Asia-Pacific Pulp and Paper Industry Water Treatment Chemicals Market: Industry Growth Analysis and Value Forecast to 2034

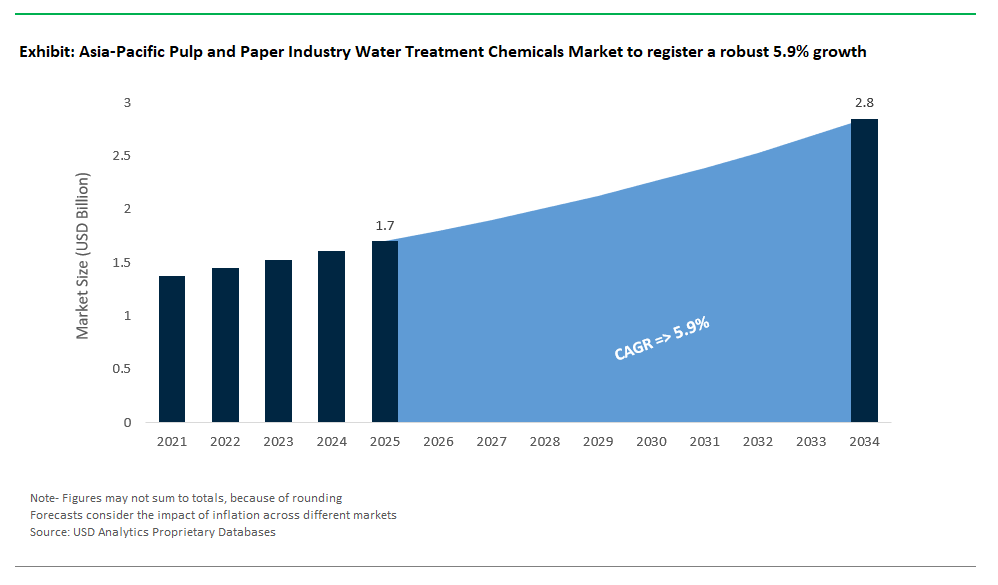

Asia-Pacific Pulp and Paper Industry Water Treatment Chemicals Market Size is estimated at $1.7 Billion in 2025 and is forecast to register an annual growth rate (CAGR) of 5.9% to reach $2.8 Billion by 2034.

The water treatment chemicals market in Asia-Pacific's pulp and paper industry is experiencing major changes. Mills across China, India, Indonesia, Vietnam, and other Southeast Asian countries are adjusting to different feedwater compositions, closed-loop production models, and stricter environmental discharge regulations. As these facilities work to improve process efficiency and meet sustainability requirements, they are optimizing chemical programs for better performance and lower environmental impact.

Coagulation and flocculation are essential for water clarification in pulp and paper mills. Traditional coagulants like aluminum sulfate (alum) and polyaluminum chloride (PAC) are commonly used, with dosages typically between 300 and 800 mg/L. These treatments can reduce chemical oxygen demand (COD) by up to 60%. However, they also produce significant sludge volumes, estimated at 0.8 to 1.5 kg of dry solids per ton of paper, especially in mills following India's Central Pollution Control Board (CPCB) guidelines. To lower sludge generation and improve efficiency, high-charge-density organic polymers such as polyDADMAC are becoming popular in Chinese mills, particularly those that process recycled fiber. These polymers can achieve turbidity removal rates over 90% at lower dosages and minimize environmental issues. In Indonesia, bio-based flocculants like modified cationic starch are being used as safer alternatives, meeting both performance and sustainability goals.

Biocide management is another key area of focus. As mills increasingly operate in closed or semi-closed loop systems, microbial buildup can hinder product quality and damage equipment. Chlorine dioxide is still widely used in alkaline process streams, especially in Japan, thanks to its effectiveness against biofilms and its lower potential for forming adsorbable organic halides (AOX). In Australia and parts of Southeast Asia, peracetic acid is gaining popularity due to its broad-spectrum antimicrobial properties and its biodegradable, non-halogenated byproducts. In Thailand and South Korea, where water reuse cycles are common, biocides like DBNPA (2,2-dibromo-3-nitrilopropionamide) and isothiazolinones are chosen for their short half-life and quick action, often breaking down fully within 24 hours. This allows mills to meet both microbial control and safety standards.

Managing deposits is crucial for controlling scale and organic fouling in utility and process water systems. In regions like Indonesia, where high-silica groundwater is often used in high-pressure boilers, scale inhibitors such as HEDP (1-hydroxyethylidene-1,1-diphosphonic acid) and PBTC (2-phosphonobutane-1,2,4-tricarboxylic acid) are commonly used. These phosphonates prevent calcium carbonate and calcium sulfate scaling under high temperature conditions. In Thailand's non-wood pulp mills, such as those that process rice straw, silica levels can exceed 250 ppm. In these cases, maleic acid-based copolymers help disperse colloidal silica. In Vietnam, where handling black liquor is common in kraft pulping, scale inhibitors with phosphinate groups are used to manage barium sulfate deposition, especially when saturation indices (SI) approach 2.0, as outlined in Vietnam's Decree 40/2019/ND-CP on environmental protection standards.

Tailoring chemical strategies to local needs is increasingly important. In India and Indonesia, where raw water often has high silica and magnesium levels, a mix of polyacrylate dispersants and magnesium chloride is used to manage scaling related to hardness. Chinese mills, especially those treating high-COD effluent streams, have adopted advanced oxidation processes like Fenton's reagent (a mix of hydrogen peroxide and iron salts) to break down difficult organics before biological treatment. Japan has taken the lead by using ozone-based bleaching and wastewater treatment technologies to comply with national AOX limits established by JIS K 0102 water quality standards. Meanwhile, mills in the Philippines facing high chloride concentrations often above 500 ppm are using ceramic membrane pretreatment systems and antioxidant dosing to prevent corrosion in stainless steel process lines.

Green chemistry innovations are gaining popularity across the region as mills strive to meet ESG goals and reduce their chemical usage. In Japan, sulfonated kraft lignin dispersants have been successful in lowering pitch deposition, with some mills reporting over 90% reductions in pitch-related fouling. In India, lipase-based enzyme treatments help break down triglycerides in process water, particularly in kraft pulping systems, providing operational return on investment (ROI) within a year due to less downtime and cleaner process circuits. China has also progressed by using electrochemical oxidation systems to lower COD in treated effluent, with units operating at energy consumption rates of around 8 to 12 kWh per kilogram of COD removed. This supports long-term goals of zero liquid discharge (ZLD) in water-stressed areas.

As water reuse and environmental compliance become central to pulp and paper operations across Asia-Pacific, chemical suppliers that provide integrated, low-impact, and digitally optimized solutions are best equipped to meet changing industrial needs. These suppliers must deliver high-performance formulas while ensuring regulatory compliance, safe handling practices, and compatibility with closed-loop and circular water systems. The region’s shift toward advanced treatment integration highlights the importance of innovation, sustainability, and local adaptation in the competitive market for water treatment chemicals.

Market Trend: ZLD Regulations Accelerate Uptake of Scale and Color Removal Solutions

The Asia-Pacific pulp and paper sector is shifting as more facilities adopt zero liquid discharge (ZLD) systems and face stricter discharge standards. Countries like China and India are updating their regulations. This reflects changes such as China’s draft GB standards and revisions from India’s Central Pollution Control Board. Mills must invest in better treatment strategies. Traditional coagulants and dispersants are increasingly replaced or supplemented with specialized inhibitors and decolorizing treatments, which are tailored to different raw materials like bamboo and bagasse. These non-wood fibers often produce higher levels of silica and color, which requires more specific chemical solutions.

For instance, mills that process bamboo may experience increased silica scaling, which leads to the need for strong scale inhibitors in their boiler and recovery systems. Additionally, treating black liquor-rich effluents especially in kraft mills using non-wood inputs demands oxidative or catalytic decolorization processes to lower color, chemical oxygen demand (COD), and biochemical oxygen demand (BOD). This is necessary to meet stricter national limits, like those set by Indonesia in recent technical regulations.

In addition to chemical choices, China’s expansion of emissions trading schemes and the introduction of discharge-based taxes encourage mill operators to reduce COD and BOD before discharge. This creates a demand for pre-oxidation methods, such as advanced oxidation or electrochemical treatments, to lower organic load and help meet ZLD targets. As mills increasingly close their process water loops, the need for durable, compatible chemical treatments that can perform under high cycles of concentration and within recirculated water systems is growing across the region.

Market Opportunity: Recycled Fiber Growth Spurs Demand for Stickies Control and Deinking Chemicals

The rise of recycled pulp production in the Asia-Pacific region is increasing the demand for stickies control agents and deinking chemicals. With more mills committed to using recycled fiber particularly old corrugated containers (OCC) issues with adhesive residues, pressure-sensitive adhesives (PSAs), waxes, and hot melt contaminants are becoming more common in closed-loop operations.

To tackle these challenges, mills are using advanced surfactant blends, polymer dispersants, and process-enhancing additives that prevent adhesive redeposition and boost debris removal during flotation and washing. More automated systems are being implemented to monitor water zeta potential, conductivity, and turbidity in real time. This optimizes chemical dosing and improves contaminant separation. This approach supports efficient drainage, fiber yield, and quality while minimizing overall chemical use.

Future innovations are likely to focus on enzymatic and biobased deinking aids that break down contaminants without harming fibers. High-performance dispersants designed specifically for OCC-based paper streams will also be important. These tools will help mills maintain pulp and water quality while adhering to stricter recycled-content regulations and environmental standards.

Strategic Insights

- ZLD mandates- Drive need for high-performance, ZLD-compatible chemicals

- Non-wood fiber processing- Requires robust scale and decolorization treatments

- Recycled fiber shift- Creates growth in stickies control and deinking solutions

- Automation & analytics- Enables more efficient chemical management

- Eco-focused innovations- Enzymatic and biobased chemistries gaining preference

The combined effect of regulatory pressure, feedstock variability, and closed-loop operations is changing the role of water chemistry. It is moving from a support function to a strategic part of mill sustainability and efficiency. Suppliers that can deliver application-specific, digital-ready, and environmentally sustainable chemical programs are likely to find the most success in the Asia-Pacific pulp and paper market.

Competitive Landscape: Asia-Pacific Pulp and Paper Industry Water Treatment Chemicals Market

The Asia-Pacific pulp and paper water treatment chemicals market is influenced by high service intensity, strict environmental regulations, and the need for chemical solutions that improve process efficiency and wastewater compliance. Key players compete across the full value chain, offering essential flocculants, deposit control agents, complete effluent treatment programs, and ZLD (zero liquid discharge) systems, along with wide-ranging portfolios and deep sector knowledge.

Global leaders like Kemira, Solenis, and Ecolab (Nalco Water) define the high-performance segment with their expertise in pulp and paper process chemistry. These companies provide integrated solutions that cover raw water, process water, and effluent treatment. Kemira is notable for its Superfloc® product line, which includes retention aids, drainage polymers, pitch control agents, biocides, and scale inhibitors, all tailored to the specific chemistry of paper mills. With extensive technical service and production capabilities in APAC, Kemira blends product innovation with strong regional responsiveness.

Solenis, which has roots in Ashland Hercules, offers a broad portfolio with products like Fennopol® and Fennofix® coagulants and flocculants, along with microbial control and defoamers. Its robust technical service capabilities extend across China, Southeast Asia, India, and Japan. Ecolab, through its Nalco Water division, integrates water treatment and process solutions with its proprietary 3D TRASAR™ digital monitoring platform. This platform provides mills with real-time chemical optimization and system control. These companies are especially valued by large and mid-sized mills aiming to lower chemical oxygen demand (COD), boost fiber yield, and meet water reuse targets.

SNF Floerger leads in the polymer flocculant segment, providing high-performance polyacrylamide-based products for process and effluent water applications. With significant manufacturing capacity in China and Australia, SNF is a vital partner for sludge dewatering and clarification in high-volume paper mills. Its leadership in commodity and specialty polymers makes it essential for both formulators and end-users in the region.

At the upstream end of the value chain, BASF, Mitsui Chemicals, and Dow supply key raw materials such as monomers, dispersants, chelants, and functional chemicals that support the formulations of many downstream companies. BASF’s Zetag® range of flocculants, along with its biocides, sizing agents, and defoamers, are widely used in APAC pulp and paper applications, backed by a strong regional manufacturing presence. Mitsui Chemicals contributes with specialty coagulant aids and papermaking additives, providing essential input to regional formulators and integrated companies.

Regional and domestic specialists like Kurita Water Industries, Ion Exchange (India), and Thermax are crucial players that utilize local knowledge and cost-effective service models. Kurita, with a strong position in Japan and a solid presence in Southeast Asia and China, offers customized chemical programs covering boiler and cooling systems, process defoamers, and effluent coagulants tailored for specific mill setups. Ion Exchange takes an integrated approach in India and Southeast Asia, combining coagulants, biocides, and antiscalants with the design and operation of ETPs and ZLD systems. Thermax is best known for its engineered water treatment systems but also provides an expanding range of treatment chemicals, particularly for effluent and cooling water circuits in paper mills.

Veolia Water Technologies works at the crossroads of chemical supply and engineering. It delivers water treatment programs, including its Hydrex® chemical line, as part of complete solutions for effluent management and resource recovery. Veolia’s ability to combine chemical dosing, biological treatment, and thermal ZLD technologies makes it well-suited for regions like India and China, where large-scale pulp and paper operations face growing regulatory demands.

Asia-Pacific Pulp & Paper Industry Water Treatment Chemicals Market – Segmentation Insights (2025–2034)

By Type of Chemical: Coagulants & Flocculants Lead While Nutrient Addition Grows Fastest

Coagulants and flocculants dominate the Asia-Pacific pulp and paper industry water treatment chemicals market, accounting for approximately 29.8% of the market in 2025. These chemicals are indispensable for primary wastewater clarification, helping to aggregate suspended solids, fibers, and colloidal matter before biological or tertiary treatment stages. Their effectiveness in reducing turbidity, total suspended solids (TSS), and color makes them central to both effluent treatment and recycled water recovery across paper mills. Biocides and dispersants also play a significant role in controlling microbial slime formation and deposit buildup on paper machine components, which can lead to operational inefficiencies and product defects. Meanwhile, nutrient addition is the fastest-growing category, projected to grow at a 6.7% CAGR through 2034. This growth is driven by the expansion of biological treatment systems in environmentally compliant “eco-mills,” where consistent nutrient dosing is essential to support microbial activity and ensure stable biological oxygen demand (BOD) removal. Other key chemical types include defoamers for white water loop control, pH adjusters for process balance, and retention aids for improving fiber recovery and dewatering efficiency. Dye fixatives, chelating agents, and de-inking formulations cater to specialty and recycled paper manufacturing segments, while oxidizing agents support bleaching and advanced oxidation processes.

By Application: Process Water Treatment Leads While Wastewater Treatment Grows Fastest

Process water treatment accounts for the largest share of chemical consumption in the pulp and paper sector, holding approximately 37.9% of the Asia-Pacific market in 2025. Water is heavily used throughout pulping, screening, bleaching, and papermaking operations, requiring ongoing chemical treatment to maintain pH balance, control microbial growth, enhance drainage, and ensure pulp quality. High chemical loadings are especially prevalent in kraft pulping and mechanical pulping operations, where process efficiency and water reuse depend on stable water quality. In contrast, wastewater treatment is the fastest-growing application segment, expanding at a 7.2% CAGR through 2034. Rising enforcement of industrial discharge norms particularly for chemical oxygen demand (COD), color, and total nitrogen across countries like China, Indonesia, and India is pushing mills to adopt advanced biological, tertiary, and zero-liquid discharge (ZLD) systems supported by chemical aids. Raw water treatment remains vital for pretreating river or groundwater sources used in pulp and paper plants, ensuring consistent quality for downstream operations. Heat exchanger cleaning, though a smaller application area, maintains relevance in kraft recovery and evaporator systems where scaling and organic deposition can compromise energy efficiency and heat recovery.

.png)

Asia-Pacific Pulp and Paper Industry Water Treatment Chemicals Report Scope

Asia-Pacific Pulp and Paper Industry Water Treatment Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.7 Billion

|

|

Market Size (2034)

|

$2.8 Billion

|

|

Market Growth Rate

|

5.9%

|

|

Segments

|

By Type of Chemical (Coagulants and Flocculants, Biocides and Dispersants, Defoamers and Antifoaming Agents, pH Adjusters and Neutralizers, Scale and Corrosion Inhibitors, Retention and Drainage Aids, Dye Fixatives and Color Removal Agents, Chelating Agents, De-inking Chemicals, Nutrient Addition (for biological treatment), Oxidizing Agents, Others), By Application (Raw Water Treatment, Process Water Treatment, Wastewater Treatment, Heat Exchanger Cleaning), By End-User (Pulp and Paper Mill Type) (Integrated Mills, Non-integrated Mills, Tissue Mills, Board Mills), By Form of Chemical (Liquid, Powder/Solid

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Kemira Oyj (Finland), Ecolab Inc. (U.S.), Solenis LLC (U.S.), Kurita Water Industries Ltd. (Japan), BASF SE (Germany), SNF Floerger (France), Ion Exchange (India) Ltd. (India), Veolia Water Technologies (France), Thermax Limited (India), Mitsui Chemicals Asia Pacific, Ltd. (Japan),

|

|

Countries

|

China, India, Japan, South Korea, Australia, South East Asia

|

Asia-Pacific Pulp and Paper Industry Water Treatment Chemicals Market Segmentation

By Type of Chemical

- Coagulants and Flocculants

- Biocides and Dispersants

- Defoamers and Antifoaming Agents

- pH Adjusters and Neutralizers

- Scale and Corrosion Inhibitors

- Retention and Drainage Aids

- Dye Fixatives and Color Removal Agents

- Chelating Agents

- De-inking Chemicals

- Nutrient Addition (for biological treatment)

- Oxidizing Agents

- Others

By Application

- Raw Water Treatment

- Process Water Treatment

- Wastewater Treatment

- Primary Treatment

- Secondary (Biological) Treatment

- Tertiary Treatment

- Sludge Dewatering and Conditioning

- Heat Exchanger Cleaning

By End-User (Pulp and Paper Mill Type)

- Integrated Mills

- Kraft Mills

- Sulfite Mills

- Mechanical Pulp Mills

- Non-integrated Mills

- Recycled Paper Mills

- Specialty Paper Mills

- Tissue Mills

- Board Mills

By Form of Chemical

By Country

- China

- India

- Japan

- South Korea

- Australia

- South East Asia

- Rest of Asia

Top Companies in Asia-Pacific Pulp and Paper Industry Water Treatment Chemicals Market

- Kemira Oyj (Finland)

- Ecolab Inc. (U.S.)

- Solenis LLC (U.S.)

- Kurita Water Industries Ltd. (Japan)

- BASF SE (Germany)

- SNF Floerger (France)

- Ion Exchange (India) Ltd. (India)

- Veolia Water Technologies (France)

- Thermax Limited (India)

- Mitsui Chemicals Asia Pacific, Ltd. (Japan)

* List Not Exhaustive

Research Coverage

This report by USDAnalytics investigates the Asia-Pacific Pulp and Paper Industry Water Treatment Chemicals Market, delivering a detailed analysis of chemical programs, technological innovations, and sustainability strategies impacting pulp and paper operations. It highlights breakthroughs in coagulants, flocculants, biocides, ZLD-compliant chemistries, and automation for advanced water reuse and effluent treatment. The analysis reviews regulatory influences, process integration challenges, and eco-focused trends shaping market growth. This report is an essential resource for manufacturers, chemical suppliers, and water management professionals aiming to enhance efficiency, reduce environmental impact, and achieve regulatory compliance across pulp and paper operations.

Scope Includes:

- Segmentation By Type of Chemical: Coagulants & Flocculants, Biocides, Defoamers, pH Adjusters, Scale Inhibitors, Retention Aids, Dye Fixatives, Chelating Agents, De-inking Chemicals, Nutrient Additives, Oxidizing Agents, Others

- Segmentation By Application: Raw Water Treatment, Process Water Treatment, Wastewater Treatment (Primary, Secondary, Tertiary), Heat Exchanger Cleaning

- Segmentation By End-User: Integrated Mills (Kraft, Sulfite, Mechanical Pulp), Non-integrated Mills (Recycled, Specialty), Tissue Mills, Board Mills

- Segmentation By Form of Chemical: Liquid, Powder/Solid

- Geographic Scope: Analysis of China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia

- Study Period: Historic: 2021–2024; Forecast: 2025–2034

- Companies Covered: Kemira Oyj, Ecolab Inc., Solenis LLC, Kurita Water Industries Ltd., BASF SE, SNF Floerger, Ion Exchange (India) Ltd., Veolia Water Technologies, Thermax Limited, Mitsui Chemicals Asia Pacific Ltd.

Methodology

This report applies a comprehensive research approach, integrating primary research through interviews with mill operators, chemical suppliers, and regulatory experts, combined with secondary data from technical journals, industry associations, and government publications. Market sizing uses bottom-up and top-down modeling, supported by demand-side validation and supply-side assessments. Advanced data triangulation ensures robust estimates, while trend analysis and scenario modeling incorporate factors such as regulatory changes, ZLD adoption, and recycled fiber demand. This methodology ensures actionable insights for stakeholders aiming to enhance operational efficiency and sustainability.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements