Green Chelating Agents Market in Water Treatment: Industry Analysis and Growth Forecast

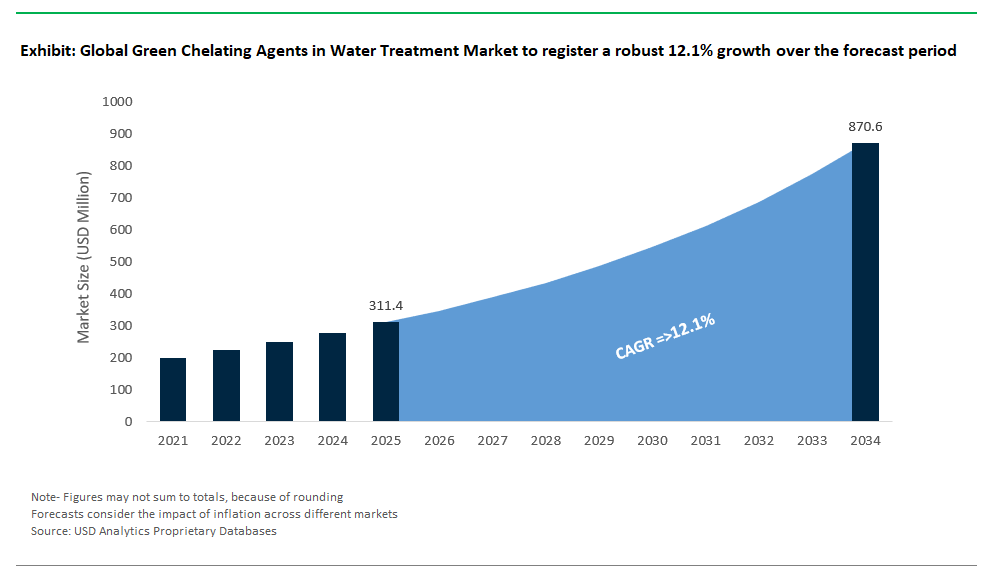

The green chelating agents in water treatment market is valued at $311.4 million in 2025 and projected to reach $870.5 million by 2034, reflecting a CAGR of 12.1%. The market is gaining significant traction as industrial sectors transition away from legacy chelators like EDTA and NTA compounds, long criticized for persistence, bioaccumulation, and aquatic toxicity. New-generation biodegradable chelants are redefining the standard for complexation efficiency without compromising environmental or regulatory benchmarks.

Among these, glutamic acid diacetate (GLDA) stands out for its calcium carbonate inhibition efficacy, achieving high inhibition rates at a dose of just 10 ppm while complying fully with OECD 301B biodegradability criteria (complete degradation, typically meaning >60% biodegradation, within 28 days). GLDA’s amino acid-based structure offers favorable metal chelation dynamics, low aquatic toxicity, and compatibility across a range of water treatment and cleaning applications.

In harsher thermal regimes, such as geothermal brine systems or high-pressure industrial boilers, phytate-based chelants are emerging as credible alternatives. These agents demonstrate strong ferric ion binding, while remaining functionally stable at temperatures up to 150°C and pressures approaching 10 bar an environment where traditional chelants often hydrolyze or lose binding affinity (Green Chem., 2023).

Regulatory acceptance has been a major driver for adoption, particularly in Europe, where REACH has flagged multiple synthetic chelants as Substances of Very High Concern (SVHC). In contrast, green chelants like GLDA and phytates register zero SVHC flags and exhibit marine LC50 values greater than 100 mg/L (OECD 202), ensuring compliance with wastewater discharge permits and Ecolabel criteria. These performance and safety credentials are being leveraged not only in water treatment but also in agrochemical formulations, personal care products, and household detergents.

The market trajectory is further reinforced by brand-led sustainability mandates, carbon footprint reduction targets, and rising stakeholder pressure to phase out legacy inputs from supply chains. Companies offering high-purity, application-specific green chelants with proven thermal, oxidative, and pH stability are expected to lead this transition, especially where regulatory, reputational, and ESG performance converge.

Sustainable Chemistry and Growth Opportunities in Green Chelating Agents for Water Treatment

Market Trend: Bio-Based and Biodegradable Chelators Replace Traditional Phosphonates

The global shift toward sustainable chemistry is catalyzing a rapid transformation in the chelating agents market, with bio-based and biodegradable alternatives displacing traditional phosphonates. In 2024, the EU’s regulations on phosphonates in consumer detergents and water treatment has created a demand surge for plant-derived chelators such as GLDA and IDS. Meanwhile, the U.S. EPA’s Safer Choice certification of tartaric acid-based chelators marks the formal market entry of next-generation agents into industrial boiler and cooling water systems. The sustainability case is compelling: traditional phosphonates degrade into persistent and non-biodegradable byproducts that disrupt aquatic ecosystems, whereas bio-chelators like GLDA are >60% biodegradable within 28 days. Importantly, performance is no longer a compromise studies published by ACS Sustainable Chemistry & Engineering (2024) confirm that GLDA offers equivalent metal-binding capacity to EDTA across a broad pH range. On the cost front, fermentation-based manufacturing has slashed GLDA prices to ~$2,500/ton, down from $3,800 in 2020, closing the affordability gap. Innovations are proving that chelation chemistry can align with circular economy principles, currently trialed in German municipal WWTPs for heavy metal remediation. With environmental compliance, cost efficiency, and performance converging, the market is rapidly coalescing around green chelators as the next standard in both industrial and consumer applications.

Growth Opportunity: Critical Mineral Recovery & Hydrometallurgy

A transformative growth frontier for green chelating agents lies in critical mineral extraction and hydrometallurgy, where selectivity, biodegradability, and chemical safety are emerging as differentiators. Technologies like EnergyX’s LiTAS™ are integrating GLDA-based leaching processes to enhance lithium recovery from hard rock sources like spodumene. This aligns with U.S. strategic supply chain goals and qualifies for 30% tax credits under the Inflation Reduction Act (IRA). Similarly, MP Materials is utilizing bio-chelators to extract rare earth elements (REEs) such as neodymium and praseodymium (Nd/Pr) from tailings, reducing hydrochloric acid usage, thereby improving safety and environmental impact. In industrial wastewater applications, Novel applications also include 3M’s modified cyclodextrins for PFAS chelation and destruction in landfill leachates, bridging the gap between heavy metal capture and persistent organic pollutant control. In agriculture, Food processors like Tyson Foods are leveraging GLDA to replace EDTA in cleaning-in-place (CIP) systems, achieving compliance with FDA 21 CFR §173.315. First-mover firms not only benefit from carbon credits but also hold patent portfolios that secure their market advantage. As global industries seek to decarbonize and detoxify resource-intensive processes, green chelating agents will play a pivotal role in closing resource loops and meeting next-gen sustainability mandates.

Competitive Landscape: Green Chelating Agents in Water Treatment

The shift from traditional chelants like EDTA and NTA to biodegradable options is changing formulation strategies in industrial water treatment, cleaning, and membrane systems. This change stems from increasing regulatory demands, customer preferences for sustainability, and the need for effective metal removal in various process conditions.

Dominance of Amino Acid-Based Chelants (GLDA, MGDA)

- GLDA and MGDA have become the top green chelants worldwide due to their biodegradability, wide-ranging metal chelation abilities, and balanced cost-performance.

- BASF and Nouryon are leaders in global manufacturing capacity and formulation knowledge. BASF’s Trilon® M (GLDA) and Trilon® C (MGDA) are essential components in the industrial water treatment and cleaning markets, especially for scale prevention and RO membrane protection. The company is working to increase Trilon® M capacity while also lowering its carbon footprint compared to EDTA and NTA.

- Nouryon provides a broad biodegradable range under its Dissolvine® brand, which includes GLDA, MGDA, and ASDA. The company aims to replace phosphonates like HEDP and NTA in cooling water and pulp and paper industries, utilizing its strong technical support.

- Kemira incorporates GLDA-based products (Kemconnect™ GLD) into wider treatment programs for boilers, cooling systems, and cleaning circuits. The company benefits from solid customer relationships, particularly in the pulp and paper and municipal water sectors. It is now focusing on mixing green chelants with polymers and phosphonates to improve cost and performance, especially under regulatory focus.

Bio-Based and Regional Adaptations

- Although GLDA and MGDA dominate the global market, various companies are developing alternative biodegradable or bio-sourced chelants suited to local economic and environmental needs.

- Aquapharm Chemicals targets cost-sensitive markets in Asia with its AP Chel™ bio-based chelants, designed for local water conditions and regulatory requirements. Their products emphasize phosphate-free solutions and are gaining popularity in textile, metal cleaning, and RO antiscalant uses.

- Tidal Vision takes a unique approach with its chitosan-based CrabShell™ products, which are bio-derived polymers capable of both chelation and flocculation. The company leverages its unique sourcing of raw materials and strong intellectual property to address niche markets, such as metal recovery from wastewater.

Specialty Chelants for High-Performance and Niche Applications

- Several companies are focusing on more demanding conditions where standard GLDA and MGDA may not perform well, such as high-temperature stability, heavy metal selectivity, or resistance to RO fouling.

- Nippon Shokubai sells HIDS (Hydroxyiminodisuccinic acid) for uses that require high thermal stability and strong chelation, like boiler water treatment and industrial cleaning. Its unique chemistry gives it an advantage in specialized markets in Japan and Asia.

- Dow markets Versene™ CA (EDDS), a biodegradable isomer of EDTA, for specific applications targeting transition metals like copper and iron. With a strong global presence, it integrates EDDS into formulations that require careful biodegradability, such as in personal care and water treatment.

Integration of Green Chelants into Broader Solutions

- Some companies focus on system-level solutions instead of just individual chelant products, especially when chelation is part of a complex treatment program.

- SNF Floerger, mainly a polymer manufacturer, includes biodegradable chelants in its FLOSPERSE™ Green line. The company emphasizes green offerings where flocculants and chelants work together, particularly in mining and difficult wastewater processes.

- Genesis Water Technologies acts as a solution provider, sourcing GLDA and MGDA from external suppliers and integrating them into personalized systems for heavy metal removal and RO pretreatment. Their value lies in customized engineering for clients focused on sustainability and complex waste issues.

Phosphonate-Based Intermediates in the Sustainability Transition

- Though not entirely biodegradable, some phosphonates are seen as more environmentally friendly because of their lower toxicity and greater stability in certain applications.

- Italmatch Chemicals sells PBTC (Phosphonobutane Tricarboxylic Acid) under its Dequest® PB brand. While PBTC is not easily biodegradable, it has a lower environmental impact than traditional phosphonates like HEDP and ATMP, placing it in a “greener” category. Italmatch pairs this with Dequest® GLDA for applications needing complete biodegradability, maintaining a solid presence in cooling water and detergent industries.

Green Chelating Agents in Water Treatment Market – Segmentation Insights (2025–2034)

By Type of Green Chelating Agent: GLDA Leads the Market While EDDS Grows Fastest

GLDA (L-Glutamic Acid N,N-diacetic Acid) holds the largest share in the green chelating agents market for water treatment, accounting for approximately 27.8% of the market in 2025. Its dominance is fueled by excellent biodegradability (>90%), strong chelation capabilities for calcium and magnesium ions, and broad applicability across municipal and industrial water systems. GLDA's favorable safety profile and low environmental persistence make it a preferred alternative to traditional synthetic chelators like EDTA. Meanwhile, EDDS (Ethylenediamine-N,N'-disuccinic Acid) is the fastest-growing chelating agent, projected to expand at a 13.6% CAGR through 2034. EDDS is particularly gaining traction for its effectiveness in complexing heavy metals such as copper, zinc, and nickel, making it ideal for remediation of industrial wastewater and contaminated groundwater. MGDA also continues to grow steadily in cleaning and water softening systems due to its fast biodegradation and compatibility with high-temperature processes. PASP (Polyaspartic Acid) is emerging as a dual-function scale inhibitor and biodegradable chelator, attracting interest from industrial cooling water and RO pre-treatment systems. Other bio-based agents such as sodium gluconate, citric acid, and sodium glucoheptonate maintain niche uses in food-grade and mild chelation applications, often favored in sensitive or eco-labeled product formulations.

.png)

By End-Use Industry: Municipal Sector Leads While Textile Industry Grows Fastest

Municipal water treatment remains the largest end-use segment for green chelating agents, representing approximately 34.7% of the market in 2025. This is driven by the increasing adoption of biodegradable chelants like GLDA and MGDA for iron and manganese sequestration in drinking water systems, replacing traditional phosphates and synthetic chelators under evolving environmental policies. Additionally, municipal facilities favor green chelating agents for corrosion control and metal stabilization in distribution networks. However, the textile industry is the fastest-growing segment, expanding at a 12.9% CAGR during the forecast period. As the sector shifts toward more sustainable dyeing and finishing processes, bio-based chelators are being used to stabilize dye baths, prevent metal-induced color shifts, and comply with eco-certifications. Industrial water treatment including boiler feed, cooling water, and membrane systems also sees steady growth, particularly where regulatory compliance and wastewater discharge limits are pushing demand for safer alternatives to phosphonates and EDTA. The food and beverage sector is increasingly adopting green chelators such as citric acid and GLDA, driven by clean-label processing standards and the need for residue-free water treatment solutions. The pulp and paper industry continues to rely on chelators for pitch control and bleaching, while other sectors such as electronics and cosmetics are gradually exploring green alternatives in response to consumer and regulatory pressures.

Germany: Strict EU Regulations and Green Chemistry Leadership Drive Demand for Biodegradable Chelating Agents

Germany stands at the forefront of the global green chelating agents market, leveraging strict EU environmental regulations and its long-standing leadership in green chemistry. The REACH Regulation is a significant driver, compelling industries to phase out traditional, non-biodegradable chelants like EDTA and adopt eco-friendly alternatives. BASF leads the innovation curve with its Trilon M (MGDA) and Trilon B (GLDA) product lines, both recognized for high biodegradability and superior performance in industrial and municipal water treatment applications.

The country’s commitment to a circular economy further boosts the adoption of green chelants. These agents prevent scale formation and corrosion in pipelines and critical equipment, improving operational efficiency and reducing maintenance costs in wastewater treatment plants. Additionally, their compatibility with resource recovery processes ensures that industries can reclaim valuable materials without chemical interference. Germany’s stringent regulations and sustainability-centric industrial ecosystem position it as a global innovation hub for next-generation water treatment chemicals.

United States: Sustainability Initiatives and Industry Innovation Accelerate Green Chelant Adoption

The United States is witnessing a paradigm shift toward eco-friendly water treatment chemicals, driven by growing sustainability commitments across industries and evolving state-level regulatory measures. While no federal ban exists on traditional chelants, major corporations and municipal utilities are voluntarily transitioning to biodegradable alternatives. Leading companies like Dow are investing heavily in R&D to develop green chelants that match or exceed the performance of EDTA and NTA, ensuring compliance with environmental standards while meeting industrial demands.

Industrial wastewater treatment remains the largest application segment for green chelants in the U.S., particularly in sectors such as electronics, semiconductors, and metal finishing. These agents effectively sequester heavy metals, preventing environmental contamination. Additionally, the food and beverage sector is adopting green chelants to maintain hygiene and enhance equipment cleaning without compromising safety. Coupled with the rise of AI-driven chemical dosing systems for optimized efficiency, the U.S. market is poised for sustained growth in sustainable water treatment solutions.

China: Policy-Driven Expansion and Bio-Based Innovations Power Market Growth

China’s market for green chelating agents is expanding rapidly, supported by stringent environmental regulations and a government-led commitment to green technology. National initiatives such as the "Water Ten Plan" and “Beautiful China” vision have spurred major investments in industrial wastewater treatment upgrades. Domestic producers like Shandong Taihe Water Treatment Technologies are developing bio-based chelants, such as GLDA, manufactured from renewable plant-derived raw materials to replace EDTA and other persistent chemicals.

Applications in textiles, pulp and paper, and metal processing are major growth areas, where green chelants help improve process efficiency and ensure compliance with revised discharge standards. Moreover, hybrid solutions that combine natural polymers with inorganic additives are gaining traction, offering superior metal ion control while maintaining biodegradability. As industrial modernization and environmental enforcement accelerate, China is set to dominate the Asia-Pacific green chelant market.

India: Government Initiatives and Cost-Effective Bio-Based Solutions Propel Market Growth

India is emerging as a high-potential market for green chelating agents, driven by rapid industrialization, ambitious water management programs, and the demand for sustainable solutions. Initiatives like the Jal Jeevan Mission and Namami Gange Program underscore the government’s commitment to water conservation and pollution control. Domestic innovators such as Aquapharm are spearheading the shift to biodegradable chelants like GLDA and IDS, providing eco-friendly solutions for sectors ranging from water treatment to food processing.

In industrial applications, green chelants are increasingly deployed for boiler and cooling water systems to prevent scale and corrosion, improving energy efficiency and reducing operational costs. The food industry is another major growth segment, where sustainable chelants ensure compliance with hygiene and safety standards. Supported by regulatory incentives and rising awareness, India’s green chelating agents market is transitioning from niche adoption to mainstream usage.

Japan: Advanced Manufacturing and Circular Economy Goals Drive Demand for High-Performance Green Chelants

Japan’s market for green chelating agents is characterized by technological innovation and strong regulatory frameworks aligned with its circular economy vision. Japanese companies, such as Nippon Shokubai, are developing advanced biodegradable chelants for applications in ultra-pure water systems critical for electronics and semiconductor manufacturing. These green chelants efficiently bind trace metal ions, ensuring the stringent purity levels required in high-tech industries.

Research institutions are exploring hybrid products that combine traditional and bio-based properties to enhance performance and improve biodegradability. Additionally, there is growing interest in resource recovery applications, where chelants facilitate the extraction of valuable metals from industrial effluents. This focus on innovation, coupled with Japan’s strict water quality regulations, positions the country as a leader in sustainable water treatment chemistry across Asia-Pacific.

Brazil: New Sanitation Framework and Bio-Based Supply Chain Strengthen Market Prospects

Brazil’s green chelating agents market is gaining momentum, fueled by the country’s new sanitation framework and strong emphasis on environmental sustainability. Recent legislation targeting universal water access by 2033 is catalyzing investments in municipal and industrial wastewater treatment infrastructure. Academic research is complementing these efforts, with studies on bio-based chelants derived from agricultural waste like sugarcane bagasse and soy residues.

The oil and gas and mining sectors represent key end-users, adopting green chelants to mitigate scale and corrosion challenges in pipelines and processing units. Brazil’s abundant biomass resources provide a cost advantage for local production of biodegradable chelants, supporting the development of a regional supply chain. These dynamics position Brazil as a strategic growth hub for green water treatment chemicals in Latin America.

United Kingdom: Regulatory Pressure and Innovation in Micropollutant Management Boost Market Growth

The United Kingdom is rapidly advancing in green water treatment solutions, propelled by the Plan for Water and the Environment Act 2021, which enforce stricter nutrient and contaminant control in wastewater systems. This regulatory environment is accelerating the adoption of green chelants for municipal and industrial applications. Research projects are exploring their effectiveness in micropollutant removal, addressing contaminants such as pharmaceuticals and personal care products that conventional treatment struggles to eliminate.

Private companies are investing in R&D for bio-based chemicals that minimize sludge toxicity and improve sustainability metrics. The UK government’s support for green innovation through funding programs ensures continued progress in water treatment technologies. With rising demand for environmentally responsible solutions, the UK market for biodegradable chelants is set for steady growth.

Australia: Water Scarcity and Ecosystem Protection Fuel Demand for Green Chelating Agents

Australia’s green chelating agents market is expanding in response to chronic water scarcity and the need to safeguard fragile aquatic ecosystems. With a high per-capita water consumption rate, the country prioritizes technologies that enable efficient water recycling and treatment. Green chelants are increasingly used in industrial and municipal sectors to prevent scale formation, reduce corrosion, and optimize resource use in water treatment systems.

Companies are also developing advanced dosing control systems integrated with green chelants to minimize chemical waste and energy use. Regulatory pressure to protect sensitive waterways, combined with an industry focus on sustainability, is creating significant growth opportunities for eco-friendly chelating agents. Australia’s position as a leader in sustainable water management underscores its critical role in the global transition to green water treatment chemicals.

Green Chelating Agents in Water Treatment Market Report Scope

Green Chelating Agents in Water Treatment Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$311.4 Million

|

|

Market Size (2034)

|

$870.5 Million

|

|

Market Growth Rate

|

12.1%

|

|

Segments

|

By Type of Green Chelating Agent (L-Glutamic Acid N,N-diacetic Acid (GLDA), Methylglycine Diacetic Acid (MGDA), Ethylenediamine-N,N'-disuccinic Acid (EDDS), Iminodisuccinic Acid (IDS), Polyaspartic Acid (PASP) and its Salts, Sodium Gluconate, Sodium Glucoheptonate, Citric Acid and its Salts, Other Bio-derived Chelators), By Function/Application in Water Treatment (Scale Inhibition, Corrosion Inhibition, Heavy Metal Removal/Sequestration, Hardness Control/Softening, Cleaning and Descaling, Enhancing Biocidal Efficacy, Oxidant Stabilization, Wastewater Treatment, Water Clarification), By End-Use Industry (Municipal Water Treatment, Industrial Water Treatment, Pulp and Paper, Textile, Food and Beverage, Other Industries

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE (Germany), Nouryon (The Netherlands), Kemira Oyj (Finland), Aquapharm Chemicals Pvt. Ltd. (India), Nippon Shokubai Co., Ltd. (Japan), The Dow Chemical Company (U.S.), SNF Floerger (France), Italmatch Chemicals S.p.A. (Italy), Tidal Vision (U.S.), Genesis Water Technologies, Inc. (U.S.),

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Green Chelating Agents in Water Treatment Market Segmentation

By Type of Green Chelating Agent

- L-Glutamic Acid N,N-diacetic Acid (GLDA)

- Methylglycine Diacetic Acid (MGDA)

- Ethylenediamine-N,N'-disuccinic Acid (EDDS)

- Iminodisuccinic Acid (IDS)

- Polyaspartic Acid (PASP) and its Salts

- Sodium Gluconate

- Sodium Glucoheptonate

- Citric Acid and its Salts

- Other Bio-derived Chelators

By Function/Application in Water Treatment

- Scale Inhibition

- Corrosion Inhibition

- Heavy Metal Removal/Sequestration

- Hardness Control/Softening

- Cleaning and Descaling

- Enhancing Biocidal Efficacy

- Oxidant Stabilization

- Wastewater Treatment

- Water Clarification

By End-Use Industry

- Municipal Water Treatment

- Industrial Water Treatment

- Pulp and Paper

- Textile

- Food and Beverage

- Other Industries

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Green Chelating Agents in Water Treatment Market

- BASF SE (Germany)

- Nouryon (The Netherlands)

- Kemira Oyj (Finland)

- Aquapharm Chemicals Pvt. Ltd. (India)

- Nippon Shokubai Co., Ltd. (Japan)

- The Dow Chemical Company (U.S.)

- SNF Floerger (France)

- Italmatch Chemicals S.p.A. (Italy)

- Tidal Vision (U.S.)

- Genesis Water Technologies, Inc. (U.S.)

* List Not Exhaustive

Research Coverage

This report investigates the Green Chelating Agents in Water Treatment Market, offering deep insights into emerging trends, technological breakthroughs, and sustainability-driven innovations that are reshaping the industry. USDAnalytics provides an extensive review of biodegradable chelants, their applications in water treatment, and integration strategies for high-performance industrial systems. This report highlights growth drivers, regulatory shifts, and competitive dynamics, making it an essential resource for industry professionals seeking actionable intelligence and strategic planning tools.

Scope Highlights:

- Segmentation:

- By Type of Green Chelating Agent: L-Glutamic Acid N,N-diacetic Acid (GLDA), Methylglycine Diacetic Acid (MGDA), Ethylenediamine-N,N'-disuccinic Acid (EDDS), Iminodisuccinic Acid (IDS), Polyaspartic Acid (PASP) and its Salts, Sodium Gluconate, Sodium Glucoheptonate, Citric Acid and its Salts, Other Bio-derived Chelators

- By Function/Application in Water Treatment: Scale Inhibition, Corrosion Inhibition, Heavy Metal Removal/Sequestration, Hardness Control/Softening, Cleaning and Descaling, Enhancing Biocidal Efficacy, Oxidant Stabilization, Wastewater Treatment, Water Clarification

- By End-Use Industry: Municipal Water Treatment, Industrial Water Treatment, Pulp and Paper, Textile, Food and Beverage, Other Industries

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Data Coverage: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies Covered: BASF SE, Nouryon, Kemira Oyj, Aquapharm Chemicals Pvt. Ltd., Nippon Shokubai Co. Ltd., The Dow Chemical Company, SNF Floerger, Italmatch Chemicals S.p.A., Tidal Vision, Genesis Water Technologies.

Methodology

USDAnalytics uses a hybrid methodology combining primary and secondary research to ensure robust market insights. Primary data is sourced from structured interviews with key stakeholders, including manufacturers, distributors, and water treatment experts. Secondary research includes analysis of technical papers, regulatory frameworks, and industry whitepapers. Market size estimations are derived through top-down and bottom-up approaches, validated by triangulation techniques. Forecasting considers technological advancements, regulatory changes, and sustainability trends, ensuring accuracy in projections for 2025–2034.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements