Water Treatment Chemicals Market in Oil and Gas: Growth Overview, Analysis, and Forecast

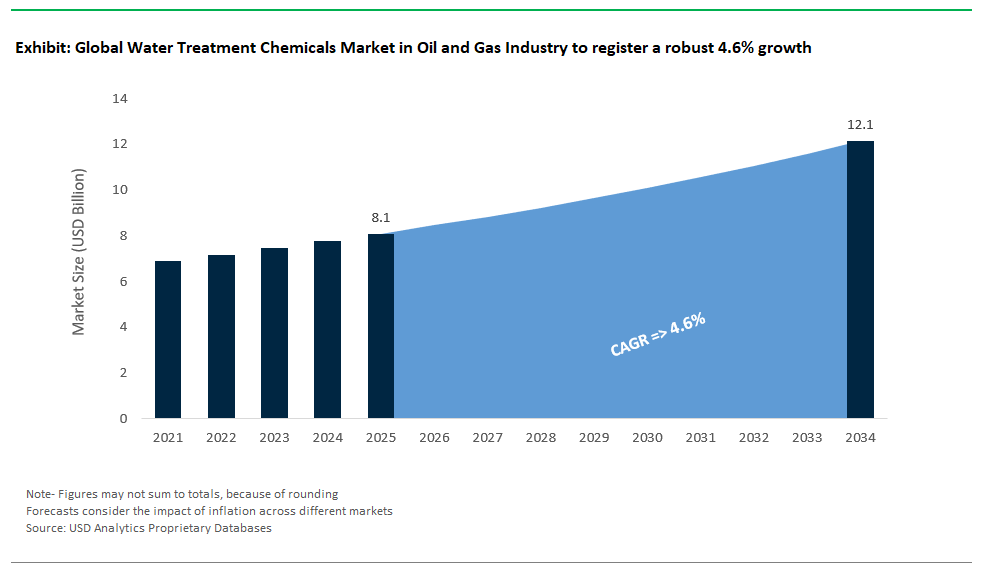

The water treatment chemicals market in the oil and gas industry is valued at $8.1 billion in 2025 and projected to reach $12.1 billion by 2034, with a CAGR of 4.6%. The market plays a pivotal role in sustaining production integrity, asset longevity, and regulatory compliance across upstream, midstream, and downstream operations. As extraction activities extend into harsher environments from high-TDS shale plays to offshore deepwater assets the chemical treatment of water streams has become more complex, precise, and performance-critical. Oilfield operators are increasingly reliant on a diverse portfolio of chemical solutions to manage produced water, hydraulic fracturing fluids, injection water for enhanced oil recovery (EOR), and cooling systems, each with its own operational constraints and treatment demands.

Produced water management remains the largest and most technically demanding application. Demulsifiers, scale inhibitors, hydrogen sulfide (H₂S) scavengers, and oxidants are routinely applied to meet discharge regulations and protect processing infrastructure. Demulsifier formulations particularly ethoxylated polymers are optimized to reduce oil-in-water levels to below 10 ppm, aligning with discharge thresholds under EPA’s NPDES guidelines. In parallel, MEA-triazine remains a mainstay for H₂S control, though its environmental footprint is increasingly scrutinized, prompting exploration of bio-based and metal-free scavenger alternatives.

In hydraulic fracturing, the use of water treatment chemicals is shaped by both technical and environmental considerations. Key applications include microbial control, scale mitigation, and friction reduction in high-shear environments. Biocides such as glutaraldehyde and THPS continue to dominate for their efficacy against sulfate-reducing bacteria, yet there is rising adoption of biodegradable options to comply with regional groundwater protection standards. Friction reducers typically polyacrylamide-based are being replaced or supplemented with cellulose-derived polymers in regions with high ESG oversight, offering comparable shear resistance with enhanced biodegradability.

Injection water treatment, particularly in waterflooding and polymer flooding EOR, requires precise chemical management to prevent scaling and microbial fouling in high-pressure systems. Corrosion inhibitors, oxygen scavengers, and compatibility additives are dosed at optimized levels to ensure sustained injectivity and minimal formation damage. Similarly, in cooling and boiler systems used across oilfield and refinery infrastructure, scale dispersants, filming amines, and alternating biocide programs are employed to control thermal efficiency losses and microbial biofouling while remaining within regulatory toxicity and VOC emission limits.

Across all segments, regulatory frameworks such as EPA 40 CFR 435 for discharge, OSHA limits for chemical exposure, and ISO/ASTM standards for chemical performance are increasingly influencing both formulation development and procurement strategy. Cost efficiency remains a key consideration, but it is intertwined with stricter operational KPIs such as scaling index thresholds, corrosion rate ceilings (<0.1 mm/year), and bacterial count reductions.

Innovation in this market is rapidly shifting toward green chemistry and digital optimization. Bio-derived scavengers, enzymatic breakers, and PFAS-free friction reducers are gaining traction, particularly in regions with strong environmental disclosure mandates. Simultaneously, the integration of real-time monitoring using IoT-based ORP and pH sensors and AI-driven chemical dosing platforms is allowing operators to dynamically adjust treatment regimens, often reducing overall chemical usage by up to 30% without compromising performance.

Next-Generation Water Treatment Chemicals for Shale Plays: Innovation and Produced Water Reuse Drive Market Evolution

Market Trend: Shale Boom Spurs High-Temperature, High-Performance Chemical Innovation

The resurgence of shale development particularly in North America’s Permian, Eagle Ford, and Haynesville basins is fueling a fundamental shift in water treatment chemical requirements, especially for high-pressure/high-temperature (HPHT) wells. Operators drilling deeper into ultra-hot formations (exceeding 250°C and 15,000 psi) are encountering severe scale deposition and corrosion that overwhelm traditional inhibitors like phosphonates or linear polyacrylates. This has triggered an accelerated wave of innovation toward thermally stable, nanocomposite-based inhibitors and hybrid polymers tailored to endure extreme downhole conditions. Field deployments by ChampionX, for instance, validate that sulfonated copolymer–nanoclay blends can sustain high scale inhibition efficiency at higher temperatures. Moreover, the new frontier in material science includes smart-release inhibitors, ceramic-encapsulated anti-scalants, and HPHT-corrosion/scale dual-function agents, which are rapidly gaining traction in the Gulf of Mexico and MENA offshore markets. As the industry pivots toward deeper, hotter, and more chemically complex reservoirs, the scalability and efficacy of next-gen water treatment chemicals will become a cornerstone of E&P operational economics.

Market Opportunity: $1.2B Boom in TDS-Tolerant Friction Reducers for Produced Water Reuse

The growing regulatory and ESG pressure to reuse produced water in hydraulic fracturing has given rise to a lucrative $1.2 billion market for next-generation friction reducers (FRs) that can operate effectively in high-TDS, oil-contaminated water streams. With leading shale operators like Pioneer Natural Resources targeting 90% produced water reuse across Permian assets, conventional FRs are no longer viable. This compatibility not only supports closed-loop water systems but also reduces chemical overuse and mitigates operational failures during high-rate slickwater fracs. Adding further momentum is the upcoming overhaul of the EPA’s Underground Injection Control (UIC) Rule, expected to impose stricter TDS and sulfate discharge limits on flowback reinjection, forcing midstream firms to embrace pretreatment and dual-action FR/scale inhibitor blends. Technologies from startups like ION Clean Energy, which offer mobile dosing skids with AI-controlled viscosity adjustment, are reshaping the market with real-time adaptability. On the ESG front, innovations are helping operators meet Scope 3 water intensity and toxicity reduction targets. As state-level discharge restrictions loom on the horizon, early adopters of recyclable, green, and produced water–tolerant chemistries will gain both operational and reputational edge.

Competitive Landscape: Water Treatment Chemicals in Oil & Gas

In oil and gas operations, from upstream production to dehydration and reinjection, the chemical treatment system focuses on managing scale, corrosion, H₂S, biofilm, and water reuse efficiency under harsh conditions. Competitive differentiation depends on three main capabilities: integrated chemical platforms, digital dosing and monitoring, and environmental and safety credentials.

- Integrated Chemical and Digital Value Chain- Ecolab/Nalco Water leads globally through its 3D TRASAR™ platform. This platform connects real-time corrosion and scale sensors to automated chemical dosing programs like ECOTRAX™ and PHOSSTREAT™ scavengers. They manage millions of oilfield injection points and provide predictive management through analytics-driven control systems. Their upstream leadership is backed by global delivery and technical service networks.

- Deep Expertise in Scale and Biofilm Management- Solenis focuses on fouling and biofilm prevention, especially in deepwater environments, with patented solutions for scale control and Drewfloc™ polymers for produced-water clarity. Their high-performance chemicals are supported by a pipeline of formulation patents and digital dosing analytics. They also promote environmental sustainability by using enzyme-based biofilm removers instead of glutaraldehyde.

- Production Chemical Integration and Field Optimization- SLB (Schlumberger) combines oilfield service scale with chemistry. Its non-triazine scavengers, such as ScavConnect™, reduced chemical use by about 79% and lowered CO₂ emissions in North Sea operations. This improvement enhances uptime and injection rates through IoT-enabled dosing systems. Their offerings include triazine and non-triazine chemistries designed for broader integration into Production Chemicals frameworks.

- Scale and Souring Control at Scale - Baker Hughes, through its merged TETRA portfolio, provides a range of drag reducers, demulsifiers, and corrosion and scale inhibitors. It holds a leading market share in pipeline drag reduction and has extensive experience in heavy oil and sour-gas systems. Their technical strength is based on large-scale field deployment and integrated logistics support, though specific public data on scale share is limited.

- Raw Material and Specialty Polymer Enablers- BASF supports oilfield treatment indirectly by providing high-temperature oxygen scavengers and H₂S removal products, such as SulfaScav®, designed for HPHT environments. Their advantage stems from a reliable global supply and innovations in chemical formulation. Dow contributes through membrane technologies, including RO/UF systems tailored for produced water reinjection and SAGD operations. These membranes enhance chemical treatments in reuse contexts and meet high-reliability standards certified by ASME.

- Specialized Regional and Integrated Players - Kurita excels in Japanese and NE Asian upstream segments by using KURIVER™ nitrification boosters and StellaLine™ cooling inhibitors. Their systems-level recovery rates, which exceed 90% chemical use in refineries, show their deep integration within local energy infrastructure. Emerging regional integrators, such as Dorf Ketal from India and ChemTreat with a focus on the US Gulf Coast, are also emerging. This trend is common in markets where local regulatory complexity and price sensitivity favor regional expertise at the OEM level.

Water Treatment Chemicals Market in Oil and Gas Industry – Segmentation Insights (2025–2034)

By Type of Chemical: Demulsifiers Lead While H₂S Scavengers and Membrane Cleaners Grow Fastest

Demulsifiers hold the largest share in the oil and gas water treatment chemicals market, accounting for approximately 20.4% of total demand in 2025. Their dominance is driven by the essential role they play in breaking oil-water emulsions, a critical step in produced water treatment across upstream operations. Efficient separation of oil and water improves throughput, reduces environmental liabilities, and enhances water reuse potential. Corrosion and scale inhibitors also maintain strong demand in both upstream and midstream systems, safeguarding infrastructure such as wellbores, pipelines, and storage tanks from degradation and mineral deposition. However, H₂S scavengers are the fastest-growing chemical segment, projected to expand at a 6.1% CAGR through 2034. With the expansion of sour gas fields and shale basins especially in the Middle East, North America, and Central Asia the need for rapid hydrogen sulfide mitigation is becoming increasingly urgent to ensure operational safety and regulatory compliance. Membrane cleaning chemicals are also growing rapidly, supported by the increased deployment of reverse osmosis (RO) and nanofiltration (NF) systems for produced water reuse. Biocides, coagulants, oxygen scavengers, and specialty additives like paraffin inhibitors and friction reducers continue to support diverse treatment needs across oilfield water systems.

By End-User: Upstream Segment Dominates While Midstream Maintains Strategic Importance

The upstream sector dominates the oil and gas water treatment chemicals market, comprising approximately 64.3% of the total demand in 2025. Produced water management, which accounts for nearly 80% of chemical consumption in this segment, remains central to operational sustainability and compliance. Key treatments include demulsification, hydrogen sulfide scavenging, scaling and corrosion control, and enhanced oil recovery (EOR) chemical applications. The shift toward zero-liquid discharge (ZLD) and closed-loop systems in shale operations and offshore platforms is further increasing the need for advanced chemical programs and smart dosing technologies. The midstream segment, holding 28% of the market, primarily focuses on pipeline integrity through corrosion inhibition and scale prevention in long-distance transport and gathering systems. Biofouling and deposit management are also crucial, particularly for crude oil pipelines and produced water transport lines. Downstream applications account for a smaller share, but remain important in areas like refinery cooling water systems, boiler feedwater conditioning, and process water recycling. As sustainability targets rise across the oil and gas value chain, all three segments are expected to continue integrating more advanced, targeted, and eco-compliant chemical solutions.

.png)

United States: Innovation in Produced Water Reuse and Smart Chemical Dosing

The U.S. leads the global market for water treatment chemicals in oil and gas operations, driven by regulatory reforms and technological innovation. The EPA’s modernization of Effluent Limitation Guidelines (ELGs) aims to promote produced water reuse for agriculture and wildlife, accelerating demand for advanced chemical treatments. Hydraulic fracturing activities, especially in shale plays like the Permian Basin, require on-the-fly water treatment systems that use optimized blends of scale inhibitors, corrosion inhibitors, and biocides.

Companies are introducing biodegradable chemicals to meet sustainability goals while ensuring compliance with federal and state regulations. Additionally, real-time monitoring systems integrated with AI are being deployed to optimize dosing, reduce chemical waste, and lower costs. With DOE-backed research on safe hydraulic fracturing practices and produced water recycling, the U.S. market continues to prioritize zero-discharge strategies and eco-friendly solutions for wastewater treatment.

Saudi Arabia: Sustainability and Large-Scale Sour Crude Operations Drive Demand

Saudi Arabia’s oil and gas industry generates vast volumes of produced water, creating a substantial demand for high-performance water treatment chemicals. Saudi Aramco plays a pivotal role, implementing advanced formulations to combat hydrogen sulfide (H2S), scaling, and corrosion in its extensive sour crude fields. Vision 2030 initiatives are pushing companies toward environmentally friendly and biodegradable chemical solutions, aligning with the Kingdom’s sustainability goals.

Saudi Arabia’s enhanced oil recovery (EOR) programs depend heavily on water injection systems, which require precise chemical dosing to mitigate scaling and microbial growth. Investments in real-time monitoring technologies are helping optimize chemical application, ensuring operational efficiency and environmental compliance in one of the world’s largest oil-producing regions.

Norway: Stringent Offshore Regulations Fuel Advanced Chemical Adoption

Norway enforces some of the strictest offshore discharge standards, limiting oil content in produced water to 15 mg/L annually. This regulation, combined with the Norwegian Petroleum Directorate’s environmental performance mandates, makes innovative, non-toxic water treatment chemicals essential.

The country is seeing a strong move toward non-triazine H2S scavengers, reducing fouling and chemical waste while maintaining offshore safety. Companies like SLB have introduced advanced formulations optimized for harsh North Sea conditions. Norway’s focus on sustainability and its extensive offshore infrastructure ensure consistent demand for corrosion inhibitors, scale control agents, and environmentally friendly treatment chemicals.

China: Regulatory Pressure and Hybrid Water Treatment Technologies Drive Growth

China’s oil and gas sector is embracing hybrid treatment solutions that combine chemical and physical processes to address the challenges of produced water reuse under Zero Liquid Discharge (ZLD) policies. The government’s “War on Pollution” campaign and strict discharge norms are compelling operators to adopt advanced chemical blends for treating saline, hydrocarbon-rich wastewater.

The demand is especially high in sour gas fields and shale basins, where operators require robust H2S scavengers, scale inhibitors, and corrosion control chemicals. Additionally, digitally integrated treatment systems with IoT sensors and automated dosing platforms are emerging as key trends, improving cost efficiency and reducing chemical wastage.

India: ZLD Mandates and Circular Economy Push Chemical Innovation

India’s market is expanding rapidly as oil companies adopt Zero Liquid Discharge (ZLD) strategies and invest in Effluent Treatment Plants (ETPs). Public sector giants like Oil India Limited (OIL) are implementing reinjection of treated water, boosting demand for coagulants, flocculants, and corrosion inhibitors.

The National Framework for Safe Reuse of Treated Wastewater encourages industrial recycling, driving innovation in low-cost, high-efficiency treatment chemicals. India is also pioneering bioremediation techniques using microbial agents for oily sludge, reducing reliance on conventional chemicals and promoting eco-friendly solutions.

Brazil: Offshore Pre-Salt Projects Drive Advanced Water Treatment Solutions

Brazil’s offshore pre-salt reserves present unique challenges due to high salinity and scale-forming contaminants in produced water. Petrobras is investing heavily in research and real-time monitoring technologies to optimize chemical dosing and reduce environmental impact.

The new national sanitation framework further supports private investment in sustainable water treatment infrastructure. Demand is rising for biodegradable scale inhibitors, corrosion control chemicals, and advanced demulsifiers, ensuring compliance with stringent environmental regulations and operational efficiency in offshore environments.

United Kingdom: Green Chemistry and Policy Reforms Shape Market Trends

The UK’s oil and gas water treatment market is evolving under the Environment Act 2021 and the government’s “Plan for Water”, both aimed at improving environmental performance. Companies are developing bio-based and biodegradable water treatment chemicals to reduce sludge toxicity and meet sustainability goals.

Research initiatives are targeting micropollutant management, encouraging the use of eco-friendly chelants and advanced inhibitors. With new funding for green R&D projects, the UK market is becoming a hub for innovative chemical solutions that align with regulatory compliance and carbon reduction targets.

Australia: Sustainable Water Management for Oil and Gas Operations

Australia’s oil and gas sector faces unique challenges due to water scarcity and strict environmental regulations. The market is embracing smart dosing systems and real-time quality monitoring to ensure efficient chemical usage and minimize water wastage in cooling and injection operations.

There is a growing preference for green chemicals and low-toxicity treatment agents that meet sustainability requirements and protect sensitive marine ecosystems. Investment in digital water management tools combined with eco-friendly chemicals positions Australia as an emerging market for next-generation water treatment solutions in oil and gas operations.

Water Treatment Chemicals in Oil and Gas Report Scope

Water Treatment Chemicals Market in Oil and Gas Industry

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8.1 Billion

|

|

Market Size (2034)

|

$12.1 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Type of Chemical (Demulsifiers, Corrosion Inhibitors, Scale Inhibitors, Biocides and Disinfectants, H2S Scavengers, Coagulants and Flocculants, Oxygen Scavengers, Defoamers and Antifoaming Agents, pH Adjusters/Neutralizers, Sludge Conditioners/Dewatering Aids, Gellants/Viscosifiers, Friction Reducers, Paraffin and Asphaltene Inhibitors/Dispersants, Membrane Cleaning Chemicals), By Segment of the Oil and Gas Industry (Upstream, Midstream, Downstream), By Form (Liquid, Powder/Solid), By Sales Channel (Direct Sales, Distributors/Channel Partners

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ecolab Inc. (U.S.), Solenis LLC (U.S.), SLB (formerly Schlumberger Limited) (U.S.), Baker Hughes Company (U.S.), BASF SE (Germany), Veolia Water Technologies (France), Kurita Water Industries Ltd. (Japan), The Dow Chemical Company (U.S.), Kemira Oyj (Finland), ChemTreat, Inc. (U.S.), Dorf Ketal Chemicals I Pvt. Ltd. (India), Clariant AG (Switzerland),

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Water Treatment Chemicals in Oil and Gas Market Segmentation

By Type of Chemical

- Demulsifiers

- Corrosion Inhibitors

- Scale Inhibitors

- Biocides and Disinfectants

- H2S Scavengers

- Coagulants and Flocculants

- Oxygen Scavengers

- Defoamers and Antifoaming Agents

- pH Adjusters/Neutralizers

- Sludge Conditioners/Dewatering Aids

- Gellants/Viscosifiers

- Friction Reducers

- Paraffin and Asphaltene Inhibitors/Dispersants

- Membrane Cleaning Chemicals

By Segment of the Oil and Gas Industry

- Upstream

- Produced Water Treatment

- Drilling and Completion Fluids

- Workover and Intervention Fluids

- Pipeline and Flow Assurance

- Midstream

- Pipeline integrity

- Water handling in terminals and storage facilities

- Downstream

- Process Water Treatment

- Refinery Wastewater Treatment

- Desalination

By Form

By Sales Channel

- Direct Sales

- Distributors/Channel Partners

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Water Treatment Chemicals Market in Oil and Gas Industry

- Ecolab Inc. (U.S.)

- Solenis LLC (U.S.)

- SLB (formerly Schlumberger Limited) (U.S.)

- Baker Hughes Company (U.S.)

- BASF SE (Germany)

- Veolia Water Technologies (France)

- Kurita Water Industries Ltd. (Japan)

- The Dow Chemical Company (U.S.)

- Kemira Oyj (Finland)

- ChemTreat, Inc. (U.S.)

- Dorf Ketal Chemicals I Pvt. Ltd. (India)

- Clariant AG (Switzerland)

* List Not Exhaustive

Research Coverage

This report by USDAnalytics investigates the Water Treatment Chemicals Market in the Oil and Gas Industry, delivering a comprehensive analysis enriched with data-driven insights and expert perspectives. It highlights technological breakthroughs, sustainability-driven innovations, and strategic developments shaping the industry’s future. The analysis reviews market dynamics across upstream, midstream, and downstream operations, with emphasis on produced water management, demulsifiers, H₂S scavengers, and advanced chemical dosing solutions. From key application trends to regional regulations, this report is an essential resource for industry professionals seeking actionable intelligence, competitive benchmarking, and strategic decision-making to navigate evolving environmental, operational, and cost-efficiency challenges in global oil and gas operations.

Scope Highlights:

- Segmentation:

- By Type of Chemical: Demulsifiers, Corrosion Inhibitors, Scale Inhibitors, Biocides and Disinfectants, H₂S Scavengers, Coagulants and Flocculants, Oxygen Scavengers, Defoamers and Antifoaming Agents, pH Adjusters/Neutralizers, Sludge Conditioners/Dewatering Aids, Gellants/Viscosifiers, Friction Reducers, Paraffin and Asphaltene Inhibitors/Dispersants, Membrane Cleaning Chemicals

- By Segment: Upstream (Produced Water Treatment, Drilling and Completion Fluids, Workover and Intervention Fluids, Pipeline and Flow Assurance), Midstream (Pipeline Integrity, Water Handling in Terminals), Downstream (Process Water Treatment, Refinery Wastewater Treatment, Desalination)

- By Form: Liquid, Powder/Solid

- By Sales Channel: Direct Sales, Distributors/Channel Partners

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Historic Data: 2021–2024; Forecast Data: 2025–2034

- Companies Covered: Ecolab Inc., Solenis LLC, SLB (Schlumberger), Baker Hughes Company, BASF SE, Veolia Water Technologies, Kurita Water Industries Ltd., The Dow Chemical Company, Kemira Oyj, ChemTreat Inc., Dorf Ketal Chemicals, Clariant AG

Methodology

The research methodology combines primary interviews with industry stakeholders and secondary data from authentic sources, including regulatory frameworks, company filings, and technical publications. Advanced analytical tools were applied to validate market sizing, growth rates, and segment-level forecasts. USDAnalytics employed top-down and bottom-up modeling approaches supported by data triangulation to ensure accuracy and reliability. Qualitative insights were derived from expert panels, while quantitative validation involved historical trend mapping and scenario-based forecasting to deliver actionable intelligence for strategic decision-making.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements