Efficiency-Enhancing Functional Coatings and Decarbonized Materials Driving High Growth

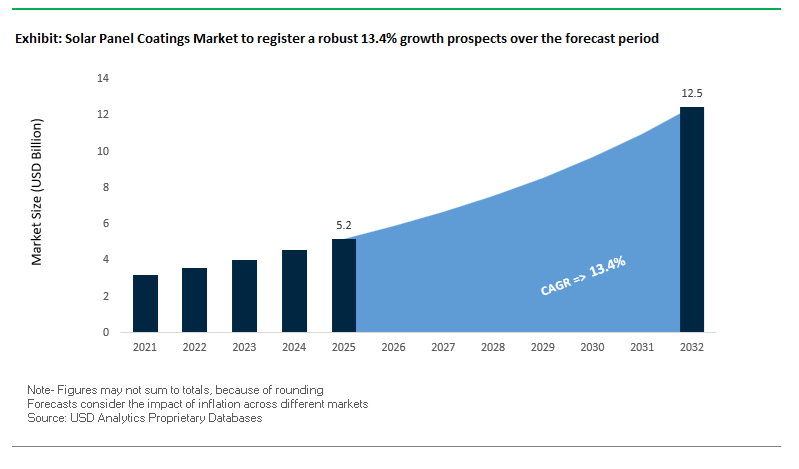

The global Solar Panel Coatings Market is expanding rapidly, supported by accelerating investments in renewable energy infrastructure, photovoltaic (PV) efficiency optimization, and advanced material technologies. The market was valued at $5.2 billion in 2025 and is projected to reach $12.5 billion by 2032, growing at a CAGR of 13.4% during 2025–2032. This growth reflects the increasing importance of coatings in enhancing solar module performance, durability, and lifecycle efficiency, particularly as solar installations scale across utility, commercial, and residential segments.

A primary growth driver is the rising demand for efficiency-enhancing coatings, including anti-reflective (AR), anti-soiling, and thermal management systems. These coatings play a critical role in maximizing light absorption, minimizing energy losses, and maintaining panel performance in harsh environmental conditions. In regions with high dust accumulation, such as the Middle East and North Africa, anti-soiling coatings are becoming essential to mitigate efficiency losses caused by particulate buildup.

Another key trend is the integration of thermal-regulating and reflective coatings that optimize the operating temperature of solar panels. Since PV efficiency declines with rising temperatures, coatings that reduce ambient heat or enhance infrared reflectivity are gaining traction, particularly in rooftop solar installations. Additionally, the emergence of solar-active coatings applied to building surfaces is expanding the market beyond traditional PV modules, transforming buildings into passive energy-generating systems.

Sustainability is also a central theme shaping the market. Manufacturers are increasingly focusing on low-carbon, VOC-free, and recyclable coating solutions, aligning with global decarbonization goals across the solar value chain. This includes the development of bio-based polymers, mass-balanced silicones, and fluoropolymer alternatives, which reduce environmental impact without compromising performance. As solar adoption continues to scale globally, coatings are becoming a critical enabler of efficiency, durability, and sustainability in next-generation energy systems.

Market Analysis: Anti-Soiling Nanotechnology, Solar-Ready Roofing Systems, and Low-Carbon Encapsulants Driving Competitive Innovation

The solar panel coatings market is being reshaped by advanced material innovation, cross-sector integration, and strategic capacity expansion, reflecting the growing complexity and performance requirements of modern solar systems. In March 2026, AkzoNobel introduced a solar-absorbing coating technology capable of converting architectural surfaces into thermal energy collectors, signaling a major expansion of solar coatings beyond traditional PV modules into building-integrated energy systems.

Durability in extreme environments remains a critical focus. Fenzi Group’s February 2026 expansion of its Duralux solar mirror coatings targets the Concentrated Solar Power (CSP) sector, providing high-performance backing layers that prevent silver oxidation in desert conditions. This development highlights the importance of coatings in maintaining optical efficiency and long-term reliability in harsh climates.

Thermal management is another key innovation area. PPG’s January 2026 launch of DURANAR® ULTRA-COOL® SMP coatings introduces infrared-reflective pigments designed to lower rooftop temperatures, indirectly improving solar panel conversion efficiency. These coatings are positioned within the “solar-ready roofing” segment, where building materials are optimized to support PV system performance.

Material advancements are also enhancing the durability and flexibility of solar coatings. Arkema’s February 2026 expansion of Rilsan® Clear production supports the development of transparent, high-durability coatings for flexible and portable solar modules, addressing the growing demand for lightweight and adaptable PV solutions.

Nanotechnology-driven solutions are gaining traction in utility-scale applications. Jotun’s October 2025 launch of anti-soiling coatings utilizes nanostructured surfaces to reduce dust adhesion and improve natural cleaning through rainfall. This innovation directly addresses one of the most significant operational challenges in large-scale solar farms—efficiency losses due to soiling.

Sustainability-driven innovation is further accelerating market transformation. Dow’s May 2025 introduction of Decarbia™ silicone encapsulants represents a shift toward mass-balanced, low-carbon materials that maintain high UV stability and moisture resistance while reducing the environmental footprint of solar module manufacturing.

Strategic consolidation is also strengthening technological capabilities. Covestro’s March 2025 integration of DSM’s solar coating assets enhances its position in sol-gel-derived anti-reflective coatings, a critical component for maximizing light transmission in solar glass. Meanwhile, KCC Corporation’s 2025 expansion of VOC-free powder coatings for solar mounting structures underscores the importance of supporting infrastructure coatings in ensuring system durability.

Infrastructure maintenance solutions are also evolving alongside solar deployment. Dalton Enterprises’ QuickPatch H2O (November 2024) provides a water-activated repair system for concrete foundations in solar farms, preventing moisture ingress and enhancing structural integrity. Additionally, AkzoNobel’s October 2024 solar plant launch in Poland demonstrated the real-world benefits of high-albedo reflective coatings, which improved the performance of bifacial solar panels installed on-site.

Market Trend: ASTM E3225-25 Standard Elevates Long-Term Durability Requirements for Anti-Reflective Coatings

The adoption of ASTM E3225-25 introduces a critical performance benchmark for anti-reflective coatings used in photovoltaic modules, addressing long-standing concerns regarding durability degradation under field conditions. Historically, AR coatings delivered initial gains in solar transmittance of 3% to 4%, but these benefits often declined within 3 to 5 years due to abrasion, humidity exposure, and environmental stress. The new standard mandates that coatings maintain a Solar Weighted Transmittance above 94.5% after 1,000 hours of accelerated abrasion testing, ensuring sustained optical performance over extended operational lifecycles. This requirement is reshaping product development strategies, with manufacturers prioritizing mechanically robust nanostructures and improved binder systems to preserve optical clarity. Additionally, ASTM E3225-25 introduces strict controls on refractive index stability, requiring deviation to remain below 0.05 units under high humidity conditions, specifically during Damp Heat testing at 85% relative humidity. This addresses the issue of optical drift, which previously introduced variability in energy yield forecasting for utility-scale solar assets. The standard is expected to drive increased investor confidence in AR-coated modules by ensuring predictable long-term performance, particularly in large-scale installations where even minor efficiency losses can significantly impact revenue models.

Market Trend: IEC 62878-2025 Establishes Unified Global Benchmark for Anti-Soiling Coatings Performance

The implementation of IEC 62878-2025 marks a significant step toward global standardization of anti-soiling technologies in the solar panel coatings market. Prior to this framework, performance validation was fragmented across regional testing methodologies, limiting comparability and scalability of anti-soiling solutions. The new standard introduces a Cleanability Index that quantitatively evaluates the ability of coatings to resist dust accumulation and facilitate natural cleaning mechanisms. Under IEC 62878-2025, compliant coatings must demonstrate the ability to limit soiling-induced power losses to less than 1% per cycle in high-dust environments such as deserts, compared to losses of 15% to 20% observed in untreated modules. This performance threshold is particularly critical for solar installations in arid regions where cleaning logistics are costly and water resources are limited. The standard also enforces surface energy requirements, mandating a maximum surface free energy below 25 mN/m for hydrophobic coatings. This ensures that particulate adhesion remains weak enough to be mitigated by low wind speeds of approximately 4 m/s, enabling passive cleaning without manual intervention. As a result, IEC 62878-2025 is accelerating the adoption of advanced anti-soiling coatings and providing a consistent framework for evaluating performance across global markets.

Market Opportunity: Dual-Function Anti-Reflective and Anti-Soiling Sol-Gel Coatings Driving Yield Optimization in Utility-Scale Solar Projects

The integration of anti-reflective and anti-soiling functionalities within a single sol-gel coating matrix represents a major advancement in solar panel surface engineering. These hybrid coatings are particularly valuable in large-scale solar deployments across regions characterized by high irradiance and dust accumulation, such as the Middle East, North Africa, and emerging Belt and Road markets. By combining enhanced optical transmission with reduced particulate adhesion, dual-function coatings deliver a cumulative increase in annual energy yield ranging from 6% to 8%. Approximately 3% of this improvement is attributed to reduced surface reflection, while an additional 5% results from minimized soiling losses. This synergistic effect significantly enhances the economic performance of photovoltaic assets. Furthermore, operational data indicates that the use of hybrid coatings can reduce scheduled cleaning frequency by up to 40%, lowering maintenance costs and extending system uptime. This reduction in operational expenditure contributes to a measurable decrease in the Levelized Cost of Electricity, estimated at $0.002 to $0.004 per kWh for coated bifacial modules. As solar developers increasingly prioritize lifecycle cost optimization and performance stability, dual-function sol-gel coatings are emerging as a preferred solution for next-generation photovoltaic installations.

Market Opportunity: Hydrophobic Anti-Icing Coatings Unlocking Solar Expansion in Cold Climate Regions

The expansion of solar energy infrastructure into cold climate regions is creating new demand for advanced anti-icing coatings capable of maintaining panel performance under snow and ice conditions. These coatings are engineered to reduce ice adhesion and facilitate passive shedding through a combination of low surface energy and photothermal effects. Field evaluations conducted in 2026 demonstrate that anti-icing coatings can enable solar panels to recover up to 85% more energy during winter months by preventing snow accumulation that would otherwise reduce generation capacity by up to 90%. The coatings achieve this by lowering ice adhesion strength to below 20 kPa, allowing snow and ice to slide off at tilt angles as low as 10 degrees, thereby reducing structural stress on mounting systems and trackers. Additionally, advanced formulations incorporate photothermal properties that increase surface temperature by 3°C to 5°C under minimal near-infrared exposure, promoting ice detachment even in sub-zero ambient conditions. This passive de-icing capability eliminates the need for energy-intensive heating systems or manual snow removal, improving overall system efficiency and reliability. As solar deployment accelerates in regions such as Northern Europe and Canada, hydrophobic anti-icing coatings are becoming a critical enabler of year-round energy generation and infrastructure resilience.

Solar Panel Coatings Market Share and Segmentation Insights: Factory Integration Dominance and Direct Manufacturer Partnerships

By Installation Type: Factory-Applied Coatings Lead with Precision and Cost Efficiency

The factory-applied segment dominated the solar panel coatings market with a 76.4% share in 2025, driven by its superior quality control, uniform coating performance, and cost efficiency at scale. Advanced coatings such as anti-reflective coatings, hydrophobic coatings, and self-cleaning coatings are integrated directly during solar panel manufacturing under controlled production environments, ensuring consistent film thickness, adhesion, and optical efficiency. This precision is critical for maximizing solar panel efficiency, light transmission, and long-term durability. Additionally, factory integration significantly reduces the cost per watt, as coatings are applied inline during production, minimizing additional labor and processing expenses. In contrast, retrofit applications require on-site cleaning, preparation, and manual coating, increasing operational costs and limiting widespread adoption. As global solar installations continue to rise, factory-applied coatings remain the preferred solution for enhancing photovoltaic performance and lifecycle efficiency in the solar energy sector.

By Sales Channel: Direct Sales to Panel Manufacturers Lead with Customization and High-Volume Procurement

The direct sales segment to panel manufacturers accounted for a dominant 66.1% share of the solar panel coatings market in 2025, reflecting the concentration of demand among large-scale photovoltaic (PV) module producers. Leading companies such as Longi, JinkoSolar, Trina Solar, and Canadian Solar procure coating materials directly from chemical suppliers to ensure bulk supply, cost optimization, and consistent product quality. These manufacturers require customized coating formulations tailored to specific glass textures, solar cell technologies (PERC, TOPCon, HJT), and environmental durability standards, including compliance with IEC 61215 and IEC 61701 testing protocols. Direct collaboration enables faster innovation cycles and ensures coatings meet stringent performance, durability, and efficiency benchmarks. Additionally, long-term supply agreements provide stable sourcing, technical support, and process integration, reinforcing the importance of direct relationships. As the solar industry scales rapidly, direct sales channels continue to drive efficiency, innovation, and growth in the global solar panel coatings market.

Competitive Landscape of the Solar Panel Coatings Market

PPG Leads Market with Anti-Reflective and Self-Cleaning Coating Technologies

PPG Industries, Inc. is the benchmark player in the solar panel coatings market, particularly in anti-reflective (AR) coatings, which account for 38% of market revenue in 2026. Its sol-gel-based coatings reduce reflection losses from 4% to below 1%, significantly improving panel efficiency. PPG has also scaled hydrophilic self-cleaning coatings that use ambient humidity to remove dust, reducing maintenance costs and improving energy output by lowering Levelized Cost of Electricity (LCOE) by up to 2.7%. Its strategic focus on nanotechnology and bifacial module coatings reinforces its leadership in large-scale solar applications.

Arkema Strengthens Market Leadership with PVDF-Based Durability and UV-Resistant Coatings

Arkema Group is a key player in the solar panel coatings market, leveraging its Kynar® PVDF technology to deliver long-term durability. Its coatings provide 25+ years of weatherability, making them ideal for harsh environments such as desert installations. Arkema is also advancing nanostructured coating technologies to enhance UV resistance and improve module longevity. Its partnerships with BASF and AkzoNobel highlight its role in developing low-carbon solar coating solutions, supporting sustainability goals across the renewable energy sector.

AkzoNobel Expands into Energy-Generating Coatings with Integrated Solar Solutions

AkzoNobel N.V. is transitioning into an integrated solutions provider in the solar panel coatings market, moving beyond traditional coatings. Its collaboration with Calosol introduces energy-harvesting façade coatings capable of generating power even under low-light conditions. The company is also pioneering infrared-reflective pigments for solar-integrated roofing, reducing thermal stress and improving panel efficiency. Its expansion of training centers in China supports large-scale deployment of advanced coatings in rapidly growing solar markets.

BASF Drives Market with Advanced Additives and Nanomaterial-Based Coatings

BASF SE plays a critical enabling role in the solar panel coatings market, supplying essential additives and materials. Its HALS and NOR® HALS stabilizers prevent degradation and yellowing, extending coating lifespan. BASF is also advancing nanomaterial-based coatings using TiO₂ and SiO₂ dispersions, enabling photocatalytic self-cleaning surfaces. Its integration of waterborne coating systems reduces VOC emissions while maintaining high optical performance, reinforcing its position as a key supplier in solar coating technologies.

DSM (Covestro) Leads High-Transmission Coatings for Premium Solar Modules

DSM, now integrated into Covestro, is a major player in the solar panel coatings market, particularly in high-transmission (HT) coatings. Its anti-reflective solutions deliver 3–4% higher energy yield over the lifespan of solar modules, making them critical for utility-scale projects. The company has transitioned to PFAS-free formulations, aligning with regulatory requirements and sustainability trends. DSM is also targeting the floating solar segment with coatings designed to resist moisture, salt, and biological growth.

Nippon Paint Drives APAC Growth with Reflective Coatings and Climate Mitigation Solutions

Nippon Paint Holdings Co., Ltd. is a dominant player in the Asia-Pacific solar coatings market, benefiting from rapid regional solar deployment. Its THERMOEYE coating reduces heat buildup and protects solar-integrated structures from thermal stress. The company has reported 130–150% growth in solar-related coatings, driven by government initiatives and infrastructure investments. Its advanced pigment encapsulation technologies ensure long-term reflectance and durability in high-humidity environments, strengthening its position in emerging markets.

India Emerging as a Global Hub for Anti-Soiling Solar Coatings and High-Dust Performance Solutions

India has rapidly positioned itself as a high-growth leader in the solar panel coatings market, particularly in the deployment of anti-soiling (AS) coatings designed for extreme dust-prone environments. With over 45 GW of solar capacity in key states like Rajasthan and Gujarat integrating waterless robotic cleaning systems paired with anti-soiling coatings, the country has become a large-scale testing ground for durability and efficiency enhancement technologies.

Technological advancements such as nano-textured super-hydrophilic silica coatings are transforming maintenance practices by leveraging natural dew for self-cleaning, significantly reducing operational costs. Government initiatives, including updates to the ALMM certification framework and Quality Control Orders, are mandating durability and efficiency-retention standards, making high-performance coatings essential in solar module design. Additionally, expansion in domestic manufacturing of anti-reflective (AR) coated solar glass and increased adoption in agrivoltaics applications are strengthening India’s role as a strategic growth hub in the global solar coatings ecosystem.

China Leading Advanced Functional Solar Coatings with Perovskite and BIPV Innovations

China is dominating the solar coatings industry by transitioning toward advanced functional thin films and next-generation photovoltaic technologies. Breakthrough innovations such as fluorinated interface coatings for tandem perovskite-silicon cells are significantly improving efficiency and moisture resistance, positioning China at the forefront of high-efficiency solar energy solutions.

The country is also advancing Building-Integrated Photovoltaics (BIPV) through the commercialization of translucent solar coatings that enable energy generation without compromising building aesthetics. Manufacturing innovations such as APCVD-based continuous coating processes are improving efficiency and reducing energy consumption in production. Government-backed programs are supporting the adoption of thermochromic and smart solar coatings in urban developments, while large-scale investments in bifacial module production are driving demand for dual-sided anti-reflective coatings. Additionally, strict aviation safety regulations are accelerating the use of anti-glare coatings in solar farms near urban and airport zones.

Saudi Arabia Driving Extreme Climate Solar Coatings for High-Temperature and Sand-Resistant Applications

Saudi Arabia is emerging as a critical market for high-performance solar panel coatings, driven by extreme environmental conditions and large-scale renewable energy projects under Vision 2030. The deployment of high-heat siloxane coatings in mega-projects such as NEOM is enabling solar panels to withstand intense UV exposure and temperature extremes exceeding 75°C.

Technological advancements include the development of passive radiative cooling coatings, which reduce panel operating temperatures and improve energy output. The country is also focusing on sand-resistant and abrasion-resistant coatings, essential for maintaining panel performance in desert environments. Regulatory frameworks such as SASO’s climate-adaptive standards are encouraging the adoption of advanced coating technologies. Additionally, investments in local manufacturing and collaborations with global research institutions are driving innovation in self-healing coatings designed to repair damage caused by sandstorms, further enhancing system longevity.

United States Advancing Smart Solar Coatings for Energy Efficiency and Extreme Weather Protection

The United States is a major innovator in the solar panel coatings market, driven by policy support and a focus on resilience against extreme weather conditions. Government initiatives under the Solar Energy Technologies Office (SETO) are promoting the development of circular coating solutions that facilitate easier recycling of solar components.

Technological innovations include anti-icing and snow-shedding coatings for colder regions, improving system reliability by preventing snow accumulation. The transition toward PFAS-free, silica-based superhydrophobic coatings is being driven by regulatory mandates, enhancing environmental compliance. Advanced solutions such as quantum-dot down-shifting coatings are improving the efficiency of existing solar panels by optimizing light absorption. Additionally, the deployment of fire-retardant coatings in wildfire-prone areas and continued investment in thin-film coating technologies are reinforcing the United States’ leadership in high-performance solar coatings innovation.

Germany Leading BIPV Integration and Aesthetic Solar Coatings for Urban and Heritage Applications

Germany is at the forefront of architectural solar coatings, focusing on integrating photovoltaic systems into urban and heritage structures. Innovations such as color-interference coatings allow solar panels to mimic traditional building materials, enabling seamless integration into protected heritage sites.

Technological advancements include the development of multi-layer interference coatings that maintain high energy efficiency while offering aesthetic customization. Government initiatives such as the Solar Package I are driving the adoption of consumer-grade solar coatings for balcony installations, expanding the residential solar market. Additionally, increased production of high-purity silane-based materials is supporting domestic manufacturing. Regulatory frameworks under the EU Solar Rooftop Initiative are standardizing the use of anti-reflective and low-iron coatings, while specialized coatings for floating solar systems are addressing challenges such as moisture and algae growth.

South Korea Driving Next-Generation Solar Coatings for Perovskite Stability and Optoelectronic Integration

South Korea is emerging as a key innovator in advanced solar coatings, leveraging its expertise in semiconductors and display technologies. Breakthrough developments such as taurine-based coatings for perovskite solar cells are significantly enhancing stability and lifespan by preventing oxygen-induced degradation.

Technological advancements include the use of atomic layer deposition (ALD) coatings to create highly effective moisture barriers for flexible solar applications, including wearables and automotive systems. Strategic investments by major industry players are driving innovation in interface engineering coatings for tandem solar cells, improving energy efficiency. Additionally, the integration of electrochromic coatings in automotive solar roofs is enabling dynamic control between power generation and thermal management. Regulatory policies promoting sustainable manufacturing are accelerating the shift toward waterborne and high-solid coating formulations, reinforcing South Korea’s leadership in next-generation solar technologies.

Solar Panel Coatings Market Report Scope

Solar Panel Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.2 Billion

|

|

Market Size (2032)

|

$12.5 Billion

|

|

Market Growth Rate

|

13.4%

|

|

Segments

|

By Coating Type (Anti-Reflective Coatings, Hydrophobic Coatings, Self-Cleaning Coatings, Anti-Soiling Coatings, Anti-Abrasion, Anti-Icing, Others), By Coating Material (Silicon Dioxide, Titanium Dioxide, Fluoropolymers, Polysiloxanes, Nanomaterials), By Technology (Sol-Gel Process, Physical Vapor Deposition, Chemical Vapor Deposition, Spray Coating, Dip Coating), By Installation Type (Factory-Applied, Retrofit), By End-User (Utility-Scale, Commercial and Industrial, Residential, Agriculture, Automotive, Space and Defense), By Sales Channel (Direct Sales, Specialized Distributors, Operation and Maintenance)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M Company, PPG Industries, Inc., Akzo Nobel N.V., BASF SE, Arkema S.A., Evonik Industries AG, DuPont de Nemours, Inc., Hempel A/S, Jotun Group, Saint-Gobain, Fenice S.p.A., Nanotech Products Pty Ltd, Diamon-Fusion International, Inc., Optitune Oy, Unelko Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Solar Panel Coatings Market Segmentation

By Coating Type

- Anti-Reflective Coatings

- Hydrophobic Coatings

- Self-Cleaning Coatings

- Anti-Soiling Coatings

- Anti-Abrasion

- Anti-Icing

- Others

By Coating Material

- Silicon Dioxide

- Titanium Dioxide

- Fluoropolymers

- Polysiloxanes

- Nanomaterials

By Technology

- Sol-Gel Process

- Physical Vapor Deposition

- Chemical Vapor Deposition

- Spray Coating

- Dip Coating

By Installation Type

By End-User

- Utility-Scale

- Commercial and Industrial

- Residential

- Agriculture

- Automotive

- Space and Defense

By Sales Channel

- Direct Sales

- Specialized Distributors

- Operation and Maintenance

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Solar Panel Coatings Industry

- 3M Company

- PPG Industries, Inc.

- Akzo Nobel N.V.

- BASF SE

- Arkema S.A.

- Evonik Industries AG

- DuPont de Nemours, Inc.

- Hempel A/S

- Jotun Group

- Saint-Gobain

- Fenice S.p.A.

- Nanotech Products Pty Ltd

- Diamon-Fusion International, Inc.

- Optitune Oy

- Unelko Corporation

*- List not Exhaustive