Strong Market Growth Driven by Industrial Reuse and Energy Efficiency

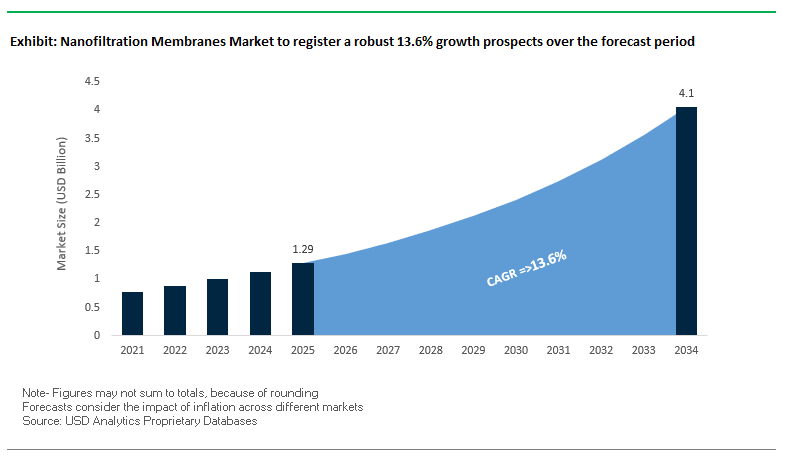

The Nanofiltration Membranes Market is projected to grow from USD 1.29 billion in 2025 to USD 4.1 billion by 2034, registering a CAGR of 13.6%. This rapid expansion reflects the rising demand for advanced water treatment technologies that balance selective contaminant removal, resource recovery, and energy efficiency.

Nanofiltration (NF) membranes are moving from niche applications to mainstream adoption:

- Industrial Water Reuse: Industries are under increasing pressure to conserve resources and comply with discharge regulations. NF membranes enable efficient treatment of complex wastewater streams, reducing discharge volumes while supporting circular water use.

- Targeted Contaminant Removal: NF membranes are uniquely suited for selective separation removing hardness, heavy metals, and viruses while retaining beneficial minerals making them ideal for drinking water treatment and food & beverage applications.

- Resource Recovery: Products such as DuPont’s FilmTec™ LiNE-XD membranes are enabling cost-efficient lithium extraction from brines, a critical step in securing sustainable raw materials for the electric vehicle battery industry.

- Energy Efficiency: NF membranes require significantly lower pressure compared to reverse osmosis (RO), delivering energy savings for desalination and municipal purification plants, while maintaining high performance.

Market Analysis: Recent News and Technological Developments

The past two years have seen rapid innovation and strategic consolidation in the nanofiltration membranes industry. In August 2025, DuPont Water Solutions was recognized with a BIG Sustainability Award for its FilmTec™ Fortilife™ membranes, which improve industrial wastewater treatment and enable minimal liquid discharge (MLD). In the same month, an academic study highlighted how advanced nanofiltration membranes are increasingly effective in removing emerging contaminants, addressing a growing regulatory challenge for industries.

In June 2025, consolidation shaped the market as Nanostone Water and Solecta merged to form Acuriant Technologies, a new entity focusing on polymeric and ceramic hybrid membranes. Also in June, NX Filtration received a repeat order to double the capacity of a large-scale water reuse system in Mexico, reinforcing the growing adoption of hollow-fiber nanofiltration. Meanwhile, Veolia launched its TERION™ S system in May 2025, integrating RO, electrodeionization, and NF pre-treatment to deliver high-grade deionized water for industrial and laboratory applications.

Academic and industry-led innovations also marked 2025, with April 2025 research highlighting electrostatic air spray deposition combined with NF membranes, enhancing hydrophilicity and separation performance. In earlier milestones, DuPont launched its FilmTec™ Hypershell™ NF245XD membranes in February 2024, specifically designed for dairy operations to improve quality and reduce costs. In March 2024, NX Filtration partnered with TZW-DVGW to advance PFAS removal from drinking water, reflecting how NF membranes are becoming critical in meeting next-generation regulatory and health standards.

Emerging Trends and Opportunities in the Nanofiltration Membranes Market

Growth in Selective Water Softening and Desalination Pre-treatment

One of the most prominent trends shaping the nanofiltration membranes industry is their adoption in municipal and industrial water treatment for softening and partial desalination. Unlike reverse osmosis, NF membranes selectively reject multivalent ions (e.g., calcium, magnesium) while allowing beneficial monovalent ions to pass.

A study by the Bhabha Atomic Research Centre (BARC) revealed that advanced charged NF membranes achieved a 97% rejection rate for sodium sulfate ($Na_2SO_4$) while maintaining only 20% rejection of sodium chloride ($NaCl$). This makes NF highly efficient for applications like brackish water treatment, where reducing hardness without stripping all minerals is essential. Importantly, NF operates at significantly lower energy costs than RO, which is accelerating adoption in cost-sensitive regions.

Expansion in the Food and Beverage Industry

The food & beverage sector is emerging as a key growth vertical for NF membranes. They are widely used for juice clarification, dairy product concentration, and beer filtration helping preserve product integrity while improving process sustainability.

For example, in September 2023, NX Filtration supplied hollow fiber NF membranes to a Carlsberg brewery in Denmark for beer filtration. This application underscores the industry’s pivot toward advanced separation technologies that avoid heat and chemicals, aligning with consumer demand for natural, minimally processed products.

Strategic Investments in Manufacturing and R&D

Global leaders in the nanofiltration membranes market are doubling down on R&D and large-scale manufacturing facilities to meet surging demand. In July 2021, NX Filtration announced a high-tech megafactory in the Netherlands to expand production capacity. Partnerships with firms such as Jacobs Engineering and Lantania highlight growing confidence in NF as the future of industrial water treatment and water reuse projects worldwide.

Application in Pharmaceutical and Chemical Separations

The pharmaceutical and chemical industries are increasingly adopting organic solvent nanofiltration (OSN) for catalyst recycling, solvent recovery, and API purification. Unlike distillation, NF enables energy savings, reduced solid waste, and scalability.

A recent review in ACS Publications highlighted that OSN could substantially reduce the carbon footprint of pharmaceutical manufacturing. With rising regulatory pressure on green chemistry and sustainable manufacturing, NF membranes are poised to become a cornerstone of high-value chemical separations.

Market Share Analysis of the Nanofiltration Membranes Market

Market Share by Type of Nanofiltration Membranes

Polymeric nanofiltration membranes will dominate the market in 2025, holding an estimated 85% share, thanks to their cost-effectiveness, manufacturing scalability, and proven performance in both municipal and industrial applications. Materials such as polyamide, cellulose acetate, and polysulfone remain the backbone of NF technology.

However, ceramic nanofiltration membranes (8%) are rapidly gaining ground due to their superior durability, thermal stability, and chemical resistance, making them indispensable in harsh industrial settings such as chemical processing and aggressive wastewater treatment.

Meanwhile, hybrid nanofiltration membranes (5%), incorporating inorganic nanoparticles like TiO2 into polymeric matrices, are emerging as the bridge between low-cost polymeric options and high-performance ceramics. The “Others” category (2%), including biomimetic and thin-film nanocomposites (TFN), represents the next wave of high-performance NF membranes currently in R&D.

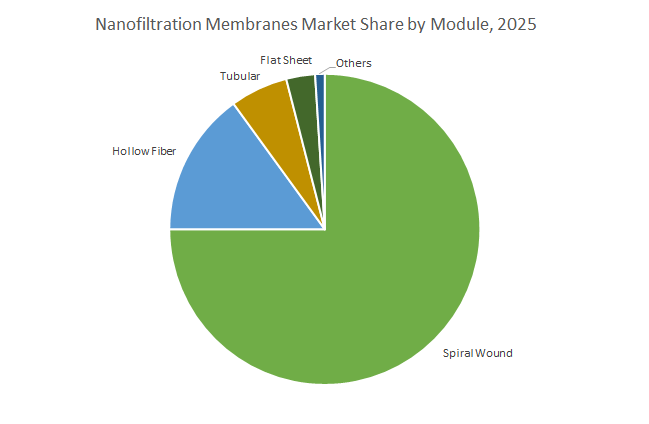

Market Share by Module Configuration

In terms of module design, spiral wound NF membranes (75%) dominate due to their high packing density, compact footprint, and cost-effectiveness, making them the industry standard for municipal water treatment and desalination pre-treatment.

Hollow fiber modules (15%) are gaining traction in wastewater treatment and industrial processes where resistance to fouling is critical. Tubular NF membranes (6%) serve niche markets with high-solid, viscous, or aggressive process streams, such as pulp & paper or textiles, where ease of cleaning is vital. Flat sheet membranes (3%) remain largely restricted to pilot-scale testing and R&D, while other niche formats (1%) serve highly specialized applications.

Market Share by Application Sector

Industrial applications (65%) account for the majority of the NF membranes market, with broad adoption across food & beverage, pharmaceuticals, textiles, mining, and chemicals. NF plays a crucial role in processes like whey demineralization, dye recovery, catalyst recycling, and selective metal removal, making it indispensable for resource recovery and sustainable manufacturing.

Meanwhile, municipal applications (35%) are steadily expanding, fueled by rising urban water demand, stricter water quality standards, and the need for potable reuse. NF is widely deployed in water softening, natural organic matter (NOM) removal, disinfection byproduct control, and micropollutant removal, as well as advanced wastewater recycling projects for direct and indirect potable reuse.

China: Regulatory Push and Industrial Investment Driving Nanofiltration

China’s nanofiltration membranes market is driven by strong government regulations and industrial expansion. The "Guiding Opinions on Promoting the Utilization of Wastewater Resources" sets a target to achieve a recycled water utilization rate of 25% or more in water-scarce cities by 2025, highlighting nanofiltration’s importance in water reuse applications. Major investments include the 2018 agreement between Sinochem International and Ningbo Xiangshan County for a RMB 3.5 billion production and R&D center, initially focused on reverse osmosis membranes with plans to expand into high-performance nanofiltration. Technological advancements such as the 2024 hollow-fiber ultrafiltration (UF) membrane with enhanced antifouling properties are increasingly integrated into multi-stage systems with nanofiltration for producing high-quality water. Key applications include seawater desalination and ultrapure water preparation for electronics and high-tech industries.

United States: Government-Funded Innovation and Advanced Manufacturing

The U.S. nanofiltration membranes market benefits from substantial government funding and academic research. The Department of Energy (DOE) and the National Alliance for Water Innovation (NAWI) selected 12 projects to enhance desalination and water reuse efficiency, including electrospray printing technology to fabricate porous membranes for improved filtration performance. NSF-supported research drives innovation in water purification, chemical separations, and biopharmaceutical applications, complementing federal initiatives. Corporate leaders such as DuPont Water Solutions are developing nanofiltration membranes to address emerging contaminants like PFAS, aligning with U.S. infrastructure modernization under the Bipartisan Infrastructure Law.

India: Rural Water Initiatives and Nanomaterial Integration

India’s nanofiltration membranes market is expanding through government programs and technological adoption. The “Jal Jeevan Mission” and the Department of Science & Technology’s Water Technology Initiative promote advanced filtration technologies in rural areas. In 2025, researchers highlighted the integration of nanomaterials graphene oxide, carbon nanotubes, and metal-organic frameworks (MOFs) into nanofiltration membranes, enhancing mechanical strength, permeability, and antifouling properties. Infrastructure investments, such as the Ghaziabad Nagar Nigam’s ₹150 crore Certified Green Municipal Bond for a Tertiary Sewage Treatment Plant (TSTP), underscore the commitment to advanced wastewater reuse, industrial water applications, and sustainable water management.

Germany: Industrial Leadership and Advanced Nanofiltration Solutions

Germany remains a leader in industrial nanofiltration applications, driven by environmental sustainability and regulatory compliance. Companies like PWT Wassertechnik specialize in nanofiltration to treat and reuse industrial wastewater efficiently. Technological innovations from MANN+HUMMEL focus on digital integration and membrane solutions to optimize industrial processes and support green energy initiatives. A 2025 market report noted Germany’s nanofiltration membranes market holds the largest market share in Europe, reflecting the country’s robust adoption of advanced water treatment systems and commitment to environmental sustainability.

Japan: Academic Excellence and Global Technology Provider

Japan’s nanofiltration membranes market is propelled by advanced research and international projects. The Membrane Engineering Group at Kobe University continues to develop novel functional membranes for water and atmospheric applications, advancing filtration performance. Toray Industries’ high-performance RO membranes for large-scale desalination plants in Saudi Arabia highlight Japan’s global role as a provider of cutting-edge membrane technologies, where nanofiltration is often employed as a critical stage for water purification.

Australia: Water Recycling Leadership and Research-Driven Advancements

Australia faces severe water scarcity, making water recycling and reuse a national priority. The government’s National Water Grid Fund invests in projects incorporating advanced nanofiltration and treatment plants. Academic research at the Institute for Sustainable Industries and Liveable Cities (ISILC) at Victoria University focuses on improving desalination recovery rates and reducing membrane fouling and scaling, addressing key technical challenges in nanofiltration systems. These initiatives enhance Australia’s capabilities in sustainable water management and advanced membrane technologies.

Competitive Landscape: Key Companies Shaping the Nanofiltration Membranes Market

The nanofiltration membranes market is highly competitive, with global leaders investing in R&D, large-scale projects, and sustainability-focused innovations. Companies are differentiating themselves through product portfolios, digital integration, project execution expertise, and application-specific solutions.

DuPont Water Solutions Leads in Resource Recovery

DuPont has established itself as a global leader in nanofiltration membranes with a strong emphasis on circular economy solutions. Its FilmTec™ LiNE-XD membranes enable high-yield lithium extraction from brines, addressing a critical supply chain need for EV batteries. The company’s FilmTec™ Fortilife™ portfolio is designed for brine concentration and industrial reuse, pushing the limits of energy efficiency. Complementing its hardware, DuPont offers WAVE PRO, a digital modeling tool that helps water Stakeholders optimize NF and RO designs. In August 2025, DuPont’s innovation earned it the BIG Sustainability Award, reinforcing its position as a market pioneer.

SUEZ Water Technologies & Solutions Expands Large-Scale Projects

As part of Veolia, SUEZ has strengthened its position as a holistic water and waste management solutions provider, with nanofiltration at the core of many projects. The company has executed some of the world’s largest water infrastructure projects, including China’s biggest industrial NF desalination facility. In addition, its acquisition of the LANXESS RO product line enhances its membrane portfolio and creates synergies between NF and brackish water RO solutions. Application-specific products, such as SWSR membranes for offshore oil projects in Brazil, underscore its ability to deliver tailored separation solutions.

Koch Separation Solutions Rebrands as Kovalus with a Focus on Custom Engineering

Koch Separation Solutions (KSS), now operating as Kovalus Separation Solutions, has built a reputation for advanced engineering and custom-designed NF and RO systems. Its Fluid Systems® NF membranes are designed for high purity and long operational lifetimes, while innovations such as low-fouling reinforced membranes support cost-efficient industrial operations. The company is also expanding its manufacturing capacity with a new assembly plant in Mexico, targeting a 50% increase in production to meet rising global demand. KSS serves a wide spectrum of industries, from food and beverage to lithium brine recovery, showcasing its diverse application expertise.

Toray Industries Strengthens Its Role in Global Desalination

Toray Industries leverages deep expertise in polymer science and advanced material design to deliver high-performance nanofiltration membranes. Its product portfolio is engineered with corrugated structures and high-strength polymers, improving selectivity and flow rates. Toray continues to be a key partner in Saudi Arabia’s Yanbu 4 and Shuaibah 3 desalination projects, advancing the shift from energy-intensive systems to eco-friendly NF-driven plants. To support long-term innovation, Toray established a Water Research Center in India, where it develops solutions tailored to regional challenges in industrial and municipal water treatment.

Nitto Denko Corporation Enhances Integrated Membrane Solutions

Through its Hydranautics brand, Nitto offers a comprehensive range of RO, NF, UF, and MF membranes for complex water treatment needs. Its nanofiltration products are particularly effective for brackish water treatment and reclaimed wastewater reuse, making them a preferred choice in municipal and industrial projects. The company has invested heavily in low-fouling NF membranes to reduce maintenance costs while boosting system performance. By combining its strong technical support with integrated membrane solutions, Nitto continues to play a pivotal role in scaling sustainable water infrastructure globally.

NX Filtration Specializes in Hollow Fiber Direct NF Technology

NX Filtration is emerging as a disruptive innovator with its direct nanofiltration (dNF) hollow fiber technology, which simplifies treatment by reducing pre-treatment steps. Its sustainability credentials including B Corp and BREEAM-NL certifications demonstrate a strong commitment to responsible growth. The company has rapidly expanded its global footprint, winning repeat orders to double the capacity of water reuse plants in Mexico and signing strategic agreements in Vietnam. Collaborations with partners like Bucher Denwel (beer filtration) and TZW-DVGW (PFAS removal) highlight NX Filtration’s growing application-specific leadership in both industrial and municipal sectors.

Nanofiltration Membranes Market Report Scope

Nanofiltration Membranes Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.29 Billion

|

|

Market Size (2034)

|

$4.1 Billion

|

|

Market Growth Rate

|

13.6%

|

|

Segments

|

By Type (Polymeric, Ceramic, Hybrid, Others), By Module (Spiral wound, Tubular, Hollow Fiber, Flat sheet, Others), By Application (Municipal, Industrial)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

DuPont de Nemours, Inc., SUEZ, Veolia, Toray Industries, Inc., Pentair plc, Asahi Kasei Corporation, The Dow Chemical Company, NX Filtration, Kubota Corporation, LG Chem, MANN+HUMMEL, Evoqua Water Technologies, Koch Industries, Hydranautics (a Nitto Group Company), V.A. TECH WABAG Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Nanofiltration Membranes Market Segmentation

By Type

- Polymeric

- Ceramic

- Hybrid

- Others

By Module

- Spiral wound

- Tubular

- Hollow Fiber

- Flat sheet

- Others

By Application

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Nanofiltration Membranes Industry include-

- DuPont de Nemours, Inc.

- SUEZ

- Veolia

- Toray Industries, Inc.

- Pentair plc

- Asahi Kasei Corporation

- The Dow Chemical Company

- NX Filtration

- Kubota Corporation

- LG Chem

- MANN+HUMMEL

- Evoqua Water Technologies

- Koch Industries

- Hydranautics (a Nitto Group Company)

- V.A. TECH WABAG Ltd.

*- List not Exhaustive

Research Coverage

This report investigates the fast-rising nanofiltration membranes market, delivering analysis reviews on how selective separations, resource recovery, and energy efficiency are propelling NF from niche to mainstream across municipal and industrial plants. It highlights breakthroughs in thin-film chemistries, direct-NF hollow fiber designs, and digitally modeled RO–NF–EDI trains that sharpen multivalent ion rejection while cutting pressure and OPEX. The study further highlights consolidation moves, project wins, and application pivots (softening, PFAS/NOM control, lithium brines, OSN in chemicals) that are reshaping vendor strategies and qualification criteria. By converting performance metrics (permeance, selectivity, fouling resistance) into lifecycle economics and procurement scorecards, USDAnalytics equips decision-makers with bankable evidence this report is an essential resource for utilities, EPCs, and plant owners standardizing NF in reuse, pre-treatment, and high-value process lines. Scope Includes-

- Segmentation: By Type (Polymeric, Ceramic, Hybrid, Others); By Module (Spiral Wound, Tubular, Hollow Fiber; Flat Sheet; Others); By Application (Municipal, Industrial)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Frame: Historic 2021–2024; Forecast 2025–2034.

- Companies: Analysis/profiles of 15+ companies.

Methodology

We combine primary interviews (operators, OEMs/EPCs, formulators, and regulators) with secondary intelligence (standards, patents, technical papers, and disclosures). Market sizing triangulates top-down demand from reuse mandates and capacity additions with bottom-up bill-of-materials models by module type (spiral, hollow fiber, tubular) and duty (municipal vs. industrial), normalizing for flux (LMH), TMP, recovery, cleaning cadence, and replacement intervals. Forecasts apply learning curves for sheet/coating lines, energy-price scenarios, and policy cadence for softening, PFAS/NOM limits, and industrial reuse. Competitive benchmarking scores membranes on permeability–selectivity balance, fouling propensity, chemical/thermal window, and lifecycle cost per 1,000 m³, cross-validated against commissioning data and recent project announcements.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Nanofiltration Membranes Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Insights for Stakeholders

1.3. Global Market Snapshot

2. Nanofiltration Membranes Market Outlook (2025–2034)

2.1. Introduction: Strong Market Growth and Industry Transformation

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $1.29 Billion

2.2.2. Forecasted Market Size (2034): $4.1 Billion

2.2.3. Projected Compound Annual Growth Rate (CAGR): 13.6%

2.3. Key Trends and Opportunities

2.3.1. Growth in Selective Water Softening and Desalination Pre-treatment

2.3.2. Expansion in the Food and Beverage Industry

2.3.3. Strategic Investments in Manufacturing and R&D

2.3.4. Application in Pharmaceutical and Chemical Separations

3. Recent Developments and Strategic Shifts

3.1. Market Analysis: Recent News and Technological Developments

3.1.1. DuPont Water Solutions Wins BIG Sustainability Award

3.1.2. Academic Study Highlights Removal of Emerging Contaminants

3.1.3. Nanostone Water and Solecta Merge to Form Acuriant Technologies

3.1.4. NX Filtration Receives Repeat Order for Mexican Water Reuse Plant

3.1.5. Veolia Launches Integrated TERION™ S System

3.1.6. DuPont Launches Hypershell™ NF245XD Membranes for Dairy

3.1.7. NX Filtration Partners with TZW-DVGW for PFAS Removal

4. Competitive Landscape: Leading Companies

4.1. Market Overview: From Niche Technology to Mainstream Solutions

4.2. Key Competitive Factors

4.2.1. Integrated Product Portfolios

4.2.2. R&D and Innovation in Advanced Materials

4.2.3. Expertise in Large-Scale Project Execution

4.3. Profiles of Top Players

4.3.1. DuPont Water Solutions

4.3.2. SUEZ Water Technologies & Solutions

4.3.3. Koch Separation Solutions (Kovalus)

4.3.4. Toray Industries

4.3.5. Nitto Denko Corporation

4.3.6. NX Filtration

5. Nanofiltration Membranes Market – Segmentation Insights

5.1. By Type

5.1.1. Polymeric

5.1.2. Ceramic

5.1.3. Hybrid

5.1.4. Others

5.2. By Module

5.2.1. Spiral wound

5.2.2. Tubular

5.2.3. Hollow Fiber

5.2.4. Flat sheet

5.2.5. Others

5.3. By Application

5.3.1. Municipal

5.3.2. Industrial

6. Country Analysis and Outlook: Nanofiltration Membranes Market

6.1. China: Regulatory Push and Industrial Investment

6.2. United States: Government-Funded Innovation and Advanced Manufacturing

6.3. India: Rural Water Initiatives and Nanomaterial Integration

6.4. Germany: Industrial Leadership and Advanced Nanofiltration Solutions

6.5. Japan: Academic Excellence and Global Technology Provider

6.6. Australia: Water Recycling Leadership and Research-Driven Advancements

6.7. Other Key Countries

6.7.1. North America (Canada, Mexico)

6.7.2. Europe (UK, France, Spain, Italy, Russia, Rest of Europe)

6.7.3. Asia Pacific (South Korea, South East Asia, Rest of Asia)

6.7.4. South America (Brazil, Argentina, Rest of South America)

6.7.5. Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

7. Nanofiltration Membranes Market Size Outlook by Region (2025-2034)

7.1. North America Market Size Outlook to 2034

7.1.1. By Type

7.1.2. By Module

7.1.3. By Application

7.2. Europe Market Size Outlook to 2034

7.2.1. By Type

7.2.2. By Module

7.2.3. By Application

7.3. Asia Pacific Market Size Outlook to 2034

7.3.1. By Type

7.3.2. By Module

7.3.3. By Application

7.4. South America Market Size Outlook to 2034

7.4.1. By Type

7.4.2. By Module

7.4.3. By Application

7.5. Middle East and Africa Market Size Outlook to 2034

7.5.1. By Type

7.5.2. By Module

7.5.3. By Application

8. Company Profiles: Additional Leading Players

8.1. DuPont de Nemours, Inc.

8.2. SUEZ

8.3. Veolia

8.4. Toray Industries, Inc.

8.5. Pentair plc

8.6. Asahi Kasei Corporation

8.7. The Dow Chemical Company

8.8. NX Filtration

8.9. Kubota Corporation

8.10. LG Chem

8.11. MANN+HUMMEL

8.12. Evoqua Water Technologies

8.13. Koch Industries

8.14. Hydranautics (a Nitto Group Company)

8.15. V.A. TECH WABAG Ltd.

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures