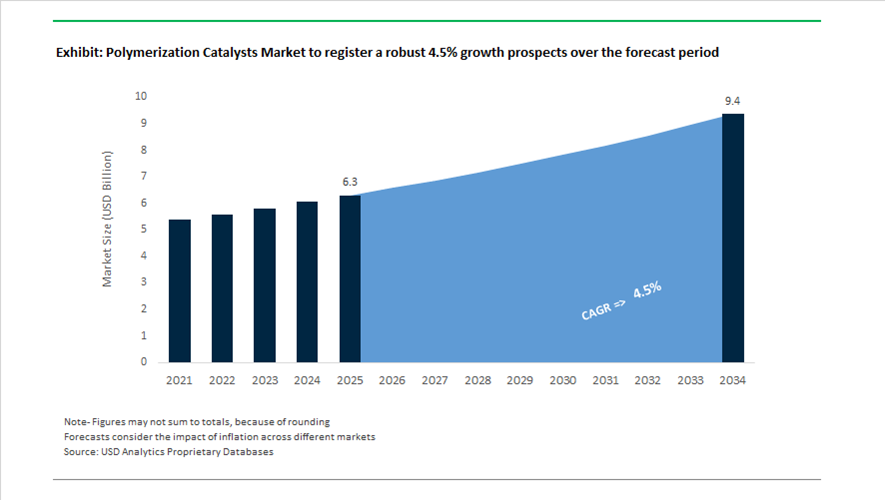

Polymerization Catalysts Market Valued at $6.3 Billion in 2025, Projected to Reach $9.4 Billion by 2034 at 4.5% CAGR

The global polymerization catalysts market is valued at $6.3 billion in 2025 and is projected to reach $9.4 billion by 2034, expanding at a CAGR of 4.5%. Growth is driven by rising demand for polyolefin catalysts, metallocene catalysts, Ziegler–Natta systems, polyester catalysts, styrene monomer catalysts, and advanced catalyst supports across packaging, automotive, textiles, energy infrastructure, and specialty engineering plastics. Market expansion is closely linked to energy efficiency mandates, heavy-metal-free catalyst development, crude-to-chemicals integration, and regional capacity additions in Asia and the Middle East.

In January 2024, BASF introduced a high-efficiency polymerization catalyst system engineered to reduce energy consumption during high-performance plastic production, supporting low-carbon manufacturing objectives. In February 2024, W.R. Grace expanded its licensing agreement with China Coal Shaanxi, doubling polypropylene production capacity to 600 KTA using its CONSISTA® catalyst and donor systems. In October 2024, Birla Carbon inaugurated a specialty carbon post-treatment facility in India to enhance catalyst support materials used in polymerization reactions. These developments reinforced the importance of catalyst efficiency optimization, polyolefin capacity expansion, and advanced catalyst support technologies in high-throughput polymer manufacturing.

Technology differentiation accelerated in 2025. In January 2025, W.R. Grace launched ActivCat®, enabling polyethylene film manufacturers to down-gauge film thickness by up to 20% without compromising mechanical strength. This catalyst solution reduces resin consumption and raw material costs, addressing cost pressures in flexible packaging and consumer goods sectors. In April 2025, Clariant introduced StyroMax™ UL-100, an advanced ethylbenzene dehydrogenation catalyst achieving a steam-to-oil ratio of 0.76, significantly lowering energy intensity in styrene monomer production. In June 2025, LyondellBasell announced selection of its fifth-generation Spheripol polypropylene technology, incorporating advanced non-phthalate catalysts, for a major petrochemical complex in Shaanxi, China. In October 2025, Aramco, Honeywell, and KAUST signed a Joint Development Agreement to develop next-generation crude-to-chemicals catalytic pathways designed to convert crude oil directly into light olefins, redefining feedstock conversion efficiency. In November 2025, Evonik successfully completed a second polyamide reactor trial in Shanghai, doubling regional capacity for long-chain polyamides using proprietary catalyst systems.

Structural consolidation also intensified. In late 2023 and early 2024, LyondellBasell completed the acquisition of a specialized catalyst manufacturing firm to secure supply of high-performance polyolefin catalyst components. In 2025, Honeywell announced its move to acquire Johnson Matthey’s Catalyst Technologies division, significantly expanding its petrochemical and polymerization catalyst portfolio, including applications in renewable fuels and advanced process catalysis. In October 2025 at K 2025, Clariant unveiled its AddWorks™ titanium-based catalyst, scheduled for full commercial launch in 2026. This innovation replaces traditional antimony catalysts in polyester production, enabling lower processing temperatures and heavy-metal-free PET formulations. The development addresses China’s 2024 antimony export restrictions and strengthens the market for antimony-free polyester catalysts and sustainable PET production technologies.

The polymerization catalysts market is increasingly shaped by energy-efficient catalytic systems, heavy-metal-free polyester catalysts, down-gauging polyethylene solutions, crude-to-chemicals process innovation, non-phthalate polypropylene catalysts, and advanced catalyst support materials. Capacity expansions in Asia, vertical integration by major petrochemical players, and regulatory-driven substitution of legacy catalyst chemistries are redefining competitive dynamics across global polymer production chains.

Key Trends and High-Value Opportunities Shaping the Polymerization Catalysts Market

Strategic Shift Toward Single-Site Catalyst Capacity for High-Value Polyolefins

The polymerization catalysts market is undergoing a decisive transition from conventional Ziegler–Natta systems toward single-site catalysts, including metallocenes and constrained geometry catalysts. This shift reflects rising demand for polyolefins with tightly controlled molecular weight distribution, uniform comonomer incorporation, and predictable rheological behavior. These attributes are no longer niche requirements but baseline specifications for medical-grade films, high-clarity packaging, pressure pipes, and impact copolymers used in automotive and infrastructure applications.

Capital allocation patterns confirm this structural change. In late 2024, Reliance Industries announced its Jamnagar New Energy and Materials complex, positioning single-site catalyst-based polyolefin production as a core pillar of its downstream strategy. The facility integrates advanced catalyst systems to support high-purity polyethylene and polypropylene grades required for solar photovoltaic backsheets, fuel cell membranes, and hydrogen infrastructure components. This signals a broader industry pivot where catalyst technology is becoming inseparable from downstream performance differentiation rather than a commodity input.

However, industrial scalability constraints are reshaping catalyst innovation priorities. A March 2025 technical review underscored that traditional metallocene catalysts suffer from rapid deactivation above 120°C in solution polymerization environments. In response, leading producers are accelerating the qualification of non-metallocene early transition metal catalysts using bidentate ligand architectures such as N,N′, N,O, and N,S systems. These catalysts maintain high activity and stereochemical control at elevated temperatures, enabling stable operation in large-scale reactors while preserving the narrow molecular architecture demanded by premium polyolefin grades.

Development of Poison-Tolerant Catalysts for Circular and Bio-Derived Feedstocks

The transition toward circular polymers is exposing a critical limitation of legacy catalyst systems: sensitivity to impurities. Monomers derived from chemical recycling, pyrolysis oils, or bio-based feedstocks often contain trace oxygenates, nitrogen compounds, and sulfur species that irreversibly poison conventional polymerization catalysts. Addressing this challenge has become a strategic priority as regulatory mandates increasingly require recycled content in finished polymer products.

By mid-2025, a new class of poison-tolerant catalyst systems began moving from laboratory validation toward pilot-scale deployment. A notable breakthrough involves air-assisted oxidative recycling processes operating at moderate temperatures between 250°C and 400°C. These systems use oxygen-reactive catalysts to depolymerize mixed polyolefin waste into polymerization-grade monomers while reducing energy consumption by approximately 40% compared with conventional thermal cracking. The resulting monomer streams, while cleaner, still demand catalyst systems engineered for impurity resilience rather than absolute feedstock purity.

Regulatory pressure is amplifying this demand. Amendments to India’s Plastic Waste Management Rules notified in June 2025 mandate 30% recycled content in Category I rigid packaging by 2025–26, rising sharply to 60% by 2028–29. Similar targets across Europe and Southeast Asia are forcing brand owners and resin producers to adopt catalyst platforms that can reliably polymerize recycled monomers without yield loss or product inconsistency. As a result, catalyst suppliers are increasingly competing on feedstock tolerance and circular compatibility, not just polymer performance metrics.

Specialized Polyolefin Elastomer Catalysts for EV Lightweighting and Solar Encapsulants

Polyolefin elastomers represent one of the most commercially attractive downstream opportunities for advanced polymerization catalysts. Produced almost exclusively using metallocene-based systems, POEs offer superior flexibility, impact resistance, and moisture stability compared with traditional PVC and thermoset elastomers. These properties align directly with the lightweighting and durability requirements of electric vehicles and renewable energy systems.

By December 2025, global POE production exceeded 1.35 million metric tons, with demand accelerating across EV battery insulation films, cable jacketing, and interior components. High-performance POE blends now account for approximately 48% of EV battery insulation film usage, driven by their thermal stability and electrical insulation characteristics. From a system-level perspective, substituting PVC with POE-based materials enables up to 12% weight reduction in interior and under-the-hood components, delivering measurable gains in vehicle range and energy efficiency.

The solar sector represents an equally compelling growth vector. More than 30% of newly installed solar panels in 2025 adopted POE encapsulant films instead of conventional EVA. This shift is enabled by catalyst systems that impart superior UV resistance, low moisture permeability, and long-term thermal stability to POE resins. These performance gains can extend photovoltaic module operational lifespans to 25 years or more, positioning catalyst-enabled POE materials as a foundational technology in global renewable energy infrastructure.

High-Temperature Polymerization Catalysts for Engineering Thermoplastics

The expansion of high-performance thermoplastics is creating a parallel, high-margin opportunity for polymerization catalysts capable of operating under extreme chemical and thermal conditions. Materials such as PEEK, PPS, and liquid crystal polymers require catalyst systems that can sustain nucleophilic aromatic substitution or condensation reactions at temperatures ranging from 300°C to 400°C while maintaining precise molecular architecture.

By late 2025, these engineering polymers were increasingly specified as metal replacements in aerospace engines, downhole oil and gas equipment, and chemical processing systems where continuous service temperatures exceed 200°C. Catalyst performance directly determines polymer crystallinity, flow behavior, and dimensional stability, making catalyst selection a critical design variable rather than a background process choice.

In electronics and telecommunications, liquid crystal polymer catalysts are enabling the production of ultra-thin, high-flow resins for 5G and emerging 6G connectors. These specialized catalyst systems ensure exceptionally low dielectric loss and high-frequency signal integrity, attributes that are essential as device architectures move toward higher data rates and miniaturized form factors. As a result, catalyst suppliers capable of supporting both extreme thermal environments and electronic-grade purity are positioned to capture disproportionate value in the high-performance plastics segment.

Polymerization Catalysts Market Share and Segmentation Insights

Ziegler-Natta Catalysts Dominate Global Polyolefin Production Technologies

Ziegler-Natta catalysts accounted for 48.60% of the Polymerization Catalysts Market by catalyst type in 2025, reflecting their long-established role in high-volume polyolefin manufacturing. These catalysts are widely used in polyethylene and polypropylene production due to their reliability, cost efficiency, and compatibility with gas phase, slurry phase, and bulk polymerization processes. Decades of industrial optimization have enabled Ziegler-Natta catalyst systems to deliver consistent polymer morphology, particle size control, and stereoregularity required for commercial polyolefin grades used in packaging, automotive components, and consumer products. In 2025, fourth generation Ziegler-Natta catalyst technologies are improving polypropylene performance, enabling enhanced stiffness, impact resistance, and optical clarity that allow polypropylene materials to compete with higher-cost metallocene catalyst based polymer systems.

Polyethylene Segment Drives Polymerization Catalyst Consumption in Global Polyolefin Manufacturing

Polyethylene represented 52.80% of the Polymerization Catalysts Market by application in 2025, reflecting its position as the highest-volume plastic produced worldwide. High-density polyethylene, low-density polyethylene, and linear low-density polyethylene are used extensively in packaging films, blow molded containers, pipes, and consumer goods, requiring large-scale catalyst consumption across gas phase, slurry phase, and solution polymerization technologies. The scale of global polyethylene production continues to support steady demand for high-performance catalyst systems tailored to specific polymer grades. In 2025, bimodal polyethylene production technologies are gaining traction, utilizing cascade reactor systems and dual catalyst formulations to achieve controlled molecular weight distribution and comonomer incorporation for advanced pipe, film, and blow molding polyethylene applications.

Polymerization Catalysts Market Competitive Landscape

The global polymerization catalysts market is evolving toward single-site metallocene catalysts, titanium-based alternatives, and circular polymerization solutions. Competitive intensity is driven by demand for high-purity polymers in EV, medical, and packaging applications, alongside AI-driven catalyst design and chemical recycling technologies.

LyondellBasell Strengthens Polyolefin Dominance with Avant™ Catalysts and MoReTec Circular Technology

LyondellBasell Industries remains a global leader in polymerization catalysts, leveraging its Avant™ catalyst family for high-performance polypropylene and polyethylene production. The company is restructuring its European asset base in 2026 to prioritize investments in MoReTec chemical recycling technologies, converting plastic waste into virgin-grade feedstock. Despite margin pressures in 2025, LYB achieved $800 million in savings and raised its 2026 target to $1.3 billion to support catalyst innovation. A new propylene production unit at Channelview utilizes advanced dimerization catalysts to enhance output efficiency. Its Spheripol and Spherizone licensing platforms ensure widespread adoption of its catalyst technologies globally. Strategy centers on circular economy integration, process licensing leadership, and advanced polyolefin catalyst systems.

W. R. Grace Leads Catalyst Customization with ActivCat® and Non-Phthalate Polyolefin Solutions

W. R. Grace & Co. dominates the independent catalyst segment with highly customizable polymerization catalyst systems. Its ActivCat® technology enhances metallocene catalyst performance, enabling production of high-clarity and high-toughness metallocene polyethylene (mPE). Grace catalysts are validated for PE-RT pipe applications, ensuring superior molecular weight distribution and long-term durability. The company expanded its CONSISTA® and HYAMPP® catalyst lines with non-phthalate internal donors to meet regulatory requirements in medical and food-contact polymers. Its SYLOID® and LUDOX® silica platforms serve as foundational catalyst carriers across the industry. Strategy emphasizes catalyst flexibility, regulatory compliance, and high-performance polymer applications.

Clariant Advances Titanium-Based and Chromium-Free Catalysts for Sustainable Polymer Production

Clariant AG is positioning itself as a sustainability leader in polymerization catalysts with a focus on heavy-metal-free solutions. The AddWorks titanium-based catalysts provide an antimony-free alternative for PET production, addressing global supply constraints and regulatory pressure. Its HySat™ platform eliminates hazardous chromium compounds, earning recognition for innovation in hydrogenation catalysts. Through its EDHOX™ joint venture with Linde, Clariant enables ethane-to-ethylene conversion at lower temperatures, reducing CO₂ emissions by over 60%. The company’s catalyst innovations align with REACH compliance and low-carbon petrochemical production. Strategy focuses on sustainable catalysis, emission reduction, and next-generation polyester and olefin technologies.

Evonik Expands Circular Polymerization with Purocel™ Catalysts and Alkoxide Production Scale

Evonik Industries is a key innovator in catalysts for circular polymerization and feedstock upgrading. Its Purocel™ catalyst series enhances pyrolysis oil quality, enabling seamless integration into conventional polymerization systems. The company commissioned a world-scale alkoxides plant in Singapore, strengthening its position in homogeneous catalyst production for specialty polymers. Evonik reported €1.87 billion EBITDA in 2025, with growth driven by advanced materials and catalyst applications. Its partnership with Oerlikon Barmag supports PET chemical recycling, closing the loop in textile and packaging industries. Strategy emphasizes circular feedstock utilization, specialty catalyst development, and sustainable polymer chemistry.

INEOS Enhances Operator-Centric Catalyst Systems with INcat™ Portfolio and Metallocene Innovation

INEOS is strengthening its position in polymerization catalysts through its INcat™ portfolio, focusing on operational efficiency and process flexibility. The INcat™ P series offers non-phthalate catalysts optimized for multiple polymerization processes, enabling production of advanced impact copolymers. Its INcat™ M metallocene catalysts support differentiated LLDPE and HDPE production with direct reactor injection, eliminating pre-polymerization steps. INEOS is expanding compatibility with third-party technologies to capture a larger share of the global catalyst market. Its expertise as a polymer producer ensures catalysts are engineered for reduced fouling and enhanced throughput. Strategy centers on operability, process optimization, and advanced metallocene systems.

Mitsui Chemicals Drives Single-Site Catalyst Innovation for Electronics and Healthcare Applications

Mitsui Chemicals is a pioneer in single-site and metallocene catalyst technologies, focusing on high-value functional polymers. The company is restructuring to prioritize specialty materials and advanced catalyst R&D, targeting electronics and healthcare sectors. Its collaboration with Dispelix highlights the role of catalysts in producing high-refractive-index polymers for AR applications. The MCI-iCONM Co-Creation Lab advances nanomedicine development, where precise polymer architecture is critical. Mitsui continues to lead academic and industrial innovation through its Catalysis Science Awards program. Strategy emphasizes precision polymerization, specialty applications, and next-generation catalyst technologies.

China: State-Directed Scale-Up and Localization of High-End Polyolefin Catalysts

China’s polymerization catalysts industry in 2025 is being reshaped by coordinated industrial policy and accelerated localization of advanced catalyst systems. In September 2025, the Ministry of Industry and Information Technology, together with six central departments, issued a petrochemical sector work plan for 2025 to 2026 that prioritizes breakthroughs in high-end polyolefin catalysts as a strategic lever for sustained industrial upgrading. This policy direction has translated into tangible capacity and technology deployments. By early 2025, China Coal Shaanxi Company successfully doubled polypropylene capacity at its Yulin complex to 600 KTA using W.R. Grace UNIPOL® process technology and CONSISTA® catalyst systems, reinforcing the role of licensed catalyst platforms in China’s large-scale polymer expansion.

Self-sufficiency remains a central objective. Government mandates now target an increase in domestic production of specialty chemical intermediates to above 90% by 2026, directly stimulating localized manufacturing of Ziegler–Natta and metallocene catalyst variants. Parallel investments in advanced polymerization chemistry are evident. In November 2025, BASF commissioned a new Controlled Free Radical Polymerization production line in Nanjing for high-performance dispersants used in automotive coatings. Sustainability and process efficiency are also being enforced, with chemical clusters required to integrate hydrogen utilization and digital process optimization to lower emissions during catalyst synthesis. Additionally, Evonik doubled long-chain polyamide capacity at its Shanghai site in November 2025, deploying advanced catalyst reactors to meet rising demand from electric vehicle battery housing applications. Collectively, these developments position China as a market where scale, policy alignment, and localized catalyst innovation converge.

Germany: Advanced Catalyst Engineering and Digitalized Polymerization Systems

Germany’s polymerization catalysts market in 2025 is defined by precision engineering, regulatory stewardship, and early commercialization of next-generation production technologies. In December 2025, BASF announced the planned Q1 2026 start-up of a commercial-scale 3D-printed catalyst plant in Ludwigshafen. The X3D technology enables complex catalyst geometries with higher surface area, improving reactor productivity and process control in polyolefin and specialty polymer applications. Regulatory visibility also improved, as the European Commission confirmed in late 2025 that the REACH revision introducing new registration requirements for polymers and their catalysts has been postponed to 2026, providing temporary planning clarity for catalyst manufacturers.

Germany is simultaneously leading implementation of the Omnibus VI package, which streamlines chemical marketing rules while strengthening competitiveness for small and mid-sized catalyst producers. Innovation is extending beyond traditional metal-based systems. In October 2025, BASF and IFF launched a collaboration on Designed Enzymatic Biomaterials, advancing enzyme-based bio-catalysts for sustainable industrial cleaning applications. Digital transformation is equally prominent. At K 2025, German producers demonstrated polymerization lines equipped with Digital Twins capable of real-time catalyst dosage optimization based on feedstream variability. During the 2025 National Catalysis Conference, industry leaders emphasized Single-Site Catalysts as a cornerstone for achieving the EU’s green transformation objectives, particularly in enabling fully recyclable plastics. Germany’s market thus reflects a balance of regulatory foresight, digitalization, and frontier catalyst design.

United States: High-Purity Systems, AI-Driven Reactors, and Alternative Hydrogen Pathways

The United States polymerization catalysts landscape in 2025 is characterized by convergence between healthcare-grade polymer requirements, artificial intelligence integration, and low-carbon process innovation. In October 2025, LyondellBasell expanded its Purell healthcare polymer portfolio across North America, relying on high-purity catalyst systems compliant with USP and EU Pharmacopeia standards for medical syringes and intravenous containers. This expansion underscores the growing importance of catalyst purity and traceability in regulated polymer applications.

Innovation at the catalyst support level is also advancing. During summer 2025, W.R. Grace presented Catalagram® briefings highlighting new solid silica supports for enzyme immobilization, signaling cross-sector applications that bridge polymerization chemistry and pharmaceutical synthesis. U.S.-based laboratories further showcased AI-driven reactor systems in late 2025, where automated reaction cycles dynamically adjust conditions to maximize yield while minimizing losses of precious metal catalysts. At the intersection of energy and materials, ExxonMobil and BASF finalized a joint agreement in 2025 to construct a methane pyrolysis hydrogen demonstration unit producing high-purity carbon byproducts suitable for polymer reinforcement. These developments position the United States as a market where digital intelligence, regulatory-grade performance, and alternative process routes are shaping catalyst demand.

India: Digital Catalyst Management and Domestic Downstream Expansion

India’s polymerization catalysts market is entering a structurally transformative phase driven by digitalization initiatives and expanding downstream polymer investments. The government has scheduled the Gujarat Chem & Petchem Conference for May 2026, with a central theme focused on digital revolutions in catalyst management aimed at reducing reliance on imported specialty additives. This policy emphasis aligns with accelerating investments in domestic polymer processing. In 2025, HMEL announced a ₹2,600 crore investment in polypropylene downstream and fine chemical projects, creating secondary demand for high-performance polymerization initiators and catalyst systems.

Strategic assessments released by Indian research agencies in late 2025 identified India as a significant driver for metallocene catalyst adoption, particularly in automotive polymers, reflecting the country’s growing role in lightweighting and performance plastics. On the innovation infrastructure side, the Office of the Principal Scientific Adviser to the Government of India announced plans in 2025 to expand national Science and Technology clusters from eight to twenty-five by 2028, with dedicated focus areas covering advanced materials and performance additives. These coordinated initiatives indicate that India’s catalyst market trajectory is increasingly shaped by domestic capability building, digital process control, and downstream polymer diversification.

Russia and CIS: Building End-to-End Catalyst Sovereignty

Russia and the broader CIS region are pursuing catalyst self-reliance as a strategic priority within their polymer industries. In March 2025, SIBUR announced construction of a new catalyst factory scheduled to commence operations in Q2 2025. This facility represents the first site in the CIS capable of producing the full spectrum of polymerization catalysts required for polyethylene and polypropylene manufacturing. The initial phase focuses on chromium-based catalysts, which are critical for film-grade and blown polyethylene used in fuel tanks and industrial canisters.

The project targets annual production exceeding one thousand tons and is explicitly designed to secure technological independence for basic polymer production by 2027. By internalizing catalyst manufacturing, Russia and CIS producers aim to mitigate supply chain risks and reduce exposure to external technology constraints. As a result, the region is emerging as a self-contained market where polymerization catalyst development is closely tied to national industrial resilience objectives.

Comparative Overview of Country-Level Developments

Polymerization Catalysts Market County Level Snapshot

|

Country / Region

|

Strategic Focus in 2025

|

Implications for Polymerization Catalysts

|

|

China

|

Policy-led scale-up, catalyst localization, green synthesis mandates

|

Accelerated demand for domestic Ziegler–Natta and metallocene systems

|

|

Germany

|

3D-printed catalysts, digital twins, bio-catalysts

|

Higher reactor efficiency and advanced catalyst engineering

|

|

United States

|

Medical-grade purity, AI reactors, methane pyrolysis

|

Convergence of digital control and high-performance catalyst systems

|

|

India

|

Digital catalyst management, downstream PP investments

|

Rising adoption of advanced initiators and metallocenes

|

|

Russia & CIS

|

Catalyst sovereignty, chromium catalyst production

|

Reduced import dependence and regional self-sufficiency

|

Polymerization Catalysts Market Report Scope

Polymerization Catalysts Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.3 Billion

|

|

Market Size (2034)

|

$9.4 Billion

|

|

Market Growth Rate

|

4.5%

|

|

Segments

|

By Catalyst Type (Ziegler-Natta Catalysts, Metallocene Catalysts, Chromium Catalysts, Specialty Catalysts), By Process Technology (Gas Phase Processes, Slurry Phase Processes, Solution Phase Processes, Bulk Phase Processes), By Application (Polyethylene, Polypropylene, Specialty Polymers), By End-Use Industry (Packaging, Automotive, Building & Construction, Electronics, Consumer Goods)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

W. R. Grace & Co., LyondellBasell Industries NV, BASF SE, Mitsui Chemicals Inc., Evonik Industries AG, INEOS Group, Clariant AG, Chevron Phillips Chemical Company, Sinopec, Albemarle Corporation, Johnson Matthey PLC, Idemitsu Kosan Co. Ltd., SIBUR, Univation Technologies LLC, Toho Titanium Co. Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Polymerization Catalysts Market Segmentation

By Catalyst Type

- Ziegler-Natta Catalysts

- Metallocene Catalysts

- Chromium Catalysts

- Specialty Catalysts

By Process Technology

- Gas Phase Processes

- Slurry Phase Processes

- Solution Phase Processes

- Bulk Phase Processes

By Application

- Polyethylene

- Polypropylene

- Specialty Polymers

By End-Use Industry

- Packaging

- Automotive

- Building & Construction

- Electronics

- Consumer Goods

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Polymerization Catalysts Industry

- W. R. Grace & Co.

- LyondellBasell Industries NV

- BASF SE

- Mitsui Chemicals Inc.

- Evonik Industries AG

- INEOS Group

- Clariant AG

- Chevron Phillips Chemical Company

- Sinopec

- Albemarle Corporation

- Johnson Matthey PLC

- Idemitsu Kosan Co. Ltd.

- SIBUR

- Univation Technologies LLC

- Toho Titanium Co. Ltd.

*- List not Exhaustive