Water Filters Market Overview

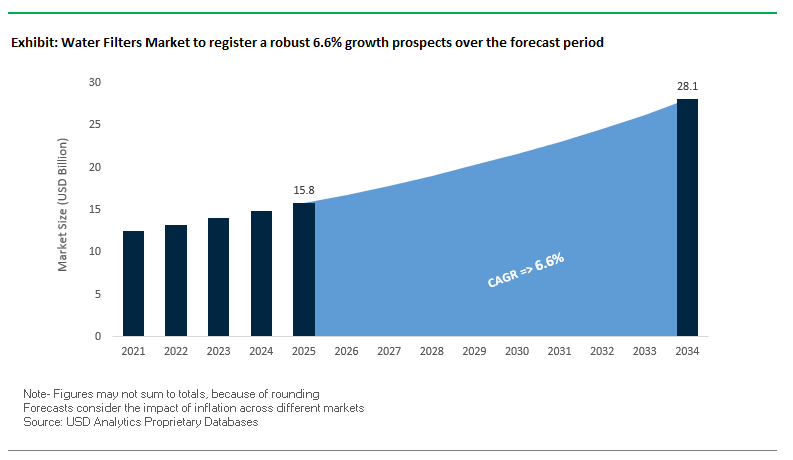

The global water filters market is projected to grow from $15.8 billion in 2025 to $28.1 billion by 2034, representing a CAGR of 6.6%. Rising concerns about water contamination and safety are driving widespread adoption of point-of-use (POU) and whole-house water filtration solutions. With significant portions of the global population exposed to water exceeding World Health Organization (WHO) standards, both residential and commercial sectors are increasingly seeking reliable filtration systems.

Aging water infrastructure in developed nations, particularly in the U.S. and Europe, has heightened demand for water filters as a primary defense against contaminants such as lead, chlorine, and microorganisms. Furthermore, the integration of smart technology and AI-powered monitoring systems enables real-time water quality tracking, predictive maintenance, and automated performance adjustments, enhancing operational efficiency. The trend toward decentralized water management is also shaping market dynamics, as compact and user-friendly filtration systems gain traction for both residential and commercial applications.

Key Insights for Industry Stakeholders:

- Health and Safety Priority: Increased awareness of water contamination drives adoption of POU and whole-house filters.

- Infrastructure Modernization: Aging municipal systems in developed markets necessitate upgrades and filtration solutions.

- Smart Filtration Adoption: AI and IoT integration allows real-time monitoring, predictive maintenance, and automatic adjustments.

- Decentralized Water Management: Growing use of POE and POU systems creates opportunities for compact, efficient, and high-performance units.

- Industrial and Commercial Uptake: Filtration systems are crucial in food, beverage, and manufacturing industries to ensure quality and compliance.

Market Analysis: Recent Developments in Water Filters

The water filters market has witnessed notable strategic and technological developments from 2024 to 2025. In August 2025, Pentair announced the acquisition of Hydra-Stop, enhancing its portfolio to address aging municipal water infrastructure. That same month, Transfilm Technology launched IonClear, a North American water technology hub focused on accelerating innovation in reverse osmosis (RO) and nanofiltration membranes, strengthening the regional supply chain. One Water Systems also reinforced its 15-year warranty for whole-house, salt-free filtration systems in August 2025, emphasizing long-term value for consumers.

June 2025 saw Ahlstrom complete its production unit for advanced molecular filtration media in Turin, Italy, expanding capacity to meet growing demand for specialized filter materials. Earlier, in April 2025, Ahlstrom introduced Optipad™, a high-performance, sustainable filtration pad, while in March 2025, the company launched Ahlstrom ECO™, a lignin-based sustainable filtration platform targeting industrial and automotive applications. In December 2024, A.O. Smith Corporation acquired Pureit from Unilever, reinforcing its product portfolio and distribution network in India. Additionally, Clean Harbors, Inc., in October 2024, unveiled its Total PFAS Solution, covering all stages of filtration and remediation for emerging contaminants.

Key Trends Driving the Water Filters Market

Regulatory Compliance and Public Health as Market Catalysts

The water filters market is experiencing heightened demand due to regulatory pressures and public health concerns. The U.S. EPA’s enforcement of maximum contaminant levels for six PFAS compounds, alongside the designation of PFOA and PFOS as hazardous substances, is driving adoption of high-performance filtration systems. In Europe, the recast Drinking Water Directive mandates closer monitoring of emerging contaminants like microplastics and endocrine disruptors, creating a strong market pull for compliant water filters. These regulations underscore the critical role of filtration in ensuring safe drinking water and protecting human health.

Integration of IoT and AI for Smart Filtration Management

The adoption of Industry 4.0 technologies, including IoT sensors and AI-driven analytics, is transforming water filtration operations. Smart water filters can autonomously monitor water quality, detect leaks, and optimize filter replacement schedules, reducing operational costs by 20–30%. Real-time data allows operators to adjust filtration processes dynamically, enhancing efficiency and reducing downtime. Companies investing in AI-enabled and IoT-integrated filtration solutions are positioning themselves to capture growth in both residential and commercial markets, where operational efficiency and predictive maintenance are increasingly valued.

Advanced Materials and Novel Filtration Media

Technological advancements in filter materials are opening new avenues in the water filters market. Novel adsorbents, nanomaterials, and biosorbents derived from agricultural waste, such as mango and banana peels, are being developed to remove heavy metals, pharmaceuticals, and microplastics with high efficiency. These innovations support sustainability and circular economy principles by converting waste into high-performance filtration media. The adoption of advanced nanomaterials and bio-based adsorbents is expected to differentiate premium products and enhance environmental compliance.

Emerging Opportunities in the Water Filters Market

The water filters market presents opportunities for manufacturers offering smart, regulatory-compliant, and sustainable solutions. The convergence of IoT-enabled monitoring, advanced materials, and hybrid filtration systems creates avenues for high-value residential, commercial, and industrial applications. With increasing awareness of emerging contaminants and stricter water quality regulations, companies that integrate real-time monitoring, predictive maintenance, and eco-friendly filtration media are likely to gain a competitive advantage. Additionally, the growing adoption of whole-house and under-sink systems in premium residential markets reflects a trend toward holistic water quality management, representing a significant growth opportunity.

Market Share Analysis of Water Filters Market

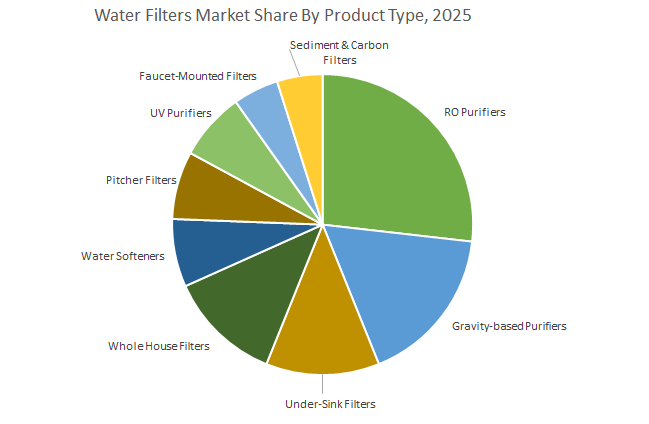

Market Share by Product Type: RO Purifiers Lead, Gravity-Based Filters Dominate Volume

RO purifiers (26.9%) dominate the value share of the water filters market due to their multi-stage purification capabilities, removing dissolved salts, heavy metals, and a broad range of contaminants. Gravity-based purifiers (16.9%) and pitcher filters lead in volume, especially in price-sensitive regions, providing low-cost, effective solutions for basic taste and odor improvement. Under-sink (11.8%) and whole-house filters (11.8%) are rapidly growing segments, offering convenience and comprehensive protection for residential water systems. Other niche segments like UV purifiers, faucet-mounted filters, and water softeners cater to specialized microbiological and hardness removal needs.

Market Share by Technology: Activated Carbon Remains the Workhorse

Activated carbon technology (32.8%) continues to dominate due to its ability to remove chlorine, VOCs, bad taste, and odor, making it indispensable across nearly all product types. RO systems (22.5%) represent the premium segment, offering unparalleled contaminant removal for TDS, heavy metals, and fluoride. Sediment filters (16.9%) serve as the first line of defense, protecting subsequent filtration stages. Ion exchange (11.8%) and UV/UF technologies address hardness, microbial, and turbidity challenges. Hybrid systems combining multiple technologies, such as Sediment → Carbon → RO, are increasingly common, reflecting the market’s focus on broad-spectrum water purification.

Market Share by End-User: Residential Dominates, Commercial and Industrial Show Growth Potential

The residential segment (64.3%) represents the largest market, driven by mass-market adoption, rising disposable incomes, and heightened health awareness. The commercial segment (22.5%) covering offices, hotels, restaurants, and hospitals is high-value, with larger equipment and long-term maintenance contracts. The industrial segment (11.8%) focuses on process water pre-treatment, boiler feed water, and specialized manufacturing applications, such as in food & beverage and pharmaceuticals. The growth in commercial and industrial filtration is fueled by regulatory compliance, process protection, and sustainability initiatives, highlighting opportunities for high-capacity, smart filtration solutions.

U.S. EPA PFAS Regulations and Federal Infrastructure Funding Accelerating Water Filters Adoption

The United States water filters market is being reshaped by stringent environmental regulations and large-scale federal investments. In April 2024, the U.S. Environmental Protection Agency (EPA) finalized the first-ever national, enforceable drinking water standards for six PFAS compounds. Public water systems must adopt advanced treatment technologies by 2029, creating unprecedented demand for filtration systems capable of removing PFAS and other emerging contaminants. Federal funding under the Bipartisan Infrastructure Law (BIL), which allocates billions to upgrading water systems, ensures rapid modernization of municipal and industrial filtration infrastructure. Industry consolidation is also fueling growth Hawkins’ April 2025 acquisition of WaterSurplus, a leading U.S. filtration solutions provider, highlights the trend of strengthening equipment portfolios through mergers. The U.S. market is primarily driven by the need to safeguard public health, comply with EPA mandates, and deploy high-performance water filters in industrial, food & beverage, and oil & gas applications.

China’s “Water Ten Plan” and RMB 26 Billion Investments Driving Filtration Market Expansion

China remains one of the fastest-growing markets for water filters, propelled by government-led pollution control programs and infrastructure investment. Under the “Water Ten Plan” and “War on Pollution”, the country expanded its water monitoring network, strengthening regulatory oversight and transparency. In 2024, more than RMB 26 billion was allocated to water pollution control initiatives, directly fueling the demand for advanced filtration technologies. Recent reports also highlight stricter pollutant discharge standards and a nationwide shift toward technologies such as MBR membranes and reverse osmosis (RO) systems both integral to high-efficiency filtration. The China water filters market is driven by the dual challenges of rapid industrialization and urbanization, alongside the need to protect drinking water sources and mitigate urban and agricultural runoff contamination. This alignment of regulatory pressure, investment, and technology adoption positions China as a global leader in next-generation water treatment solutions.

India’s Jal Jeevan Mission and Strong Regulatory Push Boosting Water Filters Market

India’s water filters market is expanding rapidly, fueled by government initiatives, regulatory enforcement, and corporate innovation. The “Jal Jeevan Mission” is providing safe drinking water to rural households, requiring hundreds of new water treatment plants. Additionally, the National Mission for Clean Ganga sanctioned ₹2,056 crore across 39 new projects in 2024, directly increasing the demand for water filters in sewage treatment systems. From a regulatory standpoint, the Ministry of Environment, Forest, and Climate Change (MoEFCC) introduced the Control of Water Pollution Guidelines, 2025, strengthening industrial compliance with wastewater discharge norms. Corporate activity is reshaping the market landscape Livpure’s collaboration with IIT Madras in 2023 for advanced purification R&D, and A.O. Smith Corporation’s acquisition of Pureit from Unilever in 2024, underscore the growing importance of technological innovation and market consolidation. Key applications are concentrated in municipal water supply, river rejuvenation, and industrial wastewater management, making India one of the fastest-growing water filter markets in Asia.

UK’s £104 Billion Water Infrastructure Plan and AMP 8 Regulations Fueling Water Filters Demand

The United Kingdom water filters market is witnessing a transformative phase due to record infrastructure spending and strict regulatory cycles. Water UK, the industry body, announced a £104 billion investment plan (2025–2030) for water and sewage systems, including new reservoirs and large-scale water transfer schemes. This near-doubling of expenditure compared to the previous five years ensures large-scale demand for advanced filtration systems in municipal water utilities. Regulatory policies under Asset Management Period (AMP) 8 mandate water utilities to build infrastructure that reduces environmental risks while ensuring compliance with stringent water quality standards. This regulatory push makes high-purity water filtration technologies a necessity. The UK’s demand is primarily driven by the dual needs of modernizing aging water systems and improving resilience against future environmental and population challenges.

Germany’s Revised EU Wastewater Directive and Innovation in Micro-Pollutant Removal Driving Filters Market

Germany is one of Europe’s most advanced water filters markets, heavily influenced by EU regulatory frameworks and domestic innovation. The revised EU Urban Wastewater Treatment Directive, effective January 2025, requires stricter monitoring and removal of pollutants, creating significant demand for filtration technologies in municipal and industrial plants. German companies and research institutions are investing in innovative filter systems capable of removing pharmaceuticals, micro-pollutants, and PFAS, making the country a hub for high-tech water purification. Public awareness and demand for sustainable solutions further accelerate the adoption of advanced filters. The German water filters market is driven by the combined forces of strict compliance requirements, cutting-edge R&D, and industrial wastewater treatment needs, reinforcing Germany’s leadership role in Europe’s clean water initiatives.

Japan’s Integrated Water Management and Digital Filtration Advancements Boosting Market Adoption

Japan’s water filters market is being transformed by integrated government oversight and digital innovation. Since April 2024, the Ministry of Land, Infrastructure, Transport and Tourism (MLIT) has overseen both water supply and sewerage systems, promoting coordinated infrastructure upgrades. In December 2024, MLIT released the Water Supply Performance Report, highlighting the seismic and financial vulnerabilities of nearly 1,300 utilities, emphasizing the urgent need for filtration system upgrades. To address rural water challenges, MLIT launched a “Catalogue of Digital Technology in Water and Sewerage Systems”, showcasing 119 advanced digital solutions for predictive maintenance, inspection, and data management. These advancements accelerate the adoption of smart, technology-enabled water filtration systems. Market drivers include industrial water treatment, recycling and reuse, and modernization of aging municipal infrastructure, positioning Japan as a leader in digital-driven water filtration innovation.

Competitive Landscape of Water Filters Market

The water filters market is highly competitive, with leading global players focusing on innovative technologies, strategic acquisitions, and integrated solutions to address residential, commercial, and industrial water needs. Companies differentiate through proprietary filtration media, smart monitoring platforms, and extensive distribution networks, ensuring broad market coverage and enhanced performance.

Pentair plc focuses on municipal and residential water infrastructure solutions

Pentair is a global leader in water filtration solutions, offering under-sink systems, whole-house filters, and industrial filtration products. Its August 2025 acquisition of Hydra-Stop enhances its capabilities in municipal water infrastructure. The company emphasizes sustainable water use, combining product innovation with initiatives such as the Pentair Foundation Water Grants Program to reinforce brand value and social responsibility.

Xylem Inc. integrates smart water technologies with advanced filtration

Xylem combines a broad portfolio of water technologies with digital services and analytics. Its acquisitions of Evoqua Water Technologies (2023) and Idrica (December 2024) have strengthened its market position in mission-critical water treatment and smart water management. Xylem provides filter cartridges, membranes, and complete filtration systems as part of end-to-end water solutions, integrating sustainability and efficiency across municipal and industrial operations.

A. O. Smith Corporation expands through strategic acquisitions

A. O. Smith has a strong market presence in residential water treatment, particularly in North America and Asia. The December 2024 acquisition of Pureit from Hindustan Unilever expanded its footprint in India, Bangladesh, Sri Lanka, Vietnam, and Mexico. The company offers a full range of residential solutions, including RO systems, water softeners, and whole-house filtration units, catering to growing global demand for safe and convenient water treatment.

Veolia Water Technologies leverages digital innovation for advanced filtration

Veolia provides technology-driven water filtration solutions, including high-rate clarifiers and RO systems, as well as mobile water fleets for emergency needs. Its June 2025 partnership with AECOM to deploy PFAS destruction technology emphasizes the company's commitment to emerging contaminant management. Veolia’s Hubgrade platform utilizes AI and analytics to optimize system performance, offering integrated, sustainable water solutions for municipal and industrial clients.

SUEZ S.A. delivers integrated circular water filtration solutions

SUEZ specializes in circular water and waste management solutions, offering microfiltration, ultrafiltration, and RO systems. Recent contracts in Asia, including a new desalination plant in the Philippines, highlight the company’s focus on large-scale infrastructure projects. SUEZ leverages digital tools and advanced technologies to improve plant performance and resilience against climate and operational challenges.

Pall Corporation drives high-tech filtration and purification

Pall Corporation, a subsidiary of Danaher, focuses on high-tech filtration, separation, and purification solutions for microelectronics, life sciences, and industrial applications. Its August 2022 Singapore plant investment doubled production capacity for the Asia Pacific semiconductor industry. Pall emphasizes research-driven innovation, supporting decarbonization and energy transition initiatives while addressing complex filtration challenges in critical industries.

Water Filters Market Report Scope

Water Filters Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$15.8 Billion

|

|

Market Size (2034)

|

$28.1 Billion

|

|

Market Growth Rate

|

6.6%

|

|

Segments

|

By Product Type (RO Purifiers, UV Purifiers, Gravity-based Purifiers, Sediment Filters, Carbon Filters, Water Softeners, Under-Sink Filters, Faucet-Mounted Filters, Pitcher Filters, Whole House Filters), By Technology (Reverse Osmosis (RO), Ultraviolet (UV), Ultrafiltration (UF), Activated Carbon, Ion Exchange, Sediment Filtration, Others), By End-User (Residential, Commercial, Industrial), By Distribution Channel (Retail Stores, Online Stores, Direct Sales, Dealers & Distributors)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

A.O. Smith Corporation, Veolia, Evoqua Water Technologies, Pentair plc, 3M, Xylem Inc., SUEZ, Eaton Corporation, MANN+HUMMEL, Kurita Water Industries Ltd., Culligan International, Pall Corporation (A Subsidiary of Danaher Corporation), Watts Water Technologies, Inc., Parker Hannifin Corporation, Kent RO Systems Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Water Filters Market Segmentation

By Product Type

- RO Purifiers

- UV Purifiers

- Gravity-based Purifiers

- Sediment Filters

- Carbon Filters

- Water Softeners

- Under-Sink Filters

- Faucet-Mounted Filters

- Pitcher Filters

- Whole House Filters

By Technology

- Reverse Osmosis (RO)

- Ultraviolet (UV)

- Ultrafiltration (UF)

- Activated Carbon

- Ion Exchange

- Sediment Filtration

- Others

By End-User

- Residential

- Commercial

- Offices

- Restaurants

- Hotels

- Hospitals

- Educational Institutions

- Industrial

- Manufacturing

- Food & Beverage

- Pharmaceutical

By Distribution Channel

- Retail Stores

- Online Stores

- Direct Sales

- Dealers & Distributors

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Water Filters Industry include-

- A.O. Smith Corporation

- Veolia

- Evoqua Water Technologies

- Pentair plc

- 3M

- Xylem Inc.

- SUEZ

- Eaton Corporation

- MANN+HUMMEL

- Kurita Water Industries Ltd.

- Culligan International

- Pall Corporation (A Subsidiary of Danaher Corporation)

- Watts Water Technologies, Inc.

- Parker Hannifin Corporation

- Kent RO Systems Ltd.

*- List not Exhaustive

Research Coverage

USDAnalytics’ Water Filters Market study provides a boardroom-ready assessment of demand inflections across residential, commercial, and industrial users. Drawing from utility datasets, channel checks, and technology benchmarks, this report investigates how evolving drinking-water standards, PFAS controls, and aging networks are reshaping adoption of RO, activated carbon, ion exchange, and hybrid stacks; it captures breakthroughs in AI/IoT-enabled smart filters, sustainable media, and modular POE/POU designs; our competitive analysis reviews capacity additions, M&A, and portfolio moves across leading brands; and it highlights pricing, mix, and replacement cycles that determine profitability by region and end-user. With defensible sizing, specification trends, and install economics through 2034, this report is an essential resource for executives, product leaders, investors, and EPCs aligning filtration strategy with compliance, resilience, and lifecycle cost. Scope Includes-

- Segmentation: By product type (RO, UV, gravity, sediment, carbon, softeners, under-sink, faucet, pitcher, whole-house), technology (RO/UV/UF/activated carbon/ion exchange/sediment/others), end-user (residential; commercial offices, restaurants, hotels, hospitals, education; industrial manufacturing, F&B, pharma), and distribution (retail, online, direct, dealers/distributors).

- Geographic Scope: “Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.”

- Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies (Profiles of 15+ companies): A. O. Smith Corporation; Veolia; Evoqua Water Technologies; Pentair plc; 3M; Xylem Inc.; SUEZ; Eaton Corporation; MANN+HUMMEL; Kurita Water Industries Ltd.; Culligan International; Pall Corporation (Danaher); Watts Water Technologies, Inc.; Parker Hannifin Corporation; Kent RO Systems Ltd.

Methodology

We combine a bottom-up model (sell-in units by product/technology/channel across 25+ countries) with a top-down cross-check (supplier revenues, public program spend, and import/export HS flows). Primary research spans OEMs, media suppliers, distributors, and installers to capture ASPs, attachment rates (POU vs POE), replacement intervals, and service revenues. Regulatory mapping (EPA PFAS MCLs, EU DWD, local reuse ordinances) is translated into addressable-market triggers by segment. A Monte-Carlo forecast links macro drivers (household formation, infrastructure funding), technology shifts (AI/IoT adoption, advanced media), and price/mix to shipments and installed base. Results pass QA via variance analysis to prior vintages, BOM sanity checks, and triangulation with channel inventory turns.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Water Filters Market

1. Executive Summary

1.1. Market Highlights & Key Projections

1.2. Global Market Snapshot

1.3. Key Findings

2. Water Filters Market Overview (2025–2034)

2.1. Introduction

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $15.8 Billion

2.2.2. Forecasted Market Size (2034): $28.1 Billion

2.2.3. Projected Compound Annual Growth Rate (CAGR): 6.6%

2.3. Market Drivers and Challenges

2.3.1. Drivers: Public Health and Safety, Aging Infrastructure, and Regulatory Compliance

2.3.2. Challenges: High Initial Costs and Maintenance

2.4. Key Insights for Industry Stakeholders

3. Key Market Trends and Recent Developments

3.1. Regulatory Compliance and Public Health as Market Catalysts

3.2. Integration of IoT and AI for Smart Filtration Management

3.3. Advanced Materials and Novel Filtration Media

3.4. Recent Developments & Strategic Moves (2024–2025)

3.4.1. Strategic Acquisitions and Partnerships

3.4.2. Technology and Product Launches

4. Water Filters Market – Segmentation Insights

4.1. By Product Type

4.1.1. RO Purifiers (26.9% Market Share)

4.1.2. Gravity-based Purifiers (16.9% Market Share)

4.1.3. Under-Sink Filters (11.8% Market Share)

4.1.4. Whole House Filters (11.8% Market Share)

4.1.5. Other Product Types (UV, Sediment, Carbon, Pitcher, etc.)

4.2. By Technology

4.2.1. Activated Carbon (32.8% Market Share)

4.2.2. Reverse Osmosis (RO) (22.5% Market Share)

4.2.3. Sediment Filtration (16.9% Market Share)

4.2.4. Ion Exchange (11.8% Market Share)

4.2.5. Ultraviolet (UV) / Ultrafiltration (UF)

4.3. By End-User

4.3.1. Residential (64.3% Market Share)

4.3.2. Commercial (22.5% Market Share)

4.3.3. Industrial (11.8% Market Share)

4.4. By Distribution Channel

4.4.1. Retail Stores

4.4.2. Online Stores

4.4.3. Direct Sales

4.4.4. Dealers & Distributors

5. Country Analysis and Outlook: Water Filters Market

5.1. United States: EPA PFAS Regulations and Federal Infrastructure Funding

5.2. China: “Water Ten Plan” and Multi-Billion Investments

5.3. India: Jal Jeevan Mission and Strong Regulatory Push

5.4. United Kingdom: £104 Billion Water Infrastructure Plan and AMP 8 Regulations

5.5. Germany: EU Wastewater Directive and Innovation in Micro-Pollutant Removal

5.6. Japan: Integrated Water Management and Digital Filtration Advancements

6. Water Filters Market Size Outlook by Region (2025–2034)

6.1. North America Water Filters Market Size Outlook to 2034

6.1.1. By Product Type

6.1.2. By Technology

6.1.3. By Country (US, Canada, Mexico)

6.2. Europe Water Filters Market Size Outlook to 2034

6.2.1. By Product Type

6.2.2. By Technology

6.2.3. By Country (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

6.3. Asia Pacific Water Filters Market Size Outlook to 2034

6.3.1. By Product Type

6.3.2. By Technology

6.3.3. By Country (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

6.4. South America Water Filters Market Size Outlook to 2034

6.4.1. By Product Type

6.4.2. By Technology

6.4.3. By Country (Brazil, Argentina, Rest of South America)

6.5. Middle East and Africa Water Filters Market Size Outlook to 2034

6.5.1. By Product Type

6.5.2. By Technology

6.5.3. By Country (Saudi Arabia, UAE, South Africa, Egypt, Rest of MEA)

7. Competitive Landscape: Key Companies

7.1. Pentair plc

7.1.1. Company Overview

7.1.2. Municipal and Residential Water Infrastructure Solutions

7.2. Xylem Inc.

7.2.1. Company Overview

7.2.2. Integrated Smart Water Technologies with Advanced Filtration

7.3. A. O. Smith Corporation

7.4. Veolia Water Technologies

7.5. SUEZ S.A.

7.6. Pall Corporation

7.7. Other Prominent Companies

7.7.1. 3M

7.7.2. Kurita Water Industries Ltd.

7.7.3. Culligan International

7.7.4. Kent RO Systems Ltd.

8. Methodology

8.1. Research Scope

8.2. Market Research Approach

8.3. Data Sources and Validation

8.4. Assumptions and Limitations

9. Appendix

9.1. Acronyms and Abbreviations

9.2. List of Tables

9.3. List of Figures