Strong Growth Driven by Desalination, Industrial Water Reuse, and Energy Efficiency

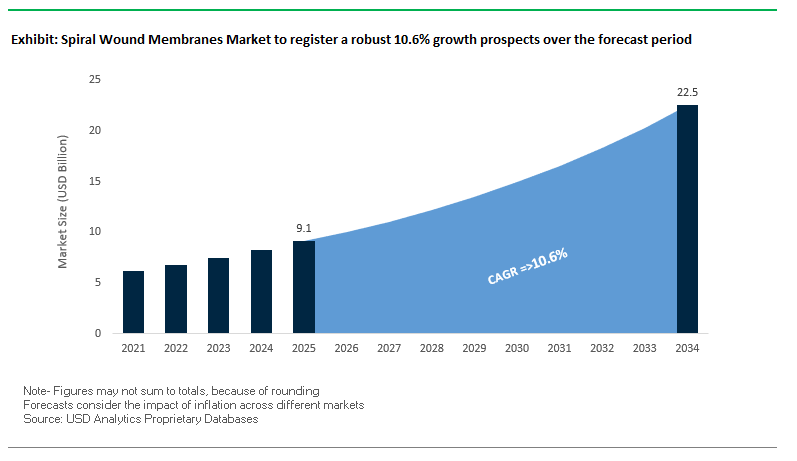

The global spiral wound membranes market is set to expand significantly, with a market value projected at USD 9.1 billion in 2025 and expected to reach USD 22.5 billion by 2034, reflecting an impressive CAGR of 10.6%. This growth trajectory highlights the increasing reliance of industries and municipalities on spiral wound reverse osmosis (RO) membranes for applications ranging from seawater desalination to ultrapure water generation. For Stakeholders in water treatment, electronics, food processing, and energy sectors, the report answers key questions around cost efficiency, sustainability, and technology innovation.

The market’s expansion is anchored in the growing adoption of ultrapure water solutions in semiconductors and pharmaceuticals, where production processes demand millions of gallons of high-purity water per day. At the same time, spiral wound membranes remain the technology of choice for cost-effective desalination across water-stressed geographies. The integration of energy-efficient membranes that operate at reduced pressure is enabling industries to lower operational costs while reducing their carbon footprint. Beyond water treatment, spiral wound membranes are carving a niche in food and beverage concentration, dairy fractionation, and industrial product recovery, reinforcing their role as a multi-sector technology platform.

Key Market Insights

- High-Purity Water for Industry: Critical for semiconductors and biopharmaceuticals, where ultrapure water is essential for precision manufacturing.

- Cost-Effective Desalination: Spiral wound RO membranes dominate seawater and brackish water desalination projects worldwide.

- Versatile Industrial Applications: Used in dairy, beverages, and specialty industrial recovery processes beyond traditional water treatment.

- Energy Efficiency Innovations: New low-energy membranes are reducing pressure requirements, helping lower operational costs and emissions.

Market Analysis: Recent Developments Reshaping the Spiral Wound Membrane Industry

The spiral wound membranes industry is experiencing rapid transformation driven by sustainability goals, project expansions, and strategic corporate moves. A landmark development came in August 2025, when DuPont Water Solutions was honored with a BIG Sustainability Award for its pioneering work in industrial wastewater reuse, underscoring the industry’s pivot towards circular water management. Around the same period, SUEZ announced in July 2025 the commissioning of China’s largest industrial membrane-based seawater desalination plant for Wanhua Chemical, positioning spiral wound membranes as a backbone of industrial water independence.

Strategic reshaping is also evident in July 2025, when LG Chem sold its water filter business, including NanoH2O™ spiral wound membranes, to Glenwood Private Equity for USD 692 million, signaling a shift toward its core green materials and energy businesses. In June 2025, SUEZ expanded its presence in Asia by winning three new seawater reverse osmosis (SWRO) projects in the Philippines, further reinforcing its regional stronghold. Meanwhile, Veolia launched its TERION™ S unit in May 2025, integrating reverse osmosis with continuous electrodeionization for compact high-grade water purification in industrial labs.

On the innovation front, DuPont introduced FilmTec™ Hypershell™ NF245XD nanofiltration membranes in February 2025, optimized for dairy operations to boost efficiency and product quality. Simultaneously, the academic sector contributed breakthroughs in April 2025 with electrostatic air spray deposition enhancing composite nanofiltration membranes, improving hydrophilicity and stability. The competitive push in desalination was reinforced in January 2025, when Toray Industries secured a major RO membrane order for the Yanbu 4 IWP plant in Saudi Arabia, the Kingdom’s first seawater desalination facility powered by clean energy. These developments underline how corporate strategy, technological advancements, and regional projects are collectively reshaping the spiral wound membranes market landscape.

Key Trends Shaping the Future of Spiral Wound Membranes

Dominance in Large-Scale Desalination and Water Treatment

Spiral wound membranes remain the backbone of global desalination efforts, particularly in reverse osmosis (RO) and nanofiltration (NF) plants. Their compact design and ability to pack large surface areas into limited footprints make them indispensable for mega-scale projects. Studies published in Frontiers in Membrane Science and Technology and MDPI confirm that spiral wound RO modules account for over 85% of desalination projects in China, with 121 projects recorded by the end of 2018. Furthermore, the rise of “Mega-SWRO” plants exceeding 500,000 m³/day capacity in Saudi Arabia and the UAE underscores the scalability and reliability of spiral wound technology, solidifying its global dominance in large-scale water security projects.

Innovation in Anti-Fouling and High-Performance Membranes

Fouling continues to be the biggest operational challenge for spiral wound membranes, especially in industrial wastewater and high-solids streams. To combat this, manufacturers are investing in R&D to develop next-generation anti-fouling membranes. Research from ACS Applied Materials & Interfaces highlights advancements using graphene and carbon nanotubes to create hydrophilic surfaces that resist organic and biological deposits. These cutting-edge innovations extend membrane life, reduce chemical cleaning cycles, and cut down operational costs, creating a competitive edge for suppliers offering enhanced anti-fouling designs.

Growth in Industrial Wastewater Treatment and Water Reuse

With industries under pressure to comply with stricter discharge regulations and sustainability goals, spiral wound membranes are increasingly deployed for on-site wastewater recycling and process water reuse. A case study by a European water technology company demonstrated how a Polish potato starch processor saved €2.4 million annually by using spiral wound membranes to recover proteins and potassium while avoiding the cost of building a new biological treatment plant. This example underlines the economic value of integrating spiral wound systems into industrial processes, making them attractive for food, chemicals, mining, and heavy industries.

Rising Demand for Modular and Decentralized Water Treatment Systems

Spiral wound membranes’ modular “plug-and-play” design is fostering the rise of decentralized water treatment in both industrial and municipal sectors. Their scalability allows plants to easily expand or downsize without infrastructure overhauls, which is critical for industries facing fluctuating demand. Companies like Veolia are customizing spiral wound modules to withstand extreme pH and temperature environments, showcasing their adaptability. This flexibility is driving uptake in remote communities, industrial clusters, and resource-limited regions, where decentralized water solutions offer resilience and cost savings.

Market Share Analysis of the Spiral Wound Membranes Market

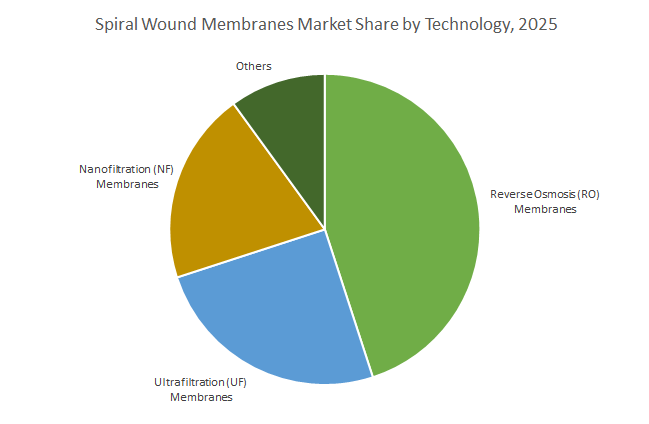

Market Share by Technology- Reverse Osmosis Leads with 45% Global Market Share

Reverse Osmosis (RO) spiral wound membranes dominate the technology landscape with a projected 45% market share by 2025. Their leadership stems from their critical role in desalination and high-purity water production across municipal, industrial, and power applications. Despite their higher operating pressures and system complexity, RO membranes provide unmatched salt rejection and water quality, ensuring their continued revenue leadership. Ultrafiltration (UF), accounting for 25%, plays a crucial role as a pre-treatment solution that extends RO performance by reliably removing particulates, bacteria, and viruses. Nanofiltration (NF) membranes (20%) are a rapidly growing segment due to their energy-efficient ion-selective separation, making them ideal for softening, color removal, and food processing. The “Others” category (10%), including microfiltration and emerging gas separation applications, is expected to open new growth frontiers such as biogas upgrading and nitrogen generation.

Market Share by Membrane Material- Polyamide Thin-Film Composites Dominate with 80% Share

Polyamide Thin-Film Composite (TFC) membranes are the undisputed leaders, capturing 80% of the spiral wound membranes market by 2025. Their superior salt rejection rates, durability, and broad chemical tolerance make them the backbone of modern RO and NF systems. UF-specific materials such as Polysulfone (PS), Polyethersulfone (PES), and PVDF, which account for 15%, remain critical for pre-treatment and stand-alone UF systems, valued for their mechanical strength and chlorine resistance. Meanwhile, cellulose acetate (CA/CTA) membranes, once the pioneer material, have declined to 5% due to their inferior performance compared to TFC. However, their high chlorine tolerance ensures they remain relevant in select wastewater treatment applications, particularly where aggressive disinfection regimes are unavoidable.

Market Share by Application- Water & Wastewater Treatment Dominates with 60% Share

Water and wastewater treatment applications lead the market with 60% share, reflecting the dominance of desalination, municipal water purification, and industrial wastewater reuse as global priorities. The integration of spiral wound RO and NF membranes is critical to addressing water scarcity, making this the anchor segment. Industrial processing holds 25%, with strong adoption in food and beverage, pharmaceuticals, and chemical industries, where spiral wound membranes support product concentration, purification, and solvent recovery. Power and energy applications account for 10%, driven by demand for boiler feed water purification and zero liquid discharge (ZLD) systems in thermal power plants. Finally, the electronics industry, while holding 5%, represents a high-value niche as spiral wound membranes are vital for producing ultra-pure water (UPW) used in semiconductor and microchip fabrication, where even minute contaminants can cause multi-million-dollar losses.

China: Driving Industrial ZLD and Water Reuse with Spiral Wound Membranes

China’s spiral wound membranes market is experiencing robust growth due to stringent industrial wastewater regulations and strategic investments in advanced water treatment technologies. The Ministry of Ecology and Environment (MEE) enforces strict wastewater discharge standards, compelling companies to adopt spiral wound membranes for both municipal and industrial wastewater applications. The country is investing heavily in zero-liquid discharge (ZLD) systems that leverage spiral wound reverse osmosis (SWRO) technology. Key applications include textile wastewater recycling, where ultra-high-pressure SWRO membranes enable recovery of over 95% of process water, enhancing sustainability and addressing water scarcity challenges.

United States: Government Initiatives and R&D Fuel Spiral Wound Innovation

In the United States, government funding and academic research are accelerating adoption of spiral wound membrane technologies. The Bipartisan Infrastructure Law allocates over $50 billion to the EPA for water infrastructure improvements, including projects targeting emerging contaminants such as PFAS. NSF-funded research centers are developing advanced membranes for water purification, chemical separations, and biopharmaceutical processing, driving innovation in spiral wound RO, NF, and UF membranes. Leading companies like Veolia Water Technologies have deployed spiral wound membrane systems to meet strict regulatory standards, highlighting the market’s growing industrial and municipal adoption.

Saudi Arabia: Advanced Desalination and Sustainable Water Infrastructure

Saudi Arabia is a global leader in membrane-based desalination, with spiral wound reverse osmosis (SWRO) membranes playing a central role in sustainable water supply. The ACWA Power-led Jubail 3A desalination plant produces 600,000 cubic meters of fresh water daily, while the SWCC’s Yanbu 4 facility delivers 450,000 cubic meters per day using energy-efficient SWRO membranes. These projects reflect the Kingdom’s strategic shift toward membrane-based desalination solutions. The Saudi Water Partnership Company (SWPC) continues to launch new RO-focused initiatives, cementing spiral wound membranes as integral to the country’s water security and sustainable development goals.

India: Green Bonds and Large-Scale SWRO Deployments

India is accelerating spiral wound membrane adoption through government initiatives and significant infrastructure investments. The “Jal Jeevan Mission” and the Department of Science & Technology’s Water Technology Initiative support R&D in membrane filtration and nanomaterials to provide safe drinking water. The Ghaziabad Nagar Nigam issued India’s first Certified Green Municipal Bond, raising ₹150 crore to develop a Tertiary Sewage Treatment Plant (TSTP) utilizing spiral wound membranes for industrial water reuse. Additionally, VA TECH WABAG’s seven-year O&M contract for the 110 MLD SWRO Nemmeli Desalination Plant, valued at INR 415 crores, demonstrates large-scale deployment and operational commitment to spiral wound membrane infrastructure.

Japan: R&D Leadership and Global Technology Exports

Japan is a leading innovator in spiral wound membrane technologies, driven by both corporate and academic research. Toray Industries has developed durable RO membranes that maintain high removal efficiency in industrial wastewater treatment. Hydranautics, a Nitto Group company, offers a complete portfolio of spiral wound RO, NF, UF, and MF membranes designed for challenging wastewater applications. Japan also contributes globally, supplying RO membranes for next-generation sustainable desalination plants in Saudi Arabia, converting conventional facilities into eco-friendly systems with advanced spiral wound membrane technology.

Germany: Industrial Excellence and Digital Integration

Germany maintains a leadership position in applying spiral wound membranes for industrial wastewater treatment. PWT Wassertechnik specializes in spiral wound filtration for industrial applications, ensuring strict compliance with European environmental regulations. Companies like MANN+HUMMEL are driving technological advancements by integrating digital solutions with membrane technology, enhancing efficiency and sustainability in industrial water reuse and green energy sectors. Germany’s focus on innovation and compliance positions it as a key hub for spiral wound membrane adoption in Europe.

Competitive Landscape: Leading Players Driving Innovation and Global Adoption

The spiral wound membranes market is highly competitive, with multinational companies shaping its direction through innovation, acquisitions, and large-scale project delivery. Leaders such as DuPont Water Solutions, Toray Industries, SUEZ Water Technologies & Solutions, Koch Separation Solutions, LG Chem, and Nitto Denko (Hydranautics) are continuously expanding their portfolios while focusing on energy-efficient, sustainable, and application-specific solutions. Their global footprints, technological depth, and execution capacity make them the dominant forces steering industry adoption.

DuPont Water Solutions – Innovation Anchored in FilmTec™ Technology

DuPont continues to hold a dominant position with its FilmTec™ spiral wound membranes, a brand recognized globally for performance and reliability. Its FilmTec™ Fortilife™ series has gained traction for its ability to handle high brine concentrations while maintaining energy efficiency, particularly in industrial reuse applications. In August 2025, DuPont was honored with the BIG Sustainability Award for its advancements in wastewater treatment and minimal liquid discharge solutions, underscoring its leadership in sustainable practices. Its wide global footprint, supported by technical training and customer service, enables it to address complex application requirements across industries.

Toray Industries – Strength in Desalination and Ultra-Low Energy RO

Toray Industries has cemented its reputation as a leading supplier for large-scale desalination projects, including Saudi Arabia’s Yanbu 4 and Shuaibah 3 IWP plants. The company’s spiral wound RO membranes are renowned for ultra-low energy consumption, enabling sustainable desalination at reduced operational costs. Toray’s Water Treatment Technology Center in India provides regional support and enhances customer engagement, reflecting its long-term focus on growth markets. With a diversified membrane portfolio spanning RO, NF, UF, and MF, Toray offers comprehensive solutions for water and industrial processes alike.

SUEZ Water Technologies & Solutions – Large-Scale Projects and Sustainability Leadership

As part of Veolia, SUEZ brings holistic expertise in water and waste management, integrating spiral wound membranes as part of its wider sustainability solutions. Its acquisition of LANXESS’s RO membrane line strengthened its brackish water RO portfolio, while its track record in executing China’s largest membrane-based seawater desalination plant in July 2025 highlighted its engineering and project management capabilities. SUEZ also plays a pivotal role in advancing water reuse in Europe, evidenced by its work on France’s largest treated wastewater reuse project in Argelès-sur-Mer, aligning its strategy with circular economy principles.

Koch Separation Solutions (Kovalus) – Pioneer in Sanitary Spiral Membranes

Koch Separation Solutions (KSS) has long been a pioneer in sanitary spiral wound membranes, especially in food and dairy applications. Its Fluid Systems® NF and RO elements are widely used for challenging industrial wastewater and high-purity water applications. The company has been enhancing its value proposition through acquisitions, including RELCO, enabling integrated membrane–evaporation–drying solutions. With its planned USD 20+ million investment in a new spiral assembly facility in Mexico, KSS is boosting capacity and supply resilience, reinforcing its market competitiveness.

LG Chem – Strategic Shift Away from Water Filtration

LG Chem, through its NanoH2O™ spiral wound membranes built on Thin Film Nanocomposite (TFN) technology, had established itself as a key supplier for desalination and municipal water projects. However, in July 2025, LG Chem exited the water filtration market by selling its water filter business to Glenwood Private Equity for USD 692 million. Prior to this divestment, the company had a strong global presence in desalination and invested in IoT-enabled smart membrane systems for real-time performance monitoring, highlighting its innovative edge before shifting focus toward eco-friendly materials and energy solutions.

Nitto Denko Corporation (Hydranautics) – Diverse Portfolio and Anti-Fouling Expertise

Through its Hydranautics brand, Nitto Denko Corporation delivers one of the most diverse portfolios in the spiral wound membrane industry, spanning RO, NF, UF, and MF technologies. Its membranes are widely applied in brackish water treatment, reclaimed water processing, and ultrapure water generation, particularly for electronics and industrial facilities. Hydranautics has also been a leader in anti-fouling innovation, with product series like ESPA2-LD and SWC5-LD designed to reduce scaling and extend membrane life. Its strong global presence, coupled with application-specific expertise, makes Nitto a critical player in both municipal and industrial projects.

Spiral Wound Membranes Market Report Scope

Spiral Wound Membranes Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$9.1 Billion

|

|

Market Size (2034)

|

$22.5 Billion

|

|

Market Growth Rate

|

10.6%

|

|

Segments

|

By Technology (Reverse Osmosis Membranes, Nanofiltration Membranes, Ultrafiltration Membranes, Others), By Membrane Material (Polyamide TFC, Cellulose Acetate, UF Membrane Materials), By Application (Water & Wastewater Treatment, Industrial Processing, Power & Energy, Electronics)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

DuPont de Nemours, Inc., Toray Industries, Inc., SUEZ, Veolia, Xylem Inc., Pentair plc, LG Chem, The Dow Chemical Company, Kubota Corporation, Hydranautics (a Nitto Group Company), Koch Industries, V.A. TECH WABAG Ltd., MANN+HUMMEL, Evoqua Water Technologies, Mitsubishi Chemical Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Spiral Wound Membranes Market Segmentation

By Technology

- Reverse Osmosis (RO) Membranes

- Nanofiltration (NF) Membranes

- Ultrafiltration (UF) Membranes

- Others

By Membrane Material

- Polyamide TFC

- Cellulose Acetate

- UF Membrane Materials

By Application

- Water & Wastewater Treatment

- Industrial Processing

- Food & Beverage

- Chemical & Petrochemical

- Pharmaceutical & Biotechnology

- Power & Energy

- Electronics

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Spiral Wound Membranes Industry include-

- DuPont de Nemours, Inc.

- Toray Industries, Inc.

- SUEZ

- Veolia

- Xylem Inc.

- Pentair plc

- LG Chem

- The Dow Chemical Company

- Kubota Corporation

- Hydranautics (a Nitto Group Company)

- Koch Industries

- V.A. TECH WABAG Ltd.

- MANN+HUMMEL

- Evoqua Water Technologies

- Mitsubishi Chemical Corporation

*- List not Exhaustive

Research Coverage

USDAnalytics’ Spiral Wound Membranes Market study delivers a decision-grade view of demand across desalination, ultrapure water, and industrial reuse. Building on verified installations, supplier interviews, and project trackers, this report investigates how RO/NF/UF stacks are scaling from mega-SWRO to modular, decentralized systems; it surfaces material science breakthroughs in thin-film composites and anti-fouling coatings; our competitive analysis reviews capacity expansions, plant wins, and portfolio realignments; and it highlights energy-efficiency levers, cost-per-m³ benchmarks, and lifecycle OPEX under varying feedwater chemistries. With defensible sizing through 2034, technology roadmaps, and regional pipeline visibility, this report is an essential resource for strategy, product, capex, and ESG teams seeking to align membrane selection with reliability, compliance, and total cost of ownership. Scope Includes-

- Segmentation: By technology (RO, NF, UF, others); membrane material (Polyamide TFC, Cellulose Acetate, UF materials); application (Water & Wastewater Treatment; Industrial Processing Food & Beverage, Chemical & Petrochemical, Pharma & Biotech; Power & Energy; Electronics).

- Geographic Scope: “Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.”

- Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies (Analysis/ profiles of 15+ companies, include the list of given companies): DuPont de Nemours, Inc.; Toray Industries, Inc.; SUEZ; Veolia; Xylem Inc.; Pentair plc; LG Chem; The Dow Chemical Company; Kubota Corporation; Hydranautics (Nitto Group); Koch Industries (Koch Separation Solutions); V.A. TECH WABAG Ltd.; MANN+HUMMEL; Evoqua Water Technologies; Mitsubishi Chemical Corporation. List not exhaustive.

Methodology

We apply a hybrid bottom-up/bottom-across model: (i) cataloging active and announced plants (desalination, UPW, reuse) to derive element counts, recovery ratios, and normalized flux; (ii) triangulating vendor shipments, bid awards, and distributor sell-through to estimate units and ASPs by element type; (iii) mapping energy curves (LE/ULE vs standard) to power intensity and chemical-cleaning frequency for OPEX; and (iv) converting project pipelines and regulatory triggers into adoption curves by region. Primary research spans OEMs, EPCs, utilities, and industrial users to validate replacement intervals, clean-in-place (CIP) cycles, and failure modes. We stress-test forecasts via Monte-Carlo on feed TDS/fouling indices, financing milestones, and membrane learning-rate effects, with QA checks against historical install ramps and BOM consistency.

Table of Contents: Spiral Wound Membranes Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Insights for Stakeholders

1.3. Global Market Snapshot

2. Spiral Wound Membranes Market Outlook (2025–2034)

2.1. Introduction: Growth Drivers and Industry Transformation

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $9.1 Billion

2.2.2. Forecasted Market Size (2034): $22.5 Billion

2.2.3. Projected Compound Annual Growth Rate (CAGR): 10.6%

2.3. Key Trends and Opportunities

2.3.1. Dominance in Large-Scale Desalination and Water Treatment

2.3.2. Innovation in Anti-Fouling and High-Performance Membranes

2.3.3. Growth in Industrial Wastewater Treatment and Water Reuse

2.3.4. Rising Demand for Modular and Decentralized Water Treatment Systems

3. Recent Developments and Strategic Shifts

3.1. Market Analysis: Recent News and Technological Developments

3.1.1. DuPont Water Solutions Wins BIG Sustainability Award

3.1.2. SUEZ Commissions China’s Largest Industrial Desalination Plant

3.1.3. LG Chem Sells Water Filter Business to Glenwood Private Equity

3.1.4. SUEZ Expands with New Projects in the Philippines

3.1.5. Veolia Launches Integrated TERION™ S Unit

3.1.6. DuPont Introduces New Hypershell™ Nanofiltration Membranes

3.1.7. Toray Industries Secures Major Order for Yanbu 4 IWP Plant

4. Competitive Landscape: Leading Companies

4.1. Market Overview: From Material Specialists to Global Solution Providers

4.2. Key Competitive Factors

4.2.1. Integrated Product Portfolios

4.2.2. R&D and Innovation in Advanced Materials

4.2.3. Global Project Execution and Aftermarket Support

4.3. Profiles of Top Players

4.3.1. DuPont Water Solutions

4.3.2. Toray Industries

4.3.3. SUEZ Water Technologies & Solutions

4.3.4. Koch Separation Solutions (Kovalus)

4.3.5. LG Chem (Divestment noted)

4.3.6. Nitto Denko Corporation (Hydranautics)

5. Spiral Wound Membranes Market – Segmentation Insights

5.1. By Technology

5.1.1. Reverse Osmosis (RO) Membranes

5.1.2. Nanofiltration (NF) Membranes

5.1.3. Ultrafiltration (UF) Membranes

5.1.4. Others

5.2. By Membrane Material

5.2.1. Polyamide Thin-Film Composite (TFC)

5.2.2. Cellulose Acetate

5.2.3. UF Membrane Materials

5.3. By Application

5.3.1. Water & Wastewater Treatment

5.3.2. Industrial Processing

5.3.2.1. Food & Beverage

5.3.2.2. Chemical & Petrochemical

5.3.2.3. Pharmaceutical & Biotechnology

5.3.3. Power & Energy

5.3.4. Electronics

6. Country Analysis and Outlook: Spiral Wound Membranes Market

6.1. China: Driving Industrial ZLD and Water Reuse

6.2. United States: Government Initiatives and R&D

6.3. Saudi Arabia: Advanced Desalination and Sustainable Water Infrastructure

6.4. India: Green Bonds and Large-Scale SWRO Deployments

6.5. Japan: R&D Leadership and Global Technology Exports

6.6. Germany: Industrial Excellence and Digital Integration

6.7. Other Key Countries

6.7.1. North America (Canada, Mexico)

6.7.2. Europe (UK, France, Spain, Italy, Russia, Rest of Europe)

6.7.3. Asia Pacific (South Korea, South East Asia, Rest of Asia)

6.7.4. South America (Brazil, Argentina, Rest of South America)

6.7.5. Middle East and Africa (UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

7. Spiral Wound Membranes Market Size Outlook by Region (2025-2034)

7.1. North America Market Size Outlook to 2034

7.1.1. By Technology

7.1.2. By Membrane Material

7.1.3. By Application

7.2. Europe Market Size Outlook to 2034

7.2.1. By Technology

7.2.2. By Membrane Material

7.2.3. By Application

7.3. Asia Pacific Market Size Outlook to 2034

7.3.1. By Technology

7.3.2. By Membrane Material

7.3.3. By Application

7.4. South America Market Size Outlook to 2034

7.4.1. By Technology

7.4.2. By Membrane Material

7.4.3. By Application

7.5. Middle East and Africa Market Size Outlook to 2034

7.5.1. By Technology

7.5.2. By Membrane Material

7.5.3. By Application

8. Company Profiles: Additional Leading Players

8.1. DuPont de Nemours, Inc.

8.2. Toray Industries, Inc.

8.3. SUEZ

8.4. Veolia

8.5. Xylem Inc.

8.6. Pentair plc

8.7. LG Chem

8.8. The Dow Chemical Company

8.9. Kubota Corporation

8.10. Hydranautics (a Nitto Group Company)

8.11. Koch Industries

8.12. V.A. TECH WABAG Ltd.

8.13. MANN+HUMMEL

8.14. Evoqua Water Technologies

8.15. Mitsubishi Chemical Corporation

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures