Stormwater Treatment Systems Market Overview: Growth Outlook to 2034

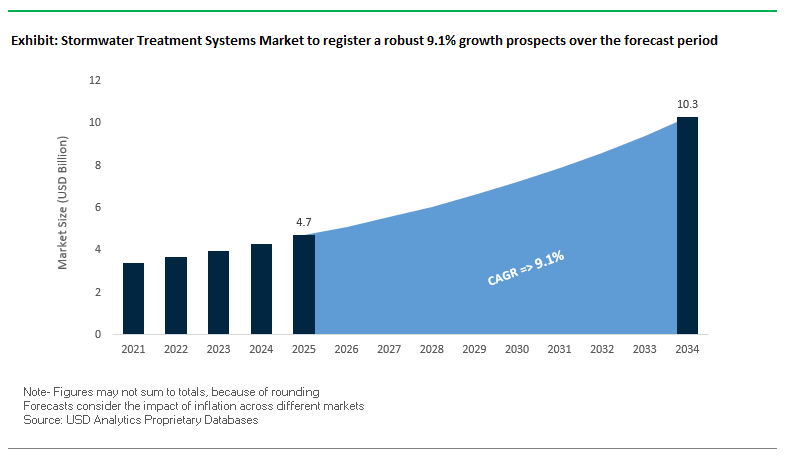

The global stormwater treatment systems market is projected to reach $10.3 billion by 2034, up from $4.7 billion in 2025, advancing at a robust CAGR of 9.1%. This strong growth trajectory underscores the increasing demand for advanced urban drainage solutions driven by rapid urbanization, stricter environmental regulations, and climate resilience strategies. Rising impermeable surfaces in urban areas have amplified polluted runoff volumes, triggering flash floods and severe water quality degradation. Municipalities, industrial sectors, and developers are under mounting regulatory and public pressure to deploy sustainable stormwater treatment technologies.

Key Insights for Industry Leaders

- Over the past decade, urban flooding incidents have surged by more than 30%, particularly in North America and Asia, driving adoption of engineered drainage systems.

- According to the World Resources Institute, impermeable urban surfaces increase runoff volumes by up to 300% compared to undeveloped land, intensifying pressure on cities to invest in stormwater management.

- Regulatory enforcement is a major growth driver: the U.S. Clean Water Act and the EU Water Framework Directive mandate compliance, with penalties up to $50,000 per violation for non-compliant municipalities.

- Green infrastructure solutions, such as permeable pavements and bioretention systems, are increasingly being mandated in new developments, reshaping urban planning practices.

Market Analysis: Recent News, Partnerships, and Strategic Developments

The stormwater treatment systems industry is undergoing rapid transformation fueled by mergers, acquisitions, and sustainability-driven innovation. Companies are not only expanding product portfolios but also forming partnerships with governments, academic institutions, and industrial players to accelerate technology adoption.

In August 2025, DuPont Water Solutions was recognized in the BIG Sustainability Awards for its advancements in industrial wastewater reuse an acknowledgment of how stormwater treatment is aligning with broader water circularity initiatives. A month earlier, in July 2025, StormTrap acquired Faircloth Skimmer, strengthening its footprint in surface drain dewatering solutions. That same month, Veolia Water Technologies was chosen to equip France’s largest treated wastewater reuse project in Argelès-sur-Mer, reinforcing its leadership in sustainable water reclamation. Meanwhile, H2O America announced a $540 million acquisition of Quadvest, including a $500 million modernization plan, highlighting growing investment flows into water infrastructure.

Another significant move came in June 2025, when Grundfos acquired Newterra, expanding its decentralized water treatment solutions in the U.S. Earlier in the year, in February 2025, StormTrap partnered with Northwestern University to advance stormwater research, underscoring the increasing role of academic-industry collaborations. The ASCE’s 2025 Infrastructure Report Card (January 2025) assigned U.S. wastewater systems a D+ rating, underlining the urgent need for stormwater upgrades nationwide. Looking back, in October 2024, StormTrap’s Sequesterer Row System earned regulatory approval from the Wisconsin Department of Natural Resources, opening new opportunities in the U.S. Midwest market.

Key Market Trends Shaping Stormwater Treatment

Policy and Financial Support for Green and Hybrid Infrastructure

Government initiatives are a major driver for stormwater treatment adoption. The U.S. EPA actively promotes green infrastructure (GI) under the NPDES program, with pilot facilities like Boston’s integrating green roofs and permeable pavements to capture and treat runoff. Similarly, the European Union’s revised Urban Wastewater Treatment Directive (effective 2025) mandates integrated management plans to minimize urban flooding and pollution. Funding programs such as the U.S. Infrastructure Investment and Jobs Act have allocated $11.7 billion for Clean Water State Revolving Funds (CWSRF), nearly $2.2 billion of which has already supported over 1,100 stormwater projects, enabling municipalities and private developers to implement advanced treatment and green infrastructure projects.

Shift Towards Advanced and Novel Filtration Media

The stormwater treatment market is moving toward innovative filtration solutions. Multi-stage treatment using tailored filter media achieves up to 95% heavy metal removal, as demonstrated in a 2024 MDPI study. Sustainable alternatives, such as recycled asphalt and crushed brick in bioretention systems, meet stringent environmental standards while reducing costs, as highlighted in a 2025 ResearchGate publication. These developments underscore a growing preference for material innovation and sustainability in stormwater management.

Integration of Digitalization and Real-Time Monitoring

Smart stormwater treatment systems leveraging IoT and AI are increasingly adopted to optimize system performance and regulatory compliance. Real-time monitoring of water quality, flow, and system efficiency enables predictive maintenance and continuous operational assurance. New York City’s green infrastructure program exemplifies this trend: bioswales, rain gardens, and permeable surfaces are integrated with performance monitoring to retain 78% of inflows in pilot installations, significantly reducing combined sewer overflows (CSOs).

Stormwater Treatment Systems Market Share Insights

Market Share by Technology: Traditional BMPs Lead, Green Infrastructure Accelerates

Structural Best Management Practices (BMPs) (44.1%) dominate due to proven engineering reliability, predictable pollutant removal, and high capacity. Non-Structural & Green Infrastructure (GI) (32.8%) is the fastest-growing segment, including bioretention cells, green roofs, and permeable pavements, driven by municipal mandates and sustainability goals. Infiltration & Harvesting Systems (24.6%) facilitate stormwater capture and reuse, addressing water scarcity and regulatory requirements for volume reduction. Hybrid “treatment train” approaches combining GI and BMPs are increasingly recognized as best practice, enhancing system efficiency and market demand across technologies.

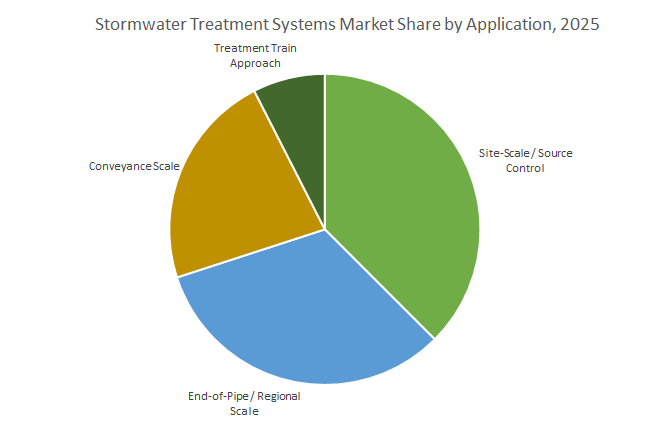

Market Share by Application (System Scale): Site-Level Control is Preferred

Site-Scale / Source Control (38%) remains the foundational approach, treating runoff at its origin to reduce pollutant loads and comply with local ordinances. End-of-Pipe / Regional Scale (32.8%) addresses large watersheds through centralized facilities such as detention ponds and treatment wetlands, often mandated by federal or state permits. Conveyance Scale (24.6%) focuses on retrofitting drainage networks using in-line filters and hydrodynamic separators in space-constrained urban areas. The Treatment Train Approach integrates multiple scales and technologies, representing the most comprehensive, high-performance solution that influences market adoption trends across all other scales.

Market Share by Pollutant Removal Focus: Sediment and Nutrient Control Dominate

Sediment & Particle Control (32.8%) is the primary target due to sediment’s role as a carrier for metals and nutrients, making it foundational for pollutant removal. Nutrient Management (Nitrogen & Phosphorus) (26.9%) is driven by regulatory priorities to prevent eutrophication in sensitive water bodies, fostering demand for advanced filter media. Hydrocarbon & Metal Removal (24.6%) is crucial for industrial and roadway runoff, while Volume & Flow Control (16.9%) addresses urban flooding and hydrology restoration. Pathogen Removal remains niche, relevant primarily for recreational waters or shellfish protection. This segmentation highlights the market’s dual focus on water quality and urban flood management.

United States: Federal Funding and Decentralized Stormwater Management Driving Market Growth

The United States stormwater treatment systems market is being propelled by substantial government funding, regulatory policies, and corporate innovations. Under the Bipartisan Infrastructure Law (BIL), over $50 billion has been allocated to the U.S. Environmental Protection Agency (EPA) to modernize water infrastructure, including stormwater systems. The Sewer Overflow and Stormwater Reuse Municipal Grants (OSG) program, with an appropriation of $280 million, alongside five Centers of Excellence for Stormwater Control Infrastructure Technologies (CESCITs), underscores the emphasis on research and development of advanced stormwater management solutions. Regulatory focus on PFAS Maximum Contaminant Levels and promotion of green infrastructure, such as permeable pavements, green roofs, and bioretention areas, further drive technology adoption. Corporate initiatives include modular and decentralized stormwater treatment systems and water recovery projects by major beverage manufacturers, aimed at achieving net-zero emissions while improving water reuse. Key applications focus on sustainable urban resilience, flood reduction, and enhanced water quality in metropolitan environments.

China: Sponge City Program and PPP Investments Transform Urban Stormwater Management

China’s stormwater treatment systems market is strongly influenced by government-led initiatives and investments in innovative infrastructure. The "Sponge City" program, launched in 2014, targets over 80% of urban areas meeting stormwater management standards by 2030, promoting significant investment in engineered and natural stormwater management systems. Public-Private Partnerships (PPP) play a pivotal role, with private investors contributing around 50% of project funding in cities like Wuhan. Technological advancements in green-grey drainage infrastructure mimic natural hydrologic processes, supporting infiltration and bioretention to control runoff. These initiatives are driving the adoption of integrated stormwater solutions in rapidly urbanizing regions, addressing urban flooding, improving water quality, and promoting sustainable rainwater management.

Germany: Nature-Based Solutions and Advanced Digital Monitoring Enhancing Urban Resilience

Germany’s market is shaped by EU regulatory frameworks, technological innovation, and government support for sustainable water management. The revised Urban Wastewater Treatment Directive (January 2025) mandates the "4th purification stage," incentivizing advanced oxidation processes and membrane filtration techniques in stormwater treatment. The Ecologic Institute’s 2024 workshop highlighted the integration of nature-based solutions in urban stormwater management. German cities are adopting advanced digital twins, AI-driven monitoring, and real-time water management systems to mitigate urban flooding and enhance resilience against climate change. Key applications include decentralized rainwater harvesting, pollutant removal, and urban water reuse, positioning Germany as a leader in integrated and sustainable stormwater solutions.

Australia: Long-Term Water Stewardship and Infrastructure Investments Driving Stormwater Solutions

Australia’s stormwater treatment systems market benefits from strict environmental regulations, major infrastructure investments, and corporate participation. State environment protection policies, such as SEPP Waters of Victoria, guide sustainable water management to preserve beneficial uses. Sydney Water’s planned $34 billion investment over the next decade, including the Mamre Road Precinct Stormwater project, demonstrates the focus on renewing infrastructure and implementing modern treatment solutions. Corporate initiatives from Melbourne Water emphasize continuous water delivery upgrades and sustainable urban stormwater management. The market’s key applications focus on managing runoff from mining and urban areas, preventing flooding, and supporting long-term environmental stewardship.

India: Regulatory Mandates and Smart Technologies Accelerating Stormwater Management

India’s stormwater treatment systems market is driven by regulatory frameworks, government initiatives, and technological adoption. The Central Pollution Control Board (CPCB) and National Green Tribunal (NGT) mandate Zero Liquid Discharge (ZLD) for industries in water-scarce regions, indirectly influencing urban stormwater management. Infrastructure upgrades by the Public Works Department (PWD) in Delhi, including automated stormwater systems at Pragati Maidan, Minto Bridge, Azad Bhawan, and ITO, exemplify the modernization efforts. Government missions such as "Jal Jeevan" and "Namami Gange" encourage widespread adoption of water treatment infrastructure. Advanced hydraulic analysis, design, and stormwater modeling software like StormCAD are driving the deployment of efficient and effective stormwater treatment solutions. The key market focus is on mitigating urban flooding, ensuring water reuse, and addressing challenges from rapid urbanization and climate change.

Singapore: Flood Resilience and Smart Infrastructure Investments Promoting Market Expansion

Singapore’s stormwater treatment systems market is shaped by proactive government initiatives, regulatory reforms, and adoption of advanced technologies. With a budget of S$150 million in the 2025 financial year, the government is strengthening flood resilience through drainage upgrading projects, with 19 ongoing and six new projects slated to commence in 2025. Regulatory amendments to the Sewerage and Drainage Act ensure proper operation and maintenance of flood protection measures by property owners and developers. The Singapore International Water Week (SIWW) Spotlight 2025 is fostering knowledge exchange on flood resilience strategies, integrating innovative solutions, policy interventions, and community engagement. Key applications include managing unpredictable rainfall, optimizing limited land use for drainage, and promoting sustainable urban stormwater management in a highly urbanized city-state.

Competitive Landscape: Leading Stormwater Treatment Companies

The competitive environment of the stormwater treatment systems market features a mix of multinational corporations, specialized technology providers, and niche innovators. Companies are differentiating themselves through portfolio breadth, R&D intensity, digital integration, and global expansion strategies. Below are detailed profiles of leading players shaping the industry.

Xylem Inc.: Driving IoT-Enabled Water Solutions

Xylem Inc. is a global leader in water technology, offering end-to-end solutions that cover the entire water cycle, including stormwater. Its 2023 acquisition of Evoqua created one of the world’s largest integrated water platforms, enhancing its stormwater management offerings. The company provides advanced oxidation processes, membrane bioreactors (MBR), high-capacity pumps, and mixers, essential for urban runoff management. With a strong digital strategy, Xylem invests heavily in IoT-enabled monitoring and predictive maintenance, helping municipalities and industrial customers reduce flood risks while improving system resilience.

DuPont Water Solutions: Membrane Innovations for Water Circularity

DuPont Water Solutions leverages its materials science expertise to deliver high-performance membranes for advanced water purification. Its FilmTec™ Fortilife™ XC160 Membrane, awarded in 2025, enables efficient concentration of wastewater streams, making water reuse more sustainable. The company’s FilmTec™ RO, NF membranes, and IntegraTec™ UF systems are widely deployed in stormwater treatment and reclamation. Operating across 112 countries, DuPont supports the purification of more than 50 million gallons of water per minute, positioning itself as a global enabler of water circularity and reduced carbon footprints.

Veolia Water Technologies: Ecological Transformation in Stormwater

Veolia’s leadership stems from its integrated portfolio, spanning biological and membrane systems to thermal evaporators and ZLD solutions. In May 2025, the company took full ownership of its Water Technologies & Solutions unit, accelerating its push toward sustainable stormwater infrastructure. Its offerings extend from design and construction to long-term O&M contracts, making Veolia a preferred partner for complex industrial and municipal projects. Through its GreenUp strategic plan, Veolia is channeling innovation to fight climate change, supporting cities with sustainable drainage and water reuse systems.

SUEZ – Water Technologies & Solutions: Custom Industrial Stormwater Systems

SUEZ specializes in customized, high-performance stormwater treatment solutions, particularly for industrial environments with challenging wastewater profiles. Its recent project wins in Asia, including a wastewater plant in China achieving 100% recycling, underscore its expertise in ZLD systems. Its portfolio integrates biological processes, membrane systems, and predictive analytics that help customers optimize performance, minimize fouling, and reduce operational costs. SUEZ’s digital platforms reinforce its ability to deliver data-driven efficiency gains across large-scale stormwater projects.

CONTECH Engineered Solutions: Infrastructure-Centric Stormwater Management

CONTECH focuses on civil engineering infrastructure solutions, offering a comprehensive portfolio of hydrodynamic separators, detention systems, and filtration technologies. In a recent innovation, the company launched the Contech Design Center, a digital engineering platform that accelerates the design of stormwater projects with automated CAD drawings and calculations. Its solutions are widely used in urban and commercial developments, where regulatory compliance is critical. By providing durable, cost-effective, and regulation-ready systems, CONTECH plays a vital role in modern stormwater planning.

Hydro International: Proprietary Technologies for Sustainable Drainage

Hydro International delivers specialized products and engineering services for stormwater and wastewater management. Its proprietary technologies, such as Hydro-Brake® flow controls and Hydro-Flo® filtration systems, are widely adopted for controlling runoff and capturing pollutants. Recently integrated into Oldcastle Infrastructure, Hydro International now benefits from broader distribution and project synergies. With a strong focus on SuDS (Sustainable Drainage Systems) and Low Impact Development (LID), the company is advancing urban resilience by embedding green infrastructure principles into stormwater management strategies.

Stormwater Treatment Systems Market Report Scope

Stormwater Treatment Systems Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.7 Billion

|

|

Market Size (2034)

|

$10.3 Billion

|

|

Market Growth Rate

|

9.1%

|

|

Segments

|

By Technology (Structural Best Management Practices, Non-Structural & Green Infrastructure, Infiltration & Harvesting Systems), By Application (Treatment Train Approach, Site-Scale / Source Control, Conveyance Scale, End-of-Pipe / Regional Scale), By Pollutant Removal (Sediment & Particle Control, Nutrient Management, Hydrocarbon & Metal Removal, Volume & Flow Control, Pathogen Removal), By End-User (Municipalities & Public Works, Commercial & Industrial, Transportation, Residential)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia, SUEZ, Xylem Inc., Evoqua Water Technologies, DuPont de Nemours, Inc., Pentair plc, Toray Industries, Inc., Aquatech International, Kubota Corporation, The Dow Chemical Company, V.A. TECH WABAG Ltd., Mitsubishi Chemical Corporation, Kurita Water Industries Ltd., H2O GmbH, Thermax Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Stormwater Treatment Systems Market Segmentation

By Technology

- Structural Best Management Practices

- Non-Structural & Green Infrastructure

- Infiltration & Harvesting Systems

By Application

- Treatment Train Approach

- Site-Scale / Source Control

- Conveyance Scale

- End-of-Pipe / Regional Scale

By Pollutant Removal

- Sediment & Particle Control

- Nutrient Management

- Hydrocarbon & Metal Removal

- Volume & Flow Control

- Pathogen Removal

By End-User

- Municipalities & Public Works

- Commercial & Industrial

- Transportation

- Residential

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Stormwater Treatment Systems Industry include-

- Veolia

- SUEZ

- Xylem Inc.

- Evoqua Water Technologies

- DuPont de Nemours, Inc.

- Pentair plc

- Toray Industries, Inc.

- Aquatech International

- Kubota Corporation

- The Dow Chemical Company

- V.A. TECH WABAG Ltd.

- Mitsubishi Chemical Corporation

- Kurita Water Industries Ltd.

- H2O GmbH

- Thermax Limited

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the global Stormwater Treatment Systems Market with a practical lens on regulation, design standards, controllable cost drivers, and ROI under climate-stressed hydrology. It highlights breakthroughs in hybrid “green–grey” treatment trains, novel filtration media, and IoT-enabled, real-time controls, and the analysis reviews procurement pipelines, policy catalysts (NPDES, WFD), and funding flows shaping adoption. Benchmarking removal efficiencies for sediments, nutrients, hydrocarbons, and metals alongside lifecycle OPEX, the study maps competitive moves, partnerships, and scaling strategies to 2034 this report is an essential resource for municipalities, transportation agencies, industrial owners, EPCs, and solution providers seeking code-compliant, flood-resilient designs with measurable outcomes. Scope Includes-

- Segmentation

- By Technology: Structural Best Management Practices; Non-Structural & Green Infrastructure; Infiltration & Harvesting Systems

- By Application: Treatment Train Approach; Site-Scale / Source Control; Conveyance Scale; End-of-Pipe / Regional Scale

- By Pollutant Removal: Sediment & Particle Control; Nutrient Management; Hydrocarbon & Metal Removal; Volume & Flow Control; Pathogen Removal

- By End-User: Municipalities & Public Works; Commercial & Industrial; Transportation; Residential

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Timeframe: Historic data 2021–2024; forecasts 2025–2034.

- Companies (15+ analysis/profiles): Veolia; SUEZ; Xylem Inc.; Evoqua Water Technologies; DuPont de Nemours, Inc.; Pentair plc; Toray Industries, Inc.; Aquatech International; Kubota Corporation; The Dow Chemical Company; V.A. TECH WABAG Ltd.; Mitsubishi Chemical Corporation; Kurita Water Industries Ltd.; H2O GmbH; Thermax Limited.

Methodology

USDAnalytics employed a triangulated approach: bottom-up sizing from city and project-level capex/opex datasets (detention, hydrodynamic separators, bioretention, permeable pavements, harvesting systems), validated with >80 stakeholder interviews (municipal engineers, DOTs, industrial EHS, OEMs, financiers). Performance and cost models normalize rainfall IDF curves, imperviousness, watershed load coefficients, and permit targets (TSS, TN/TP, hydrocarbons, metals) against control types and maintenance regimes. We integrated funding disbursement traces (SRF/PPP), tender pipelines, and retrofit density into scenario analyses for climate intensification, PFAS oversight, and GI mandates, producing defensible market shares, pricing bands, and five regional adoption trajectories to 2034.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Stormwater Treatment Systems Market

1. Executive Summary

1.1. Market Highlights and Key Projections

1.2. Key Insights for Industry Stakeholders

1.3. Global Market Snapshot

1.3.1. Current Market Valuation (2025): $4.7 Billion

1.3.2. Projected Market Valuation (2034): $10.3 Billion

1.3.3. Compound Annual Growth Rate (CAGR): 9.1%

2. Market Outlook (2025–2034)

2.1. Introduction: Growth, Drivers, and Key Challenges

2.2. Market Valuation and Growth Projections (2025–2034)

2.3. Key Market Trends Shaping Stormwater Treatment

2.3.1. Policy and Financial Support for Green and Hybrid Infrastructure

2.3.2. Shift Towards Advanced and Novel Filtration Media

2.3.3. Integration of Digitalization and Real-Time Monitoring

3. Innovations and Strategic Developments Redefining the Market

3.1. Market Analysis: Recent Developments and Strategic Shifts

3.1.1. DuPont Water Solutions Recognized for Wastewater Reuse Innovations (August 2025)

3.1.2. StormTrap and H2O America Announce Strategic Moves (July 2025)

3.1.3. Grundfos Acquires Newterra, Expanding Decentralized Solutions (June 2025)

3.1.4. StormTrap-Northwestern University Partnership (February 2025)

3.1.5. ASCE's 2025 Infrastructure Report Card Underlines Urgency (January 2025)

3.1.6. Badger Meter's Acquisition of SmartCover for IoT Monitoring (January 2025)

3.1.7. Recent Product Approvals and Technology Launches (2024-2025)

4. Competitive Landscape: Leading Players

4.1. Market Overview: Multinational Leaders and Innovative Specialists

4.2. Strategic Profiles of Key Companies

4.2.1. Xylem Inc.: Driving IoT-Enabled Water Solutions

4.2.2. DuPont Water Solutions: Membrane Innovations for Water Circularity

4.2.3. Veolia Water Technologies: Integrated Ecological Transformation

4.2.4. SUEZ – Water Technologies & Solutions: Custom Industrial Systems and Digital Integration

4.2.5. CONTECH Engineered Solutions: Infrastructure-Centric Solutions

4.2.6. Hydro International: Proprietary Technologies for Sustainable Drainage

5. Stormwater Treatment Systems Market Segmentation Insights

5.1. By Technology

5.1.1. Structural Best Management Practices (BMPs)

5.1.2. Non-Structural & Green Infrastructure (GI)

5.1.3. Infiltration & Harvesting Systems

5.2. By Application (System Scale)

5.2.1. Treatment Train Approach

5.2.2. Site-Scale / Source Control

5.2.3. Conveyance Scale

5.2.4. End-of-Pipe / Regional Scale

5.3. By Pollutant Removal

5.3.1. Sediment & Particle Control

5.3.2. Nutrient Management (Nitrogen & Phosphorus)

5.3.3. Hydrocarbon & Metal Removal

5.3.4. Volume & Flow Control

5.3.5. Pathogen Removal

5.4. By End-User

5.4.1. Municipalities & Public Works

5.4.2. Commercial & Industrial

5.4.3. Transportation

5.4.4. Residential

6. Country Analysis and Outlook

6.1. United States: Federal Funding and Decentralized Stormwater Management

6.2. China: Sponge City Program and PPP Investments

6.3. Germany: Nature-Based Solutions and Advanced Digital Monitoring

6.4. Australia: Long-Term Water Stewardship and Infrastructure Investments

6.5. India: Regulatory Mandates and Smart Technologies

6.6. Singapore: Flood Resilience and Smart Infrastructure Investments

6.7. Other Countries Analyzed

6.7.1. North America (Canada, Mexico)

6.7.2. Europe (UK, France, Spain, Italy, Russia, Rest of Europe)

6.7.3. Asia Pacific (South Korea, South East Asia, Rest of Asia)

6.7.4. South America (Brazil, Argentina, Rest of South America)

6.7.5. Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

7. Market Size Outlook by Region (2025-2034)

7.1. North America Stormwater Treatment Systems Market Size Outlook to 2034

7.1.1. By Technology

7.1.2. By Application

7.1.3. By Pollutant Removal

7.1.4. By End-User

7.2. Europe Stormwater Treatment Systems Market Size Outlook to 2034

7.2.1. By Technology

7.2.2. By Application

7.2.3. By Pollutant Removal

7.2.4. By End-User

7.3. Asia Pacific Stormwater Treatment Systems Market Size Outlook to 2034

7.3.1. By Technology

7.3.2. By Application

7.3.3. By Pollutant Removal

7.3.4. By End-User

7.4. South America Stormwater Treatment Systems Market Size Outlook to 2034

7.4.1. By Technology

7.4.2. By Application

7.4.3. By Pollutant Removal

7.4.4. By End-User

7.5. Middle East and Africa Stormwater Treatment Systems Market Size Outlook to 2034

7.5.1. By Technology

7.5.2. By Application

7.5.3. By Pollutant Removal

7.5.4. By End-User

8. Company Profiles: Leading Players in Stormwater Treatment Systems Market

8.1. Xylem Inc.

8.2. DuPont de Nemours, Inc.

8.3. Veolia Water Technologies

8.4. SUEZ

8.5. CONTECH Engineered Solutions LLC

8.6. Hydro International

8.7. Oldcastle Infrastructure

8.8. StormTrap

8.9. Advanced Drainage Systems, Inc. (ADS)

8.10. Prinsco, Inc.

8.11. ACO Group

8.12. Zurn Water Solutions

8.13. Toray Industries, Inc.

8.14. Kurita Water Industries Ltd.

8.15. H2O GmbH

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures