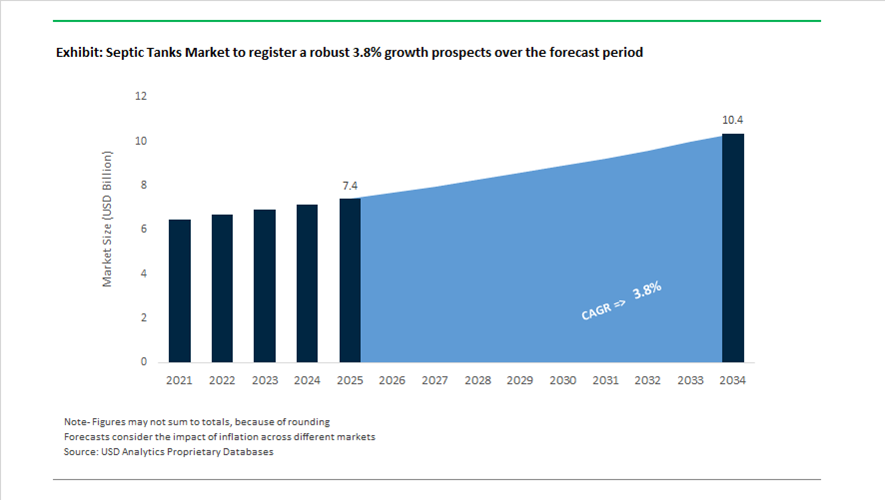

Septic Tanks Market Valuation 2025–2034: $7.4 Billion to $10.4 Billion at 3.8% CAGR Anchored by Decentralized Wastewater and Circular Materials

The global septic tanks market is valued at $7.4 billion in 2025 and is projected to reach $10.4 billion by 2034, expanding at a CAGR of 3.8%. Market expansion is underpinned by increasing adoption of decentralized wastewater treatment systems, stricter effluent discharge regulations, rising rural housing development, and infrastructure upgrades in non-mains sewer regions. Demand is shifting from traditional concrete septic tanks toward lightweight, corrosion-resistant plastic septic tanks manufactured using recycled polyethylene and polypropylene. Growth is particularly visible in regions enforcing nutrient reduction mandates and groundwater protection standards, where advanced onsite wastewater treatment systems are preferred over basic containment solutions.

In October 2024, Advanced Drainage Systems (ADS) completed the acquisition of Orenco Systems, Inc., integrating advanced decentralized wastewater purification technologies into its Infiltrator Water Technologies division. Orenco’s treatment solutions are engineered for high-level nitrogen and phosphorus removal, positioning ADS to compete in environmentally sensitive markets with stringent discharge requirements. In the same year, Kingspan introduced 12 new Lower Embodied Carbon products, including wastewater treatment innovations designed to reduce lifecycle emissions across onsite systems. Between 2024 and 2025, GRAF expanded its high-efficiency product line with the one2cleanXtra packaged wastewater treatment system, targeting small-to-medium residential and commercial developments in areas lacking centralized sewer connectivity.

Throughout 2025, consolidation and sustainability initiatives accelerated competitive repositioning. In March 2025, Infiltrator Water Technologies partnered with Rainwater Management Solutions to integrate commercial-scale rainwater harvesting with decentralized wastewater treatment, aligning with green building certification standards and water reuse strategies. In early 2025, ADS broke ground on a major recycling facility expansion in Cordele, Georgia, enhancing capacity to process recycled resins used in plastic septic tank manufacturing. In July 2025, Wavin launched AquaCell NG, an infiltration and attenuation system manufactured from 100% recycled polypropylene. The design improves storage density fourfold and reduces installation time by three times, supporting cost-efficient stormwater and septic integration. Wavin also confirmed achieving 90% product recyclability by the end of 2025, reinforcing circular economy compliance across its drainage and septic portfolios.

Service integration and safety innovation further defined market activity. In July 2025, Premier Tech acquired RMS Waste Disposal in the United Kingdom, strengthening septic maintenance and tankering services across the UK and Ireland. In August 2025, Premier Tech expanded its U.S. footprint by acquiring Karr’s Septic Service in Iowa, shifting from a pure manufacturing model toward turnkey septic system support, diagnostics, and lifecycle maintenance services. In November 2025, Entegris opened its Center of Excellence in Colorado, where advanced liquid filtration technologies are being adapted for high-purity wastewater treatment applications in industrial septic environments. In February 2026, Infiltrator launched the Guardian safety gate for septic tank riser systems, engineered with a spring-loaded latch requiring 50 pounds of force to open, addressing safety compliance and liability concerns in residential installations. These developments illustrate how the septic tanks market is transitioning toward integrated wastewater solutions, recycled material adoption, advanced treatment performance, and full lifecycle service models through 2034.

Regulatory-Driven Trends and Scalable Opportunities Transforming the Septic Tanks Market

Performance-Based Nitrogen Removal Mandates Reshaping System Design and Replacement Cycles

The septic tanks market is undergoing a decisive regulatory shift as state and local governments move from prescriptive installation rules toward performance-based nutrient discharge standards. This transition is directly accelerating the replacement of legacy gravity-fed septic tanks with Advanced Treatment Units and Innovative or Alternative systems capable of delivering verified nitrogen reduction. In Massachusetts, the revised Title 5 framework implemented by the Massachusetts Department of Environmental Protection has fundamentally altered upgrade economics in nitrogen-sensitive watersheds. Homeowners in designated Natural Resource Areas across Cape Cod are now required to install Best Available Nitrogen Reducing Technology within five years unless covered by a municipal Watershed Permit. This requirement has driven a sharp increase in demand for NSF ANSI 245 certified systems, which demonstrate nitrogen reductions exceeding 50% under field conditions.

A similar enforcement-driven demand surge is unfolding in Florida, where nutrient pollution controls have been codified into wastewater permitting. Under Section 403.086 of the Florida Statutes, onsite sewage facilities within Basin Management Action Plan zones must now meet advanced treatment thresholds. The 2025 updates establish a Total Nitrogen limit of 3 mg per liter for reclaimed water in sensitive basins, effectively mandating secondary and tertiary treatment solutions such as sequencing batch reactors and pressurized drip dispersal systems. These rules are transforming septic tanks from low-cost infrastructure into regulated treatment assets, structurally increasing average system value and technical complexity.

Large-Scale Public Funding for Rural Septic Rehabilitation and Environmental Justice

Parallel to regulatory tightening, unprecedented public funding is being mobilized to address failing septic infrastructure as part of environmental justice and public health initiatives. Federal and state programs are prioritizing the replacement of straight pipes, cesspools, and undersized tanks that disproportionately impact rural and low-income communities. In September 2024, the U.S. Environmental Protection Agency announced $49 million in new funding for the Rural Small and Tribal Clean Water Technical Assistance program, specifically to help communities access Bipartisan Infrastructure Law wastewater funding. By May 2025, an additional $30.7 million had been allocated to assist small systems and private well owners in bringing failing septic installations into Clean Water Act compliance.

At the state level, New York’s Septic System Replacement Fund has become a catalyst for market acceleration. Updated in April 2024, the program provides grants of up to $20,000 per household, with counties such as Suffolk layering local funds to raise total support to $30,000 per installation. These subsidies are explicitly tied to nitrogen-reducing technologies, directly underwriting a transition toward pressurized shallow drainfields and advanced treatment units and creating predictable, policy-backed demand for higher-value septic systems.

IoT-Enabled Smart Septic Systems for Professionally Managed Properties

The growing professionalization of short-term rentals and hospitality portfolios is creating a differentiated opportunity for IoT-integrated septic tanks that enable remote monitoring and proactive maintenance. In high-occupancy properties, septic failure carries reputational, financial, and regulatory risk, elevating demand for systems that provide real-time visibility into performance. Smart monitoring platforms such as Septilink, expanded in late 2025, deploy sensors to track pump runtimes, cycle frequency, and sludge accumulation, transmitting alerts directly to mobile dashboards. This allows property managers to identify hydraulic overload from leaking fixtures or abnormal usage patterns before system failure occurs, protecting asset value and guest experience.

Industry data released in December 2025 indicates that smart septic monitoring can materially reduce unnecessary pumping events by shifting maintenance from fixed schedules to condition-based interventions. By triggering service only when sludge levels approach critical thresholds, these platforms lower operating costs while aligning with ESG-oriented property management practices. As institutional ownership of vacation rentals expands, smart septic capability is increasingly specified as a baseline requirement rather than a premium feature.

Modular Cluster Systems for High-Density Rural and Semi-Commercial Development

A second growth opportunity lies in modular cluster wastewater systems designed to serve applications that fall between single-family homes and municipal sewer networks. Restaurants, RV parks, remote resorts, and pocket neighborhoods are increasingly adopting pre-engineered community-scale treatment plants that combine regulatory compliance with rapid deployment. Plug-and-play modular systems, including membrane aerated biofilm reactor platforms, are being specified to minimize on-site civil work and accelerate project timelines. In 2025, manufacturers such as Anua and Cleantech Water reported rising adoption across remote hospitality and light industrial sites, with systems handling flows from 500 to 5,000 gallons per day and allowing incremental capacity expansion.

Integration with water reuse further enhances the value proposition. According to October 2025 projections from Bluefield Research, the U.S. water reuse pipeline is set to drive $47.1 billion in infrastructure investment through 2035. Modular septic providers that deliver purple-pipe-ready systems capable of producing non-potable reuse water for irrigation and process applications are positioned to capture a growing share of this decentralized treatment market.

Septic Tanks Market Share and Segmentation Insights

Concrete Septic Tanks Dominate Market Adoption Due to Durability and Precast Construction Standardization

Concrete septic tanks accounted for 52.80% of the septic tanks market in 2025, making them the most widely installed material type across decentralized wastewater treatment systems. Their dominance is driven by high structural strength, long service life, and resistance to soil pressure and groundwater conditions, which make concrete tanks particularly suitable for residential wastewater management systems. Concrete also supports large tank capacities and stable underground installation, ensuring long-term reliability in rural and suburban environments. A key 2025 industry development is the standardization of precast concrete septic tanks, where manufacturers produce common tank sizes and configurations for faster deployment. Precast manufacturing improves installation efficiency, reduces on-site construction labor, and enhances product consistency, while fiber reinforcement technologies improve crack resistance and structural durability.

Residential Applications Lead Septic Tank Demand as Decentralized Wastewater Systems Expand

Residential use represents the largest application segment in the septic tanks market, accounting for 72.80% of total installations in 2025 due to the widespread reliance on septic systems in areas without centralized sewer infrastructure. Single-family homes in rural, suburban, and developing regions rely on septic tanks for decentralized wastewater treatment and disposal. Demand is supported by ongoing residential construction, property development in non-sewered areas, and regulatory compliance for onsite wastewater management. A major 2025 market driver is the increasing replacement of aging septic systems, many of which were installed 30 to 40 years ago and are approaching the end of their operational lifespan. Replacement projects often involve larger tank capacities, improved treatment efficiency, and nitrogen-reducing septic technologies to meet modern environmental regulations.

Septic Tanks Market Competitive Landscape

The 2026 septic tanks market is driven by decentralized wastewater treatment (DWWT), IoT-enabled monitoring, and modular plug-and-play systems. Demand is rising for PE and FRP tanks, nutrient removal technologies, and effluent reuse solutions aligned with EU and EPA wastewater regulations.

Kingspan accelerates smart decentralized wastewater infrastructure with LEC tank solutions and global capacity expansion

Kingspan Group is strengthening its septic tank market leadership through rapid expansion of advanced wastewater infrastructure solutions. The company reported €9.2 billion revenue in 2025, with its Advnsys division growing 12% and maintaining a 24% higher backlog entering 2026. Manufacturing capacity is expanding across the U.S., Middle East, and Asia to meet rising decentralized treatment demand. Order intake in early 2026 doubled year-over-year, driven by data center and infrastructure projects. The LEC product range introduces low-carbon septic tanks aligned with net-zero construction mandates. Focus on high-performance modular systems supports IoT-integrated wastewater treatment.

ADS drives plastic septic tank adoption with IM-Series innovation and integrated drainage platform expansion

Advanced Drainage Systems, through Infiltrator Water Technologies, is leading material conversion from concrete to advanced plastic septic systems. The $1 billion acquisition of NDS strengthens its integrated drainage and wastewater platform. The company reported $2.4 billion in fiscal 2026 sales, supported by strong performance in the Infiltrator segment. IM-Series injection-molded tanks enable shallow installation and flexibility in high water table environments. Integration of Orenco technology enhances nitrogen-reduction capabilities in advanced treatment systems. Focus on high-efficiency plastic tanks supports regulatory compliance and infrastructure modernization.

GRAF advances SBR-based septic systems with recycled materials and smart IoT monitoring integration

Otto Graf GmbH is transforming the European septic tanks market through SBR technology and circular water management. Its EN 12566-certified systems reduce percolation area requirements by up to 50%, improving land-use efficiency. Nearly 70% of tank production utilizes recycled plastics, supporting sustainability targets. Expansion in the UK and Ireland is driven by regulatory upgrades and grant-supported installations. IoT-enabled sensors enable predictive maintenance and real-time system monitoring. Focus on integrated rainwater and wastewater solutions aligns with the Sponge City concept.

Premier Tech expands global septic solutions with Ecoflo biofilter and localized manufacturing strategy

Premier Tech Water and Environment is strengthening its global footprint through acquisitions and localized production. Expansion in Spain following the Aquatreat acquisition enhances distribution across Southern Europe. Entry into the U.S. market includes regulatory approvals for Ecoflo Linear Biofilter systems. The Ecoflo® biofilter uses natural coconut husk media, offering passive treatment with up to 15-year lifespan and zero energy consumption. Global rebranding aligns regional operations under a unified market strategy. Focus on sustainable, low-maintenance wastewater solutions supports decentralized treatment adoption.

Fuji Clean pioneers Jokaso decentralized systems with phosphorus removal and municipal-scale deployment

Fuji Clean is advancing decentralized wastewater treatment through its Jokaso technology and compact septic systems. Deployment of CRX units in the UK demonstrates scalability for municipal wastewater replacement. The CRX model enables chemical-free phosphorus removal within a single tank, reducing operational complexity. Participation in U.S. programs supports nitrogen reduction for coastal protection. Systems are designed for resilience in seismic regions, ensuring rapid recovery after disruptions. Focus on small-scale municipal applications supports sustainable rural wastewater management.

Wavin integrates digital drainage and recycled plastic systems to capture emerging market infrastructure demand

Wavin is expanding its septic and drainage solutions through digital engineering and regional partnerships. Collaboration with Supreme Industries strengthens its presence in India and South Asia under the Make in India initiative. Supply chain optimization in Europe enhances delivery efficiency for septic components. AquaCell Next Generation systems utilize 100% recycled materials for sustainable water management integration. BIM-based digital tools enable simulation of septic system performance during design stages. Focus on smart drainage and infiltration systems supports urban wastewater infrastructure development.

United States: Decentralized Infrastructure Modernization and Smart System Adoption

The United States septic tanks industry is being reshaped by a combination of federal infrastructure funding, state-level incentives, and technology-led upgrades aimed at reducing groundwater contamination. Under the Infrastructure Investment and Jobs Act, the Environmental Protection Agency expanded the “Closing America’s Wastewater Access Gap” initiative in 2025, targeting 150 underserved and rural communities where centralized sewerage is not economically viable. This funding focus has accelerated the replacement of aging cesspools with nitrogen-reducing and secondary-treatment septic systems, particularly in environmentally sensitive watersheds. Product innovation has kept pace. Infiltrator Water Technologies introduced its Advanced Enviro-Septic system in 2025, a passive treatment solution that delivers secondary treatment performance without mechanical aerators, significantly lowering lifecycle operating costs and improving adoption in remote locations.

Regulatory alignment and lifestyle-driven demand are reinforcing this trajectory. New York State recapitalized its Septic System Replacement Fund with an additional USD 15 million in 2025, offering grants of up to USD 10,000 per household for compliant system upgrades. At the federal level, SepticSmart Week 2025 coincided with new guidance promoting IoT-enabled float switches and high-level alarms, signaling a gradual shift toward monitored “smart septic” installations. Demand has also expanded beyond residential use. Growth in barndominiums and rural short-term rentals has driven a 20% increase in installations of commercial-grade Aerobic Treatment Units across western states, while coastal regions are adopting vacuum-pressurized shallow drain fields designed for high water tables and poor percolation soils.

China: Rural Revitalization and Modular Prefabrication at Scale

China’s septic tanks market is being driven by rural infrastructure mandates embedded in the concluding phase of the 14th Five-Year Plan. By 2025, county-level areas were required to achieve a 95% sewage treatment rate, positioning prefabricated fiberglass-reinforced plastic septic tanks as the preferred alternative to concrete systems due to their rapid installation and consistent quality. The National Development and Reform Commission’s 2024–2025 action plan to renovate 45,000 kilometers of rural sewage networks has further accelerated the use of decentralized modular septic units, particularly in mountainous regions such as Yunnan where centralized pipelines are impractical.

Technology differentiation is emerging as a secondary growth lever. Engineering firms in Chengdu have commercialized AI-enabled self-cleaning nanofilters that trigger automated back-flushing through IoT sensors, improving performance in communal septic clusters. Product design has also evolved. Three-compartment high-density polyethylene tanks with integrated anaerobic bio-filters are now widely adopted to comply with Class 1A discharge standards that enable treated effluent reuse for agriculture. Government subsidies under the “Beautiful Village” program cover up to 70% of installation costs for resource-recovery systems that capture biogas for heating, while containerized, solar-powered wastewater units are expanding in Tibet and remote Sichuan to support off-grid sanitation.

India: Policy-Led Scale-Up of Faecal Sludge and Septic Infrastructure

India’s septic tanks industry is transitioning from basic containment toward standardized, serviceable sanitation infrastructure under Swachh Bharat Mission Grameen Phase II. Running through 2025–26, the program has shifted focus from toilet construction to solid and liquid waste management, emphasizing twin-pit systems and septic tanks aligned with ODF Plus criteria. As of September 2025, the Ministry of Jal Shakti reported remediation of 143.7 million tonnes of legacy waste, underscoring the parallel expansion of faecal sludge management assets required to service rural and semi-urban septic installations.

Operational and technological innovation is improving system reliability. The Bhabha Atomic Research Centre piloted radiation-processed water hyacinth bio-filter media in 2025, enhancing nutrient removal in low-cost septic tanks deployed near sensitive river basins. Digitization is also reshaping maintenance. QR-code-based feedback systems and GPS-tracked desludging vehicles have been deployed across 761 districts to enforce scheduled emptying and curb illegal dumping. Financially, over INR 1.4 trillion allocated under the 15th Finance Commission to rural local bodies has strengthened demand for community-scale septic tanks, while the updated National Faecal Sludge and Septage Management Policy mandates standardized septic designs for new semi-urban residential developments from 2025 onward.

European Union (France and Germany): Compliance-Driven Innovation and Hybrid Treatment

The European septic tanks market is being redefined by regulatory tightening under the Revised Urban Wastewater Treatment Directive, effective January 1, 2025. The directive requires all agglomerations of 1,000 population equivalent to implement either formal collection systems or rigorously regulated individual systems, elevating the compliance threshold for septic tanks. Member States must establish national registries by 2027, ensuring tanks are impervious, leak-proof, and subject to routine inspection. This has driven replacement demand in France and Germany, particularly in peri-urban and tourism-heavy regions.

Technology and materials innovation are central to compliance. For larger individual systems, the directive mandates quaternary treatment for micropollutant and pharmaceutical removal, prompting the development of hybrid septic tanks with integrated activated carbon filtration for eco-lodges and premium rural housing. Manufacturers such as Tricel and Kingspan increased the use of recycled composite materials in 2025, cutting manufacturing carbon footprints by approximately 15%. Parallel adoption of nature-based solutions, where advanced septic tanks are paired with constructed wetlands, reflects alignment with the EU Zero Pollution ambition while preserving decentralized wastewater flexibility.

Australia: Environmental Sensitivity and Remote System Intelligence

Australia’s septic tanks industry is shaped by stringent environmental standards and the geographic reality of dispersed populations. The 2025 update to AS/NZS 1547 tightened nitrogen and phosphorus discharge limits, favoring sand filtration septic systems in sensitive catchment areas. These systems are gaining traction where nutrient loading poses risks to groundwater and coastal ecosystems. Technology deployment has accelerated, with Oxy-Septic solutions using solar-powered peripheral pumps to increase dissolved oxygen, reducing land application area requirements and improving suitability for smaller plots.

Remote infrastructure investment is a defining feature. The Western Australian Government has rolled out decentralized smart tanks in Indigenous communities, equipped with satellite-enabled telemetry to alert maintenance teams to high sludge levels. Beyond residential demand, agritourism has emerged as a key application segment. Farms and eco-stays require high-peak-load septic systems capable of handling seasonal visitor surges without performance degradation, supporting demand for robust, monitored, and scalable septic solutions.

Comparative Snapshot: Septic Tanks Industry by Country

Septic Tanks Market County Level Snapshot

|

Region

|

Primary Growth Driver

|

Dominant Technology Focus

|

|

United States

|

Federal funding and smart monitoring

|

Passive secondary treatment, IoT-enabled systems

|

|

China

|

Rural revitalization mandates

|

Prefabricated FRP and HDPE modular tanks

|

|

India

|

Sanitation policy and FSM expansion

|

Standardized septic designs with digital maintenance

|

|

EU (France & Germany)

|

Regulatory compliance

|

Hybrid septic systems and nature-based solutions

|

|

Australia

|

Environmental standards and remoteness

|

Sand filtration and solar-powered smart tanks

|

Septic Tanks Market Report Scope

Septic Tanks Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$7.4 Billion

|

|

Market Size (2034)

|

$10.4 Billion

|

|

Market Growth Rate

|

3.8%

|

|

Segments

|

By Material Type (Concrete Septic Tanks, Fiberglass Reinforced Plastic Septic Tanks, Plastic Septic Tanks, Steel Septic Tanks), By Tank Capacity (Small Capacity, Medium Capacity, Large Capacity), By Treatment Technology (Anaerobic Septic Systems, Aerobic Treatment Units, Hybrid & Advanced Systems, Pressure Distribution Systems), By Application (Residential, Commercial, Industrial, Institutional)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Infiltrator Water Technologies, Orenco Systems Inc., Premier Tech Aqua, Kingspan Group, Tricel Group, Bio-Microbics Inc., WPL Limited, Norweco Inc., Graf Group, Snyder Industries, Fuji Clean USA, Zoeller Company, Oldcastle Infrastructure, Rewatec, Hoot Systems LLC

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Septic Tanks Market Segmentation

By Material Type

- Concrete Septic Tanks

- Fiberglass Reinforced Plastic Septic Tanks

- Plastic Septic Tanks

- Steel Septic Tanks

By Tank Capacity

- Small Capacity

- Medium Capacity

- Large Capacity

By Treatment Technology

- Anaerobic Septic Systems

- Aerobic Treatment Units

- Hybrid & Advanced Systems

- Pressure Distribution Systems

By Application

- Residential

- Commercial

- Industrial

- Institutional

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Septic Tanks Industry

- Infiltrator Water Technologies

- Orenco Systems Inc.

- Premier Tech Aqua

- Kingspan Group

- Tricel Group

- Bio-Microbics Inc.

- WPL Limited

- Norweco Inc.

- Graf Group

- Snyder Industries

- Fuji Clean USA

- Zoeller Company

- Oldcastle Infrastructure

- Rewatec

- Hoot Systems LLC

*- List not Exhaustive