Growth Driven by MBR Adoption, Industrial Durability, and Urban Water Reuse

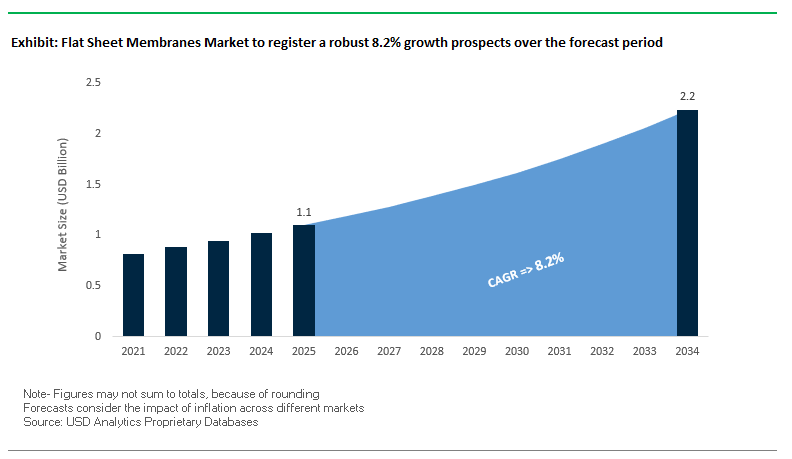

The global flat sheet membranes market is projected to reach USD 1.1 billion in 2025 and is expected to double to USD 2.2 billion by 2034, growing at a strong CAGR of 8.2%. This steady growth reflects the technology’s crucial role in modern water and wastewater treatment as well as industrial applications that demand high durability and operational resilience. For industry Stakeholders, a key question is how flat sheet membranes differentiate themselves from spiral wound or hollow fiber alternatives. The answer lies in their robust design, resistance to fouling, compact footprint, and ability to meet increasingly stringent water quality regulations.

Flat sheet membranes are being deployed extensively in membrane bioreactor (MBR) systems, which are becoming the standard for municipal wastewater treatment and water reuse. Their durability and ease of cleaning reduce long-term operational costs for utilities and industries. In urban centers, where land scarcity is a major challenge, their compact footprint enables water treatment plants to expand capacity without requiring significant space. Moreover, in harsh industrial environments, particularly those involving high-temperature fluids, abrasive chemicals, or heavy contaminants, ceramic flat sheet membranes provide unmatched reliability. These unique characteristics are positioning flat sheet membranes not only as a wastewater solution but also as a technology for food, beverage, and biopharmaceutical industries, where stable and efficient separations are critical.

Key Market Insights

- Meeting Stringent Water Quality Standards: Widely used in MBR systems to comply with tough discharge and reuse regulations.

- Durability and Lower Maintenance: Flat sheet membranes last longer, are easier to clean, and reduce replacement costs compared to other types.

- Compact Footprint for Urban Areas: Their space-efficient design makes them ideal for cities, residential developments, and industrial facilities.

- Industrial Resilience: Ceramic flat sheet membranes withstand high heat, abrasive fluids, and aggressive chemicals, supporting critical industrial operations.

Market Analysis: Recent Developments in Flat Sheet Membrane Technologies

The flat sheet membranes industry is undergoing dynamic transformation, with mergers, partnerships, product launches, and large-scale demonstrations redefining its competitive edge. In July 2025, a major announcement came when Nanostone Water and Solecta merged to form Acuriant Technologies, combining expertise in polymeric and ceramic membrane technologies. This move signals a shift toward hybrid solutions designed to address increasingly complex separation challenges. Around the same time, in June 2025, Meiden Singapore, a subsidiary of Meidensha Corporation, initiated a large-scale demonstration plant using ceramic flat sheet membranes for seawater reverse osmosis (SWRO) pre-treatment in Singapore, a project designed to boost energy efficiency in desalination.

New product introductions are further shaping the competitive landscape. In May 2025, Nanostone Water launched its CUF|ShieldPlus™ ceramic ultrafiltration module to tackle wastewater challenges in the semiconductor industry, a sector that demands extremely high water purity. Similarly, TAMI Industries announced a partnership in March 2025 to advance beer filtration efficiency using ceramic membranes, highlighting the technology’s penetration into the food and beverage segment. In February 2025, a Chinese chemical plant reported a 40% reduction in membrane replacement frequency after adopting ceramic flat sheet membranes, demonstrating tangible cost savings for industrial users.

Earlier developments underline the momentum of this market. In June 2024, Meiden Singapore partnered with PUB, Singapore’s National Water Agency, to integrate ceramic flat sheet membranes into desalination pre-treatment, emphasizing energy savings. In April 2024, QUA inaugurated a new membrane facility in Pune, India, significantly expanding production capacity for its EnviQ® flat sheet membranes. That same month, Nanostone Water and ENOWA (a NEOM subsidiary in Saudi Arabia) signed an MoU to deploy ceramic ultrafiltration for brine mining, advancing sustainable management of desalination by-products. These events collectively demonstrate how technological innovation, geographic expansion, and sustainability priorities are driving growth in the flat sheet membranes market.

Key Trends Shaping the Flat Sheet Membranes Market

The Flat Sheet Membranes Market is undergoing rapid transformation, driven by demand for sustainable water management, resilient material innovation, and cross-industry adoption. A notable trend is the accelerated adoption of flat sheet membranes in membrane bioreactor (MBR) systems for wastewater treatment. Flat sheet MBRs consistently achieve over 90% COD and TSS removal efficiency, making them the preferred choice for municipal projects under strict discharge regulations. A real-world case study from Shandong, China, demonstrated a 67% reduction in wastewater discharge at coal-fired power plants using flat sheet ultrafiltration systems, reflecting the global shift towards compliance with ecological standards.

In addition, industries are transitioning to advanced materials such as ceramics and high-performance polymers. A study from the Journal of Membrane Science highlighted that retrofitting polymeric systems with ceramic flat sheets at a 26.4 MGD water plant resulted in higher flux rates, reduced waste, and lower chemical maintenance validating ceramics as a long-term, low-maintenance alternative. Additionally, the expansion of flat sheet membranes into niche sectors like food, beverage, and biopharma is reshaping market dynamics. For example, Coca-Cola’s 2022 Belgium pilot program applied flat sheet ultrafiltration to selectively retain flavor compounds while cutting sugar content, showing how membranes can support regulatory incentives such as sugar taxes.

Further, the shift toward modular and decentralized treatment systems is expanding deployment flexibility. Companies like Meidensha Corporation are spearheading innovations in modular cassette designs that enhance scalability and energy efficiency, particularly for wastewater containing solvents, oils, and suspended solids.

Emerging Opportunities for Flat Sheet Membrane Adoption

The market presents lucrative opportunities that extend beyond traditional water and wastewater treatment. In the biopharmaceutical industry, rising global vaccine and monoclonal antibody production is fueling demand for flat sheet membranes as critical components in sterile, single-use downstream processing systems. This positions suppliers to capitalize on the industry’s growth in biologics manufacturing. Similarly, the food and beverage sector is adopting flat sheet membranes for selective separations that improve product quality while aligning with consumer trends toward healthier alternatives, creating opportunities for tailored membrane innovations.

Decentralized water solutions present another growth avenue, particularly in regions with infrastructure gaps or resource-scarce environments, where modular flat sheet systems can provide cost-effective and rapid deployment. The increasing push for advanced ceramic membranes also opens premium opportunities in industries requiring long-life, chemically resistant solutions where operational efficiency outweighs high initial costs. As governments and corporations intensify commitments to sustainability and circular economy models, flat sheet membranes are positioned as enablers of resource recovery, energy efficiency, and regulatory compliance, creating fertile ground for vendors who innovate around durability, modularity, and multi-sector applications.

Market Share Analysis of the Flat Sheet Membranes Market

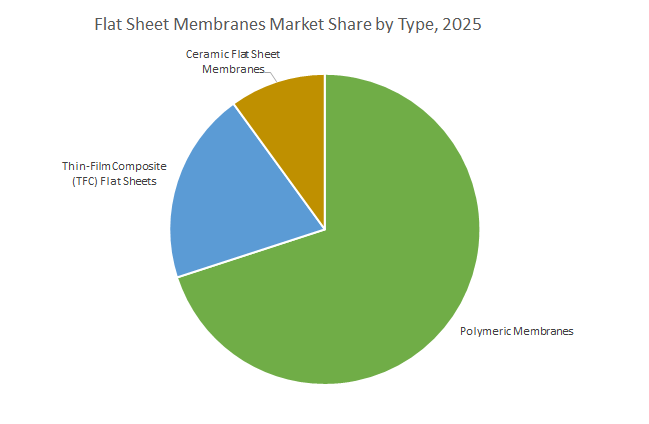

Market Share by Type: Polymeric Membranes Hold Dominance

By type, the polymeric flat sheet membranes segment commands nearly 70% of the market in 2025, reinforcing its role as the industry workhorse. Materials such as PES, PVDF, and PC dominate due to their versatility, affordability, and suitability for single-use bioprocessing systems, laboratory research, and medical devices. Their cost-effectiveness and disposability make them indispensable for applications demanding sterile and controlled environments. Thin-Film Composite (TFC) flat sheets, with an estimated 20% market share, play a strategic role in nanofiltration (NF) and reverse osmosis (RO), particularly in pharmaceutical and chemical feasibility studies where high selectivity is essential. Although ceramic flat sheet membranes account for only 10% of the market, they occupy a premium segment. Their exceptional resistance to chemical cleaning and ability to withstand harsh operating conditions make them highly attractive for industrial and bioprocessing environments, where durability and total cost-of-ownership are prioritized over upfront cost.

Market Share by Technology: Ultrafiltration Leads Bioprocessing Applications

When analyzed by technology, ultrafiltration (UF) dominates with 45% market share, underscoring its vital role in biopharmaceutical manufacturing processes such as protein concentration, buffer exchange, and diafiltration. The flat sheet format, particularly in disposable and reusable cassette systems, aligns seamlessly with industry requirements for efficiency and contamination prevention. Microfiltration (MF) follows with about 30% share, thriving in applications such as sterile filtration, cell harvest, and media clarification, especially in pharmaceutical and life sciences sectors. Nanofiltration (NF) and reverse osmosis (RO) represent 20% of the market, targeting specialized high-value separations, including ion removal and molecular purification in controlled laboratory settings before industrial scale-up. The remaining 5% under “Others” includes innovative approaches such as forward osmosis and membrane distillation, both of which are primarily researched using flat sheet configurations, reflecting the segment’s importance in early-stage technology development and pilot testing.

Market Share by Application: Bioprocessing & Pharmaceuticals Drive the Core Market

By application, bioprocessing and pharmaceutical manufacturing hold a commanding 50% market share, making it the most significant demand driver. Flat sheet membranes are central to downstream processing in the production of vaccines, monoclonal antibodies, and biologics, where sterile, disposable cassette systems accelerate throughput and minimize contamination risk. The laboratory and research use segment accounts for around 25%, highlighting its critical role in process innovation, membrane material testing, and feasibility studies that feed advancements across other applications. Industrial process separation contributes 15%, largely in specialized fields such as food & beverage product development and fine chemical manufacturing, where flexibility and scalability are valued. Meanwhile, medical device applications represent 5%, reflecting demand for flat sheets in diagnostic assays and selective blood filtration devices, where precision and reliability are non-negotiable. The remaining 5% share belongs to water and wastewater treatment, where flat sheet configurations are less economical for large-scale plants compared to spiral-wound modules but remain relevant for packaged systems and pilot-scale testing.

China: Expanding Industrial MBRs and Regulatory Compliance

China’s flat sheet membranes market is witnessing significant growth, driven by stringent industrial wastewater regulations and increasing adoption of advanced membrane bioreactors (MBRs). The Ministry of Ecology and Environment (MEE) enforces strict discharge standards, compelling industries to deploy flat sheet MBRs to meet environmental requirements. Technological innovations, such as hollow-fiber ultrafiltration membranes with enhanced antifouling properties developed in 2024, are improving efficiency and reducing maintenance costs in municipal and industrial applications. China’s expanding industrial wastewater and municipal treatment sectors are leveraging flat sheet membranes to address water scarcity and pollution, while domestic production expansions contribute to competitive pricing and wider market accessibility.

United States: Government Support and Technological Innovation

In the United States, government funding and academic R&D are propelling the adoption of flat sheet membrane technologies. Under the Bipartisan Infrastructure Law, over $50 billion is allocated to the EPA to enhance water infrastructure and address emerging contaminants like PFAS, emphasizing the need for advanced flat sheet filtration solutions. NSF-funded research centers are pioneering innovations in water purification, chemical separations, and biopharmaceutical processing. Corporate leaders such as DuPont Water Solutions and Solventum are developing new flat sheet membranes for industrial water filtration and biopharmaceutical applications. Projects like the Gillette, Wyoming, membrane-based carbon capture plant demonstrate broader deployment of advanced membrane solutions, highlighting the strategic importance of flat sheet technologies.

India: Green Bonds and Large-Scale MBR Deployments

India’s flat sheet membranes market is fueled by government initiatives and infrastructure investments. The “Jal Jeevan Mission” and the Department of Science & Technology’s Water Technology Initiative promote R&D in nano-material and filtration technologies to provide safe drinking water. The issuance of India’s first Certified Green Municipal Bond by Ghaziabad Nagar Nigam raised ₹150 crore for a Tertiary Sewage Treatment Plant (TSTP) utilizing flat sheet membranes for industrial wastewater reuse. Additionally, VA TECH WABAG’s seven-year O&M contract for the 110 MLD SWRO Nemmeli Desalination Plant, valued at INR 415 crores, underscores the growing financial commitment to large-scale flat sheet membrane infrastructure.

Germany: Industrial Excellence and Global Ceramic Membrane Projects

Germany is a global leader in industrial wastewater treatment using flat sheet membranes. PWT Wassertechnik applies flat sheet filtration in industrial water reuse, ensuring strict compliance with European environmental regulations. CERAFILTEC’s 2024 announcement to supply ceramic flat membranes for MBR projects across four continents highlights the international adoption of German membrane technology. Companies like MANN+HUMMEL are also developing innovative membrane and digital solutions for industrial process optimization and green energy applications, reinforcing Germany’s position as a key hub for advanced flat sheet membrane technologies.

Japan: Academic Innovation and Widespread MBR Applications

Japan is at the forefront of flat sheet membrane R&D, combining academic research with corporate innovation. Studies from Kobe University in 2024 focus on novel functional membranes, including biomimetic and highly porous designs. Metawater’s ceramic flat-sheet membranes are applied to public and industrial plants for efficient tap water production and wastewater recycling. With over 3,000 full-scale MBR applications, Japan demonstrates broad operational experience, including the use of Meidensha Corporation membranes for petrochemical wastewater recycling, highlighting the country’s long-standing expertise in membrane-based water treatment solutions.

Australia: Advanced Water Recycling and Ceramic Flat-Sheet Innovation

Australia’s flat sheet membranes market is driven by water stress, recycling initiatives, and technological advancements. The Australian Water Recycling Centre of Excellence has funded projects demonstrating the benefits of ceramic flat-sheet membranes for treating high-organic secondary effluent. Narromine Shire Council in NSW installed next-generation submerged flat-sheet ceramic membranes from Cerafiltec, marking a first-of-its-kind deployment in the country. Academic research at Victoria University’s ISILC focuses on increasing water recovery from desalination and reducing membrane fouling and scaling, addressing critical challenges in the performance and efficiency of flat sheet membrane systems.

Competitive Landscape: Global Leaders in Flat Sheet Membrane Innovation

The flat sheet membranes market is shaped by leading technology providers and specialists that focus on durability, application-specific performance, and sustainability. Key players such as Meidensha Corporation, LiqTech International, TAMI Industries, QUA Water Technologies, Cembrane (Ovivo), and Jiuwu Hi-Tech are investing heavily in ceramic membrane innovations, advanced materials, and global production expansions. Their strategies center on enabling utilities and industries to achieve higher water quality at lower lifecycle costs, while scaling solutions to urban and industrial demands.

Meidensha Corporation – Expanding Ceramic Membrane Footprint in Singapore

Meidensha has established itself as a leader in ceramic flat sheet membranes, with Singapore serving as its global hub for R&D and project deployments. Its collaboration with PUB (Singapore’s National Water Agency) has resulted in pioneering projects, including the Chestnut Avenue Waterworks, set to become the world’s largest ceramic flat sheet membrane filtration plant for drinking water. In June 2025, the company also began implementing a large-scale demonstration plant for SWRO pre-treatment, designed to improve desalination energy efficiency. Meidensha’s membranes, made from durable alumina, offer high resistance to chemicals and long lifespans, enabling customers to achieve cost-effective operations.

LiqTech International – Strength in Silicon Carbide (SiC) Membranes

LiqTech International is a recognized leader in silicon carbide (SiC) membranes, known for their superior mechanical and chemical durability. The company is diversifying beyond marine and oil & gas into new industries, such as steelmaking, with a recent U.S. project targeting oily wastewater treatment. In Q2 2025, LiqTech reported an 11% revenue increase, driven by demand for liquid filtration systems and pool membranes. Management expects 2025 to deliver the company’s strongest revenue in four years, signaling strong momentum. With SiC’s unique advantages, LiqTech is well-positioned for growth in harsh industrial wastewater applications.

TAMI Industries – Ceramic Expertise for Biopharma and Food Applications

TAMI Industries specializes in tangential flow filtration and ceramic flat sheet membranes, with strong penetration in biopharma and food & beverage industries. Its membranes are widely used in applications such as beer clarification, wine filtration, and whey protein concentration. In March 2025, the company announced a partnership to advance beer filtration efficiency, showcasing its application-specific innovation. With a broad product portfolio covering ultrafiltration and microfiltration porosities, TAMI delivers tailored solutions while maintaining a focus on eco-efficient ceramic membranes.

QUA Water Technologies – Scaling Production with EnviQ® Membranes

A subsidiary of Aquatech, QUA Water Technologies has expanded aggressively to meet growing demand. In April 2024, it inaugurated a state-of-the-art membrane facility in Pune, India, quadrupling production capacity. Its flagship EnviQ® flat sheet membranes are widely used in MBR systems for municipal and industrial wastewater treatment. The facility itself features a zero-discharge solution, aligning with QUA’s sustainability goals. With its application expertise in wastewater reuse and a growing global presence, QUA is becoming a significant challenger in the flat sheet membrane space.

Cembrane A/S (Ovivo) – Global Reach with SiC Membrane Technology

Cembrane, acquired by Ovivo in November 2021, is recognized for its patented silicon carbide (SiC) flat sheet membranes. The technology’s anti-fouling properties and durability have made it popular in over 450 installations across 65 countries, covering municipal, industrial, and drinking water projects. The Ovivo acquisition has expanded Cembrane’s reach, enabling it to integrate into comprehensive water solutions worldwide. With strong partnerships and proven global performance, Cembrane is a key player driving the commercialization of SiC membranes for resilient water treatment.

Jiuwu Hi-Tech Co., Ltd. – Material Innovation and Design Excellence

Jiuwu Hi-Tech has built its reputation on advanced material science, delivering flat sheet membranes with greater chemical resistance and fouling resistance than conventional designs. Its membrane modules are engineered to optimize flow dynamics and flux distribution, reducing fouling risks and improving operational performance. Jiuwu’s membranes are deployed across water and wastewater treatment, pharmaceuticals, and food & beverage processing, highlighting their versatility. The company’s consistent investment in R&D and innovative designs demonstrates its ambition to maintain leadership in the next generation of flat sheet membrane technologies.

Flat Sheet Membranes Market Report Scope

Flat Sheet Membranes Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.1 Billion

|

|

Market Size (2034)

|

$2.2 Billion

|

|

Market Growth Rate

|

8.2%

|

|

Segments

|

By Type (Polymeric Membranes, Ceramic Flat Sheet Membranes, Thin-Film Composite (TFC) Flat Sheets), By Technology (Microfiltration, Ultrafiltration, Nanofiltration and Reverse Osmosis), By Application (Bioprocessing & Pharmaceutical Manufacturing, Laboratory & Research Use, Industrial Process Separation, Medical Devices, Water & Wastewater Treatment)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

DuPont de Nemours, Inc., SUEZ, Veolia, Toray Industries, Inc., Pentair plc, Xylem Inc., Asahi Kasei Corporation, Kubota Corporation, The Dow Chemical Company, MANN+HUMMEL, Evoqua Water Technologies, LG Chem, Koch Industries, Alfa Laval, Meidensha Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Flat Sheet Membranes Market Segmentation

By Type

- Polymeric Membranes

- Polyethersulfone

- Polyvinylidene Fluoride

- Polysulfone

- Cellulose-Based

- Polyamide, Polypropylene, Polyethylene

- Ceramic Flat Sheet Membranes

- Thin-Film Composite (TFC) Flat Sheets

By Technology

- Microfiltration

- Ultrafiltration

- Nanofiltration and Reverse Osmosis

By Application

- Bioprocessing & Pharmaceutical Manufacturing

- Laboratory & Research Use

- Industrial Process Separation

- Medical Devices

- Water & Wastewater Treatment

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Flat Sheet Membranes Industry include-

- DuPont de Nemours, Inc.

- SUEZ

- Veolia

- Toray Industries, Inc.

- Pentair plc

- Xylem Inc.

- Asahi Kasei Corporation

- Kubota Corporation

- The Dow Chemical Company

- MANN+HUMMEL

- Evoqua Water Technologies

- LG Chem

- Koch Industries

- Alfa Laval

- Meidensha Corporation

*- List not Exhaustive

Research Coverage

This report investigates how flat sheet membranes are scaling from MBR-centric wastewater reuse to high-spec bioprocessing and industrial separations; the analysis reviews durability economics versus hollow fiber and spiral-wound formats, quantifies fouling resilience and cleaning cadence, and highlights vendor moves (capacity adds, ceramic advances, modular cassettes) shaping total cost of ownership. Building on validated project data and recent demonstrations in SWRO pre-treatment and semiconductor wastewater, this report is an essential resource for utilities, EPCs, plant owners, membrane OEMs, and process engineers making capex/opex tradeoffs. Developed by USDAnalytics, the study benchmarks performance under oils/solvents/high TSS, codifies retrofit pathways for space-constrained sites, and maps opportunity hot-spots across biopharma, F&B, and decentralized reuse. Scope Includes-

- Segmentation – By Type: Polymeric Membranes (Polyethersulfone; Polyvinylidene Fluoride; Polysulfone; Cellulose-Based; Polyamide/Polypropylene/Polyethylene); Ceramic Flat Sheet Membranes; Thin-Film Composite (TFC) Flat Sheets | By Technology: Microfiltration; Ultrafiltration; Nanofiltration and Reverse Osmosis | By Application: Bioprocessing & Pharmaceutical Manufacturing; Laboratory & Research Use; Industrial Process Separation; Medical Devices; Water & Wastewater Treatment

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Timeframe: Historic 2021–2024; Forecast 2025–2034.

- Companies (15+ profiled/benchmarked): DuPont de Nemours, Inc.; SUEZ; Veolia; Toray Industries, Inc.; Pentair plc; Xylem Inc.; Asahi Kasei Corporation; Kubota Corporation; The Dow Chemical Company; MANN+HUMMEL; Evoqua Water Technologies; LG Chem; Koch Industries; Alfa Laval; Meidensha Corporation

Methodology

USDAnalytics employed a mixed-method framework: top-down sizing from end-market capex (municipal, industrial, bioprocessing) and announced line-item projects; bottom-up bill-of-materials and process models at module/cassette level (flux, TMP, permeability recovery, CIP/SIP cycles, energy kWh/m³) to derive $/1,000 m³ treated; primary interviews with operators/EPCs to validate duty conditions and cleaning windows; competitive benchmarking of polymeric vs. ceramic flat sheets on integrity, chemical tolerance, and warranty terms; scenario analysis for ceramic cost learning, supply risk, and regulatory tightening; and multi-source triangulation (pilots, commissioning data, audited disclosures) to produce reproducible country/segment forecasts through 2034.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Flat Sheet Membranes Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Insights for Stakeholders

1.3. Global Market Snapshot

2. Flat Sheet Membranes Market Outlook (2025–2034)

2.1. Introduction: Growth Drivers and Industry Transformation

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $1.1 Billion

2.2.2. Forecasted Market Size (2034): $2.2 Billion

2.2.3. Projected Compound Annual Growth Rate (CAGR): 8.2%

2.3. Key Trends and Opportunities

2.3.1. Accelerated Adoption in Membrane Bioreactor (MBR) Systems

2.3.2. Transition to Advanced Materials (Ceramics and High-Performance Polymers)

2.3.3. Expansion into Niche Sectors (Food, Beverage, and Biopharma)

2.3.4. Shift to Modular and Decentralized Treatment Systems

2.4. Emerging Opportunities for Adoption

2.4.1. Biopharmaceutical Industry: Single-Use Systems

2.4.2. Food & Beverage Sector: Selective Separations

2.4.3. Decentralized Water Solutions

2.4.4. Advanced Ceramic Membranes for Premium Applications

3. Recent Developments and Strategic Shifts

3.1. Market Analysis: Recent News and Technological Developments

3.1.1. Nanostone Water and Solecta Merge to Form Acuriant Technologies

3.1.2. Meiden Singapore Initiates Large-Scale SWRO Pre-treatment Demonstration

3.1.3. Nanostone Water Launches CUF|ShieldPlus™ Ceramic Module

3.1.4. TAMI Industries Partners to Advance Beer Filtration

3.1.5. Chinese Chemical Plant Adopts Ceramic Flat Sheet Membranes

3.1.6. QUA Inaugurates New Membrane Manufacturing Facility in India

3.1.7. Nanostone Water and ENOWA Sign MoU for Brine Mining

4. Competitive Landscape: Leading Companies

4.1. Market Overview: From Material Specialists to Global Solution Providers

4.2. Key Competitive Factors

4.2.1. Durability and Operational Resilience

4.2.2. Application-Specific Performance

4.2.3. Focus on Sustainability and Lower Lifecycle Costs

4.3. Profiles of Top Players

4.3.1. Meidensha Corporation

4.3.2. LiqTech International

4.3.3. TAMI Industries

4.3.4. QUA Water Technologies

4.3.5. Cembrane A/S (Ovivo)

4.3.6. Jiuwu Hi-Tech Co., Ltd.

5. Flat Sheet Membranes Market – Segmentation Insights

5.1. By Type

5.1.1. Polymeric Membranes

5.1.2. Ceramic Flat Sheet Membranes

5.1.3. Thin-Film Composite (TFC) Flat Sheets

5.2. By Technology

5.2.1. Microfiltration (MF)

5.2.2. Ultrafiltration (UF)

5.2.3. Nanofiltration (NF) and Reverse Osmosis (RO)

5.3. By Application

5.3.1. Bioprocessing & Pharmaceutical Manufacturing

5.3.2. Laboratory & Research Use

5.3.3. Industrial Process Separation

5.3.4. Medical Devices

5.3.5. Water & Wastewater Treatment

6. Country Analysis and Outlook: Flat Sheet Membranes Market

6.1. China: Expanding Industrial MBRs and Regulatory Compliance

6.2. United States: Government Support and Technological Innovation

6.3. India: Green Bonds and Large-Scale MBR Deployments

6.4. Germany: Industrial Excellence and Global Ceramic Membrane Projects

6.5. Japan: Academic Innovation and Widespread MBR Applications

6.6. Australia: Advanced Water Recycling and Ceramic Flat-Sheet Innovation

6.7. Other Key Countries

6.7.1. North America (Canada, Mexico)

6.7.2. Europe (UK, France, Spain, Italy, Russia, Rest of Europe)

6.7.3. Asia Pacific (South Korea, South East Asia, Rest of Asia)

6.7.4. South America (Brazil, Argentina, Rest of South America)

6.7.5. Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

7. Flat Sheet Membranes Market Size Outlook by Region (2025-2034)

7.1. North America Market Size Outlook to 2034

7.1.1. By Type

7.1.2. By Technology

7.1.3. By Application

7.2. Europe Market Size Outlook to 2034

7.2.1. By Type

7.2.2. By Technology

7.2.3. By Application

7.3. Asia Pacific Market Size Outlook to 2034

7.3.1. By Type

7.3.2. By Technology

7.3.3. By Application

7.4. South America Market Size Outlook to 2034

7.4.1. By Type

7.4.2. By Technology

7.4.3. By Application

7.5. Middle East and Africa Market Size Outlook to 2034

7.5.1. By Type

7.5.2. By Technology

7.5.3. By Application

8. Company Profiles: Additional Leading Players

8.1. DuPont de Nemours, Inc.

8.2. SUEZ

8.3. Veolia

8.4. Toray Industries, Inc.

8.5. Pentair plc

8.6. Xylem Inc.

8.7. Asahi Kasei Corporation

8.8. Kubota Corporation

8.9. The Dow Chemical Company

8.10. MANN+HUMMEL

8.11. Evoqua Water Technologies

8.12. LG Chem

8.13. Koch Industries

8.14. Alfa Laval

8.15. Meidensha Corporation

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures