Primary Water and Wastewater Treatment Equipment Market Overview

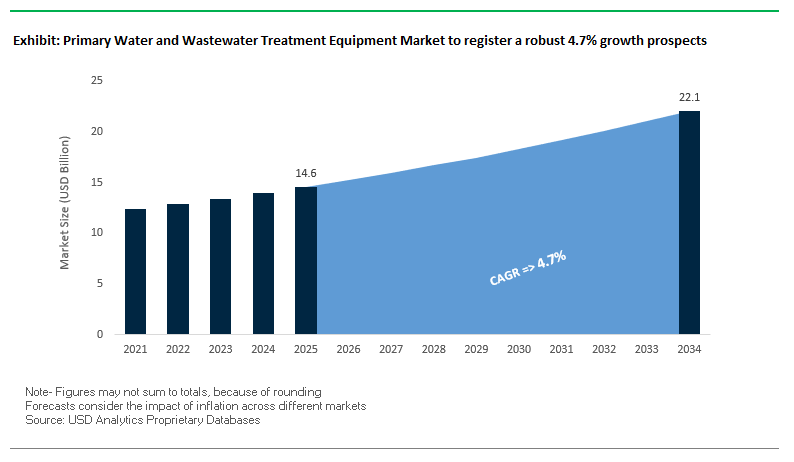

The global primary water and wastewater treatment equipment market is likely to grow from USD 14.6 billion in 2025 to USD 22.1 billion by 2034 at a CAGR of 4.7%. The segment is the essential first line of defense at wastewater treatment facilities where coarse solids, grit, and oils are drained off before secondary processes and increasingly includes resource recovery, smart automation, and modular system configurations. The contemporary market is fuelled by circular economy philosophies whereplants harvest their organic solids as a raw material for biogas factories and hence convert waste into a useful energy supply. Pre-treatment has now become mandatory to minimize downstream equipment wear and tear, cut maintenance costs, and improve general plant efficiency. Moreover, IoT-capable primary treatment plants now offer real-time influent quality information and enable automatic chemical dosing and flow optimization. More and more urbanized small-footprint areas and fast-growing municipalities are now using space-saving, module-based primary treatment units. As the impact of climate change, population growth, and industrial development exacerbates water problems worldwide, the use of sophisticated primary treatment equipment is ever more central to sustainable water management solutions.

Key Insights for Industry Professionals

- Resource Recovery Integration – Primary treatment systems increasingly recover organic matter for biogas generation.

- Efficiency Gains in Downstream Processes – Effective grit and debris removal reduces pump and clarifier wear, cutting O&M costs.

- Smart Monitoring and Automation – IoT-enabled systems improve removal rates and reduce manual intervention.

- Scalable Modular Solutions – Pre-engineered units meet the needs of small-scale plants and growing urban areas.

In-Depth Market Analysis and Recent Industry Developments

The main water and wastewater treatment equipment market is transforming fast because utilities and industry are adopting solutions beyond simple solids removal. Current systems are optimized not only for separability efficiency but also for resource recovery, automation of operations, and connection with downstream treatment. The smart trend toward primary treatment is especially strong because facilities are now using SCADA-based control systems that enable operators to access and change clarifier performance remotely, grit elimination rates, and chemical dosing in real time. It is a trend that is congruent with cost-cutting objectives and tighter environmental compliance and maximizes performance at minimal energy and manpower input. Another main catalyst is the trend toward modularized, "plug-and-play" equipment that can be quickly deployed at industrial locations and municipalities with space and budget limitations. For example, pre-engineered primary clarifier units are now being used increasingly as part of decentralized treatment strategies at remote or fast-growing locations.

Recent industry contributions highlight a strong trend toward holistic, high-efficiency water treatment systems. Veolia purchased the final 30% of Water Technologies and Solutions in July 2025 for $1.75 billion and now has complete control to achieve greater organizational efficiency and solidify its technological expertise. Veolia launched smart wastewater services in June 2025 by utilizing smart sensors and automation technologies to achieve peak performance within clarifiers and grit removal facilities. Pentair's Everpure PFAS Reduction Systems were recognized with an innovation award in April 2025 and are demonstrating an industry-wide shift toward pre-treatment configurations addressing emerging contaminants up front within the treatment system. Technology collaborations are also taking center stage; e.g., Xylem partnered on a cutting-edge anaerobic membrane bioreactor in September 2024 where organic matter being separated within primary treatment was being utilized to produce renewable biogas. Solenis' February 2024 expansion of $193 million was made within Virginia and is designed to increase PVAm polymers production crucial to successful primary sedimentation. These upgrades point toward a larger trend toward connectivity, chemical innovation, and upstream optimization within the primary treatment space.

Key Trends Shaping the Future of Primary Water and Wastewater Treatment Equipment

AI-Driven Smart Screening Systems Transforming Primary Treatment Efficiency

Integration of AI-based screening devices and IoT-capable sensors is transforming first and end-of-pipe water and wastewater treatment processes. Cities and industries are making the move from reactive maintenance strategies and are seeing up to 40% cost reductions with proactive monitoring of equipment.

Real-time operating modifications like reduced cycles of cleaning screens and regulation of flow rates are reducing energy consumption by up to 35% while simultaneously improving treatment integrity. One example is an artificial intelligence-powered sewage treatment plant in India that has cut operating expenses by 30% by automating identification of contaminants and handling of sludge.

Regulatory Push for Microplastics Removal Driving Grit and Fine Screen Upgrades

Since microplastics are now a listed U.S. Environmental Protection Agency (EPA) emerging contaminant, utilities are uprating grit removal and primary screening facilities to tighter removal standards. It has been found from research that 72% of microplastics are eliminated at the primary treatment steps and hence early-stage control is crucial.

Upgrades and new technologies like High-Density Separation grit handling facilities and Advanced Oxidation Processes (AOPs), are enhancing removals. Governments are supporting these projects with infrastructure investment like provisions of the Infrastructure Investment and Jobs Act, which is creating a long-term jobs market demand for sophisticated screening technologies.

Market Opportunities Driving Growth in Primary Water and Wastewater Treatment

Disaster-Resilient Primary Treatment Systems for Flood-Prone Regions

Increased occurrences of extreme weather are driving orders for mobile, modular, and robust first treatment units that are deployed quickly when floods or hurricanes occur. Resilience-led infrastructure investment contributes only 3% extra project cost and yields great long-term value says the United Nations Office for Disaster Risk Reduction (UNDRR). Japan water utilities offer a similar example when they invested in seismic retrofit of infrastructure, redundant network components and emergency mobile screening facilities so that service is maintained when disasters do occur.

Energy Recovery from Primary Sludge Enabling Circular Economy Models

Wastewater treatment plants are increasingly being converted to resource recovery facilities by recovering biogas and usable heat from primary sludge. Croatian examples reveal that sludge biogas supplies 30-40% of electrical requirements and up to 100% of thermal energy needs of plant processes, significantly decreasing dependence on external energy supply.

Emerging technologies like pyrolytic biochar and microbial fuel cell (MFC) technologies are extending the boundary of sludge-to-energy conversion and are reducing greenhouse gas releases by 80% or more when converted from coal-based power.

Primary Water and Wastewater Treatment Equipment Market Share Insights

Market Share by Equipment Type: Primary Wastewater Treatment Equipment Outpaces Water Treatment Solutions

In 2025, primary wastewater treatment equipment is projected to account for around 60% of the market, underscoring its non-negotiable role in every municipal and industrial plant. The dominance is attributed to the need for removing solids, fats, oils, and grease (FOG) at the very first stage before biological treatment. By contrast, primary water treatment equipment, holding nearly 40%, remains indispensable for treating raw surface water from lakes, rivers, and reservoirs to ensure municipal supply safety and protect industrial processes. Within the category, sedimentation and clarification systems alone represent about a quarter of the market, reaffirming their position as the workhorse of primary treatment, while dissolved air flotation (DAF) units are gaining momentum in industrial applications such as food & beverage and oil & gas, where buoyant materials are difficult to settle.

Market Share by Application: Municipal Wastewater Treatment Remains the Largest Contributor

The municipal wastewater treatment segment leads with nearly 45% share in 2025, driven by continuous urbanization, population growth, and the mandatory requirement for primary treatment in every municipal plant globally. These projects represent stable, high-value contracts for EPC contractors and OEMs. Industrial applications collectively account for another 45%, split between raw water preparation for industries like power and manufacturing (25%) and industrial wastewater pre-treatment (20%) to comply with discharge regulations. Within industrial wastewater, food & beverage plants generate strong demand for screening and DAF systems due to high FOG levels, while oil & gas operations rely heavily on oil-water separation units like API separators and hydrocyclones. Stormwater treatment, holding around 10%, is emerging as a fast-growing area as regulations tighten on non-point source pollution, prompting cities to invest in separators and clarifiers for runoff management.

Market Share by Technology: Physical Separation Dominates Primary Treatment Approaches

By 2025, physical separation technologies are expected to command nearly 65% of the global primary treatment equipment market, emphasizing the reliance on gravity settling, screening, and flotation as the backbone of primary treatment processes. Mechanical separation, with about 20%, complements the by automating grit removal, skimming, and screening through rotating equipment and classifiers, which improve efficiency and reduce labor costs. Meanwhile, chemical treatment methods such as coagulation and flocculation hold a 15% share, acting as critical process enhancers to boost sedimentation and flotation efficiency, especially in industries with challenging effluent compositions. The balance of technologies reflects a strong demand for both tried-and-tested physical methods and the precision enhancements provided by integrated chemical dosing systems.

.png)

Market Share by Sales Channel: EPC Contracts Anchor Large-Scale Primary Treatment Projects

Engineering, Procurement, and Construction (EPC) contracts account for around 50% of market share in 2025, reflecting their dominance as the primary procurement model for large municipal and industrial plant developments. EPC firms are central because they integrate primary treatment systems like clarifiers, screens, and DAF units into holistic facility designs. Direct sales contribute about 25%, particularly where OEMs engage directly with large industrial operators such as global food processors, oil refineries, and power plants to supply high-value equipment tailored to site-specific needs. The remaining 25% is captured by distributors and OEM networks, which are essential for servicing smaller municipalities and mid-sized industries. They play a crucial role in aftermarket sales, supplying replacement screens, parts, and packaged units, thereby ensuring continuity of operations in distributed treatment facilities.

Country Analysis of the Primary Water and Wastewater Treatment Equipment Market

United States: Infrastructure Investment Driving Primary Treatment Equipment Demand

The United States is a key market for primary water and wastewater treatment equipment driven by massive government spending and regulatory encouragement. Over $50 billion was earmarked by the Bipartisan Infrastructure Law for improving national drinking water and wastewater infrastructure, stimulating demand for primary treatment technologies outright. Innovative solutions are being encouraged by the U.S. Environmental Protection Agency (EPA) to fill the "wastewater access gap," assisting communities in seeking funds for new and renewed wastewater infrastructure. Key players are deepening their market penetration: A.O. Smith Corporation has purchased Atlantic Filter (Florida) (2022) and Master Water Conditioning Corporation (Pennsylvania) (2021), while Xylem has bolstered its portfolio by acquiring Evoqua. DuPont has unveiled new FilmTec™ Fortilife™ membranes (CR100, XC70, XC120HR, XC160) offering enhanced brine concentration and energy efficiency for industrial wastewater treatment. Moreover, the Federal Energy Management Program (FEMP) considers on-site wastewater treatment system technologies as commercially ready solutions for diminishing the use of freshwater at federal facilities and testifies to the strategic role of primary treatment equipment in sustainable water management.

China: Regulatory Mandates and Industrial Expansion Driving Equipment Adoption

China’s primary water and wastewater treatment equipment market is experiencing robust growth, driven by ambitious government targets and industrial expansion. The government aims for 95% wastewater treatment coverage in county-level cities, incentivizing investment in advanced primary treatment technologies. SUEZ established a joint venture with Shandong Public to build and operate an industrial wastewater treatment plant in the Jining New Materials Industrial Park, implementing high-efficiency treatment solutions. China’s 12th Five-Year Plan allocated RMB 430 billion for urban wastewater infrastructure, focusing on sewage pipeline expansion and enhancing treatment capacity. Policy initiatives targeting pollutants such as chemical oxygen demand (COD), ammonia nitrogen (NH4), and total phosphorus further drive demand for equipment capable of efficient primary treatment. The adoption of the polluter-pays principle encourages companies to invest in high-performance primary treatment systems, reducing effluent discharge fees while meeting regulatory compliance.

India: Government Programs and Technological Innovation Boost Market Growth

India's primary water and wastewater treatment equipment market is being driven by government big-ticket programs and innovation from the private sector. Namami Gange has approved 488 projects costing more than ₹39,730 crore, largely aimed at developing and rejuvenating sewage treatment capacity and augmenting sewer infrastructure in the Ganga basin. MIDC has entrusted Enviro Infra Engineers with ₹395.5 crore projects for installation of Zero Liquid Discharge (ZLD) facilities with primary treatment steps, while Technocraft Ventures has a healthy order book of AMRUT and Namami Gange projects. The Jal Jeevan Mission is augmenting potable water infrastructure with preliminary treatment of raw water sources. Larsen & Toubro's (L&T) Water Business Group is continuing with installation of big-ticket water supply schemes and wastewater treatment projects, boosting India's primary treatment equipment market and promoting sustainable water management.

Germany: Advanced Membrane Technologies and Green Innovations

Germany is a prominent market for primary water and wastewater treatment equipment in Europe, driven by stringent EU Water Framework Directive regulations and sustainability commitments. The country is at the forefront of integrating advanced technologies such as membrane bioreactors (MBR) with primary treatment processes to enhance overall efficiency. Germany’s dedication to green technology and resource recovery is fostering innovations in primary sludge treatment and energy recovery from wastewater. Companies like Veolia are deploying smart solutions with sensors and application software to monitor wastewater treatment plants, optimizing primary treatment performance and cost-efficiency. Kurita Water Industries has also emphasized expansion in wastewater management solutions, reflecting Germany’s strategic importance as a hub for advanced primary water treatment technology adoption.

Japan: Disaster-Resilient and Portable Primary Treatment Solutions

Japan’s primary water and wastewater treatment equipment market emphasizes innovation in disaster-resilient and portable solutions. WOTA Corp., a Japanese startup, has developed a small-scale, portable water recycling system capable of reclaiming over 98% of wastewater, deployed in areas affected by the 2024 Noto Peninsula Earthquake. METAWATER Group received an order from the Tokyo Metropolitan Government for sludge incinerator equipment removal at the Nambu Sludge Treatment Plant, demonstrating ongoing infrastructure modernization. Japan’s focus on disaster preparedness and resource scarcity has encouraged the development of portable, decentralized water and wastewater treatment systems, incorporating primary filtration components for reliable water supply in emergencies. The government and private sector are actively promoting technologies for water reuse and recycling to optimize resource efficiency.

Israel: Leading Innovations in Desalination and Primary Filtration

Israel is a global leader in water management, with primary water and wastewater treatment equipment playing a central role in large-scale desalination and reuse projects. IDE Water Technologies’ Sorek 2 – Be'er Miriam Desalination Plant, operational in March 2025, is the world’s first steam-driven seawater reverse osmosis (SWRO) facility, showcasing energy-efficient primary filtration systems. The Sorek I and Hadera plants also employ advanced primary treatment equipment to ensure the quality of incoming seawater for desalination. Israel’s national strategy for water reuse has fostered a strong domestic market for primary treatment equipment and positioned the country as a hub for exporting innovative water solutions globally.

Competitive Landscape of the Primary Water and Wastewater Treatment Equipment Market

The competitive landscape for primary water and wastewater treatment equipment is shaped by global leaders with strong engineering expertise, extensive portfolios, and strategic investments in smart automation, modular design, and resource recovery technologies. Leading companies are increasingly offering integrated solutions that link primary clarification, grit removal, and screening systems with downstream treatment processes, ensuring end-to-end operational efficiency.

Xylem Inc. – Expanding Integrated Primary Treatment Portfolios

Xylem supplies diverse primary treatment options such as coarse and fine screening, grit removal systems, and high-capacity clarifiers. Through brands such as Flygt and Sanitaire, Xylem balances mechanical toughness with smart controls to achieve maximum solids removal and energy efficiency. Through its 2023 purchase of Evoqua Water Technologies, Xylem grew its industrial application offerings and facilitates more complete solutions from screening at entry all the way to discharge. Xylem's focus on digital water management enables facilities to manage performance automation and decrease downtime and operating expense.

Veolia Environnement S.A. – Leveraging Smart Services for Upstream Efficiency

Veolia supplies the complete array of primary treatment equipment within larger-plant design, modernization, and operating contracts. It includes in its offerings screening facilities, grit tanks and dissolved air flotation clarifiers utilized to remove fats, oils, and grease. Veolia displays its intention of taking advantage of real-time monitoring and automation to boost efficiency with its 2025 rollout of smart wastewater services. It goes a step further and links primary treatment with energy recovery schemes within which clarifier sludges are utilized for fueling anaerobic digesters and producing renewable energy.

SUEZ S.A. – Compact, High-Rate Primary Clarification Solutions

SUEZ's primary treatment approach is space-efficient and is therefore applicable both within urban and retrofit contexts. Its high-end screening and grit removal technologies safeguard downstream infrastructure with minimal footprint. High investment is made by SUEZ in R&D to engineer high-rate clarifiers that can accommodate fluctuant influent quality. WRT is additionally tied to waste-to-energy schemes by the company and is witnessed within its 2024 Toulouse concession project where sludge energy recovery is incorporated within larger municipal waste facilities.

Pentair plc – Modular Primary Treatment for Industrial Efficiency

Pentair engineers mechanical separations and clarifiers for industrial and commercial applications where modular configurations can enable quick mobilization. Its technologies serve specialized industries such as food and beverage processing where pre-treatment is essential before downstream contamination can occur. The 2024 purchase of Porous Media added Pentair's filtration and separations offering and enhanced its capabilities of providing integrated primary and pre-filtration applications that consume less water and energy.

DuPont Water Solutions – Pre-Treatment Integration for Advanced Filtration

DuPont is expert at high-efficiency membrane and high-performance filtration technologies, yet its performance is only possible with successful upstream protection. DuPont pre-filtration and clarifiers protect ultrafiltration and reverse osmosis membranes from fouling. Its FilmTec™ Prime RO membranes introduced in 2025 are designed to have longer service life and hence give rise to highly efficient primary sedimentation and solid removal. DuPont cooperates with utilities and industrial customers and brings the primary and advanced treatment steps together in smooth, high-reliability integrated systems.

Primary Water and Wastewater Treatment Equipment Market Report Scope

Primary Water and Wastewater Treatment Equipment Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$14.6 Billion

|

|

Market Size (2034)

|

$22.1 Billion

|

|

Market Growth Rate

|

4.7%

|

|

Segments

|

By Primary Water Treatment Equipment (Screening Equipment, Sedimentation & Clarification Systems, Coagulation & Flocculation Systems, Grit Removal Systems), By Primary Wastewater Treatment Equipment (Oil-Water Separators, Dissolved Air Flotation (DAF) Units, Primary Settling Tanks, Comminutors & Grinders), By Application (Municipal Water Treatment, Municipal Wastewater Treatment, Industrial Water Treatment, Food & Beverage, Oil & Gas, Mining, Power Plants, Stormwater Treatment), By Technology (Physical Separation, Chemical Treatment, Mechanical Separation), By Sales Channel (Direct Sales, Distributors & OEMs, EPC Contracts)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Xylem Inc., Pentair plc., Evoqua Water Technologies LLC (now part of Xylem), Aquatech International LLC, Ecolab Inc., DuPont, Calgon Carbon Corporation, Toshiba Water Solutions Private Limited, Veolia Group, Kurita Water Industries Ltd., SUEZ, Thermax Limited, Lenntech B.V., Parkson Corporation, Ovivo

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Primary Water and Wastewater Treatment Equipment Market Segmentation

By Primary Water Treatment Equipment

- Screening Equipment

- Sedimentation & Clarification Systems

- Coagulation & Flocculation Systems

- Grit Removal Systems

By Primary Wastewater Treatment Equipment

- Oil-Water Separators

- Dissolved Air Flotation (DAF) Units

- Primary Settling Tanks

- Comminutors & Grinders

By Application

- Municipal Water Treatment

- Municipal Wastewater Treatment

- Industrial Water Treatment

- Food & Beverage

- Oil & Gas

- Mining

- Power Plants

- Stormwater Treatment

By Technology

- Physical Separation

- Chemical Treatment

- Mechanical Separation

By Sales Channel

- Direct Sales

- Distributors & OEMs

- EPC Contracts

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Primary Water and Wastewater Treatment Equipment Market

- Xylem Inc.

- Pentair plc.

- Evoqua Water Technologies LLC (now part of Xylem)

- Aquatech International LLC

- Ecolab Inc.

- DuPont

- Calgon Carbon Corporation

- Toshiba Water Solutions Private Limited

- Veolia Group

- Kurita Water Industries Ltd.

- SUEZ

- Thermax Limited

- Lenntech B.V.

- Parkson Corporation

- Ovivo

* List Not Exhaustive

Research Coverage

This report investigates the Primary Water and Wastewater Treatment Equipment Market, delivering comprehensive analysis reviews of the trends, regulatory shifts, and technological breakthroughs that are redefining the industry. Prepared by USDAnalytics, the study highlights how circular economy models, smart automation, and modular system designs are driving efficiency and sustainability in primary treatment processes. It showcases how leading companies are leveraging innovations in grit removal, clarification, and dissolved air flotation systems while integrating resource recovery and IoT-enabled monitoring. This report is an essential resource for utilities, policymakers, and industrial operators seeking to align infrastructure investments with stricter compliance requirements and operational efficiency goals across global markets.

Scope Includes:

- Segmentation: By Equipment Type (Water Treatment, Wastewater Treatment), Application (Municipal, Industrial, Stormwater), Technology (Physical, Mechanical, Chemical), Sales Channel (EPC Contracts, Direct Sales, Distributors), and Geography

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa

- Timeframe: Historic data from 2021 to 2024 and forecast data from 2025 to 2034

- Companies: Analysis and profiles of 15+ leading companies shaping the global primary water and wastewater treatment equipment market

Methodology

The research methodology applied by USDAnalytics integrates primary and secondary approaches to ensure robust insights into the Primary Water and Wastewater Treatment Equipment Market. Primary research involved detailed interviews with equipment manufacturers, EPC contractors, regulators, and utilities to capture real-world adoption trends and challenges. Secondary research relied on government reports, industry white papers, regulatory filings, and company publications to validate findings. Market sizing was established using both top-down and bottom-up modeling techniques, followed by data triangulation and scenario analysis to ensure accuracy. Expert reviews and iterative validation rounds were applied to enhance reliability, making this report a dependable tool for strategic decision-making and investment planning.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Primary Water and Wastewater Treatment Equipment Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Insights for Industry Professionals

1.3. Global Market Snapshot

2. Primary Water and Wastewater Treatment Equipment Market Outlook (2025–2034)

2.1. Introduction to the Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $14.6 Billion

2.2.2. Forecasted Market Size (2034): $22.1 Billion at 4.7% CAGR

2.3. Market Drivers and Trends

2.3.1. Resource Recovery Integration

2.3.2. Efficiency Gains in Downstream Processes

2.3.3. Smart Monitoring and Automation

2.3.4. Scalable Modular Solutions

3. In-Depth Market Analysis and Recent Industry Developments

3.1. Overview of Market Transformation

3.2. Recent Acquisitions and Strategic Partnerships

3.2.1. Veolia's Final Acquisition of Water Technologies and Solutions

3.2.2. Xylem's Anaerobic Membrane Bioreactor Partnership

3.3. Product and Technological Innovations

3.3.1. Pentair's Everpure PFAS Reduction Systems

3.3.2. Solenis's Polymer Production Expansion

3.3.3. DuPont's FilmTec™ Fortilife™ Membranes

4. Key Trends Shaping the Future of Primary Treatment Equipment

4.1. AI-Driven Smart Screening Systems

4.1.1. Impact on Operational Efficiency and Cost Reduction

4.2. Regulatory Push for Microplastics Removal

4.2.1. Driving Upgrades in Grit and Fine Screen Technologies

4.3. Market Opportunities Driving Growth

4.3.1. Disaster-Resilient Primary Treatment Systems

4.3.2. Energy Recovery from Primary Sludge for Circular Economy

5. Market Share and Segmentation Insights

5.1. By Equipment Type

5.1.1. Primary Wastewater Treatment Equipment

5.1.2. Primary Water Treatment Equipment

5.2. By Application

5.2.1. Municipal Wastewater Treatment

5.2.2. Industrial Wastewater Pre-treatment

5.2.3. Industrial Raw Water Preparation

5.2.4. Stormwater Treatment

5.3. By Technology

5.3.1. Physical Separation

5.3.2. Mechanical Separation

5.3.3. Chemical Treatment

5.4. By Sales Channel

5.4.1. EPC Contracts

5.4.2. Direct Sales

5.4.3. Distributors & OEM Networks

6. Country Analysis & Regional Outlook

6.1. United States: Infrastructure Investment Driving Demand

6.2. China: Regulatory Mandates and Industrial Expansion

6.3. India: Government Programs and Technological Innovation

6.4. Germany: Advanced Membrane Technologies and Green Innovations

6.5. Japan: Disaster-Resilient and Portable Solutions

6.6. Israel: Leading Innovations in Desalination and Primary Filtration

7. Primary Water and Wastewater Treatment Equipment Market Size Outlook by Region (2025–2034)

7.1. North America Market Size Outlook to 2034

7.1.1. By Primary Water Treatment Equipment

7.1.2. By Primary Wastewater Treatment Equipment

7.1.3. By Application

7.1.4. By Technology

7.1.5. By Sales Channel

7.2. Europe Market Size Outlook to 2034

7.2.1. By Primary Water Treatment Equipment

7.2.2. By Primary Wastewater Treatment Equipment

7.2.3. By Application

7.2.4. By Technology

7.2.5. By Sales Channel

7.3. Asia Pacific Market Size Outlook to 2034

7.3.1. By Primary Water Treatment Equipment

7.3.2. By Primary Wastewater Treatment Equipment

7.3.3. By Application

7.3.4. By Technology

7.3.5. By Sales Channel

7.4. South America Market Size Outlook to 2034

7.4.1. By Primary Water Treatment Equipment

7.4.2. By Primary Wastewater Treatment Equipment

7.4.3. By Application

7.4.4. By Technology

7.4.5. By Sales Channel

7.5. Middle East and Africa Market Size Outlook to 2034

7.5.1. By Primary Water Treatment Equipment

7.5.2. By Primary Wastewater Treatment Equipment

7.5.3. By Application

7.5.4. By Technology

7.5.5. By Sales Channel

8. Company Profiles: Leading Players in the Primary Water and Wastewater Treatment Equipment Market

8.1. Xylem Inc.

8.2. Veolia Group

8.3. SUEZ

8.4. Pentair plc.

8.5. DuPont Water Solutions

8.6. Ecolab Inc.

8.7. Aquatech International LLC

8.8. Calgon Carbon Corporation

8.9. Kurita Water Industries Ltd.

8.10. Thermax Limited

8.11. Parkson Corporation

8.12. Ovivo

8.13. Toshiba Water Solutions Private Limited

8.14. Lenntech B.V.

8.15. Evoqua Water Technologies LLC (now part of Xylem)

9. Research Coverage & Methodology

9.1. Report Scope and Focus

9.2. Research Methodology

9.3. Deliverables

10. Appendix

10.1. List of Tables

10.2. List of Figures

10.3. Abbreviations