis

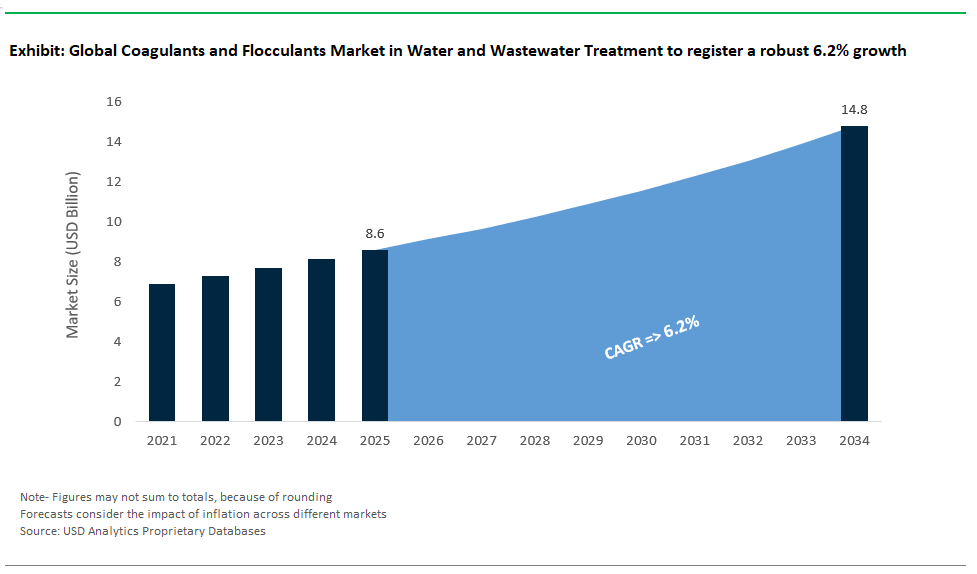

The coagulants and flocculants market in Water and Wastewater Treatment is valued at $8.6 billion in 2025 and is projected to reach $14.8 billion by 2034, registering a CAGR of 6.2%. This sector is vital for municipal and industrial water treatment, responding to the growing global need for effective solid-liquid separation, sludge volume reduction, and contaminant capture. In traditional systems, metal salt coagulants like aluminum sulfate (alum) and ferric chloride are widely used due to their versatility and recognition by regulators. These salts work well within doses of 10–150 mg/L, depending on raw water turbidity and pH, and consistently achieve over 95% turbidity removal when colloidal particles are larger than 0.1 µm, according to AWWA B403 protocols. However, their effectiveness is limited by sludge production and sensitivity to pH.

Polymer-based flocculants, especially high-charge cationic types like polyDADMAC with charge densities of 40–80%, are becoming essential for improving sludge dewatering in secondary treatment systems and centrifuge-fed processes. Anionic polymers, with molecular weights between 10–20 million Da, provide strong bridging action. They are often used to enhance settling in high-solids waste streams and mining effluents. At the same time, the market is slowly shifting toward sustainable and biodegradable options.

Bio-derived coagulants like chitosan, made from crustacean waste, show turbidity removal rates of 85–92% within pH levels of 6.0–8.0 at moderate doses (5–50 mg/L). They offer effective performance for decentralized and small-scale systems that need low-toxicity solutions. This trend aligns with the increasing regulatory focus on leftover metals, discharge toxicity, and circular economy practices. In all application areas drinking water, industrial process water, and wastewater buyers are focusing on multi-functionality, smaller chemical footprints, and real-time dose optimization. This is driving suppliers to offer integrated solutions that combine traditional metal salts, high-performance polymers, and new bio-coagulants with dosing automation and system diagnostics.

New Technologies and Sustainability Trends Shape the Future of Coagulants and Flocculants Market

Market Trend: Bio-Based and Intelligent Polymer Systems Redefine Coagulation-Flocculation in Modern Treatment Plants

The coagulants and flocculants market is changing significantly as utilities and industrial processors move away from standard metal salts like alum and ferric chloride toward bio-based alternatives and AI-optimized synthetic polymers. This shift is driven by regulatory requirements, such as national bans on aluminum-based coagulants in agricultural runoff, as seen in Thailand. It also responds to performance needs in complex waste scenarios. Lignin-based products like BASF’s Sokalan® Nature achieve over 95% turbidity removal in municipal wastewater systems at half the chemical dose of alum, with a 30% reduction in sludge volumes. This offers compelling operational and environmental benefits. Similarly, chitosan coagulants made from crab shells are marketed as safer, biodegradable options in irrigation-heavy regions. They effectively remove pesticides and organic materials without adding residual metals to soil or water. Adding to this bio-based trend is the use of machine learning in chemical dosing. These systems use real-time process data to adjust the charge density and molecular weight distribution of polyacrylamides (PAMs). This allows treatment facilities to respond to changing wastewater profiles, as seen in Chinese textile parks. These smart polymer systems have reduced coagulant usage by 25% while maintaining or even improving clarity and pollutant removal. Recent studies, such as those from the University of Tokyo in 2024, show that cationic biopolymers outperform alum in PFAS removal, highlighting their growing importance under tighter contaminant limits. As water treatment becomes more decentralized and focused on sustainability, the market for coagulants and flocculants is shifting toward programmable, low-toxicity chemicals that balance effectiveness, cost, and environmental impact.

Market Opportunity: Resource Recovery from Mining and Energy Wastewater Fuels Demand for High-Performance Flocculants

A major growth opportunity for coagulants and flocculants is in recovering valuable resources from mining tailings and oil and gas wastewater. In the extraction of lithium, copper, and rare earth elements, customized flocculant formulations not only aid in solids separation but also help concentrate and recover critical minerals. For example, Rio Tinto’s lithium brine operations use tailored PAM flocculants to extract lithium ions while clarifying water for reuse. Similarly, Codelco in Chile uses chitosan-copper complexes to capture rare earth elements from acid mine drainage, demonstrating the dual purpose of biopolymers in heavy metal remediation and resource recovery. In the oil and gas industry, advanced flocculants are essential for treating produced water, where traditional gravity separation falls short. Saudi Aramco’s SmartFloc platform uses thermoresponsive polymers that work well at high temperatures (80°C+). This approach enables 90% reuse of fracking wastewater and can save up to $0.50 per barrel. ExxonMobil’s operations in the Permian Basin have started using magnetic flocculants to remove heavy metals before discharge or reinjection. This meets new EPA discharge standards linked to PFAS and other persistent pollutants. The demand also extends to Zero Liquid Discharge (ZLD) systems, where Veolia’s RecoFloc hybrid formulations help cut the energy needed for evaporation by 40% in Indian textile clusters. This is crucial as water reuse becomes mandatory under local discharge regulations. Amid stringent EPA requirements for PFAS removal, the need for high-charge-density and modified polymers is rising, especially in applications where separation performance directly translates into recovered value. This combination of chemistry and circular economy is changing the role of coagulants and flocculants from cost centers to revenue sources in resource-heavy industries.

Coagulants and Flocculants Market in Water and Wastewater Treatment Competitive Landscape Analysis

The global market for coagulants and flocculants in water and wastewater treatment consists of major global players, highly specialized regional companies, and vertically integrated providers. The competition can be divided between synthetic flocculant polymers, where SNF Floerger is the clear global leader, and inorganic coagulants like PAC and iron/aluminum salts, which have a more diverse supplier base at the regional level. Companies such as Kemira, BASF, and Solenis hold significant influence in both chemical categories due to their extensive product ranges and strong presence in municipal and industrial markets. Vertical integration is a key feature in this field, especially for polymer producers like SNF, which oversees acrylamide monomer production, allowing for cost and formulation benefits at scale.

A major differentiator among top players is the degree of integration between chemistry, digital tools, and service delivery. Providers like Ecolab, through Nalco Water, and ChemTreat have effectively utilized this integration by offering real-time monitoring and optimization solutions, such as 3D TRASAR, along with their chemical offerings, securing a strong position in industrial water treatment. This approach, which creates a "solution ecosystem," is becoming more important as end-users seek both effective treatment and operational clarity. Similarly, Kurita and SUEZ, now part of Veolia, combine traditional chemical supply with built-in monitoring systems and equipment packages, focusing on high-value applications like ultrapure water and water reuse.

Application specialization also significantly impacts market position. Companies like Kemira and Buckman possess deep expertise in pulp and paper, allowing them to provide focused programs with proven results. In contrast, regional leaders like IXOM in Australia and New Zealand and Feralco in Europe emphasize supply chain reliability and alignment with regulations in their primary areas. They often secure long-term municipal contracts through strong logistical capabilities and dependable formulations. Additionally, the changing focus on sustainability is shifting R&D priorities across the industry, with a noticeable move toward bio-based flocculants, low-sludge coagulants, and solutions that support circular water practices.

Coagulants and Flocculants Market in Water and Wastewater Treatment – Segmentation Insights (2025–2034)

By Type: Coagulants Hold the Largest Share While Flocculants Grow Slightly Faster

In the global coagulants and flocculants market for water and wastewater treatment, coagulants account for the largest share, making up approximately 59.1% of the total market in 2025. Their dominance is attributed to their critical role in destabilizing and aggregating suspended particles and colloids in raw water sources, enabling efficient primary clarification. Coagulants both inorganic types like aluminum sulfate and ferric chloride and organic variants are indispensable in municipal and industrial water treatment systems for reducing turbidity, removing pathogens, and preparing water for further filtration. In contrast, flocculants are growing at a slightly faster pace, with a projected CAGR of 7.9% through 2034. These agents are essential during the secondary treatment phase, where they promote the formation of larger, more easily settled flocs from destabilized particles. Synthetic polymer-based flocculants, particularly polyacrylamides, are increasingly favored for their high efficiency at low dosages. Additionally, hybrid coagulant-flocculant formulations are gaining popularity for their ability to optimize treatment performance, reduce sludge volume, and lower chemical consumption.

By End-User Industry: Municipal Water Treatment Dominates; Textile Industry Registers Fastest Growth

By end-user industry, municipal water treatment leads the coagulants and flocculants market, holding a market share of approximately 42.7% in 2025. This segment benefits from large-scale implementation in both drinking water and sewage treatment infrastructure, where coagulants and flocculants are used extensively for removing suspended solids, organic matter, and pathogens to meet regulatory standards. The continuous investment in water infrastructure upgrades and population-driven demand ensures steady growth in this segment. Meanwhile, the textile industry is witnessing the fastest growth, expanding at a CAGR of 7.2% during the forecast period. This surge is fueled by stringent regulations surrounding color removal, chemical oxygen demand (COD) reduction, and zero-liquid discharge (ZLD) compliance, which require effective coagulation and flocculation solutions. Industrial wastewater treatment, particularly in sectors like food processing, chemicals, and manufacturing, is also expanding steadily as discharge norms tighten globally. The oil and gas sector continues to rely on advanced flocculant formulations for treating produced water, while other niche sectors contribute to baseline demand for both traditional and specialty coagulant-flocculant systems.

.png)

United States Expands Coagulants and Flocculants Market with Regulatory Action and Sustainable Innovation

The United States remains a powerhouse in the global coagulants and flocculants market, driven by rigorous EPA mandates, private-sector investment, and sustainability initiatives. In November 2022, SNF’s $300 million investment in its Louisiana facility boosting powder-grade polyacrylamide and acrylamide capacity underscores America’s growing demand for high-performance water treatment polymers. As the EPA clamps down on emerging pollutants like PFAS and microplastics, there’s a shift toward next-generation solutions tailored for solid-liquid separation in complex industrial effluents, municipal drinking water, and challenging sectors such as oil, gas, and mining.

A rising focus on bio-based coagulants and flocculants reflects mounting pressure for greener, petroleum-alternative chemistries in the U.S. water sector. Municipal infrastructure upgrades, paired with stricter effluent standards, are spurring demand for chemicals that deliver high removal efficiency and operational reliability. This landscape positions the U.S. as a leader in both advanced technology adoption and the sustainable evolution of the coagulants and flocculants market.

China Accelerates Coagulants and Flocculants Demand with Massive Water Infrastructure and Policy Reforms

China’s coagulants and flocculants market is surging, powered by historic government investments in environmental infrastructure and an aggressive campaign against water pollution. The "Water Ten Plan" channeled over RMB 673 billion into pollution control, enabling the country to reach a 98.69% urban wastewater treatment rate by the end of 2023. This vast network of centralized plants is a major consumer of coagulants and flocculants for primary and secondary treatment, solid-liquid separation, and aquatic ecosystem restoration.

China’s Ministry of Ecology and Environment has rolled out real-time surface water quality monitoring, increasing transparency and boosting demand for effective treatment chemicals across thousands of facilities. Pilot projects in the Yangtze and Yellow River basins demonstrate the national commitment to science-based, data-driven pollution control, fueling ongoing market expansion for both traditional and innovative coagulation and flocculation solutions.

Germany Champions Sustainable Coagulants and Flocculants with Green Chemistry and Smart Water Management

Germany is a hub for eco-innovation and regulatory leadership in the coagulants and flocculants market, with growth anchored in compliance with the German Water Resources Act (WHG) and EU Water Framework Directive. Leading firms like BASF are pioneering biodegradable and eco-friendly polymer chemistries to meet Europe’s green standards. The integration of AI and IoT into water management is transforming the sector, with German utilities and industrial users optimizing chemical dosing for efficiency, cost savings, and minimal waste.

A strong circular economy ethos is propelling the uptake of high-efficiency coagulation and flocculation systems, particularly in zero-liquid discharge (ZLD) and resource recovery applications. Germany’s continued focus on sustainability, advanced water technology, and regulatory compliance cements its role as a European leader in green, intelligent water treatment solutions.

India Drives Coagulants and Flocculants Market Growth with Government Missions and Modular Water Treatment

India’s market for coagulants and flocculants is booming, propelled by flagship programs like Jal Jeevan Mission and Namami Gange, which are transforming municipal and industrial water treatment infrastructure. States including Gujarat, Maharashtra, and Karnataka are mandating the use of treated wastewater in agriculture and industry, creating sustained demand for high-quality coagulation and flocculation chemicals to meet stringent reuse standards.

The emergence of decentralized, modular, and dual-phase treatment systems is fueling the need for optimized chemical solutions. Green bonds and public-private partnerships are unlocking investment in advanced treatment facilities, further driving market expansion. As cities and industries prioritize water reuse, India’s coagulants and flocculants market is set for robust growth anchored in innovation, policy, and infrastructure modernization.

Japan Leads in High-Performance Polymer Flocculants and Specialized Water Treatment Chemistry

Japan’s coagulants and flocculants market is characterized by its advanced technology base and a strong emphasis on precision chemistry for both municipal and industrial applications. Leading Japanese companies are developing water-soluble polymer flocculants like Hymo Corporation’s "Himoloc ZP," a cationic agent renowned for dewatering hard-to-treat sludge. The expertise of giants such as Oji Holdings is being leveraged to optimize coagulation and flocculation performance through rigorous jar testing and tailored formulations.

Japan’s need to treat complex industrial effluents particularly from electronics, paper, and chemical manufacturing drives ongoing innovation in multifunctional flocculants, including mud rheology modifiers and dust-reducing agents. Continuous R&D investment and a focus on highly functional, high-value products keep Japan at the technological frontier of the global coagulants and flocculants market.

Brazil Bolsters Coagulants and Flocculants Market with Sanitation Reforms and Infrastructure Overhaul

Brazil is undergoing a transformative phase in water and wastewater management, underpinned by regulatory reforms and major investment in sanitation infrastructure. The goal of universal potable water access by 2033 and the new federal sanitation framework have attracted significant private investment, with projects like the Vitória Water Reclamation Station setting benchmarks in water reuse technology. Advanced pre-treatment including efficient coagulation and flocculation is essential for membrane bioreactors and reverse osmosis systems now deployed nationwide.

Federal support through the Brazilian National Development Bank (BNDES) ensures that a large share of new investment is directed toward chemicals, making coagulants and flocculants critical to the success of Brazil’s modernization push. This environment supports the adoption of innovative solutions in both urban and rural water treatment markets.

United Kingdom Accelerates Coagulants and Flocculants Demand with Regulatory Shifts and Pollution Targets

The United Kingdom is seeing rapid market evolution for coagulants and flocculants, spurred by new regulatory measures and a societal focus on water quality improvement. Plans to replace Ofwat with a new, empowered regulator signal a stricter era of compliance for water utilities. The Environmental Targets (Water) (England) Regulations 2022 require a significant reduction in phosphorus and nitrogen loads, creating a critical need for enhanced chemical treatment across the sector.

Cutting-edge research partnerships, such as those led by Cranfield University, are advancing the treatment of emerging contaminants like PFAS and microplastics through robust coagulation and flocculation techniques. The government’s "Plan for Water" is channelling further investment into sustainable water treatment technologies, supporting long-term demand for advanced chemicals.

France Drives Coagulants and Flocculants Market with National Water Plan and Resource Protection Initiatives

France’s coagulants and flocculants market is advancing rapidly, powered by the government’s 2023-2030 water management plan that targets a 10% reduction in water abstraction and promotes the reuse of treated wastewater. Enhanced protection of drinking water catchment areas and stricter quality controls are intensifying demand for effective chemical treatment at both the source and municipal level.

Industry leaders such as Suez are at the forefront, developing and operating advanced water reuse plants and investing in innovative treatment solutions. With water agencies increasing budgets for research and implementation, France is prioritizing the development of sustainable and high-performance coagulants and flocculants, reinforcing its role as a leader in next-generation water treatment chemistry.

Coagulants and Flocculants Market in Water and Wastewater Treatment Report Scope

Coagulants and Flocculants Market in Water and Wastewater Treatment

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8.6 Billion

|

|

Market Size (2034)

|

$14.8 Billion

|

|

Market Growth Rate

|

6.2%

|

|

Segments

|

By Type (Inorganic Coagulants, Organic Coagulants, Flocculants (Polymers)), By Application (Primary Treatment, Secondary Treatment, Tertiary Treatment and Advanced Treatment), By End-User Industry (Municipal Water Treatment, Industrial Water and Wastewater Treatment

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

SNF Floerger (France), Kemira Oyj (Finland), BASF SE (Germany), Ecolab Inc. (U.S.), Solenis LLC (U.S.), SUEZ SA (France), Kurita Water Industries Ltd. (Japan), Veolia Water Technologies (France), Buckman (U.S.), Feralco AB (Sweden), Solvay (Belgium), IXOM (Australia), ChemTreat, Inc. (U.S.)

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Coagulants and Flocculants in Water and Wastewater Treatment Market Segmentation

By Type

- Inorganic Coagulants

- Aluminum Sulfate

- Ferric Chloride

- Ferric Sulfate

- Poly Aluminum Chloride (PAC)

- Poly Ferric Sulfate (PFS)

- Sodium Aluminate

- Others

- Organic Coagulants

- Polyamines

- PolyDADMAC (Polydiallyldimethylammonium chloride)

- Melamine Formaldehyde Resins

- Tannins

- Starches

- Chitosan

- Others

- Flocculants (Polymers)

- Synthetic Flocculants

- Polyacrylamide (PAM) and its derivatives

- Polyethylene Oxide (PEO)

- Polyethyleneimine (PEI)

- Polyacrylic Acid (PAA)

- Natural Flocculants (Bio-based/Green Flocculants)

- Starch-based Flocculants

- Cellulose-based Flocculants

- Chitosan

- Tannins

- Microbial Flocculants

- Other plant-based derivatives

By Application

- Primary Treatment

- Secondary Treatment

- Tertiary Treatment and Advanced Treatment

By End-User Industry

- Municipal Water Treatment

- Drinking Water Treatment Plants

- Municipal Wastewater Treatment Plants

- Industrial Water and Wastewater Treatment

- Power Generation

- Oil and Gas

- Chemical and Petrochemical

- Pulp and Paper

- Food and Beverage

- Mining and Metallurgy

- Textile

- Pharmaceutical

- Automotive

- Electronics

- Sugar Industry

- Other Manufacturing and Process Industries

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Coagulants and Flocculants Market in Water and Wastewater Treatment

- SNF Floerger (France)

- Kemira Oyj (Finland)

- BASF SE (Germany)

- Ecolab Inc. (U.S.)

- Solenis LLC (U.S.)

- SUEZ SA (France)

- Kurita Water Industries Ltd. (Japan)

- Veolia Water Technologies (France)

- Buckman (U.S.)

- FeralcAB (Sweden)

- Solvay (Belgium)

- IXOM (Australia)

- ChemTreat, Inc. (U.S.)

* List Not Exhaustive

Research Coverage

This report investigates the global coagulants and flocculants market in water and wastewater treatment, providing an in-depth analysis of the latest breakthroughs, trends, and regulatory dynamics shaping the industry. Through comprehensive analysis reviews, the study highlights new technologies, sustainability shifts, and the strategic role of bio-based and intelligent polymer systems in municipal and industrial water management. Covering key market drivers such as resource recovery, sludge reduction, and solid-liquid separation, this report is an essential resource for industry professionals, technology suppliers, and investors seeking actionable intelligence on market growth, value opportunities, and regional prospects. Developed by USDAnalytics, this authoritative research offers a complete overview of the competitive landscape, market share analysis, segmentation by chemical type, application, and end-user, and in-depth country-level insights—delivering the strategic foundation needed for high-value decision-making across the global water and wastewater chemicals sector.

Scope Highlights:

- Segmentation:

- By Type: Inorganic Coagulants, Organic Coagulants, Flocculants, Natural/Bio-based—Starch-based, Cellulose-based, Chitosan, Tannins, Microbial, Other plant-based derivatives)

- By Application: Primary Treatment, Secondary Treatment, Tertiary Treatment and Advanced Treatment

- By End-User Industry: Municipal Water Treatment; Industrial Water and Wastewater Treatment

- Geographic Scope: Covers 25+ countries across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

- Data Coverage: Historic data from 2021 to 2024 and forecasts from 2025 to 2034.

- Key Players: SNF Floerger (France), Kemira Oyj (Finland), BASF SE (Germany), Ecolab Inc. (U.S.), Solenis LLC (U.S.), SUEZ SA (France), Kurita Water Industries Ltd. (Japan), Veolia Water Technologies (France), Buckman (U.S.), FeralcAB (Sweden), Solvay (Belgium), IXOM (Australia), ChemTreat, Inc. (U.S.)

Methodology

USDAnalytics utilizes a robust, multi-layered research methodology, integrating both primary and secondary sources. Market sizing and forecasting leverage data triangulation from company financials, regulatory databases, project tracking, and expert interviews across the value chain. Advanced analytics, historic trends (2021–2024), and scenario-based modeling underpin the 2025–2034 forecasts, ensuring accuracy and depth. The report’s qualitative analysis is validated by industry professionals, ensuring actionable insights and high-value strategic guidance for stakeholders across the coagulants and flocculants market in water and wastewater treatment.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements