Cooling Tower Water Treatment Systems Market – Strategic Industry Overview

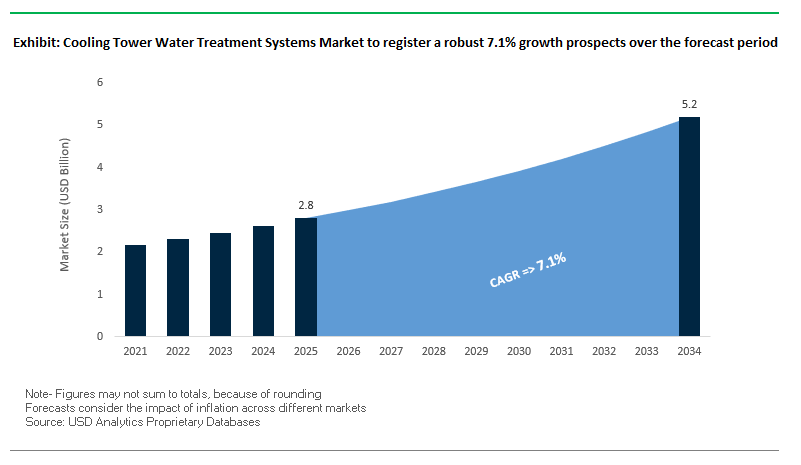

The global cooling tower water treatment systems market is projected to grow from USD 2.8 billion in 2025 to USD 5.2 billion by 2034, registering a robust CAGR of 7.1%. The growth trajectory is driven by intensifying water scarcity concerns, rapid digitalization in industrial operations, and increasingly stringent environmental and public health regulations. For industry professionals, the market offers significant opportunities to capitalize on both regulatory compliance demands and operational efficiency gains.

Key market drivers include advanced solutions for water conservation, with the U.S. Department of Energy noting that increasing cycles of concentration from three to six can reduce cooling tower makeup water needs by 20% and blowdown by 50%. Digitalization is reshaping operational management, as smart monitoring systems such as Nalco Water’s 3D TRASAR™ and Veolia’s Hubgrade enable real-time pH, conductivity, and corrosion rate tracking, delivering predictive maintenance and automated dosing for optimal performance. Additionally, strict Legionella control measures from bodies like the U.S. CDC are pushing adoption of advanced disinfection and non-chemical treatment methods. Technological innovation is also expanding into hybrid solutions and pilot programs aimed at plume water capture and reuse, signaling a broader shift towards circular water economies.

Strategic imperatives for shareholders:

- Invest in digital-first treatment platforms to align with predictive maintenance and Industry 4.0 trends.

- Diversify portfolios with non-chemical and hybrid treatment solutions to capture eco-conscious market segments.

- Target high-growth industries like data centers, driven by AI-related cooling demands.

- Expand regional presence in markets with tightening discharge and pathogen control regulations.

- Pursue M&A for technology acquisition, especially in niche, high-purity water treatment capabilities.

Market Analysis – Growth Dynamics and Recent Developments

The cooling tower water treatment market is entering an innovation-intensive phase where water efficiency, operational intelligence, and environmental compliance converge. Recent corporate activities highlight a clear strategic shift towards integrating high-purity water expertise with cooling system applications. In August 2025, Nalco Water, an Ecolab company, announced its plan to acquire Ovivo’s Electronics Ultra-Pure Water Business. While primarily a high-purity water play, the acquisition strengthens Ecolab’s broader industrial water solutions, particularly in sectors where cooling towers are critical for thermal management.

Digital intelligence is becoming central to competitive differentiation. In April 2024, Nalco Water launched its Premium Cooling Water Program, merging deposit sensing technology with low-phosphorus and non-metal chemistry. The move responds to growing regulatory pressure and customer demand for sustainable, compliant solutions. The company continued the momentum in June 2025 by introducing a direct-to-chip liquid cooling solution for data centers, extending its reach into the rapidly growing AI infrastructure segment while reinforcing its cooling tower management portfolio.

Other major players are also innovating. Veolia’s GenGard™ and Spectrus™ brands deliver corrosion and microbial control, with its patented “Targeted Delivery” biocide technology allowing precise, on-demand release. Kurita Europe is promoting phosphate-free and AOX-free treatments backed by continuous online corrosion monitoring, while SUEZ’s September 2024 trial at EDF’s Bugey nuclear power plant demonstrated cutting-edge plume water recovery capable of producing water 100 times purer than circulating water. These advancements show a clear industry trend towards eco-efficient, high-precision water treatment. Real-world case studies, such as a July 2025 textile mill implementation of smart monitoring that reduced scaling by 95% and cut chemical use by 32%, underscore the tangible ROI of digital water management technologies.

Trends and Opportunities in Cooling Tower Water Treatment Systems Market

Trend 1- Adoption of Smart Chemical Dosing Systems with IoT Monitoring

The cooling tower water treatment systems market is increasingly leveraging smart chemical dosing systems integrated with IoT sensors to enhance operational efficiency and sustainability. These advanced systems continuously monitor water quality parameters, such as pH, conductivity, and corrosion rates, enabling precise and automated chemical delivery that reduces water and chemical consumption. Case studies highlight a 22% reduction in chemical usage and a 30% reduction in blowdown water in hospital cooling systems, reflecting significant cost and environmental benefits. Real-time monitoring also enables predictive maintenance, preventing equipment failure and ensuring optimal energy efficiency. By maintaining water quality within regulatory standards, automated dosing systems support compliance and reduce operational risks, making them a highly attractive solution across industrial, commercial, and municipal cooling tower applications.

Trend 2- Non-Chemical Water Treatment for Legionella Prevention

Public health concerns and stricter biocide regulations are driving the adoption of non-chemical water treatment methods to prevent Legionella in cooling towers. Technologies such as pulsed electric fields, pulsed corona plasma, and ultrasonic systems effectively control microbial growth without relying on chemical biocides. Studies show pulsed corona plasma can achieve a log-reduction of 5.4 against Legionella pneumophila, while ultrasonic cavitation disrupts biofilm formation, limiting bacterial colonization. These non-chemical approaches reduce environmental impact by eliminating harmful biocides and improve operator safety by avoiding the handling and storage of hazardous chemicals. The trend aligns with growing regulatory pressures and sustainability goals across HVAC, industrial, and power generation sectors.

Opportunity 1- Data Center Cooling Tower Upgrades

The rapid growth of hyperscale data centers, driven by AI and cloud computing demands, is creating a significant opportunity for advanced cooling tower water treatment solutions. Medium-sized data centers can consume up to 110 million gallons of water annually, creating pressure for water-efficient and sustainable cooling systems. Industry leaders like Microsoft are implementing zero-water cooling designs, achieving up to an 80% improvement in Water Usage Effectiveness (WUE), and aligning with corporate water-positive goals. Increasing scrutiny from environmental agencies and regulatory bodies such as the 2 billion gallons consumed by Northern Virginia data centers in 2023 further drives adoption of smart, closed-loop water treatment solutions, positioning the cooling tower systems market to support the sustainable expansion of the global data center infrastructure.

Opportunity 2- Green Hydrogen Plant Cooling Systems

The emergence of green hydrogen production is generating a specialized demand for cooling tower water treatment systems capable of supporting high-purity water and efficient heat management. Electrolyzers require ultra-pure water to prevent damage to sensitive components, while the exothermic nature of electrolysis necessitates effective cooling. Research indicates that large volumes of raw water are needed to generate the ultra-pure water required, increasing the demand for multi-stage treatment systems. As green hydrogen facilities scale, advanced water treatment programs that integrate cooling water management, minimize blowdown, and optimize chemical dosing will become critical. The presents a lucrative opportunity for innovative cooling tower water treatment technologies tailored to the unique operational requirements of the renewable energy sector.

Cooling Tower Water Treatment Systems Market Share Insights

Chemical Treatment Remains the Cornerstone of Cooling Tower Management

Chemical treatment dominates the cooling tower water treatment market with 65.4% share in 2025, reflecting its long-standing effectiveness in controlling scale, corrosion, and microbial growth. Traditional chemical approaches, including oxidizing and non-oxidizing biocides, scale inhibitors, and dispersants, continue to be widely adopted across industries for their proven efficacy and flexibility. Despite growing environmental concerns, chemical methods remain essential for high-demand systems like power plants and industrial manufacturing, where precise control of water chemistry is critical to prevent catastrophic downtime, fouling, and corrosion-related losses.

.png)

Automated and Smart Systems Drive Efficiency and Growth

Automated and smart cooling water treatment systems (14.8%) are the fastest-growing segment, leveraging real-time sensors, controllers, and automated dosing pumps to optimize chemical use and system performance. By continuously monitoring pH, conductivity, and ORP, these systems reduce chemical consumption, enhance operational reliability, and minimize human error. The adoption is especially strong in power generation and HVAC sectors, where consistent water quality is critical for energy efficiency, Legionella risk mitigation, and compliance with environmental regulations.

Power Generation and HVAC Lead End-Use Adoption

Power generation (24.6%) is the largest end-use sector, driven by the immense scale of cooling towers in nuclear, fossil, and biomass plants. Ensuring reliable operation under high thermal loads is crucial to prevent efficiency losses and safety risks. HVAC systems (19.8%) form the commercial backbone, servicing hospitals, office complexes, and data centers, with emphasis on Legionella prevention, energy efficiency, and reduced operational costs. Industrial manufacturing and chemical & petrochemical facilities follow, requiring customized treatment programs to protect equipment and maintain continuous production.

Open Circuit Systems Dominate Cooling Tower Configurations

Open circuit cooling towers (70.6%) represent the largest system type, exposing water to air for evaporative cooling. The design increases scaling, fouling, and corrosion risks, necessitating intensive, continuous water treatment programs. Closed circuit systems (24.4%) offer lower maintenance and minimal exposure to the environment, appealing to cost-conscious operators with moderate cooling demands, while hybrid systems provide customized performance solutions for specialized applications requiring a balance between efficiency and cost.

Service Contracts Remain the Preferred Business Model

Service contracts (60.6%) dominate the cooling tower water treatment business model, with third-party providers delivering comprehensive solutions, including chemical supply, monitoring, dosing, and equipment maintenance. The approach ensures regulatory compliance, operational consistency, and access to specialized expertise, particularly valuable in high-stakes sectors like power generation and pharmaceuticals. Direct chemical sales remain relevant for large industrial operators capable of managing their own treatment programs to maintain control over chemical usage and potentially reduce costs.

Country Analysis of the Cooling Tower Water Treatment Systems Market

United States: Smart and Sustainable Cooling Tower Water Treatment

The U.S. cooling tower water treatment systems market is strongly influenced by the Department of Energy’s best management practices, which recommend increasing cycles of concentration, installing side-stream filtration, and adopting alternative water treatment methods like ozonation and ionization to reduce chemical usage. Companies such as Baltimore Aircoil Company are leveraging AI-driven platforms like the Loop™ Platform, which optimizes efficiency, reduces energy and water consumption, and supports predictive maintenance. Technological innovations include hybrid cooling towers capable of wet and dry operation, addressing both water scarcity and energy efficiency. Additionally, there is growing demand for ultraviolet (UV) treatment and advanced biocides to mitigate Legionella and microbial contamination. The Bipartisan Infrastructure Law further accelerates market growth by funding water infrastructure upgrades, driving the adoption of modular and environmentally sustainable cooling tower treatment solutions.

China: Government-Driven Industrial Water Management

China’s market for cooling tower water treatment systems is propelled by the Beautiful China initiative and the Water Ten Plan, which prioritize ecological protection and modernized water infrastructure. The Ministry of Ecology and Environment, along with six other departments, has launched an action plan for 2025–2027 targeting pollution reduction in rivers and lakes, directly impacting demand for industrial cooling tower water treatment solutions. New water resource tax reforms incentivize sustainable water use, including water recycling and treatment in industrial parks. China is also advancing integrated ecological governance systems in key river basins, requiring comprehensive water treatment solutions that include cooling towers. Initiatives promoting wastewater collection and treatment from ports, ships, and industrial facilities further support the market for advanced and sustainable cooling tower systems.

India: Industrialization and Decentralized Cooling Tower Solutions

India’s cooling tower water treatment systems market is witnessing strong growth, fueled by rising industrialization and strict environmental regulations from the Central Pollution Control Board (CPCB). Adoption of advanced oxidation processes (AOPs) and membrane filtration technologies is increasing to improve efficiency and reduce environmental impact. Real-time monitoring and control through IoT-enabled systems and machine learning are emerging trends, enabling continuous data collection, performance optimization, and early contaminant detection. Integrated service packages combining chemical treatment, monitoring, and maintenance are gaining popularity. Decentralized water reuse projects, promoted by initiatives such as the Namami Gange Mission, utilize cooling towers for final treatment and water recycling in smaller cities and rural areas.

Europe (Germany): Intelligent Cooling Tower Systems for Sustainable Industry

Germany’s cooling tower water treatment market is shaped by EU directives on industrial emissions and water quality, which emphasize sustainability and environmental protection. Technological advancements include intelligent controllers like the mxCONTROL 8620, which continuously measures and regulates pH, ORP, and conductivity to prevent scaling and corrosion. Increasing cycles of concentration reduce water consumption, while automated chemical feed systems optimize biocide effectiveness to control pathogens like Legionella. Case studies, such as a pharmaceutical plant in Ireland, demonstrate that tailored cooling tower water treatment programs can lower energy use and CO₂ emissions, highlighting the synergy between energy-efficient operations and sustainable water management.

Saudi Arabia: Vision 2030 Drives Industrial Cooling Tower Growth

Saudi Arabia’s Vision 2030 emphasizes sustainable water management and industrial expansion, supporting a growing market for cooling tower water treatment systems. The National Water Company (NWC) is upgrading reservoirs, pipelines, and distribution networks, incorporating advanced treatment stages for cooling towers. Industrial companies like Saudi ProTech offer comprehensive water solutions to prevent scaling, corrosion, and microbial growth. The market is witnessing demand for energy-efficient desalination integrated with cooling tower systems. Ongoing development of new cities and industrial parks creates opportunities for both temporary and permanent water treatment installations. Technologies such as reverse osmosis (RO) and ultrafiltration (UF) are increasingly used as pre-treatment to enhance cooling tower performance and extend equipment lifespan.

Japan: High-Efficiency Cooling Towers with IoT Integration

Japan’s market is driven by companies like IHI and Kubota, which supply advanced cooling towers for diverse industrial applications, including chemical plants, oil refineries, steel mills, and power generation. Innovations such as white smoke reduction technology and large-capacity cooling towers support energy-efficient operations. Integrated water treatment plants with aerobic membrane separation are commonly combined with cooling tower systems for holistic water management. IoT-based systems like KSIS provide real-time monitoring, predictive maintenance, and operational visualization, optimizing both efficiency and sustainability. Japan’s regulatory emphasis on sustainability encourages circular economy practices and energy recovery from wastewater, driving the adoption of next-generation cooling tower water treatment technologies.

Competitive Landscape – Leaders Shaping the Cooling Tower Water Treatment Market

The competitive environment in cooling tower water treatment systems is characterized by global conglomerates leveraging integrated chemical, digital, and environmental solutions to secure market leadership. Companies are differentiating through proprietary chemistry, smart monitoring platforms, and advanced service models designed for complex industrial and municipal applications.

Nalco Water – Driving Digital and Chemical Synergy in Water Treatment

Nalco Water’s strategic positioning revolves around delivering outcome-based solutions that combine advanced chemistry with automation and predictive analytics. Its flagship 3D TRASAR™ platform automatically adjusts chemical dosing based on real-time system variability, supporting operational uptime and compliance. Recent launches, including the Premium Cooling Water Program and data center cooling solutions, expand its influence in high-growth, water-critical industries. Nalco’s strength lies in its integration of decades of chemical expertise with ECOLAB3D™ analytics and 24/7 remote monitoring, enabling unmatched operational reliability for customers worldwide.

Kurita Water Industries – Eco-Friendly Customization with Digital Precision

Kurita focuses on environmentally responsible water treatment, offering phosphate-free and AOX-free solutions supported by platforms like Kurita Connect 360 for real-time monitoring and intelligent recommendations. The company’s holistic approach integrates chemical treatment with physical and digital solutions, enhanced by its merger with Avista Technologies, a membrane treatment specialist. The synergy enables Kurita to deliver optimized, conservation-focused treatment programs tailored to individual client needs, reinforcing its position as a sustainability leader.

Veolia Environnement – Ecological Transformation Through Integrated Solutions

Veolia’s cooling tower treatment strategy blends patented chemical formulations, equipment, and advanced digital services under its Hydrex™ and Spectrus™ brands. Its “Targeted Delivery” biocides release active agents only when biological activity is detected, improving efficiency and compliance. Veolia’s Hubgrade service optimizes chemical program performance while reducing environmental impact. With a comprehensive suite covering everything from risk assessment to real-time monitoring, Veolia excels at managing complex, regulation-heavy cooling tower systems.

SUEZ (Now Part of Veolia) – Proven Expertise in Water Reuse and Circularity

SUEZ’s legacy in cooling tower water treatment remains a vital part of Veolia’s portfolio. Known for robust water reuse and conservation technologies, SUEZ demonstrated its leadership with the September 2024 Bugey nuclear plant trial, capturing ultra-pure plume water for reuse. Its full-service offerings included chemical, equipment, and microbiological control programs, making it a strong player in meeting stringent environmental and operational standards for industrial clients.

Cooling Tower Water Treatment Systems Market Report Scope

Cooling Tower Water Treatment Systems Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.8 Billion

|

|

Market Size (2034)

|

$5.2 Billion

|

|

Market Growth Rate

|

7.1%

|

|

Segments

|

By Treatment Type/Technology (Chemical Treatment, Physical Treatment, Automated and Smart Systems), By End-Use Industry (Power Generation, HVAC, Industrial Manufacturing, Chemical & Petrochemical, Food & Beverage, Steel, Mining & Metallurgy, Pharmaceuticals, Oil & Gas), By System Type (Open Circuit, Closed Circuit, Hybrid Systems), By Service Mode (Chemical Sales, Service Contracts)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ecolab (Nalco Water), Veolia, SUEZ, Kurita Water Industries, Thermax Limited, Solenis LLC, ChemTreat Inc., DuPont, Kemira Oyj, Babcock & Wilcox Enterprises, Inc., Baltimore Aircoil Company, SPX Technologies, Hydrite Chemical Co., AWT (Advanced Water Treatment), Flow-Tech Systems

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Cooling Tower Water Treatment Systems Market Segmentation

By Treatment Type/Technology

- Chemical Treatment

- Corrosion Inhibitors

- Scale Inhibitors

- Biocides

- Dispersants

- Physical Treatment

- Filtration

- UV Disinfection

- Ozone & Ionization

- Automated and Smart Systems

By End-Use Industry

- Power Generation

- HVAC (Heating, Ventilation, and Air Conditioning)

- Industrial Manufacturing

- Chemical & Petrochemical

- Food & Beverage

- Steel, Mining & Metallurgy

- Pharmaceuticals

- Oil & Gas

By System Type

- Open Circuit

- Closed Circuit

- Hybrid Systems

By Service Mode

- Chemical Sales

- Service Contracts

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Cooling Tower Water Treatment Systems Market

- Ecolab (Nalco Water)

- Veolia

- SUEZ

- Kurita Water Industries

- Thermax Limited

- Solenis LLC

- ChemTreat Inc.

- DuPont

- Kemira Oyj

- Babcock & Wilcox Enterprises, Inc.

- Baltimore Aircoil Company

- SPX Technologies

- Hydrite Chemical Co.

- AWT (Advanced Water Treatment)

- Flow-Tech Systems

* List Not Exhaustive

Research Coverage

This report investigates the Global Cooling Tower Water Treatment Systems Market, delivering comprehensive analysis reviews on growth drivers, innovation trends, and regulatory imperatives shaping the sector between 2025 and 2034. Published by USDAnalytics, the study highlights key breakthroughs such as AI-enabled monitoring platforms, hybrid chemical and non-chemical treatment methods, and advanced plume water capture technologies. The report also examines the impact of digitalization, water scarcity, and stricter Legionella prevention regulations on system design and adoption. By analyzing competitive moves, from Nalco Water’s acquisition of Ovivo’s ultra-pure water business to Veolia’s patented targeted delivery biocides, the report uncovers how industry leaders are aligning portfolios with sustainability and compliance imperatives. With detailed insights into market sizing, end-use dynamics, and regional opportunities, this report is an essential resource for industry professionals, investors, and policymakers seeking a strategic edge in the rapidly evolving cooling tower water treatment systems market.

Scope Includes:

- Segmentation: By Treatment Type (Chemical, Non-Chemical, Automated & Smart Systems), By End-Use (Power Generation, HVAC, Industrial Manufacturing, Chemical & Petrochemical), By System Type (Open Circuit, Closed Circuit, Hybrid), By Business Model (Service Contracts, Direct Sales).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historic Data: 2021 to 2024, and Forecast Data: 2025 to 2034.

- Companies: Profiles and competitive analysis of 15+ leading players including Nalco Water, Kurita, Veolia, SUEZ, and others.

Methodology

The research methodology adopted by USDAnalytics combines primary interviews and secondary research to ensure robust market intelligence. Primary insights were gathered from utilities, cooling tower operators, chemical suppliers, and digital solution providers to validate adoption patterns and regulatory influences. Secondary sources included company reports, government regulations, peer-reviewed studies, and project databases. Market estimates were derived using a triangulated top-down and bottom-up approach, cross-verifying chemical consumption rates, digital system installations, and regional capacity expansions. Forecast models incorporated scenarios such as accelerated data center cooling demand, the rise of green hydrogen plants, and stricter Legionella regulations, ensuring that projections reflect both baseline and high-impact market conditions.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Cooling Tower Water Treatment Systems Market

1. Executive Summary

1.1. Market Highlights

1.2. Strategic Imperatives for Shareholders

1.3. Global Market Snapshot

2. Cooling Tower Water Treatment Systems Market Overview & Outlook (2025–2034)

2.1. Introduction to the Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): USD 2.8 Billion

2.2.2. Forecasted Market Size (2034): USD 5.2 Billion at 7.1% CAGR

2.3. Key Drivers and Market Dynamics

2.3.1. Intensifying Water Scarcity Concerns

2.3.2. Rapid Digitalization in Industrial Operations

2.3.3. Stringent Environmental and Public Health Regulations

3. Market Analysis: Growth Dynamics and Recent Developments

3.1. Overview of Key Strategic Developments

3.2. Corporate Activities and Acquisitions

3.2.1. Nalco Water's Planned Acquisition of Ovivo's Electronics Ultra-Pure Water Business (August 2025)

3.3. Digital Intelligence and Technological Innovation

3.3.1. Nalco Water's Premium Cooling Water Program (April 2024)

3.3.2. Veolia's GenGard™ and Spectrus™ Brands

3.3.3. SUEZ's Plume Water Recovery Trial at EDF's Bugey Plant (September 2024)

3.4. Case Study: Smart Monitoring in a Textile Mill (July 2025)

4. Trends and Opportunities in the Cooling Tower Water Treatment Systems Market

4.1. Trend 1: Adoption of Smart Chemical Dosing Systems with IoT Monitoring

4.1.1. Real-Time Performance and Predictive Maintenance

4.1.2. Cost and Environmental Benefits

4.2. Trend 2: Non-Chemical Water Treatment for Legionella Prevention

4.2.1. Reducing Reliance on Chemical Biocides

4.2.2. Improved Operator Safety and Reduced Environmental Impact

4.3. Opportunity 1: Data Center Cooling Tower Upgrades

4.3.1. Responding to AI and Cloud Computing Demands

4.3.2. Supporting Water-Efficient and Sustainable Goals

4.4. Opportunity 2: Green Hydrogen Plant Cooling Systems

4.4.1. Addressing High-Purity Water Needs for Electrolyzers

4.4.2. Tailored Solutions for the Renewable Energy Sector

5. Cooling Tower Water Treatment Systems Market Share Insights

5.1. By Treatment Type/Technology

5.1.1. Chemical Treatment Remains the Cornerstone

5.1.2. Automated and Smart Systems Drive Growth

5.2. By End-Use Industry

5.2.1. Power Generation and HVAC Lead End-Use Adoption

5.2.2. Industrial Manufacturing, Chemical, and Other Sectors

5.3. By System Type

5.3.1. Open Circuit Systems Dominate Configurations

5.3.2. Closed Circuit and Hybrid Systems

5.4. By Service Mode

5.4.1. Service Contracts Remain the Preferred Business Model

5.4.2. Direct Chemical Sales

6. Country Analysis of the Cooling Tower Water Treatment Systems Market

6.1. United States: Smart and Sustainable Cooling Tower Treatment

6.2. China: Government-Driven Industrial Water Management

6.3. India: Industrialization and Decentralized Cooling Tower Solutions

6.4. Europe (Germany): Intelligent Cooling Tower Systems for Sustainable Industry

6.5. Saudi Arabia: Vision 2030 Drives Industrial Growth

6.6. Japan: High-Efficiency Cooling Towers with IoT Integration

7. Competitive Landscape: Leaders Shaping the Market

Ecolab (Nalco Water)

Veolia

SUEZ

Kurita Water Industries

Thermax Limited

Solenis LLC

ChemTreat Inc.

DuPont

Kemira Oyj

Babcock & Wilcox Enterprises, Inc.

Baltimore Aircoil Company

SPX Technologies

Hydrite Chemical Co.

AWT (Advanced Water Treatment)

Flow-Tech Systems

8. Market Size Outlook by Region (2025–2034)

8.1. North America Market Size Outlook to 2034

8.1.1. By Treatment Type

8.1.2. By End-Use Industry

8.2. Europe Market Size Outlook to 2034

8.2.1. By Treatment Type

8.2.2. By End-Use Industry

8.3. Asia Pacific Market Size Outlook to 2034

8.3.1. By Treatment Type

8.3.2. By End-Use Industry

8.4. South America Market Size Outlook to 2034

8.4.1. By Treatment Type

8.4.2. By End-Use Industry

8.5. Middle East and Africa Market Size Outlook to 2034

8.5.1. By Treatment Type

8.5.2. By End-Use Industry

9. Research Coverage & Methodology

9.1. Report Scope and Focus

9.2. Research Methodology

9.3. Deliverables

10. Appendix

10.1. List of Tables

10.2. List of Figures

10.3. Abbreviations