Market Overview: Transforming Water Management with WTaaS

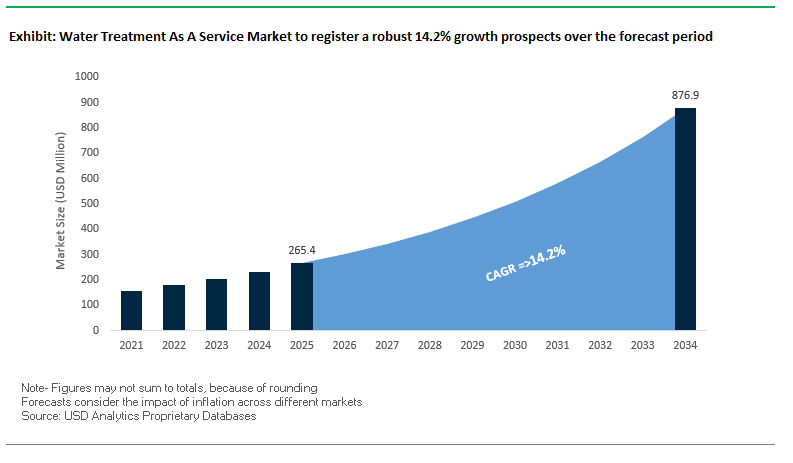

The Water Treatment as a Service (WTaaS) market is experiencing rapid transformation, evolving from a traditional capital-intensive model to a flexible, pay-per-use service that alleviates operational complexity for end-users. The market is poised to grow from $265.4 billion in 2025 to $876.8 billion by 2034, at a CAGR of 14.2%, driven by increasing demand for sustainable water management, regulatory compliance, and technological innovations.

WTaaS allows industries, municipalities, and commercial enterprises to outsource water treatment operations while benefiting from professional expertise, real-time monitoring, and advanced treatment technologies. This model is particularly vital in regions facing high water stress, aging infrastructure, and increasing environmental compliance pressures.

Key insights for industry Stakeholders include:

- North America: Strong adoption in industrial sectors as companies reduce operational risks and focus on core competencies.

- Regulatory Drivers: The U.S. Clean Water Act and the EU Water Framework Directive are pivotal, with fines reaching $50,000 per violation in certain cases.

- Urban Water Stress: Impermeable surfaces in cities increase runoff volumes by up to 300%, necessitating advanced treatment and reuse systems.

- Asia-Pacific Growth: Rapid urbanization and green building codes are driving WTaaS adoption to address population growth and water scarcity.

Market Analysis: Recent Developments Shaping the WTaaS Landscape

The WTaaS market continues to evolve through technological advancements, strategic acquisitions, and innovative collaborations designed to enhance water treatment efficiency and sustainability. In October 2024, the Da Tang Industrial Park in Foshan, China, launched a Minimum Liquid Discharge (MLD) wastewater treatment plant treating 160,000 m³/day, marking a key milestone in industrial water reuse. This project underscores the rising emphasis on sustainable water management and circular economy principles in Asia.

In January 2025, the American Society of Civil Engineers (ASCE) 2025 Report Card rated U.S. wastewater infrastructure as D+, highlighting an urgent need for upgrades, increased investment, and WTaaS adoption. Following this, strategic acquisitions and expansions have accelerated market capabilities:

- June 2025: Grundfos acquired Newterra, expanding its decentralized water and wastewater treatment portfolio in the U.S.

- May 2025: Veolia achieved full ownership of its Water Technologies and Solutions subsidiary to streamline offerings and enhance sustainable service delivery.

Strategic partnerships are also driving innovation. In July 2025, SUEZ partnered with Seabex, a French AgriTech start-up, to explore agricultural benefits from biochar produced through wastewater treatment. Similarly, Veolia implemented France’s largest treated wastewater reuse project in July 2025, supplying reclaimed water for irrigation in Argelès-sur-Mer.

In August 2025, DuPont Water Solutions was recognized for sustainability achievements in industrial wastewater treatment, while Fluence Energy, Inc. expanded its domestic supply chain in Houston, linking energy storage solutions with WTaaS offerings. These developments illustrate a dynamic market where regulatory compliance, sustainability, and technological innovation intersect to accelerate adoption globally.

Key Market Trends Shaping the WTaaS Industry

Shift from CapEx to OpEx Models Accelerates Adoption

The WTaaS market is experiencing a transformative shift as businesses and municipalities move away from traditional capital-intensive water infrastructure to flexible Operational Expenditure (OpEx) models. Leading providers like Veolia Water Technologies offer volume-based pricing, allowing customers to pay only for water treated rather than making large upfront investments. Real-world implementations, such as the City of Alice, Texas, in partnership with Seven Seas Water Group, demonstrate that this model can remove millions in planned capital outlay while ensuring predictable, lower water costs for residents. This financial flexibility is driving rapid adoption across municipal and industrial sectors, reducing risk while enabling organizations to focus on their core operations.

Integration of Digital Solutions and Smart Technologies

Digitalization is redefining WTaaS delivery, with technologies such as AI, IoT, and smart sewer systems enabling predictive monitoring, optimization, and cost reduction. Xylem’s digital water solutions, for instance, helped a utility reduce Combined Sewer Overflow (CSO) volume by 80%, saving $400 million in CapEx. Academic studies highlight that real-time monitoring and AI-driven optimization are becoming essential in WTaaS, enabling predictive maintenance, minimizing human intervention, and ensuring compliance with stringent wastewater discharge standards, reinforcing the value of service-based models over traditional infrastructure.

Public-Private Partnerships (PPPs) Fuel Market Growth

The adoption of PPPs is a critical growth driver for WTaaS, providing governments access to private capital, technology, and operational expertise while ensuring long-term sustainability. Initiatives such as India’s 2025 Liquid Waste Management Rules and the Jal Jeevan Mission support hybrid annuity-based PPP models, enabling cities like Ayodhya and Prayagraj to implement modern wastewater treatment systems with performance-based operations. Globally, PPPs are increasingly instrumental in meeting Sustainable Development Goal 6 for universal access to clean water and sanitation, positioning WTaaS as a key solution for large-scale municipal water challenges.

Opportunities in Water Treatment as a Service Market

The WTaaS market offers significant opportunities across industrial, municipal, and high-complexity applications. With CapEx-to-OpEx shifts, digital integration, and supportive PPP frameworks, providers can expand offerings in areas like predictive maintenance, advanced biological and membrane treatment, and full-service models such as BOOT and Chemicals-as-a-Service (CaaS). The growing focus on water reuse, zero liquid discharge, and compliance-driven outsourcing creates avenues for revenue growth while helping customers reduce risk, optimize resource use, and achieve regulatory compliance, reinforcing WTaaS as a scalable, future-ready water management solution.

Market Share Analysis of Water Treatment as a Service

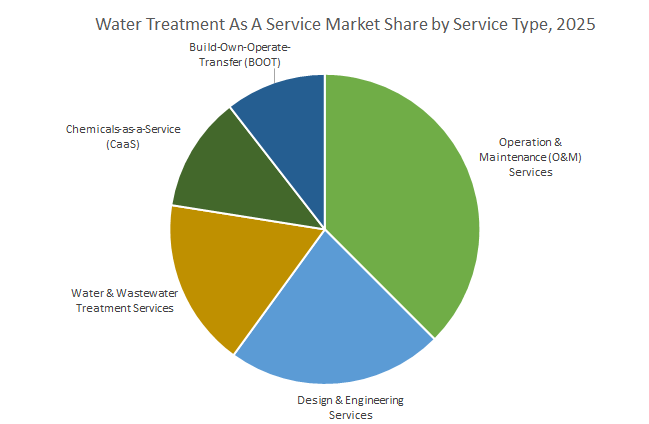

Operation & Maintenance Services Remain the Backbone of WTaaS

By service type, Operation & Maintenance (O&M) services dominate with 35.7% market share, representing the core of the WTaaS model where providers fully manage plant operations, maintenance, and compliance. Design & Engineering services (22.5%) often precede O&M contracts, offering feasibility studies and tailored system design critical for efficient, reliable service delivery. Water & Wastewater Treatment services (16.9%) and Chemicals-as-a-Service (CaaS) (11.8%) provide niche outsourcing models that align provider incentives with performance outcomes. Smaller yet strategically significant, BOOT contracts enable clients to fully outsource design, construction, and operation for long-term, capital-intensive projects, particularly in municipal and industrial settings.

Membrane and Biological Technologies Drive Market Share

By treatment technology, Membrane Filtration systems (RO, UF, NF) lead with 26.9% share due to their complexity, high-value application, and need for skilled O&M to prevent fouling and ensure reliability. Activated Sludge and Biological Treatment follow closely with 22.5%, reflecting the core role of biological processes in wastewater management. Other critical technologies include Clarification & Coagulation (15–18%), Disinfection (UV, Ozone, Chlorination, 13.2%), Ion Exchange & Demineralization, Sludge Treatment & Management, and Filtration & Media. These technologies are often bundled in full-service contracts, with sludge management and disinfection services particularly sought after for regulatory compliance and operational efficiency.

Industrial Sector Leads WTaaS Adoption

By end-user, Industrial customers account for 64.3% of the market, driven by manufacturers’ need for compliance, predictable costs, and the ability to focus on core operations. Sectors such as Food & Beverage, Pharmaceuticals, Power, and Chemicals are leveraging WTaaS to optimize water and wastewater processes without investing heavily in infrastructure. Municipal adoption, at 35.7%, is growing via PPPs and BOOT models, allowing cities to upgrade aging water infrastructure while outsourcing technical and operational risks to specialized service providers.

Wastewater Recycling and Process Water Lead Applications

By application, Wastewater Treatment & Recycling dominates with 32.8% share, driven by water scarcity, circular economy initiatives, and regulatory discharge tariffs. Process Water Treatment (22.5%) ensures product quality and production reliability, making guaranteed service models highly valuable. Boiler & Cooling Water treatment (16.9%) focuses on energy efficiency, corrosion prevention, and asset protection, while Effluent Treatment & Compliance Management mitigates regulatory risk. Zero Liquid Discharge (ZLD) projects represent the most complex and capital-intensive operations, ideally suited for fully outsourced, service-based models that transfer operational and technical risk to the provider.

United States: WTaaS Expansion Fueled by Infrastructure Funding and PFAS Regulations

The United States WTaaS market is witnessing significant growth, driven by government initiatives, regulatory mandates, and corporate innovations. The Bipartisan Infrastructure Law (BIL) allocates over $50 billion to the EPA to modernize water infrastructure, encouraging public-private partnerships and service-based models like WTaaS. Regulatory pressure from newly finalized PFAS Maximum Contaminant Levels is prompting municipalities and industrial clients to adopt advanced treatment technologies without the burden of capital-intensive purchases, making WTaaS an attractive option. Corporate initiatives, such as the 2023 merger of Xylem and Evoqua, have expanded WTaaS capabilities, including projects like waste-to-renewable energy facilities in California that integrate anaerobic digestion and operate under service contracts. Key applications include treatment of complex industrial wastewater from pharmaceuticals, electronics, and other regulated sectors, alongside municipal water management solutions that reduce upfront investment needs while ensuring compliance and sustainability.

China: Service-Based Models Drive Sponge City Water Infrastructure

China’s WTaaS market is strongly influenced by government initiatives, regulatory policies, and innovative corporate projects. The “Sponge City” program, launched in 2014, aims for over 80% of urban areas to meet stormwater management standards by 2030, necessitating large-scale investments in both natural and engineered systems. The Ministry of Ecology and Environment (MEE) enforces strict industrial wastewater discharge regulations, while the 14th Five-Year Plan emphasizes water reuse, generating significant demand for service-based water treatment solutions. Corporate adoption of WTaaS is exemplified by Danish company Aquaporin’s pilot project treating landfill leachate, highlighting the country’s openness to innovative service models. Key applications include sustainable urban water management, stormwater treatment, and improving water quality in rapidly developing cities.

India: Government Programs and Technology Partnerships Expand WTaaS Adoption

India’s WTaaS market is expanding due to government programs, infrastructure investments, technological advancements, and corporate initiatives. Initiatives like Jal Jeevan Mission, Namami Gange, and Swachh Bharat Mission-Urban 2.0 drive demand for comprehensive water and wastewater management solutions, many structured as service contracts. Technology partnerships, such as Pani Energy’s collaboration with Murugappa Water Technology & Solutions for AI-driven advanced oxidation process (AOP) solutions, demonstrate a shift from equipment sales to full-service offerings. Ion Exchange (India) Ltd.’s commercialization of TERI’s patented photocatalytic oxidation technology further highlights the adoption of advanced treatment solutions in a service model. Key applications include municipal wastewater treatment, industrial water management, and sustainable water reuse, particularly in urban centers and industrial clusters.

Germany: Stricter EU Standards and Digitalization Boost WTaaS Demand

Germany’s WTaaS market benefits from stringent EU regulations, technological innovation, and corporate expertise. The revised EU Urban Wastewater Treatment Directive (January 2025) mandates expansion to a “4th purification stage” to remove micropollutants, driving the adoption of service-based advanced oxidation processes and membrane filtration. German cities are increasingly leveraging AI, digital twins, and advanced monitoring for optimized water management, supporting the WTaaS model. Companies like H2O GmbH, GEA Group AG, and Veolia are providing integrated water treatment solutions as services, such as the Roche Penzberg project, which delivered an annual carbon emissions reduction of 950 metric tons. Key applications include industrial wastewater management, municipal water treatment, and decentralized service-based solutions for sustainable operations.

Singapore: Flood Resilience and Compliance Drive WTaaS Implementation

Singapore’s WTaaS market is shaped by government investments, regulatory frameworks, and technological leadership. The country plans to invest approximately S$150 million in 2025 on drainage upgrading projects to strengthen flood resilience. The Public Utilities Board (PUB) exemplifies WTaaS adoption, managing infrastructure and services efficiently. Amendments to the Sewerage and Drainage Act (November 2024) require proper operation and maintenance of flood protection measures, creating opportunities for WTaaS providers. The Singapore International Water Week (SIWW) Spotlight 2025 facilitates knowledge exchange on flood resilience, policy implementation, and innovative water management solutions. Key applications focus on urban flood mitigation, regulatory compliance, and sustainable water service delivery in dense urban areas.

Saudi Arabia: PPP Projects and Advanced Technologies Drive WTaaS Growth

Saudi Arabia’s WTaaS market is expanding due to investments in infrastructure, corporate innovations, and sustainable development initiatives. The Saudi Water Partnership Company (SWPC) continues to launch wastewater treatment projects under the PPP model, predominantly using advanced reverse osmosis (RO) and membrane technologies for water reuse. In 2025, VA Tech Wabag secured a major sewage treatment contract in Riyadh as part of the Vision 2030 initiative, emphasizing service-based delivery. Toray Industries supplied RO membranes for the Shuaibah 3 IWP seawater desalination plant, aligning with decarbonization and sustainability goals. Key applications include reuse of treated wastewater in non-potable municipal, industrial, and agricultural applications, highlighting the role of WTaaS in supporting the country’s water security and environmental stewardship.

Competitive Landscape: Leading Players Driving WTaaS Innovation

The competitive landscape of the WTaaS market is shaped by global technology leaders and innovative startups offering end-to-end solutions. Companies are increasingly integrating digital platforms, predictive analytics, and advanced treatment technologies to strengthen their market position.

Veolia Water Technologies – Global Leader in Water Resource Management

Veolia offers comprehensive WTaaS solutions encompassing equipment, installation, maintenance, and repairs. In May 2025, Veolia acquired full ownership of its Water Technologies and Solutions subsidiary to enhance operational efficiency and sustainability. Its GreenUp 2024–2027 strategy focuses on climate-conscious resource depollution and water reuse. Veolia provides biological, membrane, and thermal ZLD systems for municipal and industrial applications, solidifying its position as a WTaaS innovator.

SUEZ – High-Performance Water and Wastewater Solutions

SUEZ delivers tailored solutions for complex industrial and municipal environments. The company recently implemented wastewater recycling projects in Asia and leverages digital platforms for predictive performance monitoring. Its Degremont technologies are globally recognized for transforming sewage sludge into energy, emphasizing sustainability. SUEZ’s strategic use of analytics reduces operational costs and optimizes chemical use, providing clients with highly efficient water recycling systems.

Xylem Inc. – End-to-End Water Technology Specialist

Xylem’s strength lies in providing integrated water cycle solutions, from pumps and biological treatment to analytics. Its 2023 acquisition of Evoqua created the Water Solutions and Services (WSS) segment, scaling global service offerings. Xylem emphasizes IoT-driven monitoring and predictive maintenance, ensuring energy-efficient, cost-effective WTaaS solutions for diverse end-markets.

DuPont Water Solutions – Advanced Membrane Technology Provider

DuPont excels in high-performance membranes and advanced water treatment technologies. Its 2025 R&D 100 Award-winning FilmTec™ Fortilife™ XC160 Membrane exemplifies its commitment to sustainable water reuse. DuPont’s portfolio includes RO, NF, ultrafiltration, and ion exchange solutions, supporting circular water management and reducing operational costs globally.

Pentair – Residential and Commercial WTaaS Innovator

Pentair offers residential and commercial water softening and filtration systems with a professional service network. Its True Blue PROs program ensures installation, maintenance, and water analysis, helping customers avoid over 7.7 billion single-use plastic bottles in 2022. Pentair’s WTaaS model caters to homes, hotels, and commercial establishments, delivering sustainable, high-quality water solutions.

Fluence Corporation – Decentralized and Smart-Packaged Solutions

Fluence specializes in decentralized WTaaS solutions, focusing on plug-and-play systems to reduce infrastructure costs. Its innovative Membrane Aerated Biofilm Reactor (MABR) technology provides energy-efficient nutrient removal. Fluence’s smart control systems enhance effluent quality with minimal energy usage, serving clients in remote locations and dynamically changing water environments.

Water Treatment As A Service Market Report Scope

Water Treatment As A Service Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$265.4 Million

|

|

Market Size (2034)

|

$876.8 Million

|

|

Market Growth Rate

|

14.2%

|

|

Segments

|

By Service Type (Design & Engineering Services, Operation & Maintenance Services, Water & Wastewater Treatment Services, Chemicals-as-a-Service, Build-Own-Operate-Transfer), By Treatment Technology (Membrane Filtration, Ion Exchange & Demineralization, Filtration & Media, Disinfection, Activated Sludge & Biological Treatment, Clarification & Coagulation, Sludge Treatment & Management), By End-User Industry (Municipal, Industrial), By Application (Process Water Treatment, Wastewater Treatment & Recycling, Zero Liquid Discharge, Boiler Water & Cooling Water Treatment, Effluent Treatment & Compliance Management), By Contract/Pricing Model (Subscription-based, Performance-based Contracts, Fixed-price Contracts, Pay-per-volume)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia, SUEZ, Xylem Inc., Evoqua Water Technologies, DuPont de Nemours, Inc., Pentair plc, Toray Industries, Inc., Aquatech International, Kubota Corporation, The Dow Chemical Company, VA Tech Wabag Ltd., Mitsubishi Chemical Corporation, Kurita Water Industries Ltd., H2O GmbH, Thermax Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Water Treatment As A Service Market Segmentation

By Service Type

- Design & Engineering Services

- Operation & Maintenance Services

- Water & Wastewater Treatment Services

- Chemicals-as-a-Service (CaaS) / Managed Chemical Services

- Build-Own-Operate-Transfer (BOOT) / Full-Outsourcing

By Treatment Technology

- Membrane Filtration (RO, UF, NF, MF)

- Ion Exchange & Demineralization

- Filtration & Media

- Disinfection

- Activated Sludge & Biological Treatment

- Clarification & Coagulation

- Sludge Treatment & Management

By End-User Industry

- Municipal

- Industrial

- Power Generation

- Oil & Gas

- Chemicals & Petrochemicals

- Food & Beverage

- Pharmaceuticals & Healthcare

- Metals & Mining

- Pulp & Paper

- Semiconductors & Electronics

- Automotive

By Application

- Process Water Treatment

- Wastewater Treatment & Recycling

- Zero Liquid Discharge (ZLD)

- Boiler Water & Cooling Water Treatment

- Effluent Treatment & Compliance Management

By Contract/Pricing Model

- Subscription-based

- Performance-based Contracts

- Fixed-price Contracts

- Pay-per-volume / Consumption-based

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Water Treatment As A Service Industry include-

- Veolia

- SUEZ

- Xylem Inc.

- Evoqua Water Technologies

- DuPont de Nemours, Inc.

- Pentair plc

- Toray Industries, Inc.

- Aquatech International

- Kubota Corporation

- The Dow Chemical Company

- VA Tech Wabag Ltd.

- Mitsubishi Chemical Corporation

- Kurita Water Industries Ltd.

- H2O GmbH

- Thermax Limited

*- List not Exhaustive

Research Coverage – USDAnalytics

This report investigates the global Water Treatment as a Service (WTaaS) market, offering an in-depth analysis of how the sector is transitioning from capital-intensive infrastructure models to scalable, flexible, and performance-based service contracts. It highlights technological breakthroughs such as membrane-based treatment, AI-driven optimization, and digital twins, while reviewing the market impact of regulatory shifts like the revised EU Urban Wastewater Treatment Directive and PFAS standards in the U.S. The report analyzes developments such as Veolia’s full-service ZLD systems, DuPont’s membrane innovations, and PPP-driven projects in India, Saudi Arabia, and Singapore. This report is an essential resource for municipal authorities, industrial operators, ESG strategists, and infrastructure investors seeking sustainable, OpEx-driven water management solutions. Through regional deep-dives, emerging use cases, and strategic company profiles, USDAnalytics equips stakeholders with a comprehensive roadmap to navigate the rapidly evolving WTaaS landscape. Scope Includes-

- Segmentation: By Service Type, Treatment Technology, End-User Industry, Application, and Contract/Pricing Model

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Time Frame: Historic data from 2021 to 2024 and forecast data from 2025 to 2034

- Companies Covered: Analysis/profiles of 15+ companies including Veolia, SUEZ, Xylem Inc., DuPont de Nemours, Pentair, Thermax, H2O GmbH, Evoqua, Kurita, Mitsubishi Chemical, VA Tech Wabag, Dow Chemical, Kubota, Toray, Aquatech International

Methodology

The methodology for this report by USDAnalytics combines bottom-up market modeling, multi-variable forecast validation, and qualitative insights gathered from industry experts and regulatory sources. Primary research involved interviews with service providers, technology vendors, and municipal water managers, while secondary sources included ASCE infrastructure reports, government policy documents (e.g., EU WWTD, India’s Liquid Waste Rules), and published case studies from global infrastructure projects. Proprietary forecasting algorithms were applied across 5-year policy cycles and infrastructure investment horizons, allowing for regional scenario planning. Emerging technologies and contract models were analyzed for impact using case-based simulations, ensuring each segment projection aligns with regulatory trends, adoption rates, and value creation across the WTaaS value chain.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Water Treatment as a Service (WTaaS) Market

1. Executive Summary

1.1. Market Highlights & Key Projections

1.2. WTaaS: A Transformative Market Overview

1.3. Global Market Snapshot (2025–2034)

1.3.1. Current Market Valuation (2025): USD 265.4 Billion

1.3.2. Projected Market Valuation (2034): USD 876.8 Billion

1.3.3. Compound Annual Growth Rate (CAGR): 14.2%

2. Market Dynamics: Drivers, Restraints, and Opportunities

2.1. Market Drivers

2.1.1. Shift from CapEx to OpEx Models

2.1.2. Regulatory Compliance and Stricter Environmental Standards

2.1.3. Increasing Global Water Stress and Scarcity

2.1.4. Technological Advancements (AI, IoT, Smart Technologies)

2.2. Market Restraints

2.2.1. High Initial Investment for WTaaS Providers

2.2.2. Consumer Skepticism and Contractual Lock-ins

2.2.3. Competition from Alternative Water Sources (Desalination, Rainwater Harvesting)

2.3. Market Opportunities

2.3.1. Growth in Water Reuse and Circular Economy Initiatives

2.3.2. Public-Private Partnerships (PPPs)

2.3.3. Demand for Advanced Treatment of Emerging Contaminants (PFAS)

3. Market Segmentation Analysis

3.1. By Service Type

3.1.1. Operation & Maintenance (O&M) Services

3.1.2. Design & Engineering Services

3.1.3. Water & Wastewater Treatment Services

3.1.4. Chemicals-as-a-Service (CaaS) / Managed Chemical Services

3.1.5. Build-Own-Operate-Transfer (BOOT) / Full-Outsourcing

3.2. By Treatment Technology

3.2.1. Membrane Filtration (RO, UF, NF, MF)

3.2.2. Activated Sludge & Biological Treatment

3.2.3. Clarification & Coagulation

3.2.4. Disinfection

3.2.5. Ion Exchange & Demineralization

3.2.6. Filtration & Media

3.2.7. Sludge Treatment & Management

3.3. By End-User Industry

3.3.1. Industrial

3.3.2. Municipal

3.4. By Application

3.4.1. Wastewater Treatment & Recycling

3.4.2. Process Water Treatment

3.4.3. Zero Liquid Discharge (ZLD)

3.4.4. Boiler Water & Cooling Water Treatment

3.4.5. Effluent Treatment & Compliance Management

3.5. By Contract/Pricing Model

3.5.1. Subscription-based

3.5.2. Performance-based Contracts

3.5.3. Fixed-price Contracts

3.5.4. Pay-per-volume / Consumption-based

4. Recent Developments and Industry Landscape (2024–2025)

4.1. Strategic Mergers and Acquisitions

4.1.1. Xylem-Evoqua Merger (2023) and its Impact on Services

4.1.2. Grundfos' Acquisition of Newterra (June 2025)

4.1.3. Veolia's Full Ownership of Water Technologies and Solutions (May 2025)

4.2. Innovative Projects and Collaborations

4.2.1. Da Tang Industrial Park's MLD Plant (October 2024)

4.2.2. SUEZ-Seabex Partnership on Biochar (July 2025)

4.2.3. Veolia's Treated Wastewater Reuse Project in Argelès-sur-Mer (July 2025)

4.3. Regulatory and Institutional Reports

4.3.1. ASCE 2025 Report Card and U.S. Infrastructure Needs

4.3.2. EU's Revised Urban Wastewater Treatment Directive (January 2025)

4.3.3. U.S. Bipartisan Infrastructure Law and PFAS Regulations

5. Country Analysis and Outlook

5.1. United States: WTaaS Expansion Fueled by Infrastructure Funding and PFAS Regulations

5.1.1. Key Regulatory Drivers and Government Initiatives

5.1.2. Market Dynamics and Corporate Initiatives

5.1.3. Key Applications and Growth Opportunities

5.2. China: Service-Based Models Drive Sponge City Water Infrastructure

5.2.1. Government Programs (Sponge City Program, 14th Five-Year Plan)

5.2.2. Industrial and Municipal WTaaS Adoption

5.2.3. Case Studies and Future Outlook

5.3. India: Government Programs and Technology Partnerships Expand WTaaS Adoption

5.3.1. Impact of Jal Jeevan Mission and Other National Programs

5.3.2. Local and International Technology Partnerships

5.3.3. Market Challenges and Growth Trajectory

5.4. Germany: Stricter EU Standards and Digitalization Boost WTaaS Demand

5.4.1. Influence of EU Urban Wastewater Treatment Directive

5.4.2. Integration of Digital Solutions and Smart Technologies

5.4.3. Prominent Players and Regional Collaborations

5.5. Singapore: Flood Resilience and Compliance Drive WTaaS Implementation

5.5.1. Government Initiatives and Strategic Investments

5.5.2. Regulatory Frameworks and WTaaS Opportunities

5.5.3. Technological Leadership and Case Studies

5.6. Saudi Arabia: PPP Projects and Advanced Technologies Drive WTaaS Growth

5.6.1. Role of Vision 2030 and Water Security Plans

5.6.2. Dominance of RO and Membrane Technologies

5.6.3. Key SWPC Projects and Future Outlook

5.7. Analysis of Other Key Countries (UK, France, Japan, Brazil, etc.)

6. Market Size Outlook by Region (2025-2034)

6.1. North America

6.1.1. Market Size (2025–2034)

6.1.2. Key Drivers and Trends

6.2. Europe

6.2.1. Market Size (2025–2034)

6.2.2. Key Drivers and Trends

6.3. Asia Pacific

6.3.1. Market Size (2025–2034)

6.3.2. Key Drivers and Trends

6.4. South America

6.4.1. Market Size (2025–2034)

6.4.2. Key Drivers and Trends

6.5. Middle East and Africa

6.5.1. Market Size (2025–2034)

6.5.2. Key Drivers and Trends

7. Company Profiles: Leading Players

7.1. Veolia Water Technologies

7.1.1. Company Overview

7.1.2. WTaaS Offerings and Strategic Focus

7.1.3. Recent Developments and Market Position

7.2. SUEZ

7.2.1. Company Overview

7.2.2. WTaaS Portfolio and Technological Strengths

7.2.3. Recent Developments and Strategic Partnerships

7.3. Xylem Inc.

7.3.1. Company Overview

7.3.2. Integrated Solutions and Digital Platforms

7.3.3. Impact of Evoqua Acquisition and Future Strategy

7.4. DuPont Water Solutions

7.4.1. Company Overview

7.4.2. Advanced Membrane Technology and R&D Focus

7.4.3. Role in Circular Water Management

7.5. Pentair

7.5.1. Company Overview

7.5.2. WTaaS Innovation in Residential and Commercial Sectors

7.5.3. Sustainability Initiatives and Service Models

7.6. Fluence Corporation

7.6.1. Company Overview

7.6.2. Focus on Decentralized and Smart-Packaged Solutions

7.6.3. Key Technologies (MABR) and Niche Markets

7.7. Other Key Players

7.7.1. Evoqua Water Technologies

7.7.2. Aquatech International

7.7.3. Kubota Corporation

7.7.4. Toray Industries, Inc.

7.7.5. VA Tech Wabag Ltd.

7.7.6. Kurita Water Industries Ltd.

7.7.7. H2O GmbH

7.7.8. Thermax Limited

8. Research Methodology

8.1. Research Objectives

8.2. Market Research Approach

8.3. Data Sources and Validation

8.4. Assumptions and Limitations