High-Performance Coatings Driven by Industrialization, Sustainability, and Rapid-Cure Technologies

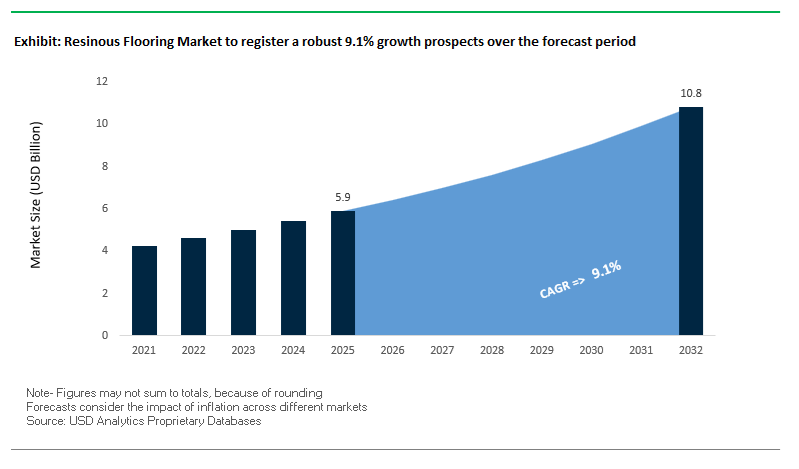

The global Resinous Flooring Market is undergoing a structural transformation driven by accelerated industrialization, stringent hygiene requirements, and the growing need for high-durability flooring systems across commercial and industrial environments. The market was valued at $5.9 billion in 2025 and is projected to reach $10.9 billion by 2032, expanding at a robust CAGR of 9.1% during 2025–2032. This strong growth trajectory is underpinned by increasing adoption in sectors such as pharmaceuticals, food processing, automotive manufacturing, logistics, and electronics, where performance attributes like chemical resistance, seamless finish, and rapid curing are critical.

A key structural shift shaping the market is the transition from traditional flooring materials toward high-performance resin systems such as epoxy, polyurethane (PU), and methyl methacrylate (MMA). These materials offer superior lifecycle cost efficiency, reduced maintenance requirements, and enhanced safety compliance, making them highly attractive for facility operators. Additionally, the surge in green building certifications and low-VOC construction materials is driving innovation in environmentally compliant resin flooring solutions. Manufacturers are increasingly focusing on low-emission, UV-resistant, and energy-efficient flooring technologies to align with global sustainability mandates.

Another defining trend is the increasing demand for fast-curing flooring systems that minimize operational downtime. Industries such as logistics and healthcare are prioritizing flooring systems that allow rapid installation and quick return-to-service, thereby improving productivity and reducing revenue losses. Simultaneously, the expansion of EV battery manufacturing, semiconductor fabs, and data centers is creating a new demand layer for specialized conductive and anti-static flooring systems, reinforcing the strategic importance of resinous flooring in advanced industrial ecosystems.

Market Analysis: Strategic Product Innovation, Capacity Expansion, and M&A Activity Reshaping Competitive Dynamics

The resinous flooring market is currently witnessing a wave of technological innovation, strategic acquisitions, and capacity expansion initiatives, signaling intensified competition and long-term growth positioning among key players. In June 2025, Sherwin-Williams High Performance Flooring introduced its Accelera One technology, which received the 2025 Concrete Contractor Top Products Award. This next-generation urethane grout and topcoat significantly enhances application speed and chemical durability, addressing the growing industry need for rapid installation and high-performance coatings in high-traffic environments.

Similarly, Stonhard’s launch of Stonkote ESD in June 2025 marked a breakthrough in conductive flooring systems. By eliminating the need for a separate conductive primer while achieving resistance levels below 1.0×10⁶ ohms, the product directly targets high-growth sectors such as EV battery plants, semiconductor manufacturing, and data centers, where electrostatic discharge control is mission-critical.

From a strategic expansion standpoint, Sika AG’s acquisition of Finja (February 2026) and planned acquisition of Akkim in 2026 reflect a clear push toward regional manufacturing hubs in Scandinavia and Türkiye. These moves align with Sika’s “Strategy 2028,” focusing on strengthening its position in industrial flooring and construction chemicals while optimizing supply chains. Complementing this, Sika announced plans to commission five new manufacturing plants across the United States, Argentina, Colombia, Bangladesh, and Tanzania in 2026, highlighting a broader trend of production localization and cost optimization.

Capacity expansion remains another critical growth lever. BASF’s October 2025 expansion in Türkiye enhances supply capabilities for construction dispersions across the Middle East and Africa, while its Shanghai facility capacity increase (from 8,000 to 18,800 metric tons) strengthens the supply of polyurethane resins essential for industrial flooring applications in Asia. These developments underscore the increasing importance of regional demand clusters and supply chain resilience in the global market.

In parallel, product innovation is increasingly aligned with aesthetic customization and sustainability. Flowcrete’s July 2025 city-inspired decorative resin series, including low-emission variants, reflects growing demand for design-oriented yet environmentally compliant flooring systems in commercial real estate and institutional spaces.

At the strategic level, AkzoNobel’s proposed merger with Axalta Coating Systems (February 2026) represents a significant consolidation move aimed at creating a dominant entity in industrial coatings and resinous flooring. This merger is expected to combine complementary capabilities in liquid, powder, and specialized flooring systems, particularly targeting logistics and automotive sectors. Additionally, Hempel’s 2026 strategy, backed by record free cash flow of €259 million, emphasizes expansion into energy-sector flooring applications, including offshore substations and hydrogen infrastructure, signaling diversification into high-growth, high-specification segments.

Market Trend: Food Safety Modernization Driving Impermeable and Thermally Resilient Resinous Flooring Systems

The resinous flooring market is experiencing a surge in demand from the food and beverage sector as regulatory scrutiny intensifies following the implementation of the FDA Modernization Act 2.0. While primarily focused on pharmaceutical development, the legislation has triggered broader audit-readiness initiatives across food processing facilities, with a strong emphasis on contamination prevention and traceability.

A critical requirement emerging in 2026 is total microbial exclusion. Flooring systems are now engineered to achieve ultra-low water absorption rates below 0.01% under ASTM D570 testing, ensuring that moisture cannot penetrate the substrate and support bacterial growth. This level of impermeability is becoming essential for high-speed processing environments where hygiene standards are continuously monitored.

Thermal performance is equally important. Modern resinous flooring systems, particularly epoxy and polyurethane-based formulations, are designed to withstand daily exposure to high-pressure washdowns at temperatures up to 85°C without delamination or structural degradation. This capability supports aggressive sanitation protocols required to meet enhanced regulatory expectations and avoid penalties associated with contamination events.

These performance benchmarks are driving the replacement of conventional flooring materials with high-performance resinous systems across meat processing, dairy production, and packaged food manufacturing facilities. As food safety standards continue to evolve, impermeable and thermally resistant flooring is becoming a baseline specification in industrial plant design.

Market Trend: EU CPR 2025 Enforcement Elevating Fire Safety and Transparency Requirements in Commercial Flooring

The revision and enforcement of the EU Construction Products Regulation, implemented under the oversight of the European Commission, is transforming compliance requirements for resinous flooring systems across Europe. As of January 2026, all construction materials must meet updated fire safety classifications and provide enhanced transparency through digital documentation.

Fire performance classification under EN 13501-1 has become a critical differentiator. High-traffic commercial and public infrastructure projects are increasingly mandating a minimum Bfl-s1 rating, which indicates very limited contribution to fire and minimal smoke production. This requirement is pushing manufacturers to reformulate resin systems with improved fire-retardant properties while maintaining mechanical durability and chemical resistance.

In parallel, the introduction of Digital Product Passports represents a significant shift toward lifecycle transparency. Starting January 8, 2026, resinous flooring manufacturers must provide detailed digital records outlining product composition, global warming potential, and fire performance metrics. This requirement is enhancing traceability and enabling specifiers to make informed decisions based on environmental and safety data.

The combined impact of fire classification and digital transparency is reshaping the competitive landscape. Manufacturers that cannot meet Bfl-s1 standards or provide compliant digital documentation are increasingly excluded from government and large-scale commercial projects, accelerating the transition toward high-performance, certified resinous flooring systems.

Market Opportunity: Polyaspartic Flooring Systems Enabling Rapid Installation in Cold-Climate Logistics and Storage Infrastructure

The expansion of cold storage infrastructure and Arctic logistics networks is creating a strong growth opportunity for polyaspartic resinous flooring systems. These coatings are uniquely suited to environments where conventional epoxy systems fail due to low-temperature curing limitations.

Polyaspartic formulations developed for 2026 applications can achieve full mechanical cure at temperatures as low as −29°C. This capability allows construction and maintenance activities to continue uninterrupted in extreme climates, eliminating seasonal delays that have historically impacted project timelines in high-latitude regions.

Speed of installation is a key advantage. In modern logistics centers, polyaspartic flooring systems enable return-to-service within six to eight hours for heavy equipment such as forklifts and automated guided vehicles. This is a significant improvement over traditional cold-weather epoxy systems, which may require several days to achieve full cure. The reduced downtime is particularly valuable in 24/7 warehouse operations where operational continuity is critical.

These performance characteristics are positioning polyaspartic coatings as a preferred solution for cold chain logistics, refrigerated warehouses, and distribution centers supporting e-commerce and food supply chains.

Market Opportunity: ESD Epoxy Flooring Supporting Lithium-Ion Battery Gigafactory Expansion Under U.S. Manufacturing Incentives

The rapid growth of lithium-ion battery manufacturing in the United States, driven by policy frameworks such as the Inflation Reduction Act, is creating a high-value opportunity for electrostatic dissipative epoxy flooring systems. Battery gigafactories require specialized flooring solutions to protect sensitive electronic components and mitigate electrostatic discharge risks during cell assembly.

Advanced ESD epoxy systems are engineered to maintain surface resistance within the range of 1.0×10⁶ to 1.0×10⁹ ohms, even under heavy mechanical loads from automated guided vehicles and robotic systems. This ensures consistent electrostatic control across large-scale manufacturing environments.

Chemical resistance is another critical requirement. Flooring systems used in battery production must withstand prolonged exposure to aggressive solvents such as N-Methyl-2-pyrrolidone. Modern ESD resin formulations provide resistance for up to 14 days, significantly outperforming conventional industrial coatings that degrade within 24 hours under similar conditions.

Structural performance is also being enhanced to meet evolving manufacturing demands. As gigafactories scale production of high-energy-density battery cells, flooring systems are required to support compressive loads exceeding 10,000 psi. This ensures long-term durability under heavy equipment and multi-ton storage systems.

The convergence of regulatory incentives, rapid capacity expansion, and stringent performance requirements is positioning ESD epoxy flooring as a critical enabling technology in the next generation of battery manufacturing infrastructure.

Resinous Flooring Market Share and Segmentation Insights: Self-Smoothing Systems Lead and Direct Sales Strengthen Market Control

By System Thickness: Self-Smoothing Flooring Systems Dominate with Seamless Performance and Cost Efficiency

The self-smoothing (2–6 mm) segment led the resinous flooring market with a 43.4% share in 2025, driven by its superior seamless finish, hygiene benefits, and balanced performance-to-cost ratio. These systems, typically based on epoxy flooring, polyurethane flooring, and MMA (methyl methacrylate) coatings, create monolithic, joint-free surfaces that are easy to clean and maintain, making them highly suitable for pharmaceutical manufacturing, food processing facilities, hospitals, and commercial retail spaces. A major advantage is their ability to provide adequate thickness for wear resistance, chemical protection, and mechanical durability without the higher labor and material costs associated with heavy-duty trowel-applied screeds. This balance of durability, aesthetics, and installation efficiency positions self-smoothing systems as the preferred choice for modern industrial and commercial flooring solutions, reinforcing their leadership in the global resinous flooring market.

By Sales Channel: Direct Sales Channel Leads with Technical Support and Large-Scale Project Integration

The direct sales segment accounted for a leading 44.8% share of the resinous flooring market in 2025, reflecting the importance of system integrity, technical expertise, and large project coordination. Resinous flooring solutions require multi-layer systems including primers, basecoats, topcoats, and aggregate broadcasts, which must be precisely specified and applied for optimal performance. Manufacturers provide direct technical support, applicator training, and certification programs, ensuring correct installation and long-term durability. Additionally, large-scale end users such as warehouses, manufacturing plants, hospitals, and logistics centers prefer direct procurement to secure bulk pricing, consistent product quality, and comprehensive warranty coverage. This direct engagement also facilitates customized flooring solutions tailored to specific operational requirements, including chemical resistance, slip resistance, and load-bearing capacity. As demand increases for high-performance industrial flooring systems, the direct sales channel continues to play a pivotal role in driving growth and ensuring quality in the resinous flooring market.

Competitive Landscape of the Resinous Flooring Market

PPG Leads Market with Advanced Flooring Systems and AI-Driven Analytics Integration

PPG Industries, Inc. is the undisputed leader in the resinous flooring market, holding 10.5% global market share. The company reported $15.9 billion in net sales in 2025, supported by strong growth in its Performance Coatings segment. In 2026, PPG launched a unified flooring coatings portfolio designed to simplify specification for architects and facility managers. Its integration of the PPG InsightsNav™ analytics platform enables real-time monitoring of coating degradation and maintenance cycles. PPG is also a global leader in 100% solids (zero-VOC) flooring systems, aligning with stringent LEED and WELL standards.

Sika Expands Global Leadership with High-Strength Flooring Systems for Smart Infrastructure

Sika AG is a major force in the resinous flooring market, driven by aggressive global expansion and strong technical expertise. The company has strengthened its presence in Asia-Pacific, particularly through its India operations, targeting high-growth markets. Its latest innovations include high-strength flooring resins with three times the impact resistance of standard epoxy, designed for automated warehouse and smart factory environments. Sika is also focusing on supply chain decarbonization and localized production to mitigate raw material volatility, reinforcing its leadership in infrastructure applications.

RPM (Stonhard) Leads Turnkey Flooring Solutions with Fast-Curing and Bio-Based Systems

RPM International Inc., through its Stonhard brand, is a leader in the resinous flooring market, particularly in direct-to-customer installations. The company reported strong financial performance in 2026, supported by its Margin Achievement Plan (MAP). Stonhard’s latest innovations include bio-based flooring chemistries and ultra-fast-curing polyaspartic systems, enabling full return-to-service in under 24 hours. Its Stonclad® and Stonshield® product lines remain industry benchmarks for heavy-duty industrial environments, now enhanced with Environmental Product Declarations (EPDs) to meet sustainability targets.

Sherwin-Williams Captures Renovation Market with Hygienic and High-Durability Flooring Systems

The Sherwin-Williams Company is a key player in the resinous flooring market, leveraging its strong North American presence. The company is capitalizing on the growing renovation and retrofit segment, which is outpacing new construction. Its FasTop® polyurethane concrete systems are widely used in the food and beverage industry, offering resistance to thermal shock and aggressive cleaning processes. Sherwin-Williams is also a leader in hygienic flooring, integrating antimicrobial additives for long-term protection.

BASF Strengthens Market with Advanced Resin Technologies and Global Production Expansion

BASF SE plays a critical role in the resinous flooring market, leveraging its vertically integrated chemical production capabilities. The company has expanded production capacity in India and South Africa to meet rising demand for construction chemicals. Its Acronal® and Basonal® technologies enable low-VOC, stain-resistant, and scuff-resistant flooring systems, supporting improved indoor air quality. BASF’s control over key raw materials such as MDI and epoxy resins ensures price stability and consistent supply, reinforcing its leadership in advanced resin solutions.

Saint-Gobain (Fosroc) Expands Market Presence with Integrated Construction Chemical Solutions

Saint-Gobain has emerged as a major contender in the resinous flooring market following its acquisition of Fosroc. Its Nitoflor® series provides high-performance, solvent-free epoxy flooring systems widely used in industrial and institutional applications. The acquisition has strengthened Saint-Gobain’s presence in Asia-Pacific and the Middle East, regions experiencing rapid growth in flooring demand. With strong R&D capabilities and a global distribution network, the company is well-positioned to scale its solutions across international markets.

China Driving High-Spec Resinous Flooring Demand Through Quality Housing and VOC Compliance

China has rapidly evolved into a high-specification leader in the resinous flooring market, transitioning from volume-based production to premium, performance-driven applications. The enforcement of GB 18584-2024 standards (effective July 2025) has imposed stringent VOC emission limits, accelerating the shift from solvent-borne epoxy systems to aqueous polyurethane dispersions (PUDs) and other eco-friendly flooring solutions.

Technological innovation is reshaping the market, with the development of magnesium-oxide (MgO) core resinous flooring systems offering superior load-bearing strength and fire resistance, aligning with modern high-rise safety requirements. Massive infrastructure investments, particularly in Guangdong’s multi-trillion project pipeline, are fueling demand for high-build industrial epoxy flooring across manufacturing zones. China is also integrating digital tools for real-time visualization of flooring patterns, streamlining project planning cycles. Additionally, the adoption of UV-stable MMA flooring systems in high-speed rail stations and the shift toward bio-polymer flooring cores for sustainability highlight China’s leadership in next-generation flooring technologies.

India Emerging as a High-Growth Hub for Industrial and Pharmaceutical Resinous Flooring

India is one of the fastest-growing markets in the global resinous flooring industry, supported by large-scale infrastructure development and expanding industrial corridors. Mega projects such as the Mumbai Trans Harbor Link and Navi Mumbai International Airport are driving strong demand for heavy-duty epoxy and polyurethane flooring systems.

The pharmaceutical and biotech sectors are key growth drivers, particularly in Hyderabad and Pune, where strict hygiene requirements are boosting demand for antimicrobial and electrostatic dissipative (ESD) flooring solutions. Technological advancements include the adoption of fast-curing polyaspartic systems, enabling rapid installation and minimal operational downtime. The expansion of e-commerce logistics hubs is further increasing the need for high-abrasion-resistant flooring systems. Additionally, the growing emphasis on sustainability is encouraging the adoption of low-VOC, LEED-compliant resinous flooring solutions, supported by localized production of resin components.

United States Leading PFAS-Free Innovation and Reshoring-Driven Flooring Demand

The United States resinous flooring market is undergoing significant transformation due to regulatory changes and reshoring of advanced manufacturing. The EPA’s PFAS-free mandates (2025–2026) are driving a shift toward MDI-based polyurethane systems and polyaspartic coatings, replacing traditional fluoropolymer-modified resins.

The expansion of the “Battery Belt” is generating strong demand for chemical-resistant flooring systems in lithium-ion battery production facilities. Technological innovation is also evident in the development of lightweight resin-encapsulated flooring systems, improving installation efficiency in residential and commercial projects. Infrastructure investments under federal programs are boosting demand for epoxy and moisture-cured urethane coatings in bridges and tunnels. Additionally, rising residential construction is increasing the popularity of decorative epoxy flooring solutions, particularly for garages and basements, while new product lines are blending aesthetic appeal with industrial-grade durability.

Germany Advancing Bio-Based Resin Flooring with Industry 4.0 and Circular Economy Integration

Germany continues to lead the European resinous flooring market through its focus on sustainability, digitalization, and regulatory compliance. The implementation of EU Regulation 923/2023, banning lead-based stabilizers from 2026, is accelerating the adoption of calcium-zinc-based resin systems across the market.

Technological advancements such as AI-driven resin batching systems are reducing material waste and improving formulation efficiency. Germany also dominates in hygienic polyurethane flooring systems, widely used in industrial environments requiring resistance to thermal shock and heavy loads. Sustainability remains a core focus, with manufacturers introducing low-VOC epoxy hardeners targeting energy-efficient buildings. The integration of digital twin monitoring systems is enhancing lifecycle management by tracking wear and performance in real time. These innovations, combined with expanded aqueous coating technologies, are reinforcing Germany’s position as a global leader in advanced resinous flooring solutions.

Saudi Arabia’s Mega Projects Driving Demand for High-Performance Resinous Flooring Solutions

Saudi Arabia is emerging as a high-value market in the resinous flooring sector, fueled by ambitious infrastructure projects under Vision 2030. Mega developments such as NEOM and “The Line” are generating substantial demand for fusion-bonded epoxy (FBE) and specialized resinous flooring systems for underground infrastructure and metro networks.

Government regulations under the Saudi Building Code (SBC 601) are promoting high-performance, energy-efficient flooring systems, while the rapidly expanding hospitality sector is driving demand for luxury resinous terrazzo flooring in hotels and resorts. Technological innovations such as solar-reflective resin coatings are enhancing outdoor usability by reducing surface temperatures. The oil and gas sector remains a key application area, utilizing phenolic epoxy flooring systems for chemical resistance. Additionally, increasing competition and local production are strengthening supply chain capabilities and supporting market expansion.

South Korea Leading Semiconductor-Grade Resinous Flooring and Cleanroom Applications

South Korea holds a dominant position in high-precision resinous flooring systems, particularly for semiconductor and electronics manufacturing. The development of photo-curable polyimide-modified resins is enabling advanced applications in flexible OLED production, requiring extreme chemical and thermal resistance.

The country is a global leader in cleanroom-grade flooring solutions, where ultra-low outgassing properties are critical for semiconductor fabrication. Investments in R&D are driving the development of fast-curing antimicrobial resin systems for biotech and pharmaceutical industries. Regulatory frameworks such as K-REACH 2025 are ensuring stricter safety and environmental compliance. Additionally, product innovations in slip-resistant and aesthetic flooring systems are expanding applications into premium residential developments, highlighting South Korea’s versatility across industrial and consumer markets.

Vietnam Emerging as a Strategic Industrial Hub for Resinous Flooring in Southeast Asia

Vietnam is rapidly gaining importance in the global resinous flooring market, driven by strong foreign direct investment and its growing role in global manufacturing supply chains. The country’s high ranking in the Asia Manufacturing Attractiveness Index is fueling demand for high-performance industrial flooring systems in export-oriented facilities.

Technological advancements include the adoption of UV-LED curing technologies, enabling faster installation and energy-efficient operations. Regulatory updates such as QCVN 19:2024 are accelerating the transition toward low-VOC, waterborne flooring systems. Key applications include marine-grade resin flooring systems in industrial parks and acid-resistant linings in food-processing industries. Despite rising raw material costs, Vietnam’s expanding industrial base and increasing technical capabilities are positioning it as a critical growth market in Southeast Asia.

Resinous Flooring Market Report Scope

Resinous Flooring Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.9 Billion

|

|

Market Size (2032)

|

$10.9 Billion

|

|

Market Growth Rate

|

9.1%

|

|

Segments

|

By Resin (Epoxy, Polyurethane, Polyaspartic, Polymethyl Methacrylate, Vinyl Ester, Hybrid Systems), By Formulation (Solvent-free, Water-borne, Solvent-borne), By System Thickness (Thin-Film Coatings, Self-Smoothing, Heavy-Duty Trowel-Applied Screeds, Broadcast Systems), By End-Use Industry (Industrial and Manufacturing, Commercial, Institutional, Residential, Transportation and Infrastructure), By Functional Property (General Purpose, Chemical and Acid Resistant, Anti-slip, Anti-static, Antimicrobial, Thermal Shock Resistant), By Project Type (New Construction, Renovation and Retrofit), By Sales Channel (Direct Sales, Specialty Construction Chemical Distributors, E-commerce)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sika AG, RPM International Inc., BASF SE, The Sherwin-Williams Company, PPG Industries, Inc., Akzo Nobel N.V., Mapei S.p.A., Fosroc International Ltd., Saint-Gobain, Huntsman International LLC, Kansai Paint Co., Ltd., Nippon Paint Holdings Co., Ltd., Dex-O-Tex, Resdev Limited, Duraamen Engineered Products Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Resinous Flooring Market Segmentation

By Resin

- Epoxy

- Polyurethane

- Polyaspartic

- Polymethyl Methacrylate

- Vinyl Ester

- Hybrid Systems

By Formulation

- Solvent-free

- Water-borne

- Solvent-borne

By System Thickness

- Thin-Film Coatings

- Self-Smoothing

- Heavy-Duty Trowel-Applied Screeds

- Broadcast Systems

By End-Use Industry

- Industrial and Manufacturing

- Commercial

- Institutional

- Residential

- Transportation and Infrastructure

By Functional Property

- General Purpose

- Chemical and Acid Resistant

- Anti-slip

- Anti-static

- Antimicrobial

- Thermal Shock Resistant

By Project Type

- New Construction

- Renovation and Retrofit

By Sales Channel

- Direct Sales

- Specialty Construction Chemical Distributors

- E-commerce

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Resinous Flooring Industry

- Sika AG

- RPM International Inc.

- BASF SE

- The Sherwin-Williams Company

- PPG Industries, Inc.

- Akzo Nobel N.V.

- Mapei S.p.A.

- Fosroc International Ltd.

- Saint-Gobain

- Huntsman International LLC

- Kansai Paint Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

- Dex-O-Tex

- Resdev Limited

- Duraamen Engineered Products Inc.

*- List not Exhaustive