Metal Carboxylates Market 2025–2034: Cobalt-Free Catalysts, PVC Stabilizer Expansion, and Sustainable Additive Transformation Driving $9.8 Billion Outlook at 5.8% CAGR

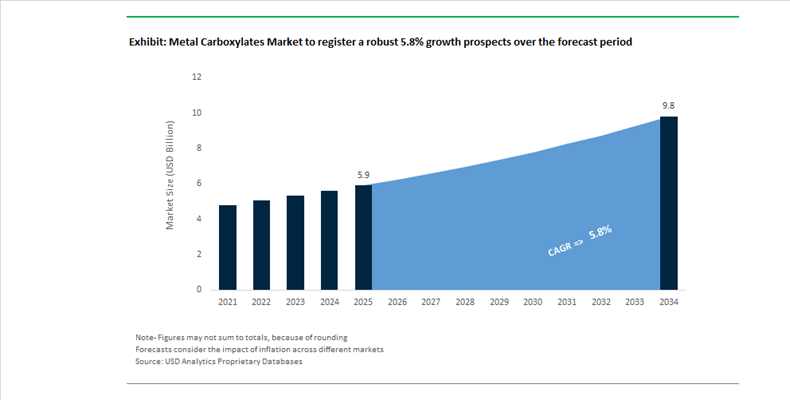

The Metal Carboxylates Market is projected to grow from $5.9 billion in 2025 to $9.8 billion by 2034, registering a CAGR of 5.8%. Market expansion is being driven by rising demand for metal soaps, metal driers, and metal-based stabilizers across alkyd coatings, PVC processing, rubber compounding, lubricants, and specialty adhesives. Regulatory tightening under REACH, TSCA, and evolving EU Occupational Exposure Limits for cobalt is accelerating the transition toward cobalt-free catalysts, low-volatility metal carboxylates, and high-performance alternatives with reduced toxicity classifications. Simultaneously, Asia-Pacific manufacturing growth and infrastructure investments are sustaining demand for sodium stearate, calcium/zinc stabilizers, and advanced neodecanoate-based adhesion promoters.

In April 2024, Arxada, integrating Troy Corporation, showcased advanced Troykyd and Troythix additive technologies at the American Coatings Show, emphasizing controlled-release drying systems designed to reduce environmental leaching. Throughout 2024, Evonik expanded availability of its VESTINAT metal carboxylate line for PVC thermal stabilization and processing optimization, targeting cost-efficient and lower-footprint construction materials. By Q4 2024, BASF completed expansion of sodium stearate production capacity at its Nanjing site to address surging Asia-Pacific demand in plastics and personal care applications. In the same year, Dura Chemicals advanced its DriCAT CV series, offering lower-metal cobalt alternatives to manage raw material price volatility while maintaining crosslink density and drying efficiency in alkyd formulations. Valtris also completed divestiture of Champlor Renewables in 2024, reallocating capital toward higher-margin metal carboxylates and specialty additives.

Strategic repositioning intensified in 2025 and early 2026. In 2025, Comar Chemicals scaled cobalt-free rubber adhesion promoters utilizing bio-neodecanoate ligands to address ethical sourcing pressures in tire manufacturing. In late 2025, Borchers, a Milliken brand, issued regulatory guidance responding to stricter EU cobalt exposure limits, promoting Cobalt-Free High-Performance Catalysts for alkyd coatings to maintain drying speed without triggering new hazard labeling. In January 2026, Valtris announced a new Chief Executive Officer and enterprise-wide transformation strategy aimed at consolidating business units and reinforcing its position as a preferred supplier of sustainable metal-based additives. In February 2026, Valtris presented low-volatility metal carboxylate solutions at PLASTINDIA, aligning with global regulatory shifts. Concurrently, Troy Minerals advanced high-purity silica projects to serve as catalyst carriers in polymerization and rubber compounding, reflecting the broader move toward supported metal carboxylate systems that enhance catalytic efficiency and durability in industrial-scale processing.

Metal Carboxylates Market Trends and Opportunities

Trend: Capacity Expansion for Zirconium and Aluminum Carboxylate Driers in Low-VOC and Solvent-Free Coatings

The Metal Carboxylates Market is experiencing a decisive capacity expansion cycle as coatings manufacturers accelerate the shift toward 100% solids, high-solids, and solvent-free systems. Zirconium and aluminum carboxylates have emerged as critical auxiliary and through-driers, enabling fast oxidative curing without relying on legacy lead or cobalt salts that face regulatory phase-out. In late 2025, the zirconium value chain reached a structural inflection point as rising energy, aerospace, and defense demand prompted upstream producers to prioritize high-purity zirconium derivatives. Processors such as ATI Inc. and mining companies including Iluka Resources, through projects such as Balranald, have redirected output toward downstream chemical applications where zirconium carboxylates are now standard in environmentally compliant aviation primers and industrial maintenance coatings.

Parallel innovation is occurring in manganese carboxylates, which are increasingly scaled as eco-friendly curing catalysts for waterborne inks and wood coatings. Company disclosures in 2025 indicate that manganese systems deliver comparable oxidative performance while complying with stringent EU and North American toxicity thresholds. This transition directly supports Net-Zero 2050 objectives by enabling lower curing temperatures and higher throughput. By Q3 2025, operational decoupling became evident as additive producers signed direct off-take agreements with miners to secure high-purity zirconium feedstock, bypassing traditional processing hubs and insulating automotive refinishing and industrial coatings supply chains from volatility.

Trend: Supply Hedging and Rare-Earth Metal Carboxylates for Advanced PVC Stabilization

Rare-earth metal carboxylates, particularly cerium and lanthanum stearates, are becoming the stabilizers of choice for premium PVC formulations used in window profiles, wire insulation, and automotive plastics. Their superior heat and light stabilization properties are driving demand, but extreme price volatility has forced a strategic rethink of supply security. In October 2025, China’s Ministry of Commerce implemented sweeping export controls on rare-earth materials and related chemicals, including a 0.1% value rule that triggered licensing requirements for foreign products containing Chinese-origin rare earths. This policy shock pushed cerium and lanthanum prices in the EU to as much as six times 2023 levels, creating immediate margin pressure for polymer additive suppliers.

In response, manufacturers are aggressively securing non-Chinese supply. Canada Rare Earth’s acquisition of a controlling stake in a Laos-based refinery in January 2025 and Lynas commissioning its Kalgoorlie Processing Facility underscore the urgency of vertical integration. These assets underpin a 20-year mine life at Mt Weld and provide the rare-earth feedstocks essential for metal carboxylate stabilizer production. At the policy level, the European Commission’s Critical Raw Materials Act accelerated strategic autonomy efforts in March 2025 by designating localized extraction and recycling projects, reinforcing long-term demand visibility for rare-earth carboxylates within the European polymer additives ecosystem.

Opportunity: High-Purity Copper and Silver Carboxylates for Conductive Ink and Electronics Manufacturing

One of the fastest-growing opportunities in the Metal Carboxylates Market lies in high-purity copper and silver carboxylates used as organometallic precursors for conductive inks. The rapid expansion of flexible hybrid electronics, in-mold electronics, and wearable devices in automotive and consumer technology is driving demand for low-temperature, high-conductivity materials compatible with heat-sensitive substrates. Research published in December 2025 highlights one-pot continuous synthesis routes that convert silver and copper carboxylates into nanoparticles that decompose cleanly at low sintering temperatures, enabling printing on PET and TPU without substrate deformation.

Performance benchmarks from advanced rolling electrodeposition techniques show resistivity levels near 13.7 micro-ohm-centimeter, meeting the electrical stability requirements of 5G antennas, smart-skin sensors, and autonomous vehicle electronics. Commercial scaling is already underway. In early 2025, Cabot Corporation announced an approximately 200 million dollar investment program in the United States to expand production of specialized conductive additives and precursors, positioning metal carboxylates as a cornerstone material class for next-generation electronics and battery-adjacent applications.

Opportunity: Biodegradable Metal Carboxylates for VIDA-Compliant Marine and Environmental Lubricants

The regulatory transition from the Vessel General Permit to the Vessel Incidental Discharge Act has created a non-discretionary growth channel for biodegradable metal carboxylates in marine lubricants. VIDA standards enforced during 2024–2025 require that 90% of lubricant formulations be biodegradable, with at least 60% CO₂ evolution or oxygen consumption during standardized testing. These criteria effectively eliminate conventional petroleum greases from oil-to-sea interfaces, accelerating the adoption of lithium and calcium carboxylates derived from renewable fatty acids.

Sector-wide adoption is already visible. In 2025, Chevron and TotalEnergies expanded their Environmentally Acceptable Lubricant portfolios, deploying biodegradable metal soaps in rudder bearings, submerged pumps, and propeller assemblies where leakage must remain non-toxic to marine ecosystems. Importantly, this demand is spilling over into adjacent industries. Forestry operations, ski resorts, and construction sites near wetlands are increasingly mandated to use EAL-style lubricants, creating a secondary growth avenue for metal carboxylate producers supplying biodegradable thickening systems beyond traditional marine applications.

Metal Carboxylates Market Share and Segmentation Insights

Cobalt Carboxylates Lead Metal Carboxylates Market Through High-Performance Drying Catalysts in Coatings

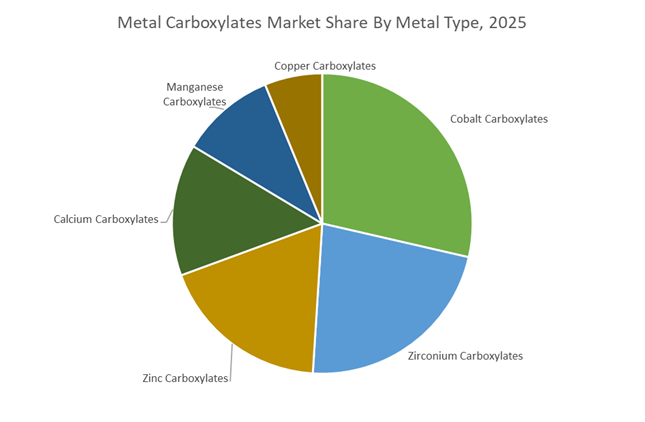

Cobalt carboxylates accounted for 28.60% of the Metal Carboxylates Market share in 2025, making them the most widely used metal-based drier catalysts in coating and resin formulations. These compounds function as oxidative drying catalysts in alkyd paints, varnishes, and printing inks, accelerating the polymerization process that converts liquid coatings into durable solid films. Cobalt carboxylates are particularly valued for their high catalytic efficiency, rapid surface drying capability, and compatibility with alkyd resin systems, enabling coatings to achieve faster drying times and improved film formation. Their effectiveness allows formulators to maintain strong coating performance with relatively low additive concentrations, which contributes to their continued dominance in industrial coating formulations. In 2025, increasing regulatory attention toward cobalt compounds under REACH and other chemical safety frameworks has encouraged coatings manufacturers to explore alternative metal drier systems. However, cobalt carboxylates continue to lead the market due to their superior drying performance and long-established formulation familiarity, with substitution efforts gradually progressing in applications where performance requirements allow cobalt-free alternatives.

Paints and Coatings Industry Drives the Largest Demand for Metal Carboxylates

Paints and coatings accounted for 52.80% of the Metal Carboxylates Market share in 2025, making the sector the largest consumer of metal carboxylate additives globally. Metal carboxylates function primarily as driers, stabilizers, and catalytic agents in solvent-based alkyd coatings, wood finishes, varnishes, and printing inks, where they accelerate oxidative curing processes and improve coating durability. The enormous global scale of architectural coatings, industrial coatings, and protective coating production drives sustained demand for these additives across the construction, automotive, and infrastructure sectors. Metal carboxylate systems typically combine primary driers such as cobalt with secondary metals including zirconium, calcium, manganese, and zinc, creating balanced catalyst packages that control both surface and through-drying of coatings. In 2025, the coatings industry’s transition toward low-VOC and waterborne alkyd formulations has driven the development of specialized metal carboxylate technologies capable of functioning effectively in aqueous systems. Manufacturers are introducing pre-complexed and emulsified drier systems designed to maintain catalytic efficiency in waterborne coatings while supporting regulatory compliance and improved environmental performance.

Metal Carboxylates Market Competitive Landscape

The metal carboxylates market in 2026 is shifting toward cobalt-free driers, manganese and iron-based catalysts, and high-purity neodecanoates and octoates. Regulatory pressure (REACH, TSCA) is accelerating demand for low-toxicity, high-performance additives in coatings, lubricants, and polymer systems with enhanced thermal stability and anti-skinning performance.

Borchers drives cobalt-free drying with iron-based catalysts for high-performance coatings

Borchers (Milliken) is leading the transition to cobalt-free metal carboxylates through Borchi® OXY–Coat 1101, an iron-based catalyst delivering uniform through-drying, improved gloss, and corrosion resistance in waterborne alkyd coatings. Its APAC expansion via the Pune lab enhances localized formulation development, reducing time-to-market for coatings manufacturers. With strategic EU distribution partnerships and a strong focus on tin-free and cobalt-free driers, Borchers is targeting high-growth direct-to-metal (DTM) coatings requiring durability, adhesion, and regulatory-compliant oxidative curing systems.

Arxada integrates green chemistry with multifunctional metal carboxylate additive platforms

Arxada, strengthened by Troy Corporation integration, is scaling its LEAP platform to combine metal carboxylate driers with multifunctional additives like Polyboost™. With five production sites and four R&D centers, the company delivers regulatory-compliant solutions aligned with GHS and EU Eco-Label standards. Its TMMA framework integrates drying catalysts with preservatives such as Polyphase® 862CR, offering end-to-end coating protection. Increased patent activity and a focus on “regulatory-ready” chemistry position Arxada as a key innovator in sustainable coatings and metalworking fluid additives.

Valtris expands zinc and calcium carboxylates for lubricant stability and polymer catalysis

Valtris Specialty Chemicals is strengthening its position in high-performance metal carboxylates by expanding zinc and calcium carboxylate production for automotive lubricants and polymer systems. These additives enhance oxidation resistance and thermal stability, extending lubricant lifecycle in high-load environments. Its customized neodecanoates and octoates address solubility challenges in hydrocarbon systems while supporting polyurethane and resin catalysis. With growing adoption in ozone catalytic oxidation and green chemistry processes, Valtris is targeting specialty industrial applications requiring precision-engineered additive performance.

Ege Kimya scales sustainable manganese and cobalt carboxylates for tire and industrial applications

Ege Kimya is advancing high-purity metal carboxylates with a focus on manganese-based alternatives and sustainable production. Its materials serve as critical adhesion promoters in tire manufacturing and functional additives across ceramics, detergents, and construction chemicals. With expanded capacity and renewable energy integration at its Istanbul facilities, the company supports multi-sector demand. Its 2026 roadmap emphasizes closed-loop manufacturing to stabilize raw material costs and ensure consistent supply of performance-matched metal salts for industrial applications.

Dura Chemicals advances zirconium-based driers and water-reducible systems for low-VOC coatings

Dura Chemicals is strengthening its leadership in metallic soaps and oxidative driers through zirconium carboxylates, replacing toxic lead systems while enhancing hardness, gloss, and curing efficiency. Its portfolio spans active and auxiliary driers, including cobalt, calcium, and zinc systems optimized for unsaturated polyester and PVC stabilization. The company’s R&D focus on water-reducible driers aligns with the rapid shift toward low-VOC, water-based architectural coatings, addressing challenges like anti-skinning, high-humidity stability, and improved solubility in modern coating formulations.

United States: Green Chemistry Incentives and Performance-Led Substitution

The United States metal carboxylates market is undergoing a structurally driven transition shaped by environmental regulation, supply chain localization, and performance requirements in coatings and lubricants. In 2025, the United States Environmental Protection Agency intensified its green chemistry incentives, explicitly encouraging the replacement of legacy cobalt-based driers in architectural and consumer coatings with bio-based and lower-toxicity metal carboxylates. This policy push is accelerating adoption of manganese, zirconium, and calcium carboxylates that deliver comparable drying performance while aligning with sustainability and worker-safety objectives.

Innovation is also being driven by tightening polymer and medical standards. In late 2025, major U.S. specialty chemical suppliers introduced liquid non-PFAS processing aids and metal carboxylate-based lubricants engineered for compliance with 2026 medical-grade polymer specifications. Demand from infrastructure, marine, and automotive segments is rising in parallel. Increased domestic vehicle output and offshore capital expenditure of approximately USD 7.0 billion in the Gulf of Mexico are supporting uptake of extreme-pressure additives, with zinc and calcium carboxylates specified for thermal stability under high-load and sub-sea operating conditions. Public-private critical mineral initiatives launched in 2025 are further stabilizing feedstock availability for cobalt, manganese, and zirconium oxides, easing cost volatility. At the state level, California’s draft Airborne Toxic Control Measure for automotive refinishing is accelerating OEM migration away from cadmium and hexavalent chromium toward zirconium and manganese carboxylates that maintain high-gloss finishes at lower curing temperatures.

China: Carbon Regulation, EV Catalysts, and Smart Manufacturing

China’s metal carboxylates market is evolving through a convergence of emissions regulation, electric vehicle supply chain expansion, and manufacturing digitalization. In March 2025, the Ministry of Ecology and Environment expanded the national Emissions Trading System to include aluminum and steel, increasing pressure on chemical producers to lower carbon intensity. As a result, manufacturers of metal carboxylates used in rubber-to-metal adhesion promoters are investing in cleaner synthesis routes and energy-efficient processing.

Feedstock security and downstream demand are reinforcing this shift. The National Critical Mineral Mission launched in early 2025 is scaling domestic refining of cobalt and nickel, both essential for carboxylates used as polymerization catalysts in EV battery casings and electronics housings. Capacity expansion by Arkema at its Nansha site during 2024–2025 underscores the focus on advanced coatings and electronics materials. Technologically, Chinese producers are adopting one-pot thermal decomposition techniques for manganese carboxylates to meet rising demand for thermal stabilizers in construction materials. Large chemical hubs in Jiangsu have also deployed AI-enabled batch monitoring to ensure consistency in liquid-form carboxylates, supporting export-oriented paint and ink customers that prioritize rapid formulation cycles.

India: Critical Mineral Security and Pharmaceutical Pull

India’s metal carboxylates market is being reshaped by resource security initiatives and rapid growth in downstream pharmaceuticals and infrastructure. The National Critical Minerals Mission launched in 2025 commits over ₹34,000 crore to securing domestic cobalt and copper supplies, directly supporting local production of paint driers, catalysts, and stabilizers. This policy framework reduces dependence on imported oxides and strengthens cost competitiveness for Indian chemical processors.

End-use demand is broadening beyond coatings. India’s pharmaceutical industry expansion is driving higher consumption of metal carboxylates as synthesis intermediates and stabilizers in drug formulations. Fiscal measures are also influencing application diversity. In late 2025, GST rationalization for value-added marine chemicals improved the economics of copper-based carboxylates used as fungicides and wood preservatives, particularly for coastal infrastructure projects. Upstream, exploration milestones reported by the Ministry of Mines in early 2025 identified significant manganese and iron ore reserves in Odisha and Madhya Pradesh, earmarked for domestic chemical processing. Together, these developments position India as an increasingly integrated producer-consumer market rather than a purely import-dependent one.

Germany: Regulatory Substitution and Advanced Catalyst Design

Germany represents the regulatory and technological frontier of the metal carboxylates market in Europe. Following the December 2024 amendments to REACH Annex XVII, stricter workplace exposure monitoring for cobalt compounds has accelerated substitution efforts. German chemical leaders including BASF and Umicore have led the transition toward polymeric cobalt technologies and cobalt-reduced systems that preserve drying efficiency while meeting carcinogen exposure limits.

Product innovation is reinforcing this pivot. In January 2025, BASF launched its Metalcat range of transition metal carboxylates designed for fine chemical synthesis under tightened EU restrictions. Parallel R&D advances include the successful piloting of ECOS MND 10, a complexed manganese polymer that functions as a direct replacement for traditional cobalt driers. This technology enables paint manufacturers to achieve ISO touch-dry benchmarks in under 60 minutes without yellowing or discoloration. Germany’s approach underscores a shift from compliance-only reformulation toward performance-led alternatives that set benchmarks for global adoption.

Country-Level Strategic Positioning in the Metal Carboxylates Market

Metal Carboxylates Market County Level Snapshot

|

Country

|

Strategic Driver

|

Key Metal Carboxylates Focus

|

Policy or Regulatory Catalyst

|

Competitive Positioning

|

|

United States

|

Green chemistry and performance compliance

|

Manganese, zirconium, calcium

|

EPA incentives, state air toxics rules

|

Sustainable substitution leadership

|

|

China

|

Carbon regulation and EV growth

|

Cobalt, nickel, manganese

|

ETS expansion, critical minerals mission

|

Scale with smart manufacturing

|

|

India

|

Resource security and pharma demand

|

Cobalt, copper, manganese

|

NCMM, GST rationalization

|

Integrated domestic value chain

|

|

Germany

|

REACH-driven substitution

|

Polymeric cobalt, manganese polymers

|

REACH Annex XVII amendments

|

Regulatory-led innovation benchmark

|

Metal Carboxylates Market Report Scope

Metal Carboxylates Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.9 Billion

|

|

Market Size (2034)

|

$9.8 Billion

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Metal Type (Cobalt Carboxylates, Manganese Carboxylates, Zirconium Carboxylates, Zinc Carboxylates, Calcium Carboxylates, Copper Carboxylates), By Product Form (Liquid, Solid, Granular), By Functionality (Catalysts and Polymerization Initiators, Driers and Siccatives, Lubricant Additives, Plastic Stabilizers, Corrosion Inhibitors, Adhesion Promoters), By End-Use Industry (Paints and Coatings, Automotive, Building and Construction, Oil and Gas, Agriculture, Pharmaceuticals and Fine Chemicals, Textiles and Electronics)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF, Dow, Arkema, DIC, Elementis, Umicore, Valtris Specialty Chemicals, PMC Group, Ege Kimya, Penta Manufacturing, Organometal, Comar Chemicals, DURA Chemicals, American Elements, Troy

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Metal Carboxylates Market Segmentation

By Metal Type

- Cobalt Carboxylates

- Manganese Carboxylates

- Zirconium Carboxylates

- Zinc Carboxylates

- Calcium Carboxylates

- Copper Carboxylates

By Product Form

By Functionality

- Catalysts and Polymerization Initiators

- Driers and Siccatives

- Lubricant Additives

- Plastic Stabilizers

- Corrosion Inhibitors

- Adhesion Promoters

By End-Use Industry

- Paints and Coatings

- Automotive

- Building and Construction

- Oil and Gas

- Agriculture

- Pharmaceuticals and Fine Chemicals

- Textiles and Electronics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Metal Carboxylates Market

- BASF

- Dow

- Arkema

- DIC

- Elementis

- Umicore

- Valtris Specialty Chemicals

- PMC Group

- Ege Kimya

- Penta Manufacturing

- Organometal

- Comar Chemicals

- DURA Chemicals

- American Elements

- Troy

*- List not Exhaustive