Seawater Desalination Systems Market Overview – Size, Growth Drivers, and Strategic Insights

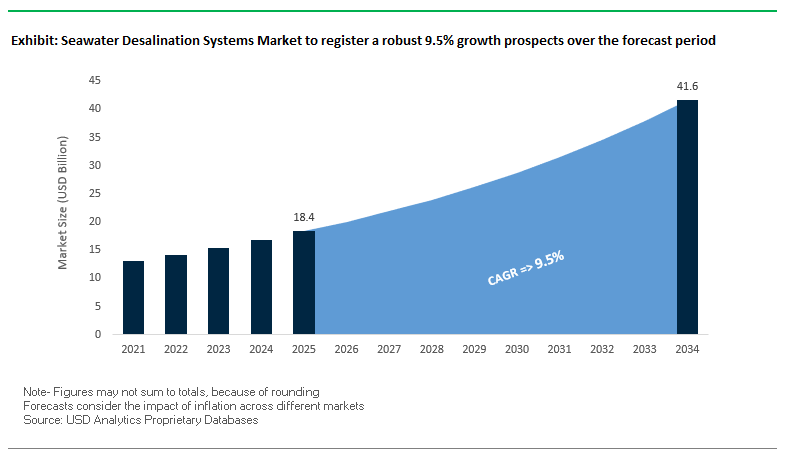

The global seawater desalination systems market is projected to grow from USD 18.4 billion in 2025 to USD 41.6 billion by 2034, registering a robust CAGR of 9.5%. The strong growth trajectory is driven by technological advancements in reverse osmosis (RO) membranes, significant government funding initiatives, and rising demand from water-stressed regions such as the Middle East and Asia.

A key factor propelling adoption is the dramatic reduction in energy consumption with modern RO plants operating at 3–4 kWh per cubic meter of freshwater compared to the 7–8 kWh of older systems. The improvement, achieved through advanced membranes and energy recovery devices, is making desalination both economically viable and environmentally sustainable.

Governments are playing a pivotal role in accelerating adoption. For example, in July 2025, the U.S. Department of the Interior announced USD 64 million in funding under the Bipartisan Infrastructure Law for desalination construction projects bolstering water security in drought-prone regions.

The Middle East and Asia remain the global epicenters for large-scale deployments, with landmark projects like the 300 MLD Yanbu SWRO plant in Saudi Arabia supporting national strategies such as Saudi Vision 2030.

Strategic imperatives for shareholders:

- Invest in energy-efficient desalination technologies to capture the shift toward sustainability.

- Target high-growth regions like the Middle East and Asia with mega-scale RO capabilities.

- Leverage public-private partnerships (PPPs) to mitigate project financing risks.

- Expand R&D into graphene-based membranes and advanced pre-treatment systems for longer plant lifecycles.

- Build capacity in offshore and industrial desalination to diversify revenue streams.

Market Analysis – Key Developments Reshaping the Seawater Desalination Systems Industry

The competitive and technological landscape of the seawater desalination systems market in 2025 is marked by a blend of mega-scale municipal projects, strategic acquisitions, and offshore industrial applications. In August 2025, Va Tech Wabag secured a USD 272 million contract to design and build a 300 MLD SWRO plant in Yanbu, Saudi Arabia as a flagship initiative under Saudi Vision 2030 aimed at ensuring long-term water security.

The month also saw IREL begin supplying 400,000 liters of drinking water daily from its Odisha desalination facility, developed with Bhabha Atomic Research Center technology. The 4.5 MLD plant exemplifies the rising trend of dual-purpose systems serving both industrial and community needs.

In June 2025, Veolia Water Technologies expanded into the offshore oil and gas segment with a multi-million-dollar contract to supply advanced desalination systems for two FPSOs in Brazil’s Santos Basin. Just a month prior, in May 2025, Veolia consolidated its position by acquiring the remaining 30% of its subsidiary Water Technologies and Solutions, streamlining operations to accelerate global project delivery.

Sustainability remains a defining trend. In March 2025, ACCIONA used World Water Day to spotlight RO’s environmental benefits, emphasizing 6.5x lower CO₂ emissions compared to traditional thermal methods. Meanwhile, IDE Technologies’ Sorek 2 plant in Israel achieved a 30% carbon footprint reduction and one of the lowest global production costs.

Trends and Opportunities in Seawater Desalination Systems Market

Trend 1: Energy-Efficient Desalination Gains Traction Due to Rising Energy Costs

The seawater desalination systems market is increasingly driven by the need for energy-efficient solutions. Traditional seawater reverse osmosis (SWRO) plants consume substantial energy, accounting for up to 70% of operational costs, prompting operators to adopt more sustainable technologies. Since the 1980s, energy requirements for desalination have dropped by roughly 80% due to technological advancements in reverse osmosis processes. Low-energy alternatives, such as forward osmosis (FO), membrane distillation (MD), and solar desalination, are gaining attention for their ability to utilize low-grade or renewable energy. Integrating solar panels and other renewable energy sources not only reduces electricity costs but also provides energy independence, making desalination more economically viable and environmentally sustainable. The trend is particularly relevant for large-scale municipal and industrial plants aiming to balance high output with lower operational costs.

Trend 2: Modular & Mobile Seawater Desalination Systems for Disaster Relief

Climate-related disasters and infrastructure failures are driving demand for modular and mobile seawater desalination systems. Containerized and vessel-based units can be deployed rapidly, providing critical freshwater access to disaster-affected communities. Their scalability allows multiple units to meet varying capacity needs, while off-grid operation ensures functionality even when local power grids are compromised. Real-world implementations, such as post-tsunami deployments in Tamil Nadu, India, demonstrated the effectiveness of mobile units producing up to 10 Kilo-Litres per Day (KLD) per system. These systems are designed to handle diverse water qualities with minimal pre-treatment, making them indispensable for emergency water management and disaster response planning.

Opportunity 1: Integration of AI & IoT for Predictive Maintenance in Large-Scale Desalination Plants

The complexity and scale of modern desalination plants offer a significant opportunity for AI and IoT integration. Predictive maintenance using sensor data from pumps, valves, and membranes helps anticipate failures, reduce downtime, and extend equipment life. AI optimizes energy consumption and chemical dosing, addressing one of the largest operational costs in desalination. Real-time quality assurance ensures that water consistently meets regulatory standards, while digital twin technology enables virtual simulation of plant operations to predict performance and prevent operational bottlenecks. The integration not only improves operational efficiency but also enhances sustainability and cost-effectiveness for large-scale desalination projects.

Opportunity 2: Green Desalination – Brine Mining for Valuable Minerals

Traditionally, brine from desalination plants is discharged into oceans, posing environmental risks. Brine mining, however, transforms the waste stream into a source of valuable minerals such as lithium, magnesium, and potassium. Globally, the minerals in desalination brine are valued at an estimated $2.2 trillion, including 15.8 million kilograms of lithium critical for batteries in electric vehicles. Extracting these minerals can offset up to 50% of desalination costs while reducing environmental impact. Technologies such as nanofiltration and electrodialysis enable high-purity mineral recovery and support circular economy initiatives, creating a sustainable and revenue-generating model for the desalination industry.

Seawater Desalination Systems Market Share Insights

By Technology Type: Reverse Osmosis Commands 76.2% While Thermal Retains Niche Role

Seawater Reverse Osmosis (SWRO) accounts for nearly 76.2% of the global desalination systems market by 2025, making it the undisputed technology of choice for new installations. Energy recovery devices (ERDs) that recycle up to 98% of pressure energy have slashed operating costs, cementing SWRO’s dominance in both municipal and industrial projects. By contrast, thermal desalination methods such as Multi-Stage Flash (MSF) and Multi-Effect Distillation (MED) maintain around 15% market share, particularly in the Middle East, where co-location with power plants and high-salinity feedwater still favor their deployment.

By System Capacity: Megaprojects Above 50,000 m³/day Define Global Production

Large-scale desalination plants above 50,000 m³/day contribute around 56.3% of global capacity, positioning them as the backbone of municipal water security in arid coastal regions. These megaprojects, often exceeding several hundred million dollars in contract value, are concentrated in the Middle East, North Africa, and parts of Asia. In comparison, mid-sized plants between 5,000–50,000 m³/day represent 34.2% of the market, serving regional hubs, island nations, and industrial complexes such as refineries and power plants, ensuring strategic diversification of supply.

By Plant Configuration: Onshore Dominates While Mobile Units Address Emergencies

Onshore desalination plants represent 83.2% of global deployments, driven by municipal-scale projects that require permanent, high-capacity infrastructure. Their role in national water security strategies underlines their continued dominance. However, mobile and containerized desalination systems, with around 8.1% market share, are increasingly vital for disaster relief, military deployments, and temporary supply gaps during plant maintenance or drought events. The segment reflects a growing demand for flexibility and rapid deployment in crisis-prone regions.

.png)

By Energy Source: Grid-Powered Leads, Renewables Accelerate Expansion

Conventional grid-powered plants still dominate with 71.2% of market share, but their environmental footprint has intensified the push toward renewable integration. Renewable-powered desalination plants, now accounting for 24.6% of the market, are the fastest-growing segment, fueled by advances in solar PV, wind-driven SWRO, and hybrid systems. The transition reflects the dual necessity of reducing operating costs and meeting decarbonization mandates, particularly in regions where electricity costs are a major contributor to water tariffs.

By End-User Sector: Municipal Utilities Drive Two-Thirds of Global Demand

Municipal utilities and governments account for about 67.8% of desalination demand, as water scarcity pressures urban centers from the Middle East to California to secure drought-resilient potable water. The segment defines the largest value contracts and dictates policy-driven adoption. In parallel, industrial users hold around 26.2% market share, with oil & gas, power generation, and mining sectors deploying desalination for process water and operational continuity. The reliability and independence from freshwater supplies make desalination indispensable to heavy industry.

By Brine Management: Discharge Still Prevails, But Resource Recovery Gains Momentum

Conventional brine discharge remains the dominant practice at 73.8% of plants, but growing environmental scrutiny and stricter regulations are reshaping the segment. Brine mining and Zero Liquid Discharge (ZLD) technologies, together representing 24.7% of the market, are emerging as the future of sustainable desalination, with research focusing on recovering lithium, magnesium, and potassium from concentrate streams. The evolution positions brine not as waste but as a potential revenue source, aligning with the circular economy transition.

Country Analysis of the Seawater Desalination Systems Market

Saudi Arabia: Vision 2030 Driving Privatization and Energy-Efficient Desalination

Saudi Arabia’s seawater desalination systems market is rapidly expanding under Vision 2030, with a strong focus on privatization and public-private partnerships (PPPs) led by the Saudi Water Partnership Company (SWPC). The government’s Saline Water Conversion Corporation (SWCC) is actively transitioning from energy-intensive Multi-Stage Flash (MSF) plants to energy-efficient reverse osmosis (RO) desalination systems, projected to reduce energy consumption per cubic meter by 80%. SWCC’s approved budget of $6.6 billion for 2023, along with plans to start five new plants by 2027, highlights the scale of investment. Additionally, Saudi Arabia is incorporating alternative energy sources like solar power into desalination projects to meet net-zero goals, while international collaborations, such as the Acciona-Power China project with a 600,000 m³/day capacity, further strengthen the country’s leadership in sustainable seawater desalination technologies.

United Arab Emirates: Clean Energy-Powered Large-Scale Desalination

The UAE seawater desalination systems market is fueled by the Water Security Strategy 2036 and Dubai’s Integrated Water Resource Management Strategy 2030. These policies aim to achieve 100% desalination using renewable energy and waste heat. The Hassyan Complex, utilizing seawater reverse osmosis (SWRO) technology, is one of the largest SWRO plants globally, with its first phase of 180 million gallons per day set for completion in 2027. The UAE emphasizes innovation through partnerships with academic institutions like Khalifa University, developing graphene-based nanostructured membranes and solar vapor generation techniques, ensuring energy-efficient and environmentally sustainable desalination solutions. Smart integration of desalination with renewable energy further positions the UAE as a hub for innovative seawater treatment technologies.

Israel: Global Leader in Desalination and Smart Modular Plants

Israel has transformed its water scarcity challenges into a model of innovation in seawater desalination systems, producing around 75% of its drinking water from the Mediterranean Sea. Companies such as IDE Technologies and Mekorot lead the development of advanced RO membranes with higher permeability, energy recovery devices, and smart modular desalination plants like Sorek II with 670,000 m³/day capacity. Israel’s Hadera plant exemplifies low-energy, low-chemical desalination technologies, emphasizing efficiency and sustainability. The country also excels in wastewater reuse, reclaiming nearly 90% of water for agriculture, highlighting its leadership in circular water economy solutions and sustainable water supply systems.

United States: Federal Investment in Innovative Desalination and Water Recycling

The U.S. seawater desalination systems market benefits from federal funding under the Biden-Harris administration, including over $300 million for water recycling, storage, and desalination projects. The Bureau of Reclamation provides up to $64 million for construction of desalination plants, supporting ocean and brackish water treatment for municipal and irrigation purposes. Programs like the Desalination and Water Purification Research Program drive innovation, enabling the development of novel technologies to make previously unusable water accessible. EPA-backed research emphasizes cost-effective, energy-efficient, and environmentally friendly desalination solutions, making the U.S. market a hub for advanced seawater treatment and smart water infrastructure.

China: Government-Led Expansion and Automation in Desalination

China has prioritized seawater desalination systems under its 14th Five-Year Plan to address water scarcity amid rapid urbanization and industrialization. The largest industrial membrane-based desalination plant in Shandong Province, built by SUEZ, utilizes advanced RO membranes and is fully automated, reflecting the country’s focus on smart operations. Thermal drainage from power plants is being used to reduce conventional energy consumption during winter months. Innovations include a new polyester thin film that resists chlorine and hydrolytic degradation, simplifying pre-treatment steps. China aims to expand desalination capacity to 3.5 million cubic meters per day by 2025, promoting urban use of desalinated seawater and supporting sustainable water supply systems.

Japan: Advanced Membrane Systems and Hybrid Desalination Innovations

Japan’s seawater desalination market is characterized by advanced technological innovation, led by companies like Hitachi and Toray Industries. Hitachi’s revolutionary system mixes seawater with treated wastewater to dilute salinity, reducing pumping costs and achieving over 30% energy savings. In Fukuoka, ultrafiltration membranes replace traditional sand filtration, ensuring stable clean water supply and minimizing maintenance. Newly developed 60% collection membranes reduce facility footprint and costs. Companies like Kanadevia and Osmoflo provide rental RO-based desalination solutions, supporting temporary water supply during emergencies, highlighting Japan’s focus on compact, efficient, and technologically advanced seawater treatment solutions.

Competitive Landscape – Key Players Driving Innovation and Market Leadership

The seawater desalination systems market is highly competitive, dominated by a mix of multinational water technology leaders and regionally specialized EPC contractors. Players are differentiating through proprietary RO technologies, energy efficiency gains, and integrated lifecycle services that encompass design, construction, and long-term O&M.

ACCIONA Agua – Championing Sustainable RO Desalination

ACCIONA focuses on delivering large-scale SWRO plants for both municipal and industrial clients, with an emphasis on sustainability and low energy use. The company’s Shuqaiq III plant in Saudi Arabia, with a capacity of 450,000 m³/d, serves over 2 million people and cements its Middle Eastern footprint. Expansion in Australia and BOT-financed projects are strengthening its global presence. Its core strength lies in proprietary low-energy RO technology and expertise in executing complex infrastructure projects.

Veolia Water Technologies – Integrating Technology and Sustainability

Veolia’s desalination portfolio spans reverse osmosis and thermal processes, with innovations like the Barrel™ modular RO system reducing plant costs by 3–5% and cutting energy use by 1.5%. The company’s May 2025 full acquisition of WTS streamlines operations, while its June 2025 offshore project in Brazil underscores its diversification strategy. Veolia’s global presence, coupled with integrated digital and chemical solutions, makes it a leader in addressing both municipal and industrial water needs.

IDE Technologies – Pioneering Low-Carbon, High-Recovery Systems

IDE specializes in mega-scale RO projects such as Sorek 1 and Sorek 2, the latter delivering a 30% lower carbon footprint at competitive costs. Proprietary solutions like PFRO™ and MAXH₂O Desalter enable ultra-high recovery and waste minimization. With deep expertise in sustainable design and high-efficiency membranes, IDE holds a strong advantage in cost-sensitive and environmentally regulated markets.

SUEZ (Part of Veolia) – Legacy in Resilient Water Infrastructure

Now integrated into Veolia, the former SUEZ brought expertise in large-scale SWRO plants and municipal water supply, such as Bahrain’s Al Dur 2 facility. Its experience in water reuse and produced water treatment enhances Veolia’s integrated service offerings, reinforcing its position in water-stressed geographies.

Va Tech Wabag Ltd. – EPC Leader in Mega-Scale Desalination

Va Tech Wabag excels in turnkey RO projects, offering design-to-commissioning services. Its USD 272 million Yanbu SWRO project in August 2025 positions it among the top EPC players in the Middle East. Its competitive edge lies in its engineering expertise, reverse osmosis specialization, and ability to deliver large, complex infrastructure under challenging environmental conditions.

Seawater Desalination Systems Market Report Scope

Seawater Desalination Systems Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$18.4 Billion

|

|

Market Size (2034)

|

$41.6 Billion

|

|

Market Growth Rate

|

9.5%

|

|

Segments

|

By Technology Type (Reverse Osmosis (SWRO), Conventional SWRO, Energy Recovery SWRO, Hybrid SWRO, Forward Osmosis (FO), Nanofiltration (NF) Pretreatment, Thermal Desalination, Solar Desalination, Membrane Distillation, Others), By System Capacity (<5,000 (m³/day), 5,000–50,000 (m³/day), >50,000 (m³/day)), By Plant Configuration (Onshore Plants, Offshore/Vessel-Based, Mobile/Containerized Units, Hybrid Plants), By Energy Source (Grid-Powered Conventional, Renewable-Powered, Waste Heat Utilization), By End-User Sector (Municipal, Industrial, Commercial, Military/Government), By Brine Management (Conventional Discharge, Brine Concentration, Brine Mining, Zero Liquid Discharge (ZLD))

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia, SUEZ, Xylem Inc., IDE Technologies, ACCIONA, Doosan Enerbility, Abengoa S.A., Aquatech International LLC, Evoqua Water Technologies (now part of Xylem), DuPont, Thermax Limited, VA Tech Wabag, Biwater Holdings Limited, Hitachi Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Seawater Desalination Systems Market Segmentation

By Technology Type

- Reverse Osmosis (SWRO)

- Conventional SWRO

- Energy Recovery SWRO

- Hybrid SWRO

- Forward Osmosis (FO)

- Nanofiltration (NF) Pretreatment

- Thermal Desalination

- Solar Desalination

- Membrane Distillation

- Others

By System Capacity

- <5,000 (m³/day)

- 5,000–50,000 (m³/day)

- >50,000 (m³/day)

By Plant Configuration

- Onshore Plants

- Offshore/Vessel-Based

- Mobile/Containerized Units

- Hybrid Plants

By Energy Source

- Grid-Powered Conventional

- Renewable-Powered

- Waste Heat Utilization

By End-User Sector

- Municipal

- Industrial

- Oil & Gas

- Power Plants

- Mining

- Others

- Commercial

- Hotels/Resorts

- Cruise Ships

- Military/Government

By Brine Management

- Conventional Discharge

- Brine Concentration

- Brine Mining

- Zero Liquid Discharge (ZLD)

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Seawater Desalination Systems Market

- Veolia

- SUEZ

- Xylem Inc.

- IDE Technologies

- ACCIONA

- Doosan Enerbility

- Abengoa S.A.

- Aquatech International LLC

- Evoqua Water Technologies (now part of Xylem)

- DuPont

- Thermax Limited

- VA Tech Wabag

- Biwater Holdings Limited

- Hitachi Ltd.

* List Not Exhaustive

Research Coverage

This report investigates the Global Seawater Desalination Systems Market, delivering in-depth analysis reviews of growth drivers, regulatory frameworks, and technological breakthroughs reshaping the industry through 2034. Published by USDAnalytics, the study highlights how next-generation reverse osmosis (RO) membranes, energy recovery devices, and government-backed infrastructure funding are redefining desalination economics and sustainability. It also reviews landmark regional projects in the Middle East, Asia, and the U.S., along with emerging opportunities in modular systems, AI integration, and brine mining. With coverage of competitive strategies, regional dynamics, and transformative technology adoption, this report is an essential resource for utilities, EPC contractors, policymakers, and investors seeking to navigate the evolving seawater desalination systems landscape.

Scope Includes:

- Segmentation: By Technology Type (Reverse Osmosis, Multi-Stage Flash, Multi-Effect Distillation, Forward Osmosis, Membrane Distillation, Solar Desalination), By System Capacity (Up to 5,000 m³/day, 5,000–50,000 m³/day, Above 50,000 m³/day), By Plant Configuration (Onshore, Offshore, Mobile/Containerized), By Energy Source (Grid-Powered, Renewable-Powered, Hybrid), By End-User Sector (Municipal Utilities, Industrial, Military & Emergency Response), and By Brine Management (Discharge, Zero Liquid Discharge, Brine Mining).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historic Data: 2021 to 2024, and Forecast Data: 2025 to 2034.

- Companies: Profiles and analysis of 15+ leading players including Veolia, IDE Technologies, ACCIONA, Va Tech Wabag, and SUEZ.

Methodology

The research methodology adopted by USDAnalytics combines primary interviews with industry stakeholders and extensive secondary research to ensure robust and reliable insights. Primary data was collected from plant operators, technology developers, regulators, and EPC contractors to validate market assumptions, technology adoption patterns, and investment priorities. Secondary research leveraged government reports, desalination project databases, company filings, and peer-reviewed studies to build a comprehensive market base. Market sizing employed both top-down and bottom-up approaches, with triangulation across technology type, system capacity, and regional deployment. Advanced scenario modeling factored in energy costs, climate-driven water scarcity, renewable integration, and brine management innovations, enabling precise long-term forecasts aligned with real-world industry dynamics.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Seawater Desalination Systems Market

1. Executive Summary

1.1. Market Highlights

1.2. Strategic Imperatives for Stakeholders

1.3. Global Market Snapshot

2. Seawater Desalination Systems Market Overview & Outlook (2025–2034)

2.1. Introduction to Seawater Desalination Systems Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $18.4 Billion

2.2.2. Forecasted Market Size (2034): $41.6 Billion at 9.5% CAGR

2.3. Key Drivers and Market Dynamics

2.3.1. Technological Advancements in Reverse Osmosis (RO) Membranes

2.3.2. Significant Government Funding Initiatives

2.3.3. Rising Demand from Water-Stressed Regions

3. Market Analysis: Key Developments Reshaping the Desalination Industry

3.1. Overview of Mega-Scale Projects and Strategic Acquisitions

3.2. Strategic Developments of Key Players

3.2.1. Va Tech Wabag's $272 Million Yanbu SWRO Plant Contract (August 2025)

3.2.2. IREL's Dual-Purpose Desalination Facility in Odisha (August 2025)

3.2.3. Veolia Water Technologies' Expansion into Offshore and Full Acquisition of WTS (May-June 2025)

3.2.4. ACCIONA's Focus on Environmental Benefits and IDE Technologies' Low-Carbon Achievements (March 2025)

3.3. Major Infrastructure Projects and Long-Term Contracts

4. Breakthrough Innovations in the Seawater Desalination Systems Market

4.1. Trend 1: Energy-Efficient Desalination

4.1.1. Technological Advancements and Cost Reduction

4.1.2. Integration with Renewable Energy Sources

4.2. Trend 2: Modular & Mobile Systems for Disaster Relief

4.2.1. Rapid Deployment and Scalability

4.2.2. Off-Grid Operation for Emergency Water Management

4.3. Opportunity 1: AI & IoT for Predictive Maintenance

4.3.1. Optimizing Operations and Reducing Downtime

4.3.2. Enhancing Sustainability and Cost-Effectiveness

4.4. Opportunity 2: Brine Mining for Valuable Minerals

4.4.1. Turning Waste Streams into a Revenue Source

4.4.2. Supporting Circular Economy Initiatives

5. Competitive Landscape: Key Players Driving Innovation and Market Leadership

5.1. ACCIONA Agua: Championing Sustainable RO Desalination

5.2. Veolia Water Technologies: Integrating Technology and Sustainability

5.3. IDE Technologies: Pioneering Low-Carbon, High-Recovery Systems

5.4. SUEZ (Part of Veolia): Legacy in Resilient Water Infrastructure

5.5. Va Tech Wabag Ltd.: EPC Leader in Mega-Scale Desalination

5.6. Other Key Players

6. Market Share and Segmentation Insights: Seawater Desalination Systems Market

6.1. By Technology Type

6.1.1. Reverse Osmosis Commands 75%

6.1.2. Thermal Desalination Retains Niche Role (15%)

6.2. By System Capacity

6.2.1. Megaprojects (>50,000 m³/day) Define Global Production (55% Share)

6.2.2. Mid-sized Plants (5,000–50,000 m³/day)

6.3. By Plant Configuration

6.3.1. Onshore Dominates (85% Share)

6.3.2. Mobile/Containerized Units Address Emergencies (7% Share)

6.4. By Energy Source

6.4.1. Grid-Powered Leads (70% Share)

6.4.2. Renewables Accelerate Expansion (25% Share)

6.5. By End-User Sector

6.5.1. Municipal Utilities Drive Demand (65% Share)

6.5.2. Industrial Users (25% Share)

6.6. By Brine Management

6.6.1. Conventional Discharge Prevails (75% Share)

6.6.2. Brine Mining and ZLD Gain Momentum (25% Share)

7. Country Analysis and Outlook of Seawater Desalination Systems Market

7.1. Saudi Arabia: Vision 2030 Driving Privatization and Energy-Efficient Desalination

7.2. United Arab Emirates: Clean Energy-Powered Large-Scale Desalination

7.3. Israel: Global Leader in Desalination and Smart Modular Plants

7.4. United States: Federal Investment in Innovative Desalination

7.5. China: Government-Led Expansion and Automation in Desalination

7.6. Japan: Advanced Membrane Systems and Hybrid Innovations

7.7. Other Country Analysis

8. Market Size Outlook by Region (2025–2034)

8.1. North America Seawater Desalination Systems Market Size Outlook to 2034

8.1.1. By Technology Type

8.1.2. By System Capacity

8.1.3. By Plant Configuration

8.1.4. By End-User Sector

8.1.5. By Brine Management

8.2. Europe Seawater Desalination Systems Market Size Outlook to 2034

8.2.1. By Technology Type

8.2.2. By System Capacity

8.2.3. By Plant Configuration

8.2.4. By End-User Sector

8.2.5. By Brine Management

8.3. Asia Pacific Seawater Desalination Systems Market Size Outlook to 2034

8.3.1. By Technology Type

8.3.2. By System Capacity

8.3.3. By Plant Configuration

8.3.4. By End-User Sector

8.3.5. By Brine Management

8.4. South America Seawater Desalination Systems Market Size Outlook to 2034

8.4.1. By Technology Type

8.4.2. By System Capacity

8.4.3. By Plant Configuration

8.4.4. By End-User Sector

8.4.5. By Brine Management

8.5. Middle East and Africa Seawater Desalination Systems Market Size Outlook to 2034

8.5.1. By Technology Type

8.5.2. By System Capacity

8.5.3. By Plant Configuration

8.5.4. By End-User Sector

8.5.5. By Brine Management

9. Research Coverage & Methodology

9.1. Report Scope and Focus

9.2. Research Methodology

9.3. Deliverables

10. Appendix

10.1. List of Tables

10.2. List of Figures

10.3. Abbreviations