Food & Beverage Water Treatment Chemicals Market: Growth Forecast and Value Analysis

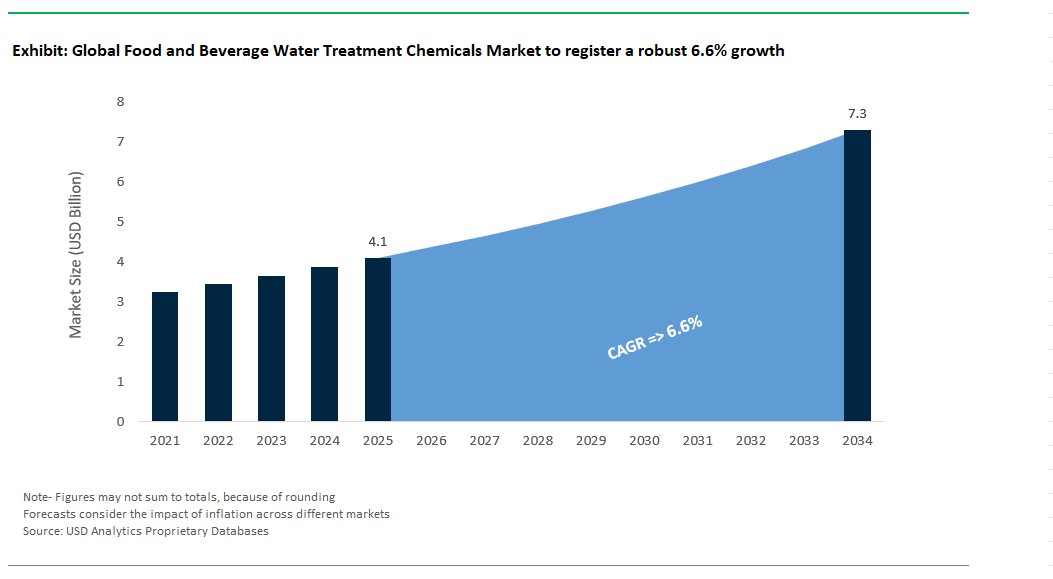

The Food & Beverage (F&B) water treatment chemicals market is valued at $4.1 billion in 2025 and projected to reach $7.3 billion by 2034, registering a CAGR of 6.6%. This market is shaped by a complex interplay of microbial safety, regulatory compliance, and process hygiene, where chemical formulations must demonstrate both technical efficacy and food-contact safety. In disinfection applications, peracetic acid (PAA) continues to dominate due to its potent oxidizing properties and clean decomposition profile breaking down into oxygen and water without halogenated byproducts. Used at concentrations between 1.5–5 mg/L, PAA is effective for biofilm control in clean-in-place (CIP) and packaging environments and is sanctioned under FDA 21 CFR 173.315 for direct food-contact water applications. However, residual oxidant levels must be stringently managed; hydrogen peroxide residues, for example, are regulated under Codex Alimentarius to remain below 0.5 ppm in final rinse waters, demanding precise dosing and validation protocols.

Membrane cleaning a recurring challenge in dairy, beverage, and ready-to-eat food operations relies heavily on alkaline formulations (pH 11–12) augmented with enzymatic components. These blends not only remove proteinaceous and fatty deposits but also restore over 90% of membrane flux in spiral-wound and hollow fiber systems, meeting both operational performance targets and FDA GRAS (Generally Recognized as Safe) status requirements. The market is further governed by dual compliance frameworks, including NSF/ANSI 60 for potable water chemicals and 3-A Sanitary Standards for food equipment and contact surfaces, especially within the meat, dairy, and aseptic bottling segments. As the F&B industry adopts more closed-loop water systems and tighter resource controls, the need for specialty chemical solutions that are both food-grade and process-robust is growing.

Food Safety, Sustainability, and Water Reuse Drive Transformation in Food & Beverage Water Treatment Chemicals Market

Market Trend: FDA-Compliant, Non-Toxic, and Sustainable Chemicals Drive Transformation in Food & Beverage Water Treatment

The food and beverage water treatment chemicals market is undergoing a paradigm shift as producers face dual pressure to meet stringent food safety regulations while aligning with corporate sustainability targets. Traditional chemical regimes often reliant on chlorine-based disinfectants, caustic CIP cleaners, and phosphonate-laden scale inhibitors are being replaced by food-grade, non-toxic, and environmentally responsible formulations designed for direct or indirect contact with consumables. At the forefront is EnviroTru®, a lactic acid-based sanitizer that achieves a significant reduction in residual chemical load across bottling lines enhancing worker safety and downstream water recovery potential. In Latin America, PepsiCo has piloted the use of Electrolyzed Oxidizing Water (EOW), which replaces conventional chemicals in equipment sanitation, halving chemical inventory and reducing cleaning cycle time. Meanwhile, smart dosing and monitoring platforms such as Veolia’s AI are redefining chemical efficiency in clean-in-place (CIP) systems. In dairy operations, AI-optimized peracetic acid (PAA) dosing has cut water consumption, enabling tighter water-energy-chemical integration. The move toward bio-based solutions extends to membrane maintenance as well: Dupont’s enzyme-based cleaners are replacing acid-alkali formulations in RO systems. This convergence of food-grade compliance, sustainability, and digital dosing control is redefining how water is treated in beverage, dairy, and processed food facilities transforming chemical programs from cost centers into strategic enablers of water resilience, regulatory readiness, and ESG performance.

Market Opportunity: Circular Water Systems Unlock Strategic Value Across Beverage, Dairy, and Plant-Based Processing Facilities

A major growth opportunity in the food and beverage water treatment chemicals market lies in enabling closed-loop and circular water systems that support both sustainability goals and cost savings. With beverage majors like Coca-Cola targeting full water neutrality by 2030, treatment chemical providers are repositioning from simple disinfection and scale control to system-wide water reuse enablers. In the brewery segment, Heineken’s “Brewery of the Future” in the Netherlands showcases the power of ozone disinfection combined with biological filtration to achieve 99% water recovery from process effluents saving over 1 million cubic meters annually while avoiding odor and taste contamination risks. Likewise, Diageo’s Guinness facility in Dublin uses electrochemical oxidation to remove organic compounds from rinse water, allowing for closed-loop reuse without compromising microbial safety reducing both water intake and wastewater discharge. In the dairy sector, Danone’s “Whey-to-Water” project combines ultrafiltration and UV/H₂O₂ oxidation to recover water while extracting valuable proteins and lactose, thus turning wastewater into both an asset and a revenue stream. The plant-based food sector often characterized by high organics and nutrient runoff is emerging as a key adopter of eco-compatible treatment. Beyond Meat’s CleanWater Initiative, using enzymatic coagulants, cuts phosphate loads, unlocking compliance with California’s strict discharge norms while enabling water recovery for cooling and cleaning. Notably, a recent WRF study confirmed that advanced reuse systems in F&B operations deliver ROI in under two years, with additional returns in brand equity and regulatory favor. As more facilities integrate wastewater valorization and reuse into core operations, the role of high-efficiency, food-grade treatment chemicals becomes critical not just for process hygiene, but as catalysts for operational circularity and long-term water security.

Competitive Landscape: Food & Beverage Water Treatment Chemicals Market

The global food and beverage (F&B) water treatment chemicals market consists of a diverse group of solution providers, specialized chemical manufacturers, and component suppliers. Each of these players addresses specific needs within a tightly regulated industry. The competitive landscape focuses on delivering chemical effectiveness, compliance with food safety standards, process integration, and sustainability.

At the top tier, a few leading companies combine extensive application knowledge with real-time monitoring systems and regulatory support throughout the production water lifecycle. This spans from treating ingredient water to managing wastewater discharge. These firms bring industry expertise in areas like dairy, brewing, beverages, meat processing, and packaged foods. They set themselves apart through intensive service, digital optimization tools, and global regulatory certifications such as NSF, FDA, Halal, and Kosher, which are essential for F&B manufacturers that follow strict hygiene and environmental rules.

A competitive advantage also comes from managing both product safety and resource efficiency. Companies that offer a strong selection of phosphate-free, biodegradable, or food-contact-approved chemicals are gaining traction as the industry moves toward zero liquid discharge (ZLD), water reuse, and chemical reduction. Players with effective flocculants, specialty biocides, chelants, and oxygen-based oxidants are in high demand for treating high-load organic wastewater, controlling microbes in clean-in-place (CIP) systems, and sanitizing packaging lines.

Integrated water service providers and membrane or separation technology firms also play an important role. They combine chemical treatment with filtration, disinfection, and process automation solutions, especially for large F&B facilities. These companies serve clients who want to optimize their plants, reduce chemical use, or implement decentralized operations. There is a growing collaboration between chemical suppliers and equipment vendors as digital water analytics platforms like AQUADVANCED or 3D TRASAR become key in maintaining treatment performance while cutting down on energy and chemical consumption.

Raw material producers impact market structure by supplying essential intermediates like polyacrylamides, ion exchange resins, biocide actives, or peroxide derivatives. Their partnerships with formulators and regional service providers guarantee that end-users receive compliant, high-performance solutions that meet global safety and environmental standards. Consequently, the F&B water treatment sector showcases a layered competitive landscape where differentiation relies on not only chemistry but also operational transparency, commitment to food safety, and ongoing innovation in response to changing regulations and sustainability goals.

Food and Beverage Water Treatment Chemicals Market – Segmentation Insights (2025–2034)

By Application: Process Water Treatment Leads While Wastewater Treatment Grows Fastest

Process water treatment accounts for the largest share of the food and beverage water treatment chemicals market, comprising approximately 49.6% of the total market in 2025. This dominance is driven by the industry’s strict hygiene and product safety standards, which necessitate high-purity process water for ingredient mixing, rinsing, and cleaning operations. Ensuring microbial control, taste neutrality, and chemical compliance is critical in food-grade water, especially for dairy, beverage, and packaged food production. The use of biocides, disinfectants, and antiscalants is standard practice in maintaining production quality and regulatory compliance. In contrast, wastewater treatment is the fastest-growing application, projected to grow at a CAGR of 7.9% during 2025–2034. Increasing regulatory enforcement on effluent discharge standards, coupled with a shift toward zero-liquid discharge and water reuse strategies, is pushing food and beverage manufacturers to invest in advanced wastewater treatment solutions. Meanwhile, utilities water treatment covering boiler and cooling systems continues to see steady demand, particularly for chemicals that control scaling, corrosion, and microbial fouling. These support operations remain essential to maintaining uptime and operational efficiency in production facilities.

By Source of Water: Groundwater Dominates; Recycled Water Segment Expands Rapidly

By source of water, groundwater holds the largest market share in 2025 at approximately 38.7%, reflecting its widespread use in the food and beverage sector due to its generally lower contaminant load, mineral content stability, and lower pretreatment requirements. Many facilities, especially those in rural or semi-urban areas, rely on borewells and local aquifers for their process and utilities water supply. However, the fastest-growing segment is recycled or reused water, forecast to grow at a strong 8.4% CAGR through 2034. This growth is propelled by sustainability-driven initiatives and corporate water stewardship goals aimed at reducing freshwater withdrawals and enhancing circular water management. Major beverage manufacturers are increasingly implementing internal water recycling systems and greywater treatment units to meet environmental targets and reduce operating costs. Surface water, while less preferred due to variability and turbidity issues, still plays a key role in regions where rivers or reservoirs are primary sources. Municipal water supplies continue to support smaller facilities or those in urban environments but show slower growth due to high treatment costs and rising tariffs.

.png)

United States: Regulatory Leadership and Sustainable Innovation Shape Market Growth

The United States leads the global food & beverage water treatment chemicals market, propelled by some of the world’s strictest food safety regulations and a mature industrial base. The FDA, EPA, and local agencies enforce rigorous standards for water quality, driving demand for specialized chemicals like food-grade biocides, antiscalants, and corrosion inhibitors. Top food and beverage companies such as The Coca-Cola Company, PepsiCo, and Nestlé USA are investing in circular water systems and setting ambitious water stewardship goals for 2030. Their initiatives, which include returning trillions of liters of water to nature, require advanced water treatment chemistries and high-efficiency automation for both incoming and wastewater streams.

There’s a clear trend toward eco-friendly, biodegradable solutions in response to rising consumer expectations and ESG commitments. Automation and smart dosing are transforming operations, enabling real-time quality assurance while reducing chemical consumption and costs. The intersection of regulatory compliance and corporate sustainability initiatives positions the U.S. as a global benchmark for innovation and best practice in food-grade water treatment.

Germany: Circular Economy and Digital Platforms Advance Water Treatment

Germany’s food & beverage water treatment chemicals market is defined by cutting-edge technological development and strong compliance with both EU and national standards. The German Water Resources Act (WHG) and EU directives impose strict limits on effluent quality and water use, fostering a market for innovative chemicals that support water reuse, resource recovery, and advanced recycling. German manufacturers and utilities are global leaders in deploying digital water platforms that use AI and data analytics to optimize coagulant, flocculant, and disinfectant dosing, minimizing both waste and environmental impact.

The brewing and beverage sectors, which are particularly water-intensive, have embraced advanced membrane bioreactors, nutrient removal, and closed-loop systems. These trends, combined with a national focus on a circular economy, drive demand for intelligent, high-performance chemical solutions that support Germany’s reputation for both product safety and environmental stewardship.

China: Pollution Control Policies and Industry Modernization Drive Demand

China’s rapid expansion in food and beverage manufacturing is matched by aggressive policy measures under the “War on Pollution” and new food safety laws. These efforts require modern water treatment solutions, including advanced biocides, flocculants, and specialty chemicals, for both potable water and effluent treatment. The dairy, brewery, and soft drink industries are leading adopters of real-time monitoring, smart dosing systems, and digital process optimization to ensure product safety and compliance.

A major trend is the push for Zero Liquid Discharge (ZLD), where companies such as Evonik are showcasing ZLD plants to reduce environmental impact and support water reuse. As China invests in new facilities and upgrades existing plants, the market for high-efficiency, food-grade water treatment chemicals continues to grow, with sustainability and automation as key purchase drivers.

India: Government Initiatives and Industrial Growth Catalyze the Market

India’s food & beverage water treatment chemicals market is expanding rapidly, thanks to landmark public programs like the Jal Jeevan Mission and explosive growth in the food processing sector. Government mandates around potable water access, as well as stringent CPCB effluent standards for BOD, COD, and TSS, have created robust demand for water purification, disinfection, and nutrient removal chemicals.

Companies are embracing sustainable water management, notably in regions like Gujarat, where industry is pivoting to using treated municipal sewage water for food and beverage processing. Major players are implementing cutting-edge effluent treatment technologies, such as advanced filtration and biological nutrient removal, to comply with regulations and improve their water use ratios. These efforts, paired with a booming consumer market, position India as a global growth hotspot for food-grade water treatment solutions.

Japan: Technological Sophistication Meets Sustainable Water Management

Japan’s market stands out for its emphasis on technological innovation and resource efficiency. Stringent hygiene standards and consumer expectations for quality drive the adoption of high-purity, low-maintenance water treatment chemicals. Japanese companies are at the forefront of developing advanced functional additives, efficient nutrient removal systems, and membrane-based solutions that ensure both incoming water purity and effective effluent treatment.

Water reuse and recycling, championed by government policies and corporate sustainability programs, are key growth areas. There’s also a strong emphasis on biodegradable and environmentally friendly chemicals to protect sensitive aquatic systems and urban waterways. Japan’s food & beverage sector thus serves as a model for integrating innovation, regulatory compliance, and sustainability.

Brazil: Legal Reforms and Agro-Industry Growth Create Opportunities

Brazil’s evolving legal framework for sanitation, aiming for universal access to water and sewage treatment by 2033, is a primary growth engine for the market. Food and beverage companies are investing in new water and wastewater treatment infrastructure, often leveraging the country’s strong agricultural base for bio-based chelants and green chemicals.

Cost-effective, high-performance chemical formulations and biological processes are gaining ground, helping producers meet both food safety and environmental regulations. The market is further shaped by public-private partnerships and a focus on sustainable resource management, making Brazil an emerging leader in the adoption of advanced, locally sourced water treatment chemicals.

United Kingdom: New Regulations and Sustainability Fuel Market Evolution

The UK’s market is defined by sweeping regulatory changes under the “Plan for Water” and the Environment Act 2021. There’s a strong focus on managing micropollutants and emerging contaminants, with research and investment directed at green chelating agents and biodegradable solutions for water treatment. Water companies are under pressure to upgrade facilities and adopt technologies that both minimize sludge toxicity and meet strict discharge limits for food and beverage processors.

Funding for research in bio-based and advanced chemical solutions is accelerating innovation, while sustainability requirements from both regulators and consumers are pushing the industry toward cleaner, safer, and more efficient water treatment practices.

Australia: Drought Resilience and Eco-Efficiency Lead Market Trends

Australia’s food & beverage water treatment chemicals market is shaped by acute water scarcity and strict environmental protection mandates. The sector is characterized by a drive for water conservation, efficiency, and protection of fragile aquatic ecosystems. Advanced controllers, sensors, and real-time chemical dosing are increasingly standard, supporting both quality and operational cost goals.

Australian companies are recognized for their leadership in sustainable sanitization solutions, collaborating with utilities and government agencies to optimize water use and minimize environmental impact. There’s also a focus on high-efficiency nutrient removal systems, reflecting a broader trend toward closed-loop, zero-waste operations that safeguard both public health and the environment.

Food and Beverage Water Treatment Chemicals Market Report Scope

Food and Beverage Water Treatment Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.1 Billion

|

|

Market Size (2034)

|

$7.3 Billion

|

|

Market Growth Rate

|

6.6%

|

|

Segments

|

By Type (Coagulants and Flocculants, Disinfectants and Biocides, Scale and Corrosion Inhibitors, pH Adjusters and Neutralizers, Oxygen Scavengers, Defoamers and Antifoaming Agents, Ion Exchange Resins, Membrane Performance Enhancers/Antiscalants, Cleaning and Sanitizing Agents, Specialty Chemicals), By Application (Process Water Treatment, Wastewater Treatment, Utilities Water Treatment), By Sub-Industry (Beverages, Food Processing, Food Service/Hospitality), By Source of Water (Groundwater, Surface Water, Municipal Water Supply, Recycled/Reused Water

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ecolab Inc. (U.S.), Solenis LLC (U.S.), BASF SE (Germany), Kemira Oyj (Finland), SUEZ SA (France), Kurita Water Industries Ltd. (Japan), Veolia Water Technologies (France), The Dow Chemical Company (U.S.), Buckman (U.S.), SNF Floerger (France), Solvay (Belgium), Arxada (Switzerland), Aries Chemical (U.S.), Genesis Water Technologies (U.S.),

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Food and Beverage Water Treatment Chemicals Market Segmentation

By Type

- Coagulants and Flocculants

- Disinfectants and Biocides

- Scale and Corrosion Inhibitors

- pH Adjusters and Neutralizers

- Oxygen Scavengers

- Defoamers and Antifoaming Agents

- Ion Exchange Resins

- Membrane Performance Enhancers/Antiscalants

- Cleaning and Sanitizing Agents

- Specialty Chemicals

By Application

- Process Water Treatment

- Wastewater Treatment

- Utilities Water Treatment

By Sub-Industry

- Beverages

- Bottled Water

- Carbonated Soft Drinks

- Juices

- Dairy Beverages

- Alcoholic Beverages

- Food Processing

- Dairy Processing

- Meat, Poultry, and Seafood Processing

- Fruits and Vegetables Processing

- Bakery and Confectionery

- Snacks and Savory Foods

- Sugar Processing

- Starch Processing

- Edible Oils and Fats

- Prepared Foods

- Food Service/Hospitality

By Source of Water

- Groundwater

- Surface Water

- Municipal Water Supply

- Recycled/Reused Water

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Food and Beverage Water Treatment Chemicals Market

- Ecolab Inc. (U.S.)

- Solenis LLC (U.S.)

- BASF SE (Germany)

- Kemira Oyj (Finland)

- SUEZ SA (France)

- Kurita Water Industries Ltd. (Japan)

- Veolia Water Technologies (France)

- The Dow Chemical Company (U.S.)

- Buckman (U.S.)

- SNF Floerger (France)

- Solvay (Belgium)

- Arxada (Switzerland)

- Aries Chemical (U.S.)

- Genesis Water Technologies (U.S.)

* List Not Exhaustive

Research Coverage

This report investigates the food and beverage water treatment chemicals market, presenting comprehensive analysis reviews, technological breakthroughs, and the latest trends shaping regulatory compliance, food safety, and sustainability. By integrating robust data from USDAnalytics, the study highlights segmental shifts, innovation in chemical formulations, and the operational priorities of food and beverage manufacturers adapting to circular water use and zero-liquid discharge initiatives. The report is an essential resource for water technology suppliers, plant operators, food processors, and policymakers, offering expert intelligence on market value trends, regional opportunities, and strategic company positioning across more than 25 countries.

Scope Highlights:

- Segmentation:

- By Type: Coagulants and Flocculants, Disinfectants and Biocides, Scale and Corrosion Inhibitors, pH Adjusters and Neutralizers, Oxygen Scavengers, Defoamers and Antifoaming Agents, Ion Exchange Resins, Membrane Performance Enhancers/Antiscalants, Cleaning and Sanitizing Agents, Specialty Chemicals

- By Application: Process Water Treatment, Wastewater Treatment, Utilities Water Treatment

- By Sub-Industry: Beverages, Food Processing, Food Service/Hospitality

- By Source of Water: Groundwater, Surface Water, Municipal Water Supply, Recycled/Reused Water

- Geographic Scope: Covers 25+ countries across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

- Data Coverage: Historic data from 2021 to 2024 and forecasts from 2025 to 2034.

- Key Players: Ecolab Inc. (U.S.), Solenis LLC (U.S.), BASF SE (Germany), Kemira Oyj (Finland), SUEZ SA (France), Kurita Water Industries Ltd. (Japan), Veolia Water Technologies (France), The Dow Chemical Company (U.S.), Buckman (U.S.), SNF Floerger (France), Solvay (Belgium), Arxada (Switzerland), Aries Chemical (U.S.), Genesis Water Technologies (U.S.).

Methodology

USDAnalytics applies a comprehensive research methodology, integrating expert interviews, real-world plant data, and cross-validated secondary sources, including industry reports, regulations, and technical publications. Market size and forecasts are developed using proprietary analytics and modeling, supported by trend mapping and comparative analysis for accuracy. Each segment is analyzed for qualitative and quantitative factors, ensuring that the findings deliver actionable, precise, and reliable insights to all stakeholders in the food and beverage water treatment chemicals market.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements