Chlorine Dioxide (ClO₂) Disinfectant Market for Drinking Water and Industrial Applications Growth Outlook

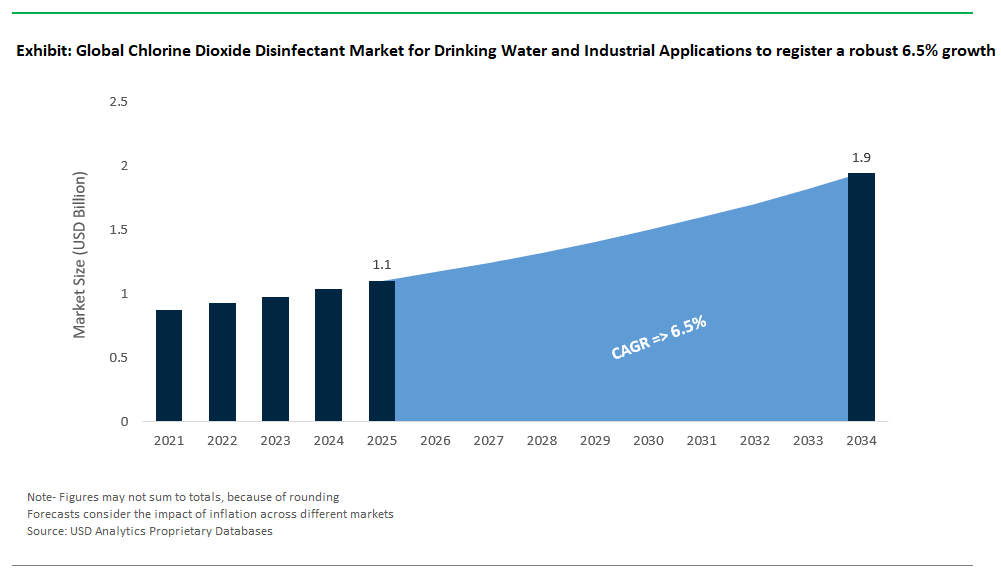

The chlorine dioxide (ClO₂) disinfectant market for Drinking Water and Industrial Applications is valued at $1.1 billion in 2025 and projected to grow to $1.9 billion by 2034, at a CAGR of 6.5%. This market is emerging as a strategic alternative to traditional halogen-based disinfection systems, offering better microbial inactivation performance, fewer byproducts, and a wider range of applications. Unlike chlorine, ClO₂ does not generate chlorinated trihalomethanes or haloacetic acids, making it more appealing in regulated environments that must reduce disinfection byproducts (DBPs). Its oxidative selectivity allows for effective pathogen control at much lower CT values; it can achieve 99.9% inactivation of chlorine-resistant Cryptosporidium parvum at just 15 mg·min/L, compared to chlorine’s 3,600 mg·min/L (USEPA EBM).

In industrial water systems, including HVAC and cooling towers, continuous ClO₂ dosing at 0.1–0.5 mg/L has proven effective in controlling Legionella while preventing corrosion a major concern for facilities with mixed-metal piping networks. Besides planktonic disinfection, ClO₂ is one of the few oxidants that can penetrate and control biofilms. Studies show that a residual of 0.5 mg/L can achieve a 3-log reduction in biofilm biomass within 24 hours, making it valuable in systems where biofouling can hurt thermal transfer or sanitation. However, the formation of chlorite (ClO₂⁻) remains a regulatory and operational issue, limited to 1.0 mg/L by the USEPA.

New generator technologies that optimize acid-chlorite ratios can reduce chlorite formation to less than 50% of applied ClO₂. This allows for safer long-term use in both municipal and industrial areas. As regulations tighten around emerging pathogens and DBP exposure, there is a growing demand for ClO₂ systems that integrate generators, are remotely monitored, and can adjust doses. This shift positions ClO₂ as a precisely controlled, multifunctional oxidant for 21st-century water systems.

Regulatory Shifts and Industrial Demand Fuel Growth in the Chlorine Dioxide Disinfectant Market

Market Trend: Chlorine Dioxide Emerges as Preferred Disinfectant Amid Regulatory Clampdown on Disinfection Byproducts

The chlorine dioxide (ClO₂) disinfectant market is seeing a significant increase in municipal water applications as utilities face stricter regulatory scrutiny over disinfection byproducts (DBPs). With the U.S. EPA focusing on DBP limits, many water utilities are moving away from free chlorine towards ClO₂-based systems. Unlike chlorine, ClO₂ does not create THMs or HAAs and remains effective at low concentrations (0.2–0.5 ppm). This makes it a compliant and efficient alternative.

Major water authorities are leading this change. The Los Angeles Department of Water & Power (LADWP) has begun piloting decentralized, on-site ClO₂ generators across old pipe networks and reports a 40% reduction in both pipeline corrosion and biofilm formation. Similarly, Singapore’s Public Utilities Board (PUB) is increasing ClO₂ dosing in surface water reservoirs after results showed it outperformed chloramines in controlling Legionella by five times. The benefits go beyond compliance; ClO₂ also helps extend asset life by reducing oxidative damage in iron, copper, and plastic pipes. Moreover, the historical cost difference that has hindered ClO₂ adoption is quickly disappearing. In this changing regulatory and technical landscape, chlorine dioxide is positioning itself not just as an alternative to chlorine but as a key disinfectant technology tailored for aging infrastructure, new pathogens, and sustainability-focused utilities.

Market Opportunity: Industrial Water Users Turn to ClO₂ for PFAS Destruction and Closed-Loop Disinfection Systems

There is a growing and underfunded opportunity in the chlorine dioxide market, especially in industrial water treatment particularly for advanced uses like PFAS removal, process water recycling, and biofilm control in valuable cooling systems. New research and pilot projects in 2024 show that ClO₂, particularly when activated by UV or paired with electrocoagulation, can effectively destroy perfluorinated compounds (PFAS) without needing high-pH conditions or expensive oxidants like ozone or hydroxyl radicals. A study from the University of Michigan found that ClO₂-UV combinations could degrade over 99% of PFOA and PFOS at neutral pH, representing a breakthrough in remediating wastewater contaminated with firefighting foam.

In addition to remediation, ClO₂ is becoming popular in closed-loop industrial water recycling. PepsiCo’s plant in Mexico uses a ClO₂-membrane hybrid to recycle up to 80% of process water while maintaining FDA-grade microbial control, which is vital for sustainable beverage operations. In highly sensitive settings like data centers, Microsoft’s Dublin facility has implemented ClO₂ dosing in closed-loop cooling systems to minimize Legionella risks without causing copper corrosion, a common side effect of traditional biocides. As industrial users strive for zero-liquid discharge (ZLD), regulatory compliance, and water resilience, chlorine dioxide’s selective oxidation, lack of lasting byproducts, and compatibility with membrane and electrochemical platforms make it an appealing choice for next-generation water management strategies. Along with the global move to phase out chlorine gas plants, this industrial shift is likely to drive double-digit growth in demand for ClO₂ generators, especially in areas and industries affected by PFAS that need non-corrosive, high-efficiency disinfection.

Competitive Landscape: Chlorine Dioxide (ClO₂) Disinfectant Market for Drinking Water and Industrial Applications

Chlorine dioxide (ClO₂) is a selective oxidizing biocide commonly used in drinking water and industrial water treatment. It is effective against microorganisms and produces few chlorinated byproducts, such as trihalomethanes. The competitive landscape consists of three main segments: precursor suppliers, generator system manufacturers, and integrators or solution providers. Notably, Solvay and Vasu Chemicals supply sodium chlorite. ProMinent, DuPont, Tecme, Iotronic, and CDG Environmental manufacture generator systems. ProMinent is a leader in chemical generation systems, while DuPont and Tecme focus on electrochemical generation using brine. Ecolab, SUEZ, and Evoqua incorporate ClO₂ systems into larger water treatment programs for municipal and industrial purposes. Companies like International Dioxcide, Accepta, Scotmas, and Vasu Chemicals provide stabilized ClO₂ solutions for applications in cooling towers, food safety, and biofilm control. Grundfos contributes to the segment with precision dosing pumps, which are essential for ClO₂ application. Key differences among competitors include safety in chemical handling, automation, dosing accuracy, and regulatory support in areas like municipal water, food and beverage, healthcare, and pulp and paper.

Chlorine Dioxide Disinfectant Market for Drinking Water and Industrial Applications – Segmentation Insights (2025–2034)

By Form: Liquid Chlorine Dioxide Leads the Market While Solid Form Records Fastest Growth

In the global chlorine dioxide disinfectant market, the liquid form holds the largest share, accounting for approximately 54.3% of the total market in 2025. This dominance is primarily due to the liquid form's ease of handling, precise dosing capabilities, and consistent performance in large-scale water treatment applications. Municipal water authorities and industrial facilities favor liquid chlorine dioxide for its superior solubility and rapid action against bacteria, viruses, and biofilms. Additionally, it is less corrosive and leaves minimal residuals compared to alternative disinfectants, making it a preferred solution for drinking water disinfection. In contrast, the solid form comprising powders and tablets is the fastest-growing format, projected to grow at a CAGR of 8.1% during 2025–2034. The growing adoption of solid chlorine dioxide is driven by its stability, lightweight transportability, and suitability for decentralized or portable disinfection systems, particularly in rural, emergency response, and low-resource settings. The gas form remains a consistent choice in industries like pulp and paper, where it is utilized for high-volume bleaching processes, though its growth is more moderate due to complex handling and safety requirements.

By Application: Drinking Water Treatment Dominates While Pharmaceutical Industry Grows Fastest

Drinking water treatment is the largest application segment in the chlorine dioxide disinfectant market, representing around 38.7% of total market share in 2025. Its dominant position is attributed to increasing global demand for safe and compliant drinking water, supported by rigorous disinfection regulations and rising concerns over waterborne diseases. Chlorine dioxide's high efficacy in neutralizing pathogens, without forming harmful chlorinated by-products, makes it a preferred disinfectant in municipal water treatment plants. On the other hand, the pharmaceutical industry is experiencing the highest growth rate, expanding at a robust CAGR of 7.8% through 2034. In this sector, chlorine dioxide is gaining ground for sterilizing cleanrooms, processing equipment, and water systems where microbial control is critical. The food and beverage industry is also contributing to growth, supported by increasing sanitation standards in production facilities. With an estimated CAGR of 9%, this segment is adopting chlorine dioxide for surface and pipeline disinfection. Meanwhile, applications in the pulp and paper, oil and gas, and healthcare industries continue to sustain stable demand, primarily driven by hygiene protocols, microbial control requirements, and environmental regulations.

.png)

United States: Regulatory Compliance and Industrial Adoption Drive ClO₂ Demand

The U.S. market for chlorine dioxide disinfectants is mature, underpinned by strict EPA regulations and an emphasis on public health. The EPA’s MRDL of 0.8 mg/L ensures ClO₂ is used effectively without exceeding safety thresholds for chlorite and chlorate by-products. A growing application is biofilm removal in water distribution systems, which enhances microbial safety and prevents secondary contamination.

Industrial demand is surging in the food and beverage sector, where ClO₂ sanitizes equipment and prevents cross-contamination without harmful residues. The EPA’s emergency disinfection guidelines highlight ClO₂ tablets as essential for crisis scenarios, demonstrating its versatility. The market is also witnessing rapid growth in on-site generation systems, reducing risks tied to chemical transport and storage while supporting sustainability goals.

China: Policy-Driven Expansion and On-Site Generation Technologies

China represents one of the fastest-growing markets for ClO₂ disinfectants, driven by the Action Plan for Water Pollution Control and significant public health initiatives. Investments in large-scale water treatment plants and industrial applications in cooling towers, pulp & paper, and textiles are fueling demand.

Safety and efficiency are central to innovation, with on-site generation technologies gaining traction as they eliminate transportation risks. ClO₂ is preferred for its strong biocidal properties, effective against Cryptosporidium and Giardia, and its ability to minimize harmful by-products. R&D efforts focus on improving the stability and cost-efficiency of ClO₂ systems, ensuring compliance with stringent national standards while addressing the need for decentralized water treatment.

Germany: Advanced Disinfection Standards and Chloramine-Free Solutions

Germany’s adoption of chlorine dioxide is reinforced by DIN 19643 standards, which limit disinfection by-products and prioritize health safety in swimming pools and public water systems. ClO₂ is extensively used for Legionella control and biofilm removal, reducing chloramine formation and improving air quality in indoor facilities.

The market is advancing through innovative generation systems offered by companies like ProMinent, providing continuous or on-demand ClO₂ production. Industrial sectors rely on ClO₂ for biofilm penetration and corrosion control, ensuring long-term integrity of pipelines and process water systems. Germany’s commitment to circular economy principles drives demand for eco-friendly and resource-efficient disinfection technologies.

India: Emerging Demand Fueled by Jal Jeevan Mission and Innovative Technologies

India’s ClO₂ market is expanding rapidly, powered by large-scale government programs such as Jal Jeevan Mission and Swachh Bharat Mission. These initiatives prioritize safe drinking water access and sustainable sanitation, creating vast opportunities for advanced disinfectants.

A major innovation is BARC’s CLEAN polymer technology, offering on-demand ClO₂ release for municipal and household applications. This solution is biodegradable and eco-friendly, addressing safety and sustainability concerns. Industrial sectors, including textiles and pharmaceuticals, are adopting ClO₂ for biofouling control and process water disinfection, ensuring compliance with environmental regulations.

Japan: Technological Leadership in Safe and Efficient ClO₂ Applications

Japan’s ClO₂ market is technologically sophisticated, supported by strict water safety standards and innovation-driven policies. Companies like Xylem and De Nora provide advanced generation systems tailored for municipal and industrial sectors.

ClO₂ is widely used as a pre-oxidant in surface water treatment, enabling the removal of iron and manganese without generating harmful disinfection by-products. It is also critical for Legionella control in healthcare and commercial facilities. Japan’s focus on automation, energy efficiency, and compact systems aligns with ClO₂’s versatility, making it a preferred disinfectant for high-density urban environments and sensitive industrial applications.

Brazil: Sanitation Framework Spurs Investment in ClO₂ Disinfection

Brazil’s market is growing due to its legal sanitation framework, which targets universal water and sewage treatment access by 2033. Large-scale infrastructure projects and private investments are driving ClO₂ adoption in municipal treatment facilities.

In the food and beverage sector, ClO₂ is increasingly used for equipment sanitization and microbial control, reducing reliance on chlorine-based solutions. The trend toward cost-effective and high-performance disinfection methods favors ClO₂ for its broad-spectrum efficacy and lower environmental impact, supporting Brazil’s sustainability objectives.

United Kingdom: Legionella Control and Sustainability Priorities Boost ClO₂ Demand

The UK market emphasizes water hygiene and risk management, guided by the Water Regulations Approval Scheme (WRAS) for ClO₂ use. Its role in Legionella prevention across hospitals, hotels, and commercial buildings is a key growth driver, as ClO₂ penetrates biofilms effectively.

Sustainability remains central, with companies introducing biodegradable formulations to reduce sludge toxicity and meet Environment Act 2021 targets. The UK government’s funding for green water treatment technologies further accelerates adoption, positioning ClO₂ as a vital component of advanced water management strategies.

South Korea: Smart Water Management Integration Enhances ClO₂ Utilization

South Korea’s market exemplifies smart technology integration in water treatment. Government-led projects like Smart Water Management (SWM) leverage IoT and real-time monitoring to optimize ClO₂ dosing and ensure compliance with water quality standards.

Industrial sectors, notably electronics and semiconductors, favor ClO₂ for biofouling control in ultra-pure water systems. The Framework Act on Water Management supports sustainable practices, reinforcing demand for ClO₂ in municipal and industrial applications. Coupled with investments in water reuse and desalination technologies, ClO₂ adoption aligns with South Korea’s commitment to efficiency and environmental stewardship.

Chlorine Dioxide Disinfectant Market for Drinking Water and Industrial Applications Report Scope

Chlorine Dioxide Disinfectant Market for Drinking Water and Industrial Applications

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.1 Billion

|

|

Market Size (2034)

|

$1.9 Billion

|

|

Market Growth Rate

|

6.5%

|

|

Segments

|

By Form (Liquid, Gas, Solid), By Application (Drinking Water Treatment, Industrial Water Treatment, Pulp and Paper Industry, Food and Beverage Industry, Oil and Gas Industry, Healthcare Industry, Pharmaceutical Industry, Agriculture Industry, Textile and Dye Industry, Swimming Pool and Spa Disinfection, Odor Control, Cleaning and Descaling), By Production Method/Generation (Chemical Method, Electrochemical Method

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ecolab (U.S.), ProMinent GmbH (Germany), SUEZ SA (France), Evoqua Water Technologies LLC (U.S.), Solvay (Belgium), International Dioxcide, Inc. (U.S.), CDG Environmental LLC (U.S.), Scotmas Limited (UK), Accepta Ltd. (UK), Grundfos Holding A/S (Denmark), Vasu Chemicals LLP (India), Tecme Srl (Italy), Iotronic Elektrogerätebau GmbH (Germany)

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Chlorine Dioxide Disinfectant for Drinking Water and Industrial Applications Market Segmentation

By Form

By Application

- Drinking Water Treatment

- Industrial Water Treatment

- Pulp and Paper Industry

- Food and Beverage Industry

- Oil and Gas Industry

- Healthcare Industry

- Pharmaceutical Industry

- Agriculture Industry

- Textile and Dye Industry

- Swimming Pool and Spa Disinfection

- Odor Control

- Cleaning and Descaling

By Production Method/Generation

- Chemical Method

- Electrochemical Method

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Chlorine Dioxide Disinfectant Market for Drinking Water and Industrial Applications

- Ecolab (U.S.)

- ProMinent GmbH (Germany)

- SUEZ SA (France)

- Evoqua Water Technologies LLC (U.S.)

- Solvay (Belgium)

- International Dioxcide, Inc. (U.S.)

- CDG Environmental LLC (U.S.)

- Scotmas Limited (UK)

- Accepta Ltd. (UK)

- Grundfos Holding A/S (Denmark)

- Vasu Chemicals LLP (India)

- Tecme Srl (Italy)

- Iotronic Elektrogerätebau GmbH (Germany)

* List Not Exhaustive

Research Coverage

This report offers an in-depth analysis of the Chlorine Dioxide (ClO₂) Disinfectant Market for Drinking Water and Industrial Applications, examining market growth, regulatory drivers, and segmentation by form, application, production method, and region. It reviews the transition from chlorine-based systems to ClO₂ for superior pathogen control, reduced disinfection by-products, and advanced industrial water treatment needs. The analysis spans emerging trends in on-site generation, biofilm and PFAS control, and decentralized disinfection, with detailed insights into municipal, industrial, and pharmaceutical adoption. USDAnalytics equips decision-makers and industry leaders with actionable market intelligence for navigating regulatory shifts, technology innovations, and growth opportunities in water disinfection.

Scope Highlights:

- Segmentation:

- By Form: Liquid, Gas, Solid

- By Application: Drinking Water Treatment, Industrial Water Treatment, Pulp & Paper, Food & Beverage, Oil & Gas, Healthcare, Pharmaceutical, Agriculture, Textile & Dye, Swimming Pool & Spa Disinfection, Odor Control, Cleaning & Descaling

- By Production Method: Chemical Method, Electrochemical Method

- Geographic Scope: Covers 25+ countries across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

- Data Coverage: Historic data from 2021 to 2024 and forecasts from 2025 to 2034.

- Key Players: Ecolab, ProMinent GmbH, SUEZ SA, Evoqua Water Technologies, Solvay, International Dioxcide, CDG Environmental, Scotmas, Accepta Ltd, Grundfos Holding, Vasu Chemicals, Tecme Srl, Iotronic Elektrogerätebau GmbH (list not exhaustive)

Methodology

USDAnalytics utilizes a rigorous, multi-source research methodology for the Chlorine Dioxide Disinfectant Market. The approach combines primary interviews with leading manufacturers, technology providers, utilities, and regulatory experts, along with comprehensive secondary research from industry databases, scientific journals, and market reports. Market sizing and forecasts are developed using proprietary models, triangulated with historic data (2021–2024) and forecast scenarios through 2034. Each segment is assessed for market share, adoption drivers, innovation impact, and regulatory influence, with particular attention to safety, environmental compliance, and new use cases. All insights are peer-reviewed and validated for reliability, ensuring industry stakeholders receive actionable, evidence-based guidance for strategy and investment.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements