Homogeneous Catalyst Market to Reach $16.7 Billion by 2034 at 6% CAGR Driven by Asymmetric Hydrogenation, Flow Chemistry, and Net-Zero Chemical Synthesis

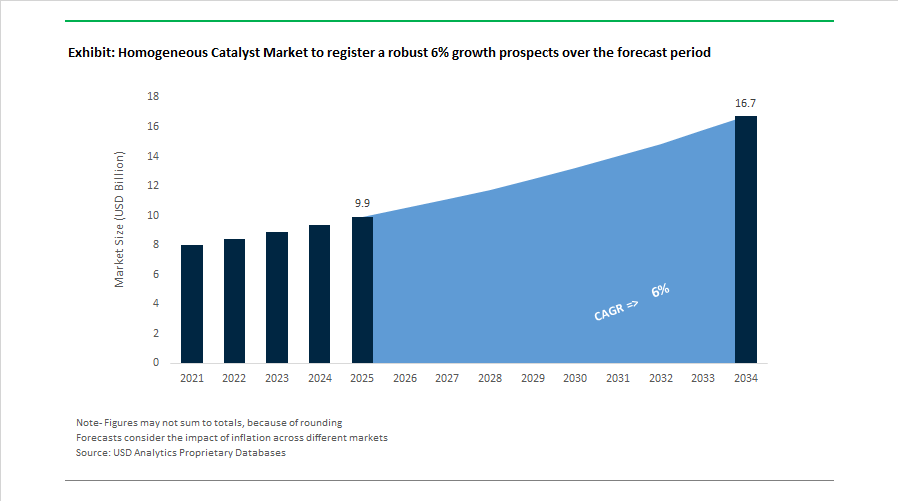

The Homogeneous Catalyst Market is projected to grow from $9.9 billion in 2025 to $16.7 billion by 2034, registering a CAGR of 6%. Growth is being driven by rising demand for soluble transition-metal complexes in pharmaceutical synthesis, asymmetric hydrogenation, C–H activation chemistry, green hydrogen production, and power-to-methanol applications. Homogeneous catalysts, particularly iridium, ruthenium, rhodium, and titanium-based complexes, are increasingly preferred for high selectivity, tunable ligand design, and atom-efficient reaction pathways. The market is further shaped by sustainability mandates, metal recycling programs, and the shift from batch to continuous flow chemistry in fine chemical and active pharmaceutical ingredient (API) manufacturing.

Strategic investments and technology launches accelerated through 2024. In January 2024, BASF Process Catalysts announced a collaboration with Envision Energy to optimize green hydrogen and CO2 conversion into e-methanol, highlighting the growing role of homogeneous catalytic systems in power-to-methanol plants. In June 2024, Heraeus acquired McCol Metals to strengthen iridium recovery capabilities, enhancing closed-loop recycling for spent soluble catalysts used in acetic acid and hydrogen production. In September 2024, Johnson Matthey announced a breakthrough in iridium-based C–H activation complexes, enabling more direct molecular editing and reducing synthetic steps in fine chemical manufacturing. In November 2024, Heraeus launched the Actydon brand to consolidate its precious metal homogeneous catalyst portfolio for hydrogen and electrolysis applications. In December 2024, BASF inaugurated its Catalyst Development and Solids Processing Center in Ludwigshafen, creating a pilot-scale hub to accelerate the industrialization of innovative homogeneous complexes for green transformation projects.

Innovation momentum intensified in 2025 with a strong focus on pharmaceutical and sustainable polymer synthesis. In March 2025, Johnson Matthey Catalysis & Chiral Technologies launched a new generation of asymmetric hydrogenation catalysts designed for the precise construction of chiral APIs. In April 2025, Johnson Matthey Life Science Technologies published research on its C1-720 homogeneous catalyst platform, demonstrating a hydrogen borrowing mechanism for the atom-efficient synthesis of polyesterether from ethylene glycol. In May 2025, Honeywell signed a definitive agreement to acquire Johnson Matthey’s Catalyst Technologies business for £1.8 billion, integrating JM’s homogeneous and specialty catalyst expertise into Honeywell’s UOP platform, with closure expected in early 2026. In October 2025, Evonik Industries introduced the Noblyst® F portfolio tailored for continuous flow chemistry, targeting pharmaceutical and fine chemical producers transitioning away from batch reactors. During the same month at K 2025, Clariant debuted AddWorks™ titanium-based homogeneous catalyst solutions as a sustainable alternative to antimony catalysts in polyester production, addressing supply disruptions linked to China’s 2024 antimony export restrictions.

Regional capacity expansion and localization strategies are extending into 2026. Following its 2025 Noblyst® launch, Evonik announced late-2025 investment plans to expand specialty catalyst production and technical service laboratories in India and China through 2026, supporting rapidly growing pharmaceutical manufacturing hubs. The pending Honeywell–Johnson Matthey transaction is expected to further consolidate licensing, catalyst supply, and net-zero process integration within the global homogeneous catalyst ecosystem. Across hydrogen production, asymmetric synthesis, polymer catalysis, and flow chemistry applications, the market is increasingly defined by metal recovery systems, ligand engineering, ultra-high selectivity, and integrated sustainability frameworks aligned with advanced chemical manufacturing standards.

Homogeneous Catalyst Market Trends and Opportunities

Strategic Capacity Consolidation and Portfolio Rationalization

The homogeneous catalyst market is undergoing a decisive consolidation phase as leading chemical producers divest non-core assets and reallocate capital toward high-margin, sustainability-aligned platforms. This restructuring is centralizing the supply of traditional homogeneous catalysts, including rhodium and cobalt complexes used in hydroformylation, among a smaller group of specialized licensors and manufacturers. For oxo-alcohol and plasticizer producers, this is reshaping long-term sourcing strategies, licensing costs, and catalyst availability.

A major inflection point occurred in May 2025 when Johnson Matthey announced the sale of its Catalyst Technologies business to Honeywell for £1.8 billion, equivalent to roughly $2.3 billion. Scheduled for completion in early 2026, the transaction transfers world-leading licensing and catalyst manufacturing capabilities for methanol and hydrogen, signaling a strategic retreat by legacy players from commodity-linked catalyst segments. This move underscores a broader market reality in which scale and capital intensity are becoming decisive advantages.

Operational efficiency is also driving portfolio rationalization. Clariant has implemented a CHF 80 million cost-savings program through 2025, including the closure of two production sites and multiple production lines. Despite its catalyst segment delivering a robust EBITDA margin of 22.5% in Q2 2025, the company is concentrating resources on chromium-free platforms such as HySat™, reflecting tighter REACH compliance requirements and customer demand for lower environmental impact. In parallel, structural synergies are emerging through regional consolidation. In September 2025, Asahi Kasei, Mitsui Chemicals, and Mitsubishi Chemical formed a joint limited liability partnership to manage ethylene assets in Western Japan. This shared infrastructure model optimizes catalyst utilization and helps offset margin pressure highlighted in 2025 industry outlooks.

Intellectual Property Surge in CO2 Valorization Pathways

Carbon utilization has moved from pilot experimentation to a strategic intellectual property race, with homogeneous catalysts at the center due to their superior selectivity and ability to operate under milder conditions. These advantages are accelerating deployment in carbon-to-chemicals pathways, where process efficiency and molecular control are critical to commercial viability.

In October 2025, Carbon Clean and NTPC successfully produced methanol from captured flue gas at the Vindhyachal Super Thermal Power Station. The pilot converts approximately 20 tons per day of waste CO2 into value-added chemicals using a specialized catalytic hydrogenation route, illustrating how homogeneous catalysts are enabling carbon capture integration at utility scale. Innovation is also extending into polymer chemistry. At the CO2-based Fuels and Chemicals Conference 2025, Far Eastern New Century unveiled its TopGreen® CO₂-based non-isocyanate polyurethane platform. This technology incorporates more than 50% carbon content and reduces manufacturing emissions by 58% versus conventional TPU, relying on novel homogeneous catalysts that eliminate toxic phosgene intermediates.

The pace of innovation is accelerating further through digital tools. According to late-2025 industry analysis, AI-driven research has doubled the rate of catalyst and ligand discovery. Companies are now mining more than 15 million existing patents using generative AI to design new ligand architectures that stabilize CO2 for polymerization and fuel synthesis. This intellectual property surge is raising entry barriers and reinforcing the strategic value of proprietary homogeneous catalyst systems.

Advanced Late-Transition Metal Catalysts for Designer Polyolefins

A high-growth opportunity is emerging around late-transition metal homogeneous catalysts based on iron, cobalt, and nickel complexes. These systems, often featuring iminopyridine or phosphine-sulfonate ligands, enable the production of ultra-high molecular weight polyethylenes and tailored elastomers that are not achievable with conventional metallocene catalysts. Recent 2025 technical reviews highlight nickel and palladium complexes sustaining activities up to 22.0 × 10⁶ g PE per mol per hour at industrial temperatures near 80°C, supporting the manufacture of thermoplastic elastomers with tensile strengths exceeding 20 MPa and elastic recovery approaching 60%.

Precise control over polymer branching is a core differentiator. Iron-based iminopyridine catalysts allow manufacturers to tune linearity and branching density, enabling mono-material packaging structures that replicate the barrier and mechanical performance of multi-layer laminates. This directly supports the European Union’s 2030 circular economy targets for fully recyclable packaging. Beyond packaging, demand is accelerating in medical and aerospace applications, where ultra-high molecular weight polyethylene is used in implants and lightweight structural components. The ability to engineer properties through ligand design positions these catalysts as a premium, high-margin offering for specialty chemical suppliers.

Ruggedized Homogeneous Systems for Distributed Modular Manufacturing

The rise of modular and decentralized chemical production is creating demand for homogeneous catalysts capable of operating reliably under non-ideal feedstock conditions. Small-scale plants located near biogas sources or renewable energy hubs require catalysts that tolerate impurities such as sulfur and moisture without rapid deactivation. Data presented at the 2025 AIChE Annual Meeting indicate that modularization can reduce total project costs by roughly 30%, with about 65% of labor shifted to factory-controlled environments.

This model is gaining traction in the bioeconomy. In November 2025, the Tech Tour Bio-based Industries program highlighted dozens of startups deploying advanced catalysts in compact, distributed units. Unibio, for example, is using patented vertical loop bioreactors and robust catalyst systems to convert methane-rich gases into sustainable proteins and specialty chemicals. Policy incentives are reinforcing this opportunity. Governments in India and the European Union are offering incentives ranging from 50 to 100% for select carbon capture and utilization projects, creating a strong market for plug-and-play homogeneous catalyst packages that can be deployed rapidly in containerized modular plants.

Homogeneous Catalyst Market Share and Segmentation Insights

Transition Metal Catalysts Lead the Homogeneous Catalyst Market in Advanced Chemical Synthesis

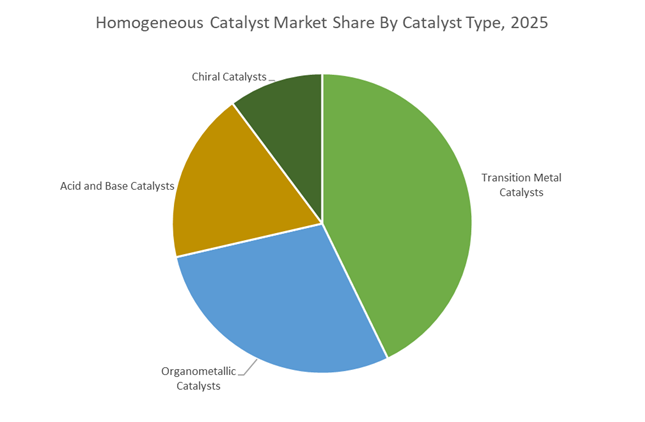

Transition Metal Catalysts accounted for 42.80% of the Homogeneous Catalyst Market share in 2025, making them the most widely used catalyst type across fine chemical and pharmaceutical synthesis processes. These catalysts typically involve complexes of palladium, nickel, copper, ruthenium, and rhodium, which provide exceptional catalytic activity and selectivity in organic reactions involving carbon–carbon and carbon–heteroatom bond formation. Transition metal catalysts are fundamental to widely used chemical transformations including Suzuki coupling, Heck reactions, Negishi coupling, hydrogenation, and hydroformylation, which are critical in the synthesis of pharmaceutical intermediates, agrochemicals, and specialty chemicals. Their ability to operate under relatively mild reaction conditions while delivering high selectivity makes them indispensable for complex organic synthesis. In 2025, research and commercial development are increasingly focused on earth-abundant transition metals such as nickel, iron, cobalt, and copper. These metals provide cost advantages and improved sustainability compared with precious metal catalysts. Advances in catalyst ligand design and reaction optimization have enabled nickel-catalyzed cross-coupling reactions and iron-based hydrogenation systems to reach commercial viability in selected pharmaceutical and fine chemical manufacturing processes.

Pharmaceutical Synthesis Drives the Largest Demand for Homogeneous Catalysts

Pharmaceutical Synthesis represented 38.60% of the Homogeneous Catalyst Market share in 2025, establishing the pharmaceutical industry as the leading consumer of homogeneous catalytic technologies. Modern drug manufacturing requires highly selective catalytic reactions capable of assembling complex molecular structures with precise stereochemistry, and homogeneous catalysts provide the molecular-level control necessary to achieve these outcomes. Catalytic processes such as asymmetric hydrogenation, palladium-catalyzed cross-coupling, and selective oxidation reactions are widely used in the production of active pharmaceutical ingredients (APIs) and key pharmaceutical intermediates. Because pharmaceutical compounds typically have high commercial value and stringent purity requirements, manufacturers are willing to adopt advanced catalytic systems that improve yield, reaction efficiency, and product selectivity. In 2025, pharmaceutical manufacturers are increasingly combining homogeneous catalysis with continuous flow chemistry platforms, which provide improved heat transfer, enhanced reaction control, and safer handling of reactive intermediates. Continuous flow reactors designed for palladium-catalyzed cross-coupling and hydrogenation reactions allow efficient catalyst utilization while simplifying downstream separation processes, supporting the growing adoption of flow-based pharmaceutical manufacturing technologies.

Competitive Landscape in Homogeneous Catalyst Market

BASF SE Advances AI-Driven Catalyst Engineering and Additive Manufacturing

BASF SE continues to expand its leadership in homogeneous catalyst systems through digitalization and advanced manufacturing. In Q1 2026, the company initiated commercial-scale operations at its 3D-printed catalyst plant in Ludwigshafen using proprietary X3D technology to optimize catalyst geometry and flow dynamics. BASF has also deployed its first AI-enabled reactor, capable of autonomously optimizing reaction cycles to maximize yield and selectivity during catalyst development. The Zhanjiang Verbund site in China, operational since late 2025, strengthens regional supply of next-generation organometallic catalysts. BASF’s portfolio includes liquid-phase transition metal catalysts and loopamid, a catalytic Nylon 6 recycling technology that supports circular polymer production and low-carbon chemical manufacturing.

Evonik Industries Expands Continuous Flow and Circular Catalysis

Evonik Industries AG focuses on specialty homogeneous catalysts tailored for pharmaceutical manufacturing and circular plastics processing. The Noblyst F series is being scaled globally to support compact continuous flow reactors, replacing conventional batch synthesis and improving safety, throughput, and reaction control. In August 2025, Evonik inaugurated a world-scale alkoxides plant in Singapore, reinforcing supply for biodiesel transesterification and polymer catalyst markets. The company’s Purocel series enhances pyrolysis oil upgrading, facilitating chemical recycling of post-consumer plastics into high-grade polymers. Evonik is also transitioning toward low-emission amine catalysts such as DABCO NE to meet tightening VOC regulations in polyurethane foam production.

Clariant AG Strengthens Digital Catalyst Management and Ligand Precision

Clariant AG has repositioned itself as a high-value specialty catalyst provider with emphasis on digital optimization and regional manufacturing resilience. The CLARITY platform, now active in 38 countries, enables real-time catalyst performance monitoring and lifecycle management. Clariant reported a 17.8% EBITDA margin in FY 2025, supported by operational efficiency improvements and cost discipline. The company is targeting more than 50% localized production in China by 2026 to mitigate supply chain volatility. Its AddWorks and OxoPhos ligand systems provide molecular-level precision for hydroformylation, carbonylation, and polymerization reactions, ensuring high conversion rates and product selectivity in fine chemical synthesis.

Honeywell UOP Consolidates Renewable Fuel Catalyst Capabilities

Honeywell UOP is reshaping the catalyst industry through its £1.325 billion acquisition of Johnson Matthey’s Catalyst Technologies business, expected to close by August 2026. This transaction expands Honeywell’s installed base in syngas, ammonia, and methanol catalysts and strengthens its renewable fuels portfolio. The company’s UOP Ecofining and eFining technologies are being deployed in large-scale sustainable aviation fuel projects, including a Jiutai Group facility designed to produce 100,000 tons of SAF annually. With integration of homogeneous catalytic systems into green fuel production pathways, Honeywell is positioned to lead decarbonized refining, hydrogen processing, and bio-feedstock upgrading technologies.

Albemarle Corporation Restructures Catalyst Portfolio for Energy Transition

Albemarle Corporation is realigning its catalyst portfolio to enhance financial flexibility and concentrate on lithium-based energy transition markets. In 2026, the company agreed to sell a 51% controlling stake in its Ketjen catalyst business to KPS Capital Partners for approximately $660 million while retaining its Performance Catalyst Solutions segment and a 49% ownership interest in the broader Ketjen entity. Through Ketjen, Albemarle continues to supply organometallic and precious metal catalysts used in polyolefin polymerization and clean fuels refining. Proceeds from divestitures are being redirected toward lithium hydroxide capacity expansion for electric vehicle battery applications, strengthening its capital structure.

Johnson Matthey Focuses on Precious Metal Homogeneous Catalysts and Circularity

Johnson Matthey is pivoting toward a Precious Metals and Circularity strategy, concentrating on homogeneous platinum group metal catalysts for highly selective synthesis. The company is advancing asymmetric hydrogenation technologies using platinum, palladium, rhodium, and ruthenium complexes for oncology and antiviral pharmaceutical manufacturing. Its Gusev catalysts and tethered ruthenium II complexes enable efficient hydrogenation of ketones and imines with superior enantioselectivity. Johnson Matthey retains its Catalyst Recovery and Recycling services, offering a closed-loop model that recovers and refines precious metals to reduce supply risk and environmental impact. The integration of homogeneous catalysis with biocatalytic cascades further strengthens its position in advanced chiral molecule synthesis.

China: Policy-Led Scale-Up, Circular Chemistry, and Closed-Loop Metal Stewardship

China’s homogeneous catalyst industry is advancing through coordinated industrial policy, circular chemistry deployment, and tighter stewardship of critical metals. In late 2025, the Ministry of Industry and Information Technology released a petrochemical growth plan for 2025–2026 that targets average annual added-value growth above 5% for the chemical sector. The plan explicitly mandates breakthroughs in high-end electronic chemicals and selective homogeneous catalysts for fine chemical synthesis, signaling sustained support for ligand engineering, organometallic systems, and high-selectivity reaction pathways.

Commercial execution is visible across textiles, fine chemicals, and energy transition pilots. In January 2025, BASF and Sinopec operationalized the first commercial loopamid production facility at Caojing in Shanghai, using specialized homogeneous catalytic processes to enable textile-to-textile recycling of Polyamide 6 with a documented 70% reduction in CO2 emissions. At the research-to-scale interface, recognition at the National Congress on Catalysis in December 2025 accelerated adoption of single-atom catalysis concepts, now progressing to thousand-ton pilot plants for cellulose-to-ethylene glycol conversion. Provincial clustering reinforces this momentum. Fujian and Guangdong launched high-end catalyst parks by 2026, offering tax exemptions for developers of rhodium-based homogeneous systems for domestic hydroformylation. Concurrently, tighter export controls and monitoring of ruthenium and iridium recovery in 2025–2026 are pushing pharmaceutical manufacturers toward closed-loop catalyst leasing models. The decarbonization agenda extends to fertilizers, with a state-backed Inner Mongolia pilot testing organometallic homogeneous catalysts for low-pressure ammonia synthesis to support a 2030 low-emissions target.

Germany: Continuous-Flow Transition, SVHC Substitution, and Low-Carbon Process Integration

Germany’s homogeneous catalyst landscape is being reshaped by regulatory substitution, continuous-flow adoption, and climate-linked financing. In 2026, BASF announced an industrial expansion at Ludwigshafen to deploy X3D catalysts. While X3D is a shaping platform, the investment is directed at housing high-performance homogeneous-on-heterogeneous tethered systems that optimize flow, heat transfer, and residence time in pharmaceutical reactors. This approach aligns with Germany’s broader shift from batch to continuous processing.

Regulatory change is accelerating safer chemistries. Following 2025 updates to EU REACH on substances of very high concern, Clariant commercialized the HySat chromium-free platform, eliminating hexavalent chromium in hydrogenation while maintaining selectivity above 99%. Innovation awards underscore performance gains. In October 2025, a joint venture between Clariant and Linde received top recognition for EDHOX technology, a one-step ethane conversion to ethylene and acetic acid that cuts Scope 1 CO2 emissions by at least 60%. Policy-backed financing further supports change. Germany’s 2026 Climate Contracts program provides subsidies for replacing energy-intensive batch operations with homogeneous continuous-flow catalysis, benefiting firms such as Evonik. In parallel, BASF and ExxonMobil signed a November 2025 collaboration on methane pyrolysis using specialized catalytic environments to produce low-emission hydrogen with substantially lower electricity demand than electrolysis.

United States: Capex Modernization, Ligand Reformulation, and SAF Conversion

The United States homogeneous catalyst industry is advancing through capital modernization, regulatory-driven reformulation, and sustainable fuels deployment. According to the American Chemistry Council, capital spending reached USD 34 billion by early 2025, with a material share directed to facilities reliant on rhodium and palladium homogeneous catalysts for carbonylation and hydroformylation. These investments emphasize reactor upgrades, ligand efficiency, and impurity control for specialty intermediates.

Regulatory guidance is reshaping ligand choices. The U.S. Environmental Protection Agency issued 2026 guidance restricting certain fluorinated ligands, prompting formulators to pivot toward phosphine-free homogeneous systems for specialty coatings and adhesives. Energy transition incentives are accelerating scale-up. Under the Inflation Reduction Act, four Midwest biorefineries slated for 2026 completion are implementing homogeneous deoxygenation catalysts to convert corn-derived ethanol into high-purity jet fuel. Specialty applications extend to oil and gas. Nouryon launched a Texas innovation center in June 2025 focused on homogeneous additives that enhance catalytic breaking of heavy hydrocarbons under high pressure, improving extraction efficiency and selectivity.

South Korea: Semiconductor-Grade Selectivity and AI-Enabled Discovery

South Korea’s homogeneous catalyst industry is tightly coupled to semiconductor leadership and AI-enabled molecular design. A government support package exceeding USD 20 billion for the semiconductor sector in 2025 earmarked funding for the development of high-purity etching chemicals synthesized via ultra-selective homogeneous catalysis. These efforts align with national priorities to localize critical materials and achieve parts-per-trillion impurity thresholds.

Technology acceleration is evident in discovery workflows. In late 2025, Taiyo Nippon Sanso and local partners integrated AI-based molecular design to reduce trial-and-error cycles in transition-metal complex discovery by 40%. Manufacturing scale followed. In 2026, SK Materials operationalized a new precursor line using homogeneous organometallic catalysts to deliver ppt-level purity for sub-3nm chip nodes, reinforcing South Korea’s position in electronic chemicals with stringent purity demands.

Summary Table: Country-Level Strategic Signals in the Homogeneous Catalyst Industry

Homogeneous Catalyst Market County Level Snapshot

|

Country

|

Primary Driver

|

Core Catalyst Focus

|

Structural Implication

|

|

China

|

MIIT growth plan, circular economy

|

Selective homogeneous systems, SAC

|

Scale-up, closed-loop metals, decarbonization

|

|

Germany

|

REACH substitution, climate contracts

|

Continuous-flow, chromium-free platforms

|

Low-carbon processing leadership

|

|

United States

|

Capex surge, EPA guidance, IRA

|

Carbonylation, deoxygenation

|

Modernization and SAF conversion

|

|

South Korea

|

Semiconductor policy, AI design

|

Ultra-selective organometallics

|

Ppt purity and rapid discovery

|

Homogeneous Catalyst Market Report Scope

Homogeneous Catalyst Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$9.9 Billion

|

|

Market Size (2034)

|

$16.7 Billion

|

|

Market Growth Rate

|

6%

|

|

Segments

|

By Catalyst Type (Organometallic Catalysts, Transition Metal Catalysts, Chiral Catalysts, Acid and Base Catalysts), By Application (Petrochemical Processing, Polymerization, Pharmaceutical Synthesis, Fine Chemicals), By End-Use Industry (Pharmaceuticals and Biomedical, Chemicals and Petrochemicals, Automotive, Plastics and Polymer Manufacturing, Energy and Power Generation)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Johnson Matthey Plc, Evonik Industries AG, Clariant AG, Umicore N.V., Dow Inc., Eastman Chemical Company, W. R. Grace & Co., Sinopec Catalyst Company, Axens, Heraeus Holding GmbH, Solvay S.A., Mitsubishi Chemical Group, Strem Chemicals, Takasago International Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Homogeneous Catalyst Market Segmentation

By Catalyst Type

- Organometallic Catalysts

- Transition Metal Catalysts

- Chiral Catalysts

- Acid and Base Catalysts

By Application

- Petrochemical Processing

- Polymerization

- Pharmaceutical Synthesis

- Fine Chemicals

By End-Use Industry

- Pharmaceuticals and Biomedical

- Chemicals and Petrochemicals

- Automotive

- Plastics and Polymer Manufacturing

- Energy and Power Generation

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Homogeneous Catalyst Industry

- BASF SE

- Johnson Matthey Plc

- Evonik Industries AG

- Clariant AG

- Umicore N.V.

- Dow Inc.

- Eastman Chemical Company

- W. R. Grace & Co.

- Sinopec Catalyst Company

- Axens

- Heraeus Holding GmbH

- Solvay S.A.

- Mitsubishi Chemical Group

- Strem Chemicals

- Takasago International Corporation

*- List not Exhaustive