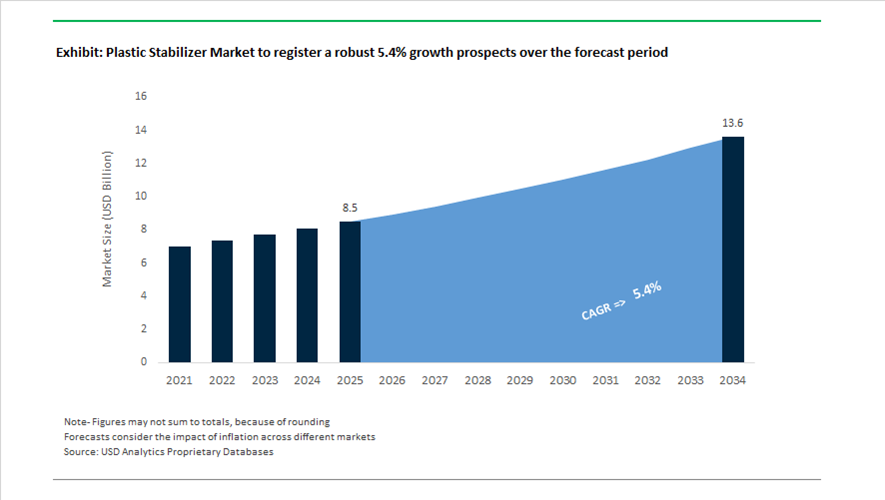

Plastic Stabilizer Market Size 2025–2034: $8.5 Billion to $13.6 Billion at 5.4% CAGR Driven by PFAS-Free Additives, Tin Replacement, and High-Voltage Cable Applications

The global plastic stabilizer market is projected to grow from $8.5 billion in 2025 to $13.6 billion by 2034, registering a CAGR of 5.4%. Growth is supported by rising demand for heat stabilizers, UV stabilizers, antioxidants, HALS (Hindered Amine Light Stabilizers), metal-based PVC stabilizers, and multifunctional systems used in construction, automotive, packaging, medical devices, and energy infrastructure. As regulatory scrutiny intensifies around PFAS, organotin compounds, aromatic amines, and phenolic antioxidants, manufacturers are accelerating innovation toward safer, high-performance, and environmentally compliant stabilization chemistries.

A major structural shift occurred in late 2024 when Clariant completed its transition to a fully PFAS-free additive portfolio. The launch of the AddWorks® PPA line delivers polymer processing aid performance—melt fracture control and extrusion efficiency—without fluorinated chemistries. This milestone aligns with tightening global PFAS regulations affecting polymer extrusion and compounding industries. Clariant further strengthened its position in 2025 by launching AddWorks® LXR 548, a phenol-free antioxidant system designed for medical-grade polyolefins, preventing yellowing after gamma sterilization and thermal exposure. Additionally, in August 2025, Clariant doubled capacity for Nylostab® S-EED at its Cangzhou facility in China, reinforcing supply of multifunctional stabilizers for high-performance nylon applications such as artificial turf and engineering plastics.

Tin replacement and PVC reformulation represent another key market driver. At K 2025, Baerlocher showcased its global Tin Replacement initiative, promoting calcium/zinc-based stabilizer systems as alternatives to organotin compounds in drinking water pipes, food-contact materials, and medical-grade PVC. This transition reflects increasing regulatory restrictions in Europe and North America on heavy-metal-based stabilizers. In parallel, Valtris Specialty Chemicals expanded its collaboration with Transfar Group in 2024 to develop phenol-free over-based barium stabilizers and mixed-metal systems for global PVC markets. In February 2026, Valtris announced new leadership to accelerate its pivot toward bio-based and non-phthalate stabilizer solutions.

Innovation in specialty polymer stabilization is expanding into energy and agricultural infrastructure. In February 2026, BASF introduced Irgastab® Cable KV 10, a thermal stabilizer tailored for peroxide-crosslinked polyethylene (XLPE) in medium- and high-voltage cables, addressing insulation reliability in modern power grids. Earlier, in 2024, BASF launched Irgastab® PUR 71, a non-aromatic amine antioxidant for polyurethane foams with an improved environmental, health, and safety profile. In August 2025, BASF expanded its VALERAS® portfolio with Tinuvin® NOR® 112, a HALS designed for greenhouse films used in organic farming, offering resistance to sulfur and chlorine exposure while extending film lifespan.

UV and light stabilization technologies continue advancing. At ECS 2025, Songwon introduced the SONGSORB® CS 400 liquid triazine UV absorber series, optimized for waterborne coatings applied to plastic and composite substrates. Meanwhile, ADEKA launched a high-performance polypropylene clarifying and nucleating agent in late 2024, enabling lightweighting in automotive and packaging applications by improving structural integrity at lower resin volumes.

Key Trends and High-Value Opportunities in the Plastic Stabilizer Market

Regulatory-Driven Forced Conversion to Calcium-Based (Ca-Zn) Stabilizer Systems

The plastic stabilizer market has entered a non-reversible regulatory transition phase, where lead-based heat stabilizers have shifted from being commercially discouraged to legally prohibited across major PVC-consuming regions. The European Commission’s adoption of Regulation (EU) 2023/923 formally ended the remaining grace period, banning the placement of PVC articles containing lead concentrations equal to or above 0.1% by weight from November 28, 2024. This regulatory inflection point has triggered immediate and large-scale reformulation across rigid PVC pipes, profiles, cables, and fittings, accelerating the global conversion toward Calcium-Zinc (Ca-Zn) and organic-based one-pack stabilizer systems.

This shift is not confined to Europe. India has institutionalized similar enforcement through the Lead Stabilizer in Polyvinyl Chloride (PVC) Pipes and Fittings Rules, directly impacting potable water and sanitation infrastructure. As of 2025, Indian manufacturers are required to demonstrate lead extraction levels below 0.05 ppm in the third extraction test, effectively making Ca-Zn stabilizers mandatory for participation in large-scale public infrastructure programs such as the Jal Jeevan Mission. Given India’s role as one of the world’s fastest-growing PVC pipe markets, this regulatory mandate has materially altered global stabilizer demand patterns.

On the supply side, stabilizer producers have responded with targeted capacity expansion. Baerlocher and other global leaders have increased calcium-based stabilizer production in Asia, including dedicated lines in Changzhou, China, to ensure regional availability and formulation customization. These next-generation Ca-Zn systems are engineered to sustain extrusion line speeds above 120 meters per minute, a performance threshold historically associated with lead stabilizers, while mitigating risks such as plate-out, die build-up, and surface chalking. Despite Zinc accounting for roughly 40–60% of Ca-Zn raw material input costs and remaining price-volatile, 2025 industry performance data indicates that modern Ca-Zn one-packs now achieve cost-to-performance parity with lead systems in rigid profiles, supported by improved color hold, gloss retention, and long-term heat stability.

Multifunctional Stabilizer Systems for High-Heat Polyolefins in EV and Battery Applications

The rapid electrification of the automotive sector is redefining the operating environment for polyolefins, particularly polypropylene and polyethylene used in battery housings, cable insulation, and under-the-hood components. These applications expose polymers to continuous thermal loads exceeding 120°C, elevated oxidative stress, and electrical insulation requirements that conventional antioxidant packages were not designed to handle. As a result, stabilizer demand is shifting toward multifunctional, synergistic systems that integrate long-term thermal stability, oxidative resistance, and electrical performance into a single formulation.

Battery safety and durability have become central drivers. Research published in MDPI in 2025 highlighted the use of functionalized polyolefin separators incorporating aramid fibers and WS2@C nanoflower coatings for lithium-ion and lithium-sulfur batteries. These next-generation separators are engineered to withstand more than 3,000 charge–discharge cycles, but their performance is contingent on advanced stabilizer packages that prevent polymer degradation under sustained electrochemical and thermal stress. This has created downstream demand for stabilizers capable of maintaining molecular integrity in extreme environments rather than merely protecting during melt processing.

In parallel, automotive polymer suppliers are adopting synergistic antioxidant blends that combine primary hindered phenols with secondary phosphites. These systems operate across the full lifecycle of the plastic, with phenols scavenging peroxy radicals during service life and phosphites decomposing hydroperoxides formed during high-temperature processing. Commercial formulations such as Vinati Organics’ Veenox blends are being increasingly specified for EV battery enclosures and thermal management components, extending part lifetimes while reducing premature embrittlement and discoloration. This evolution positions stabilizers as performance enablers rather than cost-driven additives, particularly in electrified mobility platforms.

Re-Stabilization of Post-Consumer Recycled (PCR) Polymers for High-Value Circular Applications

The most structurally significant opportunity in the plastic stabilizer market lies in the re-stabilization of recycled polymers. Mechanical recycling introduces chain scission, residual catalysts, and peroxide species that accelerate yellowing, brittleness, and odor formation. As regulatory and brand-owner pressure pushes recycled content into durable goods rather than downcycled products, stabilizers are becoming essential tools for restoring polymer performance.

In 2025, stabilizer development has shifted toward multifunctional re-stabilization packages that neutralize residual contaminants while rebuilding oxidative resistance in PCR PVC and polyolefins. These systems are increasingly deployed during recompounding to enable closed-loop recycling for long-life applications such as pressure pipes, roofing membranes, and construction profiles. Unlike traditional antioxidants, re-stabilization formulations are designed to address cumulative “recycling fatigue,” allowing polymers to survive multiple processing cycles without catastrophic property loss.

Regulatory scrutiny around NIAS (Non-Intentionally Added Substances) has further amplified this opportunity. Authorities in the European Union and Brazil have tightened migration and safety requirements for recycled plastics used in food-contact and consumer applications. This has driven demand for high-purity, low-migration stabilizers capable of passing challenge tests mandated by multinational brand owners. Nestlé’s recent R&D programs in food-grade recycled plastics exemplify this shift, as stabilizer selection becomes a gatekeeping criterion for PCR qualification in premium packaging streams.

Specialized Bio-Stabilizers for Compostable and Bio-Based Polymers

Biodegradable polymers such as Polylactic Acid (PLA) and Polyhydroxyalkanoates (PHA) present a distinct stabilization challenge. These materials are inherently sensitive to heat and moisture, undergoing hydrolytic degradation during extrusion and molding. This sensitivity has historically limited their adoption in applications requiring mechanical robustness, creating a high-margin opportunity for stabilizers that protect the polymer during processing without compromising compostability.

At the K 2025 trade fair in Düsseldorf, Braskem showcased bio-based polyethylene and EVA foams with a reported carbon footprint as low as minus 2.27 kg CO₂e per kilogram. These materials rely on non-toxic stabilizers derived from renewable feedstocks to maintain processing stability in healthcare and hygiene applications. The development underscores a broader trend toward bio-stabilizers that align with life-cycle assessment metrics while meeting industrial performance thresholds.

In parallel, PLA processors are increasingly adopting alkaline soap stabilizers such as calcium and zinc stearates to act as acid scavengers during melt processing. These additives suppress hydrolytic chain breakdown, enabling PLA to retain mechanical strength during extrusion and thermoforming. As industrial composting infrastructure expands and bio-based plastics compete more directly with conventional resins, demand for tailored stabilizer systems that balance processability, durability, and end-of-life performance is expected to scale rapidly.

Plastic Stabilizer Market Share and Segmentation Insights

Heat Stabilizers Lead Plastic Stabilizer Demand in PVC Processing and Polymer Manufacturing

Heat stabilizers accounted for 38.6% of the Plastic Stabilizer Market by type in 2025, reflecting their critical role in protecting polymers from thermal degradation during high-temperature processing operations. These stabilizers are particularly important in PVC processing where extrusion and molding temperatures can cause polymer chain degradation without adequate stabilization. Heat stabilizers such as calcium-zinc systems, organotin compounds, and organic stabilizers are widely used across PVC applications including pipes, profiles, siding, and wire insulation. In 2025, the global transition toward lead-free PVC heat stabilizers has largely been completed, with next-generation calcium-zinc and organic stabilizer systems providing improved performance while meeting international environmental regulations.

Building and Construction Sector Drives Plastic Stabilizer Consumption in Long-Life PVC Products

Building and construction represented 38.1% of the Plastic Stabilizer Market by application in 2025, reflecting the extensive use of PVC materials in infrastructure and building products. Construction applications such as PVC pipes, window profiles, roofing membranes, flooring materials, and cable insulation require effective polymer stabilization to maintain mechanical properties and durability throughout long service lifetimes. The scale of global construction activity continues to support strong demand for polymer stabilization additives. In 2025, the increasing adoption of environmentally compliant stabilizer systems in green building materials is influencing additive selection, with manufacturers adopting heavy metal free stabilizers that support certification requirements in sustainable construction projects while maintaining long-term polymer stability.

Plastic Stabilizers Market Competitive Landscape

The global plastic stabilizers market is transitioning toward circularity-enabling additives, including PFAS-free processing aids, antioxidant systems, and recycling stabilizers. Competition is defined by sustainability innovation, regulatory compliance, and high-performance stabilization solutions for automotive, packaging, construction, and medical polymers.

BASF Leads High-Performance Stabilizer Innovation with VALERAS® Portfolio and Cable-Grade Solutions

BASF SE is advancing plastic stabilizer technologies through its VALERAS® portfolio, focusing on durability and sustainability. A global price increase of up to 20% in March 2026 reflects rising input costs and continued R&D investment in antioxidants, light stabilizers, and process stabilizers. The Irgastab® Cable KV 10 stabilizer supports peroxide cross-linking in XLPE cables, ensuring thermal stability and long-term insulation performance. Tinuvin® NOR® stabilizers provide UV and agrochemical resistance for greenhouse films, supporting sustainable agriculture applications. Capacity expansion for Ultramid® and Ultradur® in India aligns with growing demand in automotive and e-mobility sectors. Strategy emphasizes high-performance stabilization, application-specific innovation, and localized production.

Songwon Strengthens Global Stabilizer Supply with Blended Systems and Logistics Integration

Songwon Industrial Co., Ltd. focuses on polymer stabilization through operational agility and supply chain resilience. A 12% to 20% global price adjustment in 2026 addresses cost pressures and logistics volatility. The company is expanding its portfolio of antioxidants and coatings additives to meet high-temperature performance requirements in electronics and packaging applications. Its South Korea-based manufacturing hub ensures reliable global supply of phosphite and phenolic antioxidants. Blended stabilizer systems (OPS) combine multiple additives into dust-free pellets, improving dosing efficiency and workplace safety. Strategy centers on supply reliability, formulation efficiency, and high-performance stabilizer systems.

Adeka Advances Heavy Metal-Free Stabilizers with Recycling-Focused Additives and Bio-Based Plasticizers

Adeka Corporation is leading innovation in heavy metal-free stabilizers, particularly for PVC and recycled polymers. The ADK CYCLOAID™ UPR series supports mechanical recycling by enabling upcycling of post-consumer plastics into high-value products. ADK CYCLOAID™ PNB-205 introduces a bio-based polymeric plasticizer that enhances PVC stability while replacing phthalate-based systems. The ADK STAB RX series provides calcium-zinc stabilizers as alternatives to lead-based systems, meeting REACH and RoHS compliance. The ADK STAB LA series offers high-performance HALS for automotive interiors and outdoor materials. Strategy focuses on sustainable additives, regulatory compliance, and circular plastic solutions.

Clariant Expands Specialty Stabilizers for Medical and High-Durability Polymer Applications

Clariant AG is focusing on niche, high-value stabilizer applications in engineering plastics and medical materials. Expansion of Nylostab™ S-EED production in China supports growth in the nylon industry, particularly for high-performance plastics. The stabilizer enhances UV resistance and durability in artificial turf and outdoor applications. AddWorks® LXR 548 provides phenol-free antioxidant solutions for medical devices, preventing yellowing during gamma sterilization. Collaboration with Beijing Tiangang Auxiliary integrates regional expertise with advanced stabilizer technologies. Strategy emphasizes high-purity stabilizers, medical-grade applications, and performance durability.

Baerlocher Drives Calcium-Zinc Stabilizer Adoption for PVC Circularity and Carbon Reduction

Baerlocher Group is advancing calcium-zinc stabilizer systems as replacements for tin- and lead-based additives in PVC applications. The BAEROSTAB family enables transition to Ca-Zn stabilizers without requiring process modifications, supporting circular plastic use. The company demonstrated up to 50% CO₂ reduction compared to traditional stabilizers through renewable energy integration. The transition of its UK Bury facility to 100% calcium-based production reflects commitment to eliminating lead-based stabilizers. BAEROPAN systems are approved for applications including potable water pipes, food packaging, and medical plastics. Strategy focuses on sustainable PVC stabilization, regulatory compliance, and carbon footprint reduction.

Evonik Integrates AI and PFAS-Free Solutions for Advanced Polymer Stabilization and Recycling Processes

Evonik Industries AG is leveraging AI and advanced chemistry to develop next-generation plastic stabilizers. The AIChemBuddy platform accelerates formulation development by analyzing experimental data and optimizing research pathways. Tego Cycle WA 111 and Tego RES 1100 enable removal of contaminants during mechanical recycling, improving recyclate quality. Tego PPA products offer PFAS-free processing aids aligned with global regulatory shifts away from fluorinated chemicals. The VESTAMID® PA12 portfolio incorporates mass-balanced production, reducing CO₂ emissions by up to 70% for high-performance applications. Strategy emphasizes digital innovation, circular economy solutions, and sustainable polymer processing.

India – Compliance-Driven Demand and Accelerated Import Substitution

India’s plastic stabilizer market is being structurally reshaped by regulatory digitization and recycled-content mandates. The July 1, 2025 enforcement of the Plastic Waste Management (Amendment) Rules by the Ministry of Environment, Forest and Climate Change introduced compulsory QR and barcode traceability on plastic packaging. This requirement has materially increased demand for stabilizer formulations with full chemical transparency, migration data, and batch-level disclosure compatibility with national compliance portals. Simultaneously, the 2025–2026 recycled-content thresholds, mandating 30% recycled input for Category I packaging, are driving strong uptake of advanced upcycling stabilizers capable of neutralizing contaminants, odor bodies, and oxidative residues in recycled polyethylene and polypropylene streams.

Policy recalibration is also influencing sourcing strategies. The December 2025 withdrawal of 14 mandatory BIS Quality Control Orders for polymers and chemicals has shifted the market toward voluntary compliance, lowering effective import costs for premium European and Japanese stabilizer systems by an estimated 12 to 15%. This has intensified competition in food-contact and medical-grade plastics. In parallel, domestic capacity is expanding under Atmanirbhar Bharat, with Indian firms scaling Hindered Amine Light Stabilizers production to reduce dependence on East Asian technical imports. Downstream petrochemical investments, including HMEL’s ₹2,600 crore polypropylene and fine chemicals expansion, are reinforcing localized supply of thermal stabilizers, while Plastic Parks are enabling shared R&D infrastructure focused on leaching and migration testing.

Germany – Innovation-Led Transition to Sustainable Additives

Germany remains the technology and sustainability bellwether for plastic stabilizers in Europe, driven by large-scale Verbund investments and regulatory foresight. In December 2025, BASF committed to annual investments of €1.5–2 billion at its Ludwigshafen site through 2028, explicitly modernizing plastic additives and light stabilizer production. Product innovation is central to this strategy, exemplified at K 2025 by the launch of Tinuvin NOR 600, a next-generation NOR-HALS designed for extreme acid resistance in agricultural films and roofing membranes, addressing long-life outdoor polymer applications.

Regulatory pressure is accelerating portfolio shifts. Baerlocher’s Tin Replacement Program gained momentum in late 2025 as tighter EU REACH requirements pushed PVC processors toward calcium-based stabilizer systems. Concurrently, Baerlocher’s carbon neutrality roadmap, targeting 2045 through solar and biomass integration, is influencing procurement decisions among OEMs prioritizing low-carbon additives. German suppliers have also moved early on PFAS-free processing aids, launching alternatives such as the Baerolub AID family to stay ahead of anticipated 2026 EU restrictions while maintaining high-speed extrusion performance.

China – Scale Expansion Under Recycled Standards and Digital Manufacturing

China’s plastic stabilizer market is expanding in volume and complexity, shaped by recycled-plastics standards and large-scale capacity additions. In August 2025, the State Administration for Market Regulation issued nine national standards for recycled plastics, effective February 1, 2026, imposing strict residue limits for stabilizers in rPET and rPS. These standards are shifting demand toward higher-purity, multifunctional stabilizers capable of meeting both mechanical performance and compliance thresholds in recycled polymers.

Multinational investments are reinforcing domestic supply. Clariant, through its joint venture with Beijing Tiangang, commissioned a second Nylostab S-EED line in Cangzhou in August 2025, doubling capacity for nylon stabilizers used in automotive and electrical applications. The scheduled 2025 startup of BASF’s Zhanjiang Verbund site, powered by renewable electricity, further strengthens China’s access to high-performance stabilizers for electric vehicles and durable goods. Environmental policies banning ultra-thin plastic bags from 2026 are also pushing the market toward thicker, stabilizer-intensive reusable plastics. At the operational level, the Ministry of Industry and Information Technology is incentivizing digital twins and real-time yield optimization, raising the bar for process control in additive manufacturing.

Saudi Arabia – Strategic Localization for Polyolefin Additives

Saudi Arabia is positioning itself as a regional hub for plastic stabilizers through targeted infrastructure investments aligned with its expanding polyolefin base. In October 2025, Songwon Industrial announced a major investment to establish a One Pack Systems facility in the Kingdom, designed to serve local and regional polyolefin producers with customized antioxidant and stabilizer blends. This move reduces reliance on imported pre-blends and shortens supply chains for GCC converters.

Feedstock integration is a core advantage. Late-2025 initiatives between Saudi Aramco and SABIC are focused on crude-to-chemicals pathways, lowering the cost base for alkyl phenols and other antioxidant intermediates. These synergies are enhancing the competitiveness of locally produced stabilizers for export markets across the Middle East, Africa, and South Asia, particularly in packaging and infrastructure plastics.

Comparative Snapshot – Plastic Stabilizer Industry by Country

Plastic Stabilizer Market County Level Snapshot

|

Country

|

Primary Demand Driver

|

Strategic Focus

|

Market Positioning

|

|

India

|

Traceability rules and recycled-content mandates

|

Upcycling stabilizers, HALS localization

|

Compliance-led growth hub

|

|

Germany

|

REACH tightening and sustainability targets

|

NOR-HALS, tin-free, PFAS-free systems

|

Global innovation leader

|

|

China

|

Recycled standards and capacity scale-up

|

Multifunctional stabilizers, digital twins

|

High-volume manufacturing base

|

|

Saudi Arabia

|

Polyolefin expansion and feedstock integration

|

One Pack Systems, antioxidants

|

Emerging regional supply hub

|

Plastic Stabilizer Market Report Scope

Plastic Stabilizer Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8.5 Billion

|

|

Market Size (2034)

|

$13.6 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Type (Antioxidants, Light Stabilizers, Heat Stabilizers, Process Stabilizers), By Physical Form (Powder, Liquid, Pellets & Pastilles, One Pack Systems), By Application (Packaging, Building & Construction, Automotive, Agriculture, Consumer Goods), By Material Compatibility (Polyethylene, Polypropylene, Polyvinyl Chloride, Polystyrene, Engineering Plastics)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Songwon Industrial Co. Ltd., Adeka Corporation, Baerlocher GmbH, Clariant AG, SABIC, Evonik Industries AG, Solvay SA, Valtris Specialty Chemicals, Sun Ace Kakoh Pte. Ltd., Sakai Chemical Industry Co. Ltd., Goldstab Organics Pvt. Ltd., Vibrantz Technologies, PMC Group Inc., Beijing Tiangang Auxiliary Co. Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Plastic Stabilizer Market Segmentation

By Type

- Antioxidants

- Light Stabilizers

- Heat Stabilizers

- Process Stabilizers

By Physical Form

- Powder

- Liquid

- Pellets & Pastilles

- One Pack Systems

By Application

- Packaging

- Building & Construction

- Automotive

- Agriculture

- Consumer Goods

By Material Compatibility

- Polyethylene

- Polypropylene

- Polyvinyl Chloride

- Polystyrene

- Engineering Plastics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Plastic Stabilizer Industry

- BASF SE

- Songwon Industrial Co. Ltd.

- Adeka Corporation

- Baerlocher GmbH

- Clariant AG

- SABIC

- Evonik Industries AG

- Solvay SA

- Valtris Specialty Chemicals

- Sun Ace Kakoh Pte. Ltd.

- Sakai Chemical Industry Co. Ltd.

- Goldstab Organics Pvt. Ltd.

- Vibrantz Technologies

- PMC Group Inc.

- Beijing Tiangang Auxiliary Co. Ltd.

*- List not Exhaustive