Hydrogen Sulfide Scavengers Market to Reach $632.6 Million by 2034 at 3.9% CAGR Driven by Sour Gas Treatment, Asphalt Safety Compliance, and Deepwater Chemical Innovation

The Hydrogen Sulfide (H2S) Scavengers Market is projected to grow from $448.3 Million in 2025 to $632.6 Million by 2034, registering a CAGR of 3.9%. Growth is anchored in expanding sour oil and gas production, tightening occupational safety limits for H2S exposure, and increasing regulatory scrutiny across refining, midstream transport, asphalt blending, and hydrogen storage infrastructure. As operators seek more efficient sulfur management solutions, the market is witnessing a shift toward non-triazine scavengers, multiphase formulations, deepwater-optimized chemistries, and hybrid mechanical-chemical injection systems that reduce fouling, improve partitioning efficiency, and lower total cost of treatment.

In January 2024, Dorf Ketal acquired a majority stake in Elixir Soltek Private Limited, expanding its distribution reach for specialty chemical additives, including hydrogen sulfide scavenger intermediates in emerging markets. In May 2024, Dorf Ketal completed the acquisition of Impact Fluid Solutions, significantly strengthening its downhole and midstream H2S management portfolio for challenging production environments. During 2024, Baker Hughes intensified the rollout of its FULLSWEET™ non-triazine multiphase scavenger, engineered to eliminate solid byproduct formation that typically causes scaling in traditional triazine systems. By early 2025, field validation demonstrated production increases of 350 barrels of oil per day in sour wells through effective downhole treatment without equipment fouling. In 2024, Baker Hughes also reported that its SULFIX™ asphalt scavenging program delivered $400,000 in savings for a major refiner by reducing finished asphalt H2S levels below 10 ppm, enabling compliance with NIOSH safety guidelines. In late 2024, Nalco Water introduced a PPA-resistant SULFIX™ chemistry to prevent H2S regeneration during polyphosphoric acid blending, addressing a persistent safety challenge in asphalt transport and storage. In December 2024, SLB expanded its liquid H2S scavenger portfolio optimized for deepwater fields, focusing on high partitioning efficiency in high-pressure subsea environments where gas-phase removal systems are limited.

The market further evolved in 2025 as energy transition applications expanded. In November 2025, Clariant Oil Services received Petrobras’ Best Supplier Award in the Chemical Products category, underscoring its performance in delivering high-efficiency H2S scavengers to offshore Brazil operations. In 2025, Innospec integrated its TORRENT® static mixer technology with its specialty scavenger portfolio, enhancing contact efficiency in gas streams and offering compact alternatives to conventional contactor towers. In November 2025, Halliburton highlighted expanded hydrogen storage and transportation services that include integrated H2S mitigation strategies for repurposed pipelines and salt caverns, supporting infrastructure durability during hydrogen conversion projects. At the 2025 Gulf Energy Information Excellence Awards, Clariant won Best Catalyst Technology for its chromium-free HySat™ platform, reflecting a broader transition toward environmentally compliant sulfur management chemistries aligned with European REACH standards.

In January 2026, Innospec announced fourth-quarter 2025 earnings, confirming that its Fuel Specialties division, which includes H2S scavengers for gasoline and diesel treatment, remains a key growth engine across Asia-Pacific and the Middle East. Effective May 2026, China’s Dangerous Chemicals Safety Law introduced stricter liabilities for toxic gas handling, compelling regional producers to implement automated, closed-loop scavenger dosing systems to minimize exposure risks and ensure regulatory compliance. The hydrogen sulfide scavengers market is increasingly defined by non-triazine chemistry adoption, sour well optimization, deepwater production chemicals, hydrogen infrastructure protection, and automated sulfur control systems across upstream, midstream, refining, and specialty fuel applications.

Scavengers Market Size Outlook, 2021-2034.png)

Hydrogen Sulfide (H₂S) Scavengers Market Trends and Opportunities

Supply Chain Localization and Basin-Level Integration in Shale and Gas Provinces

The hydrogen sulfide scavengers market is undergoing a structural shift toward localized production, blending, and injection infrastructure, driven by the operational realities of shale and high-throughput gas developments. Operators are increasingly prioritizing just-in-time chemical availability to avoid production shut-ins linked to off-spec H₂S levels. This is accelerating the deployment of basin-level blending hubs directly integrated with upstream and midstream infrastructure.

In North America, the Permian and Delaware Basins have emerged as the focal points of this localization strategy. As part of its upstream optimization program concluding in 2025, ExxonMobil expanded Permian output beyond 600,000 barrels of oil equivalent per day, supported by more than $2 billion in pipeline and terminal upgrades. This scale of development requires scavenger formulations tailored to well-specific sour gas compositions, favoring on-site or near-site blending over centralized chemical distribution. Chemical service providers are responding by embedding formulation units within production corridors to reduce response times and minimize chemical overuse.

Midstream enforcement is reinforcing this trend. Updated pipeline specifications aligned with 2025 GPA Midstream standards have tightened allowable H₂S limits to as low as 4 ppm in transmission systems. This has driven a migration from batch treatment toward continuous, data-driven injection at multiple localized points. Digital monitoring platforms deployed at basin level now enable real-time adjustment of scavenger dosing, reducing chemical consumption by an estimated 15 to 20% while maintaining pipeline compliance.

A similar localization dynamic is unfolding in the Middle East. As the region approaches approximately 70 Bcfd of gas production in 2025, national oil companies in Saudi Arabia and Qatar are investing in integrated chemical-as-a-service facilities in industrial hubs such as Jubail and Ruwais. These facilities support high-sulfur gas monetization strategies by eliminating reliance on imported blends and aligning scavenger supply directly with upstream processing schedules.

Accelerated Shift Away from Triazine Chemistry in Offshore and Sensitive Assets

While triazine-based scavengers remain cost-competitive, their operational limitations are increasingly incompatible with modern refining, offshore, and subsea systems. The formation of dithiazine solids and downstream corrosion risks has triggered a rapid reassessment of triazine use, particularly in assets where remediation costs are disproportionately high.

Refinery acceptance criteria are a key driver. Several global refineries have begun discounting or outright rejecting crude streams containing elevated triazine residuals due to their propensity to form amine hydrochloride salts in overhead systems. This has accelerated qualification of non-triazine alternatives, including metal-complexed lignosulfonates and aldehyde-based chemistries that operate within a neutral pH window of 7.5 to 8.5 and eliminate scale formation risks.

Offshore regulation is compounding this shift. Amendments to MARPOL Annex I effective January 1, 2025 designate the Red Sea and Gulf of Aden as Special Areas, tightening discharge and toxicity thresholds. Floating production systems operating in these regions are transitioning toward glyoxal-based and hemi-formal scavengers that exhibit lower aquatic toxicity and reduced interference with onboard wastewater treatment units.

For deepwater and subsea developments, solids-free performance has become non-negotiable. High-concentration non-triazine scavengers introduced by suppliers such as Baker Hughes are engineered to remain stable across wide temperature and pressure gradients, significantly reducing the risk of subsea tie-back blockage. This positions non-triazine chemistries as the fastest-growing segment within offshore H₂S scavenging applications.

H₂S Scavenging for Supercritical CO₂ and Sour CCS Infrastructure

Carbon Capture and Storage is creating an entirely new demand layer for hydrogen sulfide scavengers. Captured CO₂ streams frequently contain trace H₂S and moisture, which under supercritical conditions form one of the most aggressive corrosion environments encountered in energy infrastructure. Managing these impurities is now recognized as a prerequisite for CCS bankability.

Late-2025 corrosion studies demonstrate that even 50 ppm of H₂S can increase corrosion rates in X65 pipeline steel by more than 40% under dry supercritical CO₂ conditions. When free water is present, corrosion rates can exceed 15 mm per year, making untreated systems economically unviable. This is driving demand for scavengers that remain chemically stable under supercritical pressures and temperatures while remaining compatible with CO₂ monitoring and verification sensors.

The Global CCS Institute’s 2025 Technology Compendium identifies capture-adjacent purification technologies, including H₂S removal, as critical to achieving full commercial readiness. This has opened opportunities for advanced scavengers designed for sour CO₂ service in Gulf Coast and North Sea CCS hubs, where impurity control directly underpins storage integrity and regulatory approval.

An additional growth vector lies in multi-impurity management. CCS developers are increasingly seeking scavenger systems capable of simultaneously addressing H₂S, SOx, and NOx contaminants in captured flue gas. These multifunctional formulations are emerging as enabling technologies for large-scale, hub-based sequestration projects in the United States and the United Kingdom.

Integrated Life-Extension Chemical Programs for Mature Fields

Mature oil and gas assets represent a structurally attractive opportunity for H₂S scavenger suppliers as rising water cuts and sulfate-reducing bacteria drive progressive reservoir souring. Operators are shifting away from single-function chemicals toward integrated life-extension blends that reduce operational complexity and offshore footprint.

In 2025, corrosion inhibitors for oil and gas applications represent a market exceeding $9.5 billion, with a growing share allocated to water-based, multifunctional formulations. H₂S scavengers are increasingly bundled with corrosion inhibitors, scale inhibitors, biocides, and asphaltene control agents into single-point injection programs. This approach reduces platform storage requirements and lowers total chemical handling risk.

Automation is amplifying the value proposition. Closed-loop smart injection systems now link real-time H₂S sensors to automated dosing skids, preventing overdosing and minimizing unplanned downtime in high-water-cut wells. Field data indicates that such systems can extend the economic life of mature assets by 5 to 8 years by mitigating sulfide stress cracking and corrosion-related failures.

This transition favors integrated service providers such as Halliburton and SLB, which are increasingly positioning proprietary chemical management programs as high-margin service offerings. For the broader market, this represents a shift from commodity scavenger sales toward recurring, value-based contracts centered on asset integrity and long-term production assurance.

Hydrogen Sulfide Scavengers Market Share and Segmentation Insights

Non-Regenerative Hydrogen Sulfide Scavengers Lead the Market with Operational Simplicity in Oilfield Treatment

Non-regenerative scavengers accounted for 72.80% of the Hydrogen Sulfide Scavengers Market share in 2025, establishing them as the dominant technology for H₂S removal in oil and gas production systems. These scavengers are widely adopted because they offer simple injection-based treatment, rapid reaction kinetics, and lower operational complexity compared with regenerative systems that require additional infrastructure for chemical recovery and recycling. Non-regenerative chemistries react directly with hydrogen sulfide to form stable byproducts that can be removed during downstream separation processes. The segment is strongly led by triazine-based hydrogen sulfide scavengers, which remain the standard solution for upstream oilfield sour gas treatment, crude stabilization, and gas sweetening in production facilities. In 2025, manufacturers continue refining triazine formulations with improved thermal stability, higher H₂S loading capacity, and reduced solid byproduct formation, addressing operational challenges such as scaling and fouling in production equipment. These improvements allow non-regenerative scavengers to perform effectively even in higher H₂S concentration environments, reinforcing their position as the most practical solution for continuous oilfield sour gas management.

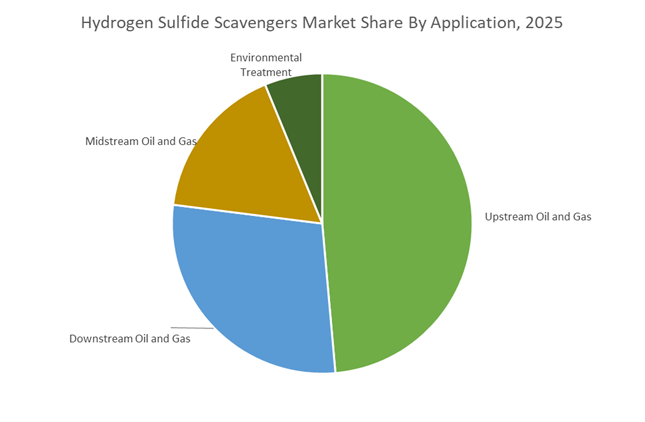

Upstream Oil and Gas Operations Drive the Largest Demand for Hydrogen Sulfide Scavengers

Upstream Oil and Gas represented 48.60% of the Hydrogen Sulfide Scavengers Market share in 2025, making production operations the largest application segment. Hydrogen sulfide is a common contaminant in crude oil and natural gas reservoirs, and its removal is essential for worker safety, corrosion prevention, and compliance with pipeline gas quality specifications. Upstream treatment typically occurs at wellheads, flowlines, and separation facilities, where liquid scavengers are injected continuously or intermittently to neutralize H₂S before hydrocarbons enter processing or transportation systems. Demand is further reinforced by the global increase in sour gas field development, as easily produced sweet gas reservoirs decline and operators expand into resources with higher sulfur content. In 2025, production from sour reservoirs in regions such as the Middle East, North America, and Central Asia has increased the intensity of H₂S treatment requirements, raising scavenger consumption per barrel produced. These conditions are also driving adoption of multi-stage H₂S removal systems that combine chemical scavenging with sulfur recovery units, improving operational efficiency while meeting strict environmental and safety standards in hydrocarbon production.

Competitive Landscape in the Hydrogen Sulfide Scavengers Market

The Hydrogen Sulfide (H2S) Scavengers Market is characterized by strong competition among leading oilfield chemical providers focusing on advanced scavenger chemistries, digital injection technologies, subsea flow assurance solutions, and integrated sour gas treatment systems. Market leaders are differentiating through non-triazine chemistries, multiphase treatment platforms, nanotechnology-based delivery systems, and automated IoT-enabled dosing technologies to improve H2S removal efficiency and reduce chemical consumption.

Baker Hughes Leads Multiphase H2S Removal Innovation with the FULLSWEET™ Non-Triazine Platform

Baker Hughes holds a strong position in the hydrogen sulfide scavengers market by developing multiphase H2S treatment technologies that overcome the operational limitations of conventional triazine scavengers. Its FULLSWEET™ platform, a first-of-its-kind non-triazine H2S scavenger system, enables removal of hydrogen sulfide directly from multiphase production fluids at early production stages, including downhole and topside environments, without generating solid reaction byproducts. Field results from 2024–2025 demonstrate H2S removal efficiencies of up to 98% while reducing treatment volumes by approximately 36% compared with traditional triazine chemistries. The company also expanded its Dammam facility in Saudi Arabia in May 2024, adding manufacturing capacity for sour gas technologies supporting Middle Eastern hydrogen and gas projects. Additionally, Baker Hughes partnered with SOCAR in late 2024 to deploy an integrated gas recovery and H2S removal system at the Heydar Aliyev Oil Refinery, targeting reductions in flaring and sulfur emissions.

SLB Advances Real-Time Digital H2S Mitigation Through IoT-Enabled Chemical Injection Systems

SLB (Schlumberger) is strengthening its competitive position in the H2S scavenger chemicals market through digitally integrated chemical treatment services and automated sour gas mitigation platforms. The company introduced an advanced H2S Scavenger Service in late 2023, scaled through 2024, designed specifically for high-pressure, high-temperature (HPHT) offshore environments with improved selectivity and regeneration capabilities. In 2025, SLB secured an integrated development contract for the Mutriba Field in Kuwait along with several offshore drilling contracts in Indonesia, where specialized sour gas treatment and H2S scavenging systems are critical for maintaining asset integrity. The company is also deploying IoT-enabled chemical injection systems that dynamically adjust scavenger dosages based on real-time hydrogen sulfide concentration monitoring, minimizing chemical waste and preventing overdosing. Furthermore, SLB strengthened its reservoir monitoring capabilities through the 2024 acquisition of RESMAN Energy Technology, enabling precision downhole H2S management.

ChampionX Delivers Multi-Function Oilfield Chemicals for H2S Control and Flow Assurance

ChampionX, an Ecolab company, is recognized for developing multi-functional oilfield production chemicals that simultaneously address hydrogen sulfide scavenging, hydrate inhibition, and scale control. One of its key innovations is HYDT16919A, a combined Kinetic Hydrate Inhibitor (KHI) and H2S scavenger, enabling operators to maintain deepwater pipeline flow assurance while preventing H2S-induced corrosion. Operational data from 2025 European offshore projects showed that replacing incumbent chemistries with ChampionX HSCV30160A, a combined scavenger and scale inhibitor, resulted in 15% lower chemical consumption while maintaining export gas H2S levels below 2.6 ppm. The company is also expanding its Extended Release (XR) nanotechnology platform, designed for squeeze applications in mature reservoirs, which extends treatment longevity and reduces intervention frequency. ChampionX’s chemical portfolio is optimized for subsea compatibility, ensuring seamless integration with corrosion inhibitors and demulsifiers to prevent fouling.

Clariant Oil Services Strengthens Sour Gas Treatment with High-Performance Specialty Chemicals

Clariant Oil Services maintains a strong position in the global hydrogen sulfide scavengers market, particularly across Latin America and North America, supported by its portfolio of high-performance specialty chemicals for sour gas management. In November 2025, Clariant was recognized by Petrobras as “Best Supplier” in the Chemical Products category, achieving a 5.7 out of 6.0 Supplier Performance Index score, largely due to its reliable delivery of H2S treatment solutions in Brazil’s offshore energy sector. The company has also demonstrated strong capabilities in HPHT reservoir conditions, successfully deploying H2S and CO2 control technologies in Canada and Brazil in February 2025, where conventional scavengers typically degrade.

Clariant is simultaneously advancing biodegradable and low-carbon “green” scavenger formulations aligned with its climate neutrality target for 2050. Its WellBoost™ and PHASETREAT product lines are increasingly integrated with H2S scavenging systems to support deliquification and gas sweetening in mature shale wells, increasing production by up to 23% in field trials.

Innospec Expands Midstream and Refinery H2S Treatment with Advanced Static Mixing Technologies

Innospec Inc. has built a strong reputation in the midstream and refinery hydrogen sulfide scavengers market, combining specialized chemical formulations with proprietary injection hardware to enhance treatment efficiency. A key differentiator is its TORRENT® Static Mixer, which improves the dispersion of H2S scavengers in gas streams and provides a more compact and cost-efficient alternative to traditional triazine atomization towers. The company’s SulfurPurge™ product range includes both water-soluble and oil-soluble scavenger technologies, with 2025 upgrades to the SulfurPurge HC line utilizing CHNO chemistry to ensure halogen-free and sulfur-free formulations that protect fuel quality.

Innospec’s solutions are widely used in residual fuel oil refining, where rapid, non-reversible scavenging reactions help refineries comply with IMO 2020 and subsequent 2025 marine sulfur regulations. The company has also expanded technical service operations in the Permian Basin, providing tailored H2S treatment solutions for mature shale fields with rising sour gas levels.

United States: Shale Optimization, Digital Dosing, and Carbon Capture Readiness

The United States remains a technology and deployment leader in hydrogen sulfide scavengers, driven by sour gas management in shale plays, tightening emissions regulation, and integration with carbon capture infrastructure. In 2025, adoption of ultra-high-capacity triazine-based scavengers accelerated across the Permian Basin as operators addressed rising H2S concentrations in maturing shale wells. These chemistries are being selected for rapid knockdown performance and compatibility with high-throughput gas processing systems, supporting production continuity while minimizing downtime associated with sour gas upsets.

Regulatory enforcement is reshaping operating practices. The U.S. Environmental Protection Agency finalized Subpart OOOOb and OOOOc standards with full enforcement by 2026, prompting operators to integrate real-time H2S monitoring with automated chemical injection to prevent unintended venting during maintenance. Refining investments reinforce this trend. In 2025, Gulf Coast refiners announced capital expenditures exceeding USD 1.2 billion to upgrade desulfurization units for heavier, sour crude imports from Canada and Latin America. Offshore, deployment of the DM-MAX line of non-triazine, non-scaling liquid scavengers increased in the Gulf of Mexico to protect subsea equipment. Technology providers are also shifting toward intelligence-led dosing. In late 2025, Baker Hughes and SLB introduced AI-enabled smart scavenger platforms using edge computing to adjust dosage in real time, reducing chemical waste by an estimated 15–20%. Under the Inflation Reduction Act, new carbon capture projects linked to natural gas processing are mandating pre-treatment H2S removal to protect amine solvents, further embedding scavengers into decarbonization workflows.

Saudi Arabia: Blue Hydrogen Scale-Up and Industrial Desulfurization Hubs

Saudi Arabia’s hydrogen sulfide scavengers market is expanding in tandem with unconventional gas development and blue hydrogen ambitions. As of May 2025, Saudi Aramco secured an USD 11 billion lease to accelerate development of the Jafurah unconventional gas field. The project relies on industrial-scale scavenging systems to treat sour gas prior to processing and conversion to blue hydrogen, establishing sustained demand for high-performance chemistries.

Downstream integration is intensifying. In March 2025, Aramco acquired a 50% stake in Blue Hydrogen Industrial Gases at Jubail, where feedstock purity requirements necessitate rigorous H2S removal ahead of carbon capture and storage units. A USD 30 billion modernization initiative at Yanbu Industrial City, scheduled across 2025–2026, includes dedicated desulfurization hubs aligned with the Saudi Green Initiative. Localization is also advancing. Through Aramco Ventures, investments are targeting domestic manufacturing of metal-based and organic scavengers to reduce dependence on European imports. Certification milestones are reinforcing quality thresholds. In July 2025, Saudi Arabia achieved the world’s first independent certification for blue ammonia, a process requiring zero-trace H2S levels and driving stringent scavenging specifications across gas treatment trains.

China: Municipal Odor Control, Gas Network Expansion, and Digital Refining

China’s hydrogen sulfide scavengers industry is broadening beyond oil and gas into municipal infrastructure and digitalized refining. In September 2025, the Ministry of Industry and Information Technology issued a petrochemical growth directive targeting 5%annual value-added growth, with explicit emphasis on high-end fine chemicals. This mandate is accelerating domestic production of G5-grade scavengers designed for precise dosing and low by-product formation.

Municipal wastewater has emerged as a dominant application. In 2025, cities across the Yangtze River Delta invested more than USD 160 million in odor control systems, positioning H2S mitigation as a public health and compliance priority. Energy infrastructure is another growth vector. To support the coal-to-gas transition by 2030, China is constructing more than 3,000 kilometers of natural gas pipelines annually, each requiring gate-station scavenging to meet pipeline quality standards. Digital optimization is improving efficiency. Sinopec deployed digital twins under its AI plus Petrochemicals initiative at the Zhenhai Refining and Chemical complex to optimize scavenger injection, targeting a 30% reduction in sulfur-related corrosion events by 2026.

Brazil: Deepwater Assurance and Refining Modernization

Brazil’s hydrogen sulfide scavengers demand is anchored in offshore production, refining upgrades, and bio-refining integration. Under its PN 2025–2029 Business Plan, Petrobras committed R$33 billion to refining and petrochemical investments in Rio de Janeiro, including major maintenance shutdowns in 2026 at the Reduc refinery to upgrade hydrotreatment and H2S scavenging units. These investments are designed to improve processing of sour streams while meeting S-10 diesel specifications.

Gas processing integration is expanding at scale. The Boaventura Energy Complex at Itaboraí is receiving an estimated R$26 billion to integrate with Reduc, including a large natural gas processing unit that requires high-volume scavenging. Offshore, Petrobras signed an R$8.4 billion contract in early 2025 for subsea interconnections at the Búzios 11 field, where non-precipitating scavengers are critical for flow assurance under high pressure. Bio-refining is creating incremental demand. Petrobras’ USD 1.5 billion BioRefining Program is testing conventional H2S scavengers to treat biogas and bio-oils prior to co-processing, linking sulfur management with renewable feedstocks.

Canada: Oil Sands Compliance and Hydrogen Pre-Treatment

Canada’s hydrogen sulfide scavengers market is being reshaped by oil sands lifecycle transitions, hydrogen strategy execution, and stricter well construction standards. By 2025, 38 oil sands projects moved from pre-payout to post-payout status, freeing capital for environmental compliance and adoption of high-efficiency scavenging in steam-assisted gravity drainage operations. These systems are increasingly selected for longevity and compatibility with continuous steam injection.

Hydrogen development is reinforcing pre-treatment demand. Natural Resources Canada reported that five million tons per annum of clean hydrogen projects are under development, all requiring specialized H2S removal ahead of steam methane reforming with carbon capture. Regulatory tightening is elevating standards. The Alberta Energy Regulator implemented a zero mol per kmol H2S requirement for specific new wells effective December 2025, mandating total scavenging for licensing. Asset modernization is following suit. During 2025–2026 shutdowns at Mildred Lake and Kearl, Suncor Energy and Imperial Oil integrated regenerative iron-redox systems to replace single-use triazines in high-volume tailings gas treatment.

Summary Table: Country-Level Strategic Signals in the Hydrogen Sulfide Scavengers Industry

Hydrogen Sulfide (H₂S) Scavengers Market County Level Snapshot

|

Country

|

Primary Driver

|

Key Application Focus

|

Structural Implication

|

|

United States

|

Shale maturity, EPA rules, IRA

|

Shale gas, refining, CCS

|

Digital dosing and efficiency gains

|

|

Saudi Arabia

|

Blue hydrogen, Jafurah gas

|

Unconventional gas, CCS

|

Industrial-scale desulfurization

|

|

China

|

Municipal odor control, pipelines

|

Wastewater, gas networks

|

High-end domestic chemistries

|

|

Brazil

|

Deepwater fields, refinery upgrades

|

Offshore gas, S-10 diesel

|

Flow assurance at scale

|

|

Canada

|

Oil sands compliance, hydrogen

|

SAGD, SMR with CCS

|

Regenerative systems adoption

|

Hydrogen Sulfide (H₂S) Scavengers Market Report Scope

Hydrogen Sulfide (H₂S) Scavengers Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$448.3 Million

|

|

Market Size (2034)

|

$632.6 Million

|

|

Market Growth Rate

|

3.9%

|

|

Segments

|

By Type (Regenerative Scavengers, Non-Regenerative Scavengers), By Physical State (Liquid Scavengers, Solid Scavengers), By Chemistry (Amine-Based, Non-Amine / Green Chemistry, Metal-Based), By Application (Upstream Oil and Gas, Midstream Oil and Gas, Downstream Oil and Gas, Environmental Treatment)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

SLB, Baker Hughes Company, Halliburton Company, BASF SE, Arkema S.A., Ecolab Inc., Clariant AG, Veolia Environmental Services, Evonik Industries AG, Solenis LLC, Dorf Ketal Chemicals, Cestoil Chemical Inc., Hexion Inc., Innospec Inc., Suez Water Technologies

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Hydrogen Sulfide Scavengers Market Segmentation

By Type

- Regenerative Scavengers

- Amine-Based

- Iron-Redox

- Solid Bed Adsorbents

- Non-Regenerative Scavengers

- Triazines

- Metal Carboxylates

- Glyoxal-Based

- Formaldehyde-Free Blends

By Physical State

- Liquid Scavengers

- Solid Scavengers

By Chemistry

- Amine-Based

- Non-Amine / Green Chemistry

- Metal-Based

By Application

- Upstream Oil and Gas

- Midstream Oil and Gas

- Downstream Oil and Gas

- Environmental Treatment

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Hydrogen Sulfide Scavengers Industry

- SLB

- Baker Hughes Company

- Halliburton Company

- BASF SE

- Arkema S.A.

- Ecolab Inc.

- Clariant AG

- Veolia Environmental Services

- Evonik Industries AG

- Solenis LLC

- Dorf Ketal Chemicals

- Cestoil Chemical Inc.

- Hexion Inc.

- Innospec Inc.

- Suez Water Technologies

*- List not Exhaustive