PFAS Filtration Market Overview

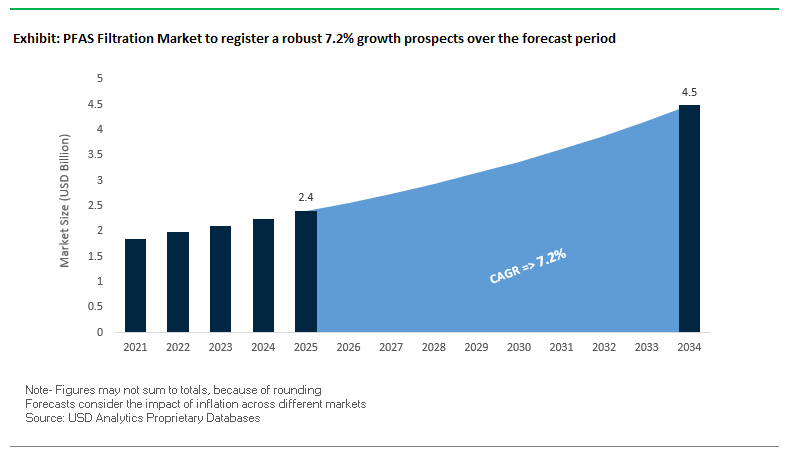

The global PFAS filtration market is projected to grow from $2.4 billion in 2025 to $4.5 billion by 2034, reflecting a robust CAGR of 7.2%. This surge is driven by increasing regulatory mandates, heightened public health awareness, and widespread contamination across multiple industries, including semiconductor manufacturing, textiles, and electronics. The market’s expansion is further propelled by technological innovations designed to efficiently remove both long- and short-chain PFAS compounds, addressing complex water treatment challenges.

For industry Stakeholders and buyers, key market drivers include compliance with stringent EPA regulations, growing adoption of granular activated carbon (GAC) and ion exchange resins, and an intensified focus on protecting public health through safe water solutions. The market also reflects a trend toward integrated digital water management systems, improving operational efficiency and treatment effectiveness.

Key Insights for Industry Stakeholders:

- Regulatory Mandates: U.S. EPA PFAS Strategic Roadmap accelerates demand for effective filtration.

- Public Health Concerns: Exposure to PFAS is linked to adverse health outcomes, increasing urgency for treatment.

- Cross-Industry Contamination: Semiconductor, textile, and electronics sectors are key PFAS contributors.

- Technological Innovation: Advanced GAC and ion exchange resins target both long- and short-chain PFAS.

- Digital Integration: AI and IoT-enabled systems optimize treatment performance and resource management.

Market Analysis: Recent Developments in PFAS Filtration

The PFAS filtration market has seen substantial innovation and strategic developments in 2024–2025. In August 2025, RSE and Siemens signed an MoU to integrate Siemens’ digital, automation, and AI technologies into RSE’s modular water treatment systems, accelerating decarbonization and operational efficiency. July 2025 marked the opening of one of the largest PFAS treatment plants in the U.S. by Veolia in Delaware, employing proprietary technologies to destroy targeted PFAS compounds, showcasing the industry’s response to emerging contaminants.

In June 2025, AECOM partnered with Aquatech to deploy DE-FLUORO™ technology, combining environmental expertise with advanced electrochemical processes for scalable PFAS destruction. May 2025 saw AqueoUS Vets introduce its FoamPro system, a vacuum-based foam fractionation technology that removes over 99% of targeted PFAS compounds, emphasizing energy-efficient solutions.

Strategic acquisitions and technology rollouts also shape the market. In December 2024, Xylem Inc. acquired Idrica, enhancing its digital water management portfolio to optimize PFAS treatment. August 2024 saw ABB release next-generation electromagnetic flowmeters with embedded IoT connectivity, enabling real-time monitoring of PFAS treatment systems. Earlier, in January 2024, DuPont introduced a new membrane technology for PFAS removal, increasing durability and fouling resistance in complex water streams.

Key Trends Driving the PFAS Filtration Industry

Surge of Stringent National and Regional Regulations

The PFAS filtration market is being propelled by a wave of stringent regulatory mandates across the globe. In the United States, the Environmental Protection Agency (EPA) has finalized Maximum Contaminant Levels (MCLs) for six PFAS compounds, requiring public water systems to implement treatment solutions by 2029 if thresholds are exceeded. Additionally, designating PFOA and PFOS as hazardous substances under CERCLA (Superfund) empowers the EPA to enforce cleanups, pushing private entities to proactively adopt filtration solutions. These regulations create an urgent demand for high-performance PFAS filtration systems and position regulatory compliance as a central driver for market growth.

Growing Public and Private Investment in PFAS Remediation

Substantial government funding and private investments are catalyzing the adoption of PFAS treatment technologies. The U.S. Infrastructure Investment and Jobs Act dedicates $50 billion to water infrastructure, with $5 billion targeting Emerging Contaminants in Small or Disadvantaged Communities (EC-SDC), directly supporting PFAS mitigation. Companies like Veolia Water Technologies have deployed systems treating over 2.1 billion gallons of water, delivering safe, PFAS-compliant water to more than 140,000 Americans. This infusion of funding accelerates both deployment and innovation in filtration technologies, creating a dynamic market environment for service providers and technology developers.

Technological Advancements in Filtration and PFAS Destruction

Technological innovation is transforming PFAS treatment beyond traditional separation methods. While Granular Activated Carbon (GAC) and Ion Exchange (IX) resins remain widely used, new methods such as Advanced Oxidation Processes (AOPs), heat-activated persulfate treatment, and electrochemical destruction are emerging to destroy PFAS molecules rather than merely concentrate them. Academic research and industry pilots highlight that these destructive technologies offer a long-term solution to the persistent challenge of PFAS-laden waste, making R&D in destructive filtration technologies a key growth area for the industry.

Emerging Opportunities in PFAS Filtration Market

Opportunities abound in scalable, cost-effective, and destructive PFAS treatment technologies. The market is expanding for ion exchange resins capable of handling short-chain PFAS, for membrane technologies that provide near-complete removal, and for emerging destructive solutions that solve the legacy waste problem. Additionally, the surge in municipal and industrial water treatment projects, driven by regulatory compliance and public health concerns, opens avenues for service providers to implement turnkey PFAS filtration systems. Companies that can combine media innovation, advanced monitoring, and destructive treatment are uniquely positioned to capture market share in both public water utilities and high-value industrial applications.

Market Share Insights of PFAS Filtration Market

Market Share by Technology: GAC Leads, Destructive Solutions Gain Momentum

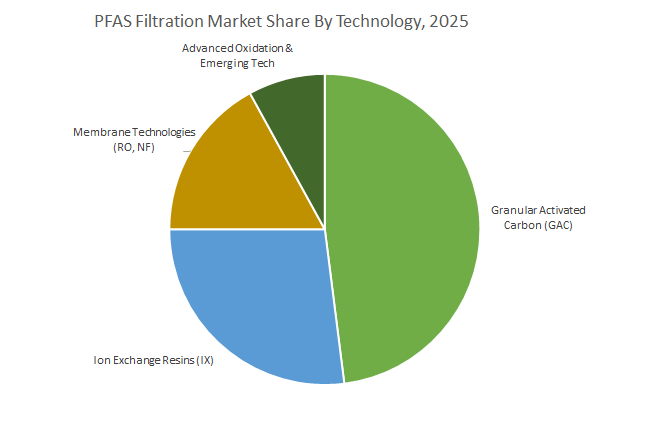

Granular Activated Carbon (GAC, 48.5%) dominates the market due to its cost-effectiveness, wide adoption, and proven performance for municipal water treatment. Ion Exchange resins (IX, 26.9%) are the fastest-growing technology, particularly effective for short-chain PFAS compounds like GenX, offering higher loading capacity and extended bed life. Membrane technologies (RO/NF, 16.9%) are highly effective at achieving non-detect PFAS levels but produce concentrated waste streams. Advanced Oxidation & emerging technologies, including AOPs and electrochemical destruction, represent a high-value, future-focused segment aimed at permanently destroying PFAS and addressing the challenge of contaminated media disposal.

Market Share by Media Type: Carbon-Based Media Retains Dominance, Resins Gain Traction

Carbon-based media (54.2%), primarily GAC, remains the incumbent due to its established supply chain, high adsorption capacity, and familiarity among water treatment engineers. Resin-based media (44.1%) is increasingly favored for its longer lifespan, higher removal efficiency, and ability to handle diverse PFAS compounds, making it particularly attractive for industrial and municipal remediation. Emerging media, such as Molecularly Imprinted Polymers (MIPs) and modified clays, are still niche but represent high-potential innovation opportunities for specialty applications.

Market Share by Application: Drinking Water Leads, Remediation Expands Rapidly

Drinking water treatment (44.1%) dominates, driven by legally enforceable MCLs and the urgent need for municipal compliance. Wastewater and groundwater remediation (32.8%) are high-value segments fueled by corporate liability, Superfund actions, and legacy contamination sites, creating long-term demand for advanced PFAS solutions. Industrial process wastewater (16.9%) represents a growing segment as regulators focus on source control, requiring industries to treat PFAS at the point of discharge. Soil remediation often involves washing contaminated soil and subsequently treating the wash water, creating integrated opportunities for filtration and treatment providers.

United States: Federal Regulations and Infrastructure Investments Accelerating PFAS Filtration Market Growth

The United States PFAS filtration market is witnessing rapid growth, driven primarily by regulatory enforcement and infrastructure investment. In April 2024, the EPA finalized the first-ever national drinking water standards for six PFAS compounds, setting a strict Maximum Contaminant Level (MCL) of 4.0 ppt for PFOA and PFOS. These rules are reshaping municipal and industrial adoption of advanced PFAS removal technologies.

The Biden-Harris Administration’s $2 billion allocation under the Bipartisan Infrastructure Law (BIL) supports small, rural, and disadvantaged communities in addressing PFAS contamination through source water treatment and infrastructure upgrades. Corporate innovation is also reshaping the market: in April 2025, Hawkins acquired WaterSurplus, enhancing its PFAS filtration equipment portfolio, while Georgia Tech researchers unveiled an AI-driven model that can identify new membrane materials capable of blocking over 95% of PFAS in days.

As utilities, industries, and municipalities race to meet federal standards, the U.S. PFAS filtration market outlook is being defined by regulatory compliance, infrastructure funding, and next-generation technologies targeting "forever chemicals."

China: National Action Plan and Emerging PFAS Removal Technologies Driving Market Expansion

The China PFAS filtration market is driven by both policy intervention and technological development. Following widespread contamination, the government launched the “Action Plan on Controlling New Pollutants” in 2022, setting reference limits for PFOA and PFOS in drinking water and restricting PFAS production. These measures have accelerated investments in PFAS removal technologies across industrial regions, particularly in the highly developed eastern provinces.

Technological advancements are strengthening China’s position in the Asia Pacific PFAS filtration market. In early 2025, Asian researchers, including teams in China, collaborated on carbon-based filtration materials designed for PFAS remediation. China is also prioritizing circular economy solutions, such as water reuse and resource recovery, integrating them into its PFAS treatment strategy.

The country’s market expansion is supported by stringent standards for drinking water safety, industrial wastewater treatment, and remediation projects, positioning China as a key driver of Asia Pacific PFAS market growth.

Canada: New National Standards and Toxic Substance Classification Driving PFAS Filtration Adoption

The Canada PFAS filtration market is accelerating under strong regulatory and governmental initiatives. In August 2024, Health Canada introduced a combined concentration limit of 30 ng/L for 25 PFAS compounds, one of the strictest standards globally, even exceeding EU benchmarks. This regulatory framework has fueled demand for advanced filtration systems across municipalities and industries.

In 2025, Canada further escalated its stance by classifying all non-polymeric PFAS as toxic substances under national law. This designation grants federal authorities broad control over PFAS management across the lifecycle, including discharge limits and mandatory wastewater monitoring.

Key applications include remediation at military bases and airports, where PFAS-containing firefighting foams were historically used, and ensuring compliance at federal sites. With strong policies and growing investment, Canada is emerging as a leader in North American PFAS remediation and drinking water protection.

Germany: EU Directives and Innovation in Advanced Water Treatment Technologies Boosting PFAS Filtration Market

The Germany PFAS filtration market is shaped by strict EU-wide regulatory frameworks and strong domestic innovation. In January 2025, the revised EU Urban Wastewater Treatment Directive came into force, mandating enhanced monitoring and treatment of pollutants, including PFAS. This regulation is pushing utilities and industries to adopt advanced PFAS filtration systems.

Germany’s leadership in water treatment technology development further supports its market strength. Research institutions and private companies are pioneering advanced filtration solutions for micropollutant and PFAS removal, ensuring compliance while addressing strong public demand for safe drinking water.

The combination of stringent EU directives and Germany’s role as a hub for PFAS removal technology innovations positions the country as a critical player in the European PFAS filtration market.

Australia: Government Research Funding and On-Site Remediation Innovations Driving PFAS Filtration Market

The Australia PFAS filtration market is expanding due to federal funding initiatives and novel remediation technologies. In December 2024, the Australian government allocated $8.2 million to nine research projects targeting PFAS remediation, including new water treatment and soil cleanup methods.

A notable technological advancement came from South Australia, where the SourceZone system demonstrated up to 99% PFAS mass removal from soil during a large-scale trial. This approach highlights Australia’s focus on sustainable, site-specific PFAS remediation technologies that minimize environmental risks.

The market’s growth is primarily driven by the need to remediate military bases, fire training facilities, and historically contaminated sites, combined with the country’s push for sustainable water management in a water-scarce environment.

Japan: Strict PFAS Ban and Cutting-Edge Membrane Technologies Reshaping Market Outlook

The Japan PFAS filtration market is undergoing rapid transformation following strong regulatory actions and technology breakthroughs. In January 2025, Japan enforced a ministerial ordinance under the Chemical Substances Control Law (CSCL), banning the manufacture, import, and use of 138 PFAS compounds, including restrictions on finished goods and components. This sweeping ban is pushing industries toward PFAS-free alternatives and advanced filtration solutions.

At the same time, Japanese researchers are pioneering PFAS removal innovations. The Institute of Science Tokyo developed a novel membrane distillation system and carbon-based adsorbents capable of removing PFAS from water without relying on conventional heaters. These electricity-free systems mark a major step toward sustainable and scalable PFAS treatment technologies.

Japan’s dual focus on regulatory compliance and technological innovation ensures its pivotal role in the Asia Pacific PFAS filtration market, particularly in driving next-generation remediation systems.

Competitive Landscape of PFAS Filtration Market

The PFAS filtration market is highly competitive, with leading companies combining technological innovation, integrated solutions, and global reach to address emerging contaminants and regulatory demands. Market players differentiate themselves through mobile treatment solutions, advanced filtration technologies, and strong project execution capabilities.

Veolia Water Technologies leads with integrated PFAS treatment solutions

Veolia offers a comprehensive portfolio of PFAS remediation technologies, including carbon adsorption, specialty ion exchange, and Drop® destruction technology (June 2025). Its mobile water fleet provides on-demand solutions for PFAS emergencies and pilot projects. Through the Hubgrade AI platform, Veolia optimizes system performance, while its presence in 52 countries solidifies its market leadership.

Xylem Inc. excels in smart water solutions for PFAS removal

Xylem combines GAC and single-pass ion exchange resin technology with its Xylem Vue platform for real-time process optimization. Strategic acquisitions, such as Evoqua Water Technologies in 2023, expanded its integrated water lifecycle solutions. With operations in over 150 countries, Xylem ensures global reach and reliable PFAS treatment services.

DuPont de Nemours, Inc. focuses on membrane-based PFAS filtration

DuPont leverages expertise in chemical and material science to develop durable reverse osmosis (RO) and nanofiltration (NF) membranes for complex PFAS-contaminated water. Recent innovations enhance fouling resistance and performance under harsh conditions. DuPont strategically targets water reuse and compliance with stringent regulations.

AECOM provides proprietary electrochemical PFAS destruction

AECOM offers the DE-FLUORO™ technology for advanced PFAS destruction, with extensive project experience across 1,200 PFAS initiatives in 600 locations. Its June 2025 partnership with Aquatech accelerates scalable deployment, reflecting AECOM’s leadership in environmental engineering and project delivery.

Calgon Carbon Corporation specializes in granular activated carbon solutions

Calgon Carbon, a Kuraray subsidiary, delivers FILTERSORB® GAC technology for effective PFAS removal. Its solutions include customized equipment, on-site support, and carbon reactivation, emphasizing performance and service. Recent reports (2024) highlight high-efficiency GAC products tailored for industrial and municipal applications.

Evoqua Water Technologies (Xylem brand) offers flexible PFAS treatment services

Evoqua, under Xylem, provides mobile water systems, GAC, and ion exchange solutions. Its service-based model emphasizes flexibility and immediate response for PFAS contamination. The company’s entrepreneurial culture enables rapid deployment of emergency and mobile treatment assets, supporting industrial and municipal clients.

PFAS Filtration Market Report Scope

PFAS Filtration Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.4 Billion

|

|

Market Size (2034)

|

$4.5 Billion

|

|

Market Growth Rate

|

7.2%

|

|

Segments

|

By Technology (Granular Activated Carbon (GAC), Anion‐Exchange Resins, Membrane Technologies, Advanced Oxidation Processes (AOPs) and Electrochemical Processes), By Media Type (Carbon-based Media, Resin-based Media), By Application (Drinking Water Treatment, Wastewater & Groundwater Remediation, Industrial Process & Wastewater, Soil Remediation), By Service Type (Installation Services, Maintenance & Monitoring Services, Consulting Services), By End-User (Municipalities & Government Agencies, Industrial Facilities, Commercial & Residential, Environmental Remediation Contractors)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia, Xylem Inc., Evoqua Water Technologies, DuPont de Nemours, Inc., SUEZ, Siemens, Kurita Water Industries Ltd., Aquatech International, Badger Meter, Calgon Carbon Corporation (A Subsidiary of Kuraray Co., Ltd.), Solvay S.A., LANXESS, Cummins Inc., Trojan Technologies (A Danaher Company), Aclarity LLC

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

PFAS Filtration Market Segmentation

By Technology

- Granular Activated Carbon (GAC)

- Anion‐Exchange Resins

- Membrane Technologies

- Advanced Oxidation Processes (AOPs) and Electrochemical Processes

By Media Type

- Carbon-based Media

- Resin-based Media

By Application

- Drinking Water Treatment

- Wastewater & Groundwater Remediation

- Industrial Process & Wastewater

- Landfill Leachate

- Firefighting Training Grounds

- Chemical Manufacturing

- Metal Plating

- Soil Remediation

By Service Type

- Installation Services

- Maintenance & Monitoring Services

- Consulting Services

By End-User

- Municipalities & Government Agencies

- Industrial Facilities

- Commercial & Residential

- Environmental Remediation Contractors

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the PFAS Filtration Industry include-

- Veolia

- Xylem Inc.

- Evoqua Water Technologies

- DuPont de Nemours, Inc.

- SUEZ

- Siemens

- Kurita Water Industries Ltd.

- Aquatech International

- Badger Meter

- Calgon Carbon Corporation (A Subsidiary of Kuraray Co., Ltd.)

- Solvay S.A.

- LANXESS

- Cummins Inc.

- Trojan Technologies (A Danaher Company)

- Aclarity LLC

*- List not Exhaustive

Research Coverage

The PFAS Filtration Market Report by USDAnalytics this report investigates the accelerating shift from simple adsorption to integrated, data-driven treatment trains; it highlights breakthroughs in short-chain capture media, electrochemical destruction, AOP hybrids, and cloud-enabled performance monitoring; delivers analysis reviews on lifecycle costs, waste minimization, and compliance pathways under evolving MCLs and CERCLA liabilities; and benchmarks municipal and industrial use cases across drinking water, remediation, and process discharge. By linking technology selection to removal efficiency, OPEX, brine/disposal strategy, and digital oversight, this report is an essential resource for utility leaders, EHS directors, asset owners, and engineering firms planning scalable PFAS removal and destruction programs. Scope Includes-

- Segmentation: By technology (GAC; anion-exchange resins; membranes; AOPs/electrochemical), media type (carbon-based; resin-based), application (drinking water; wastewater & groundwater remediation; industrial process & wastewater landfill leachate, fire-training grounds, chemical manufacturing, metal plating; soil remediation), service type (installation; maintenance & monitoring; consulting), and end-user (municipalities & government; industrial; commercial & residential; remediation contractors).

- Geographic Scope: “Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.”

- Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies (Profiles of 15+ companies): Veolia; Xylem Inc.; Evoqua Water Technologies; DuPont de Nemours, Inc.; SUEZ; Siemens; Kurita Water Industries Ltd.; Aquatech International; Badger Meter; Calgon Carbon Corporation (Kuraray); Solvay S.A.; LANXESS; Cummins Inc.; Trojan Technologies (Danaher); Aclarity LLC.

Methodology

USDAnalytics combines primary interviews with utility executives, plant managers, OEMs, and remediation EPCs with secondary validation from federal/state rulemaking dockets, bid/tender documents, pilot reports, and peer-reviewed studies. We build bottom-up market models from installed/awarded projects, media change-out intervals, and normalized loading rates (bed volumes, breakthrough curves) and reconcile with top-down spend by end-user and region. Tech scoring weights removal of long- and short-chain PFAS, EBCT, resin/gac life, waste minimization, and destructive efficacy; TCO models include media/reactivation, brine handling, power, labor, and monitoring. Forecasts (2025–2034) reflect regulatory timelines, funding flows (e.g., emerging-contaminant grants), supply-chain capacity, and adoption of digital O&M.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: PFAS Filtration Market

1. Executive Summary

1.1. Market Highlights & Key Projections

1.2. Global Market Snapshot

1.3. Key Findings

2. PFAS Filtration Market Overview (2025–2034)

2.1. Introduction

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $2.4 Billion

2.2.2. Forecasted Market Size (2034): $4.5 Billion

2.2.3. Projected Compound Annual Growth Rate (CAGR): 7.2%

2.3. Market Drivers and Challenges

2.3.1. Drivers: Regulatory Mandates, Public Health Concerns, and Cross-Industry Contamination

2.3.2. Challenges: High Capital Costs and Waste Disposal Issues

2.4. Key Insights for Industry Stakeholders

3. Key Market Trends and Recent Developments

3.1. Surge of Stringent National and Regional Regulations

3.2. Growing Public and Private Investment in PFAS Remediation

3.3. Technological Advancements in Filtration and PFAS Destruction

3.4. Recent Developments & Strategic Moves (2024–2025)

3.4.1. Strategic Acquisitions and Partnerships

3.4.2. Technology and Product Launches

4. PFAS Filtration Market – Segmentation Insights

4.1. By Technology

4.1.1. Granular Activated Carbon (GAC) (48.5% Market Share)

4.1.2. Anion‐Exchange Resins (26.9% Market Share)

4.1.3. Membrane Technologies (RO/NF) (16.9% Market Share)

4.1.4. Advanced Oxidation Processes (AOPs) & Electrochemical Processes

4.2. By Media Type

4.2.1. Carbon-based Media (54.2% Market Share)

4.2.2. Resin-based Media (44.1% Market Share)

4.3. By Application

4.3.1. Drinking Water Treatment (44.1% Market Share)

4.3.2. Wastewater & Groundwater Remediation (32.8% Market Share)

4.3.3. Industrial Process & Wastewater (16.9% Market Share)

4.3.4. Soil Remediation

4.4. By Service Type

4.4.1. Installation Services

4.4.2. Maintenance & Monitoring Services

4.4.3. Consulting Services

4.5. By End-User

4.5.1. Municipalities & Government Agencies

4.5.2. Industrial Facilities

4.5.3. Commercial & Residential

4.5.4. Environmental Remediation Contractors

5. Country Analysis and Outlook: PFAS Filtration Market

5.1. United States: Federal Regulations and Infrastructure Investments

5.2. China: National Action Plan and Emerging Technologies

5.3. Canada: New National Standards and Toxic Substance Classification

5.4. Germany: EU Directives and Innovation in Advanced Water Treatment

5.5. Australia: Government Research Funding and Remediation Innovations

5.6. Japan: Strict PFAS Ban and Cutting-Edge Membrane Technologies

6. PFAS Filtration Market Size Outlook by Region (2025–2034)

6.1. North America PFAS Filtration Market Size Outlook to 2034

6.1.1. By Technology

6.1.2. By Application

6.1.3. By Country (US, Canada, Mexico)

6.2. Europe PFAS Filtration Market Size Outlook to 2034

6.2.1. By Technology

6.2.2. By Application

6.2.3. By Country (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

6.3. Asia Pacific PFAS Filtration Market Size Outlook to 2034

6.3.1. By Technology

6.3.2. By Application

6.3.3. By Country (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

6.4. South America PFAS Filtration Market Size Outlook to 2034

6.4.1. By Technology

6.4.2. By Application

6.4.3. By Country (Brazil, Argentina, Rest of South America)

6.5. Middle East and Africa PFAS Filtration Market Size Outlook to 2034

6.5.1. By Technology

6.5.2. By Application

6.5.3. By Country (Saudi Arabia, UAE, South Africa, Egypt, Rest of MEA)

7. Competitive Landscape: Key Companies

7.1. Veolia Water Technologies

7.1.1. Company Overview

7.1.2. Integrated PFAS Treatment Solutions

7.2. Xylem Inc.

7.2.1. Company Overview

7.2.2. Smart Water Solutions for PFAS Removal

7.3. DuPont de Nemours, Inc.

7.4. AECOM

7.5. Calgon Carbon Corporation

7.6. Evoqua Water Technologies

7.7. Other Prominent Companies

7.7.1. SUEZ

7.7.2. Siemens

7.7.3. Kurita Water Industries Ltd.

8. Methodology

8.1. Research Scope

8.2. Market Research Approach

8.3. Data Sources and Validation

8.4. Assumptions and Limitations

9. Appendix

9.1. Acronyms and Abbreviations

9.2. List of Tables

9.3. List of Figures