Global Liquid Filtration Market Overview and Key Industry Statistics

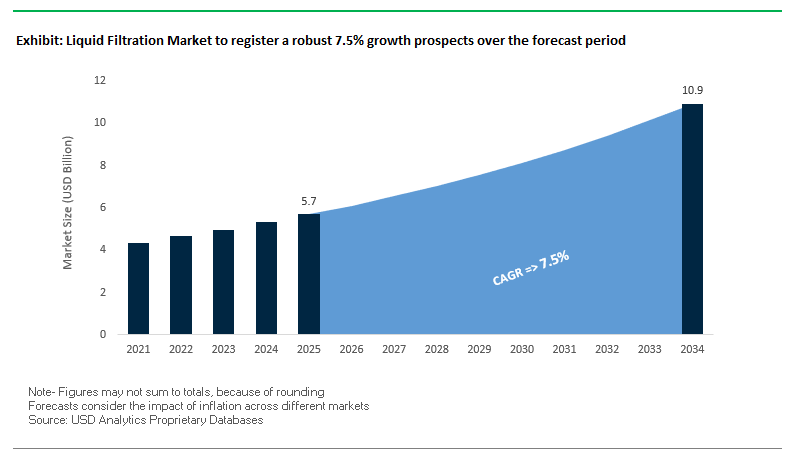

The global Liquid Filtration Market is projected to reach USD 10.9 billion by 2034, growing from USD 5.7 billion in 2025, at a steady CAGR of 7.5%. This expansion is driven by rising demand across industries such as pharmaceuticals, biotechnology, water treatment, and high-purity manufacturing. Increasing regulatory mandates, coupled with rapid technological adoption, are reshaping the market into a hub of innovation where sustainability, digitalization, and performance efficiency are critical.

Industry professionals evaluating this market should focus on three critical dynamics: (1) the regulatory landscape that directly influences demand, (2) the growing significance of high-purity requirements in life sciences and semiconductor industries, and (3) the disruptive integration of AI, IoT, and smart filtration technologies. These aspects will be decisive in determining market entry strategies, vendor partnerships, and long-term investments.

Key Insights for professionals

- Regulatory Impact: In 2024, the U.S. EPA launched a USD 1.2 billion water infrastructure improvement program, fueling immediate demand for advanced municipal and industrial liquid filtration systems.

- Pharma & Biotech Growth: The UK pharmaceutical sector allocated 18% of total business R&D spending to pharma in 2024, highlighting the sector’s increasing reliance on high-purity liquid filtration solutions.

- Smart Filtration Revolution: Adoption of IoT and AI-based monitoring reduces operational downtime by up to 20%, giving end-users measurable ROI advantages.

- Membrane Filtration Rise: Ultrafiltration and nanofiltration technologies are displacing conventional systems in high-specification industries due to their ability to remove ultra-fine contaminants.

Market Analysis and Recent Industry Developments

The liquid filtration industry is undergoing structural changes fueled by sustainability commitments, investments in advanced infrastructure, and high-profile corporate activities. Companies are restructuring portfolios, investing in low-carbon technologies, and pursuing acquisitions to strengthen their competitive edge. This indicates that the industry is not only expanding in size but also evolving in scope and sophistication, with stakeholders prioritizing circular economy principles and digital solutions.

In August 2025, a flurry of activities reshaped the global landscape. Ball Corporation divested a 41% stake in its Saudi Arabian joint venture, while Crown Holdings validated its net-zero target through SBTi, highlighting a strong ESG-driven strategy. Similarly, Novelis and DRT Holdings signed a joint development agreement to accelerate recycled alloys, while Golden Aluminum started up a next-gen strip caster in Colorado, enhancing operational efficiency. Can-Pack S.A. launched an ultra-lightweight aluminum can design, marking material innovation as a core theme, and Century Aluminum committed USD 50 million to restart smelter operations in South Carolina to expand U.S. domestic supply. These moves collectively reflect the sector’s pivot toward resource efficiency, sustainability, and regional resilience.

Earlier in February 2025, Ball Corporation acquired Florida Can Manufacturing, strengthening its North American supply chain, while in October 2024, Silgan Holdings completed the acquisition of Weener Plastics, enhancing its dispensing and closures segment. These acquisitions underline a strategic consolidation trend, where global leaders are integrating vertically and horizontally to fortify their supply chain control, improve margins, and expand specialized product portfolios. Such ongoing developments illustrate a market environment where M&A, sustainability, and advanced technologies are interlinked growth drivers.

Key Trends and Strategic Growth Opportunities in the Liquid Filtration Market

Strategic Shift to Advanced Hollow-Fiber Membranes for Biopharmaceutical Processing

The liquid filtration market is witnessing a pronounced shift toward advanced hollow-fiber membranes, particularly driven by the biopharmaceutical sector's rapid expansion in biologics, cell, and gene therapies (CGT). Hollow-fiber cartridges, a type of tangential flow filtration (TFF) system, offer extremely high surface area in compact modules, enabling efficient separation and concentration of proteins and biomolecules, which significantly increases product yield and reduces costly losses. This technology minimizes shear stress on sensitive cells and large biomolecules, maintaining their viability and potency—an essential factor for complex therapies. Hollow-fiber systems are highly scalable, supporting a seamless transition from lab-scale development to commercial manufacturing without changing the filtration platform. Additionally, single-use disposable hollow-fiber cartridges align with aseptic processing trends, reducing cross-contamination risks and cleaning requirements. These advantages make hollow-fiber membranes a core enabler for high-purity filtration in modern biopharmaceutical production.

Deployment of Ceramic Membranes for Harsh Industrial Wastewater Treatment

Industrial wastewater treatment is driving the adoption of ceramic membranes due to their chemical and thermal resilience, long operational life, and fouling resistance. Ceramic membranes, composed of alumina or silicon carbide, can withstand extreme pH ranges (0–14) and temperatures up to 800°C, making them ideal for harsh applications such as metal finishing, chemical production, and landfill leachate treatment. Their durability extends membrane lifespan, reducing replacement frequency and overall cost of ownership. The hydrophilic surface resists organic and biological fouling, maintaining high flux over prolonged operation, critical for continuous industrial processes. Case studies highlight their deployment in oily wastewater treatment, where robustness against corrosive cleaning agents allowed substantial water reuse while complying with strict discharge regulations. The combination of resilience, longevity, and high performance positions ceramic membranes as an increasingly preferred solution for industrial wastewater filtration.

Development of PFAS-Specific Selective Filtration Media

The rise of PFAS (per- and polyfluoroalkyl substances) contamination presents a pressing environmental challenge, creating demand for highly selective filtration solutions. Traditional media like granular activated carbon (GAC) and ion exchange resins are inefficient and quickly saturated when removing PFAS. Molecularly imprinted polymers (MIPs) are being developed to offer “lock-and-key” specificity for PFAS molecules, providing higher removal efficiency and longer filter life. Advanced regenerable adsorbents allow on-site regeneration, reducing disposal costs and environmental impact. Regulatory pressures, such as the U.S. EPA’s proposed drinking water standards for PFAS, accelerate market adoption and incentivize R&D investment in novel selective filtration media. This opportunity is particularly relevant for municipal water treatment facilities and industrial operators seeking compliance while minimizing operational costs.

Membrane-Based Lithium Extraction for Direct Lithium Brine Extraction (DLE)

The surging demand for lithium to support the global electric vehicle (EV) transition has opened a strategic opportunity for membrane-based Direct Lithium Extraction (DLE). Traditional evaporation ponds are slow, land-intensive, and environmentally taxing. Nanofiltration (NF) and selective electrodialysis membranes enable faster, more sustainable, and higher-yield lithium extraction from brines. Membrane-based DLE significantly reduces water use and shortens extraction timelines from months or years to hours or days. High-selectivity membranes effectively separate lithium ions from magnesium, sodium, and other brine impurities, producing high-purity lithium carbonate efficiently. Furthermore, this approach allows extraction from previously uneconomical sources such as geothermal brines and oilfield wastewater, expanding the global lithium supply base. Membrane-based DLE not only addresses sustainability and energy efficiency concerns but also strengthens the resilience and diversity of the lithium supply chain.

Competitive Landscape of the Global Liquid Filtration Industry

The competitive landscape of the liquid filtration market is defined by leading global players that are leveraging innovation, acquisitions, and sustainability as their key differentiators. Companies such as SUEZ, Evoqua, MANN+HUMMEL, Pall Corporation, and Donaldson Company are shaping market evolution by investing in digital solutions, advanced membranes, and green technologies. Each competitor brings unique strengths, ranging from life sciences expertise to municipal infrastructure dominance, making the sector highly diversified and innovation-driven.

SUEZ Water Technologies & Solutions: Driving Circular Economy in Filtration

SUEZ offers a robust portfolio covering membrane filtration, ion exchange, and biological treatment systems for industrial and municipal needs. Its energy-positive treatment plant in Nice, France, capable of generating four times more energy than it consumes, is a benchmark in sustainable infrastructure. SUEZ is investing heavily in digital solutions, AI, and data analytics to optimize client systems and has announced a 50% increase in R&D budget by 2027, reinforcing its innovation-driven roadmap. With over 260 desalination plants and multiple reuse projects, SUEZ is well-positioned to address water scarcity and climate resilience challenges.

Evoqua Water Technologies: Strengthening Life Sciences with High-Purity Solutions

Evoqua has built a strong reputation in healthcare and life sciences filtration through its acquisition of Mar Cor, expanding its North American service footprint. Its service-led model integrates digital water management and predictive analytics, offering clients higher uptime and cost efficiency. Evoqua’s strategy revolves around sustainability, innovation, and proactive contaminant removal (including PFAS and microplastics). Its strong foothold in high-specification markets gives it an edge in serving industries where water quality is mission-critical.

MANN+HUMMEL: Innovating with Sustainable and Digital Filtration Solutions

MANN+HUMMEL combines air and liquid filtration expertise, with solutions spanning automotive, industrial, and municipal sectors. In 2024, it introduced plant-based and CO2-reduced filter products, reducing emissions by 3.93 tons of CO2 annually per product line. Its strategic goal to achieve 100% renewable energy by 2025, coupled with STREAMETRIC digital monitoring solutions, reflects its dual focus on sustainability and smart filtration. MANN+HUMMEL’s portfolio supports both industrial wastewater treatment and oil & gas filtration, giving it a broad and balanced customer base.

Pall Corporation: Expanding Advanced Filtration for High-Tech Industries

As part of Danaher Corporation, Pall delivers liquid filtration for life sciences, microelectronics, and food & beverage industries. Its USD 150 million Singapore manufacturing facility (opened June 2024) is dedicated to supporting the semiconductor industry, an area with growing demand for ultra-pure water. By aligning R&D with global semiconductor and pharma needs, Pall demonstrates its ability to integrate filtration with advanced manufacturing ecosystems. With 300 new jobs created in Asia, Pall strengthens its global operational footprint while reinforcing its role as a partner for high-purity applications.

Donaldson Company, Inc.: Expanding with Technology-Led Growth and Life Sciences

Donaldson is a recognized leader in industrial and engine filtration with a diversified business portfolio. In June 2025, it reinforced its life sciences strategy, allocating USD 1.4 billion across three years for acquisitions and technology upgrades. Its vision, “Filtration for a Thriving Future,” is being realized through digitalization of dust collection systems and an expanded global presence, with 65 manufacturing plants worldwide. Donaldson’s balanced exposure across agriculture, construction, and life sciences allows it to maintain growth even during sectoral downturns, strengthening its resilience and shareholder value proposition.

Liquid Filtration Market Share Insights

Non-Woven Media Hold Market Share Leadership by Filter Media in the Liquid Filtration Industry

Non-woven filter media dominate the liquid filtration industry with a commanding 58% market share in 2025, cementing their position as the backbone of global filtration solutions. Their randomly oriented fiber matrix enables depth filtration, providing high dirt-holding capacity, superior retention efficiency, and longer service life compared to woven or mesh media. Non-wovens are indispensable in bag filters, cartridge filters, and pre-filtration stages across industries ranging from pharmaceuticals and food & beverage to chemicals, metals, and mining, making them the most versatile and widely adopted medium. Woven media sustain a meaningful share by offering high mechanical strength, durability, and reusability, particularly in dewatering, belt filters, and high-flow processes where surface filtration is more efficient. Mesh media, though the smallest contributor, remain critical in high-precision applications, offering absolute pore size control and structural integrity in high-pressure or high-temperature conditions. This segmentation underscores how non-woven media drive mainstream adoption, while woven and mesh solutions secure niche roles in heavy-duty and precision environments.

Industrial Treatment Dominates Market Share by End-User in the Liquid Filtration Industry

Industrial treatment commands 65% of the global liquid filtration market in 2025, reflecting its central role in ensuring compliance, efficiency, and water reuse across complex industrial processes. Industries such as power generation, petrochemicals, pharmaceuticals, food and beverage, and mining generate diverse and challenging effluents that require customized filtration solutions to protect equipment and meet stringent environmental regulations. The need for robust filtration systems that balance operational efficiency, sustainability, and cost control secures this segment’s dominance. Municipal treatment, while representing a smaller share of revenue, accounts for vast processing volumes in potable water production and wastewater treatment. Population growth in developing countries and infrastructure modernization in developed regions continue to drive steady investment in large-scale municipal systems, where filtration technologies must prioritize reliability, scalability, and affordability. Together, these dynamics demonstrate that industrial treatment drives revenue through complexity and compliance, while municipal applications anchor high-volume, society-critical demand.

United States Liquid Filtration Market Driven by Advanced Membrane Technologies and Regulatory Compliance

The U.S. liquid filtration market is strongly influenced by stringent Environmental Protection Agency (EPA) regulations and state-level air and water quality boards, with the Safe Drinking Water Act (SDWA) and Clean Water Act (CWA) driving demand for advanced filtration solutions across municipal and industrial sectors. Investments in manufacturing facilities and adherence to pollution control norms are key growth drivers, particularly in sectors requiring high-purity water such as pharmaceuticals, healthcare, and food and beverage production.

Technological advancements such as nanofiltration, ultrafiltration, and real-time digital monitoring systems are enabling predictive maintenance, reducing downtime, and ensuring superior system reliability. Corporate investments are robust, exemplified by Pall Corporation’s expansion in semiconductor-grade liquid filtration, reflecting the critical role of filtration in contamination-sensitive applications. Government and industrial initiatives, including infrastructure upgrades and manufacturing reshoring, further fuel demand, particularly in automotive and chemical industries where high-quality liquid filtration solutions are essential.

Germany Strengthens Liquid Filtration Market With High-Performance Systems and Circular Economy Initiatives

Germany’s liquid filtration market operates under stringent EU water directives and well-established industrial standards, fostering demand for high-performance, eco-friendly filtration solutions. The country is recognized for its technological innovation in filter media, membranes, and system design, providing extended lifespan, enhanced efficiency, and low-maintenance solutions across industrial applications.

Germany’s commitment to the circular economy and sustainable manufacturing drives the development of advanced wastewater treatment and resource recovery systems. Corporate investments are significant, with companies focusing on pharmaceutical and food and beverage sectors, expanding their capabilities to meet growing demand for high-quality, environmentally sustainable filtration technologies.

China Liquid Filtration Market Expands With Environmental Policies and Industrial Modernization

China’s liquid filtration market is supported by government initiatives targeting environmental protection and industrial modernization, including the dual carbon goal and the Action Plan for Promoting Large-Scale Equipment Updates. Regulatory reforms, such as NSF P535, establish minimum requirements for point-of-use water filters, driving adoption of high-performance, safe filtration solutions.

Technological investments, including automation, AI, and large-scale water treatment plant projects, enhance production efficiency and meet growing demand from urban and industrial sectors. Partnerships, like Xiniupi Waterproof Technology collaborating with European firms, showcase innovation in membrane systems. The emphasis on domestic manufacturing and high-quality circular solutions positions China as a key driver in the liquid filtration industry, particularly for municipal, industrial, and environmental water treatment applications.

India Liquid Filtration Market Gains Momentum From Jal Jeevan Mission and Industrial Growth

India’s liquid filtration industry is receiving a significant boost from the Jal Jeevan Mission, aimed at providing safe tap water to all rural households, supported by a ₹67,000 crore budget allocation. The focus on municipal water treatment is complemented by the growing demand in industrial and urban sectors.

Advanced filtration technologies, such as membrane filtration, are being increasingly adopted to ensure high-quality water across food and beverage, pharmaceutical, and e-commerce sectors. Corporate investments are rising, supported by the expansion of local production facilities to meet domestic demand. The growing exports of industrial products, particularly pharmaceuticals, drive the need for modern, high-performance liquid filtration solutions that comply with international standards.

Japan Liquid Filtration Market Advances With Precision Membranes and Specialized Filtration Solutions

Japan’s liquid filtration market benefits from the country’s precision manufacturing capabilities and strong regulatory emphasis on wastewater management and industrial emissions control. Companies such as Toray Industries are leading in advanced membrane design for wastewater reuse, optimizing both environmental sustainability and industrial efficiency.

The market focuses on specialty and high-performance filtration systems for sectors like electronics, automotive, and high-tech manufacturing. Innovations such as self-cleaning filters and multi-barrier contaminant removal technologies, exemplified by Hitachi Zosen’s installations, cater to the specific needs of industrial and municipal applications, ensuring superior water purity and compliance with stringent Japanese standards.

Brazil Liquid Filtration Market Grows With Water Reuse Innovations and Sustainable Sanitation Practices

Brazil’s liquid filtration industry is shaped by the National Solid Waste Policy, promoting sustainable water management and eco-friendly filtration solutions over a 20-year horizon. The sanitation sector is embracing innovative technologies, including membrane bioreactors and reverse osmosis, with projects like Veolia’s facility in Vitória, the world’s first municipal wastewater-to-reuse plant, setting a benchmark.

Demand is particularly high in industrial and agricultural sectors, as well as new construction and renovation projects. Corporate investments, supported by the EU-Mercosur trade agreement, are attracting both domestic and international players, driving diversification and enhancing Brazil’s position in the high-performance liquid filtration market.

Liquid Filtration Market Report Scope

Liquid Filtration Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.7 Billion

|

|

Market Size (2034)

|

$10.9 Billion

|

|

Market Growth Rate

|

7.5%

|

|

Segments

|

By Filter Media (Woven, Non-woven, Mesh), By Fabric Material Type (Polymer, Cotton, Aramid, Metal, Others), By End-User (Industrial Treatment, Municipal Treatment), By Technology (Mechanical Filtration, Membrane Filtration, Activated Carbon Filters, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Pall Corporation, Eaton Corporation, SUEZ, Veolia Environnement S.A., Donaldson Company, Inc., 3M Company, Parker Hannifin Corporation, Alfa Laval AB, MANN+HUMMEL Group, Lydall, Inc., Pentair plc, Ahlstrom-Munksjö Oyj, Cummins Inc., Freudenberg Filtration Technologies SE & Co. KG, Merck KGaA

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Liquid Filtration Market Segmentation

By Filter Media

By Fabric Material Type

- Polymer

- Cotton

- Aramid

- Metal

- Others

By End-User

- Industrial Treatment

- Municipal Treatment

By Technology

- Mechanical Filtration

- Membrane Filtration

- Activated Carbon Filters

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Liquid Filtration Market

- Pall Corporation

- Eaton Corporation

- SUEZ

- Veolia Environnement S.A.

- Donaldson Company, Inc.

- 3M Company

- Parker Hannifin Corporation

- Alfa Laval AB

- MANN+HUMMEL Group

- Lydall, Inc.

- Pentair plc

- Ahlstrom-Munksjö Oyj

- Cummins Inc.

- Freudenberg Filtration Technologies SE & Co. KG

- Merck KGaA

* List Not Exhaustive

Methodology

The research methodology for the Liquid Filtration Market conducted by USDAnalytics combines rigorous primary and secondary research to provide actionable insights for industry professionals. Primary research included interviews with filtration system manufacturers, industrial users, municipal water authorities, and technology experts to capture real-time data on market trends, regulatory impacts, technological adoption, and sustainability practices. Secondary research involved analyzing annual reports, scientific journals, government publications, patents, and industry white papers to validate market dynamics and quantify adoption patterns. Both top-down and bottom-up approaches were applied to estimate market size, considering factors such as end-user demand in industrial treatment and municipal water, regulatory mandates, and regional infrastructure developments. Forecasting models incorporated technological advances in membrane filtration, hollow-fiber and ceramic membranes, as well as smart and AI-enabled monitoring systems. This methodology ensures USDAnalytics delivers a comprehensive, accurate, and forward-looking market outlook, guiding strategic planning, investment decisions, and technology adoption strategies.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.