Secondary Water and Wastewater Treatment Equipment Market Overview

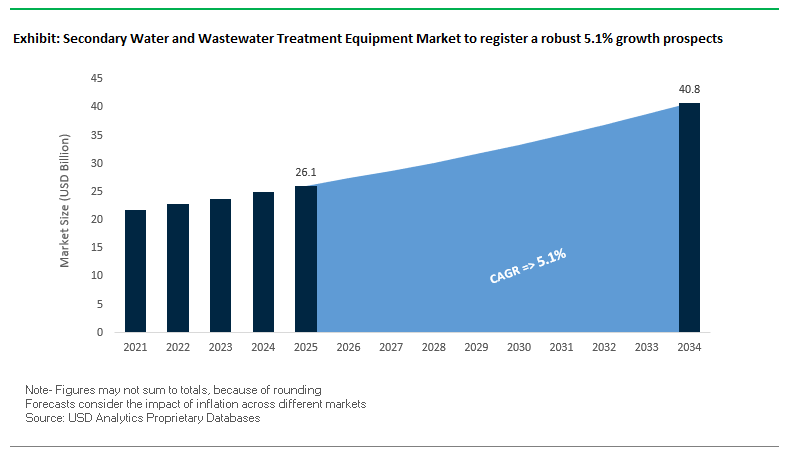

The global secondary water and wastewater treatment equipment market is projected to grow from $26.1 billion in 2025 to $40.8 billion by 2034, at a steady CAGR of 5.1%. The growth is fueled by increasingly stringent environmental regulations, rapid urbanization, water scarcity concerns, and the adoption of advanced treatment technologies.

Municipal officials and industry specialists contemplate solutions that are not only compliant but that optimize performance and aid water reuse applications. From nutrient reduction technologies to software optimization platforms, market drivers are being driven by regulatory imperatives and sustainability objectives.

Key Insights for Industry Stakeholders

- Regulatory Drivers: EU and North America lead in enforcing strict nutrient removal standards, spurring demand for nitrogen and phosphorus reduction technologies.

- Smart Treatment Plants: IoT, AI, and real-time data analytics are being integrated into secondary treatment, cutting aeration energy use by up to 25% while improving process control.

- Decentralized Treatment Adoption: Modular MBR and MBBR systems are gaining traction for urban areas with limited space.

- Water Reuse Momentum: Rising water scarcity is boosting the adoption of high-quality effluent reuse in agriculture, industry, and aquifer recharge.

Market Analysis: Digital Transformation, Resource Recovery, and Strategic Expansions Define 2024–2025

The market of secondary wastewater treatment equipment is in the midst of a transformation driven by technological convergence, investment in resource recovery, and rising global environmental pledges. Veolia closed the purchase of the rest of the 30% interest in its business of Water Technologies and Solutions in July 2025 and it is bolstering its integrated portfolio and streamlining its organization. This is consistent with the industry-wide movement toward integrated, vertically integrated treatment solutions.

In April 2025, Pentair received Kitchen Innovations Awards for its Everpure PFAS Reduction Systems, evidencing growing interest in end-of-secondary treatment technologies against emerging contaminants. Meanwhile, SUEZ's 20-year December 2024 concession of two French waste-to-energy plants is evidence of the growth of co-operation between wastewater treatment and green energy production, particularly through sewage sludge-to-biomethane projects.

Partnerships involving technology are also defining the horizon. Xylem announced its next-gen AnMBR (Anaerobic Membrane Bioreactor) commercial partnership in September 2024, marking a move toward high-efficiency biogas-generating systems. Likewise, Pentair's purchase of Porous Media in October 2024 and Solenis' Feb. 2024 $193 million expansion of PVAm polymer manufacturing show strategic investment toward better filtration, separations, and biological treatment capabilities. Supplementing these developments, Veolia's introduction of SCADA-based smart wastewater services in June 2025 confirms the increased role of digital optimization toward performance and compliance goals.

Key Market Trends Driving Innovation in Secondary Water and Wastewater Treatment Equipment

Membrane Bioreactor (MBR) Dominance in Nutrient-Sensitive and Space-Constrained Regions

Membrane Bioreactor (MBR) technology is increasingly being used to replace traditional Activated Sludge Process (ASP) configurations where nutrient discharge limitations occur. MBRs produce higher effluent quality with considerably higher removals of total phosphorus (TP) and total nitrogen (TN), making it possible for the effluent water to be used for water reuse and irrigation purposes.

One comparative investigation revealed MBRs were better than ASP systems, consistently generating cleaner water and using up to 40% less space because of their space-saving geometry. Adoption of membrane filtration instead of secondary settling tanks allows urban wastewater treatment plants to increase capacity without resorting to expensive land purchases. MBRs also achieve high biomass concentrations allowing conformance with increasingly stringent nutrient removal requirements and lowering chances of operational washout, a frequent drawback of conventional systems.

Mainstream Anammox Adoption for Energy-Neutral Wastewater Treatment

The anaerobic ammonium oxidation (Anammox) system is becoming a game-changer in reducing the 30-60% energy consumption typical of nitrification-denitrification. Without the need of using dissolved oxygen in nitrogen removal, Anammox reduces aeration requirement by 60% and reduces sludge yield by 90%.

Applications are growing from pilot projects up to full industrial wastewater treatment at full scale, particularly in pharmaceuticals, landfill leachate, and other ammonia-high waste streams. Over 30 plants worldwide have implemented the DEMON single-stage Anammox process. Increasingly considered a scalable, stable, and cost-effective solution for energy-neutral wastewater treatment, the technology is now.

High-Value Opportunities Transforming the Wastewater Treatment Equipment Landscape

Hybrid MBBR/IFAS Systems for High-Strength Industrial Wastewater

The pharmaceutical and beverage industries are fueling interest in hybrid Moving Bed Biofilm Reactor (MBBR) and Integrated Fixed-Film Activated Sludge (IFAS) system configurations to accommodate high organic loading. Hybrid configurations can accommodate cost-efficient upgrades of conventional ASP plants with minimal major capital investment.

Examples are the City & County of Broomfield upgrading to IFAS technology and attained stringent Total Nitrogen and Total Phosphorus reduction with no infrastructure expansion. MBBR system biofilm-coated plastic media allows microorganisms to survive industrial variations of load and achieve higher removal rates of COD and TSS within a reduced footprint.

Sidestream Treatment for Nutrient Load Reduction and Energy Recovery

Sludge dewatering return flow treatment is accountable for 35% or more of a facility's phosphorus load- sidestream treatment prevents main biological treatment process overload. It raises the carbon-to-nitrogen ratio and increases denitrification and optimum biogas yields at anaerobic digester facilities. Sidestream nitrogen removal retrofit like that of Hazen and Sawyer assures multi-million-dollar capital spending and enhanced plant performance. With rising energy recovery projects, sidestream treatment is a strategic investment and first priority for wastewater utilities where maximum resource recovery is desired.

Secondary Water and Wastewater Treatment Equipment Market Share Insights

Market Share by Equipment Type: Biological Systems Retain Core Dominance While MBRs Accelerate Growth

In 2025, biological treatment systems are projected to account for 63.8% of the global secondary water and wastewater treatment equipment market, underscoring their role as the backbone of organic pollutant and nutrient removal. Within the category, the activated sludge process (ASP) continues as the industry workhorse, representing about 25% of total market share, particularly in large municipal wastewater treatment plants (WWTPs). However, membrane bioreactors (MBRs), expected to capture 18% of the market, are reshaping the competitive landscape due to their smaller footprint, superior effluent quality, and suitability for water reuse applications. Their growing adoption, supported by declining membrane costs, makes MBRs the highest-growth segment within secondary treatment.

.png)

Market Share by Application: Municipal Wastewater Treatment Plants Lead While Industrial Demand Rises

The municipal wastewater treatment plants (WWTPs) segment holds the largest market share at 61.8% in 2025, driven by global mandates requiring secondary treatment as a minimum standard for municipal effluent discharge. Growth is further supported by urbanization, plant expansions, and regulatory upgrades. In contrast, industrial wastewater treatment accounts for nearly 30%, representing a high-value sector where treatment systems must be tailored to complex and variable effluent streams. Industries such as food & beverage demand robust biological solutions like MBBR to handle high BOD/COD loads, while pharmaceutical facilities are increasingly reliant on advanced oxidation processes (AOPs) following biological treatment to address trace chemical pollutants. Meanwhile, water reuse and recycling systems, holding around 10%, stand out as a strategic growth area, with almost exclusive reliance on advanced MBR and hybrid systems to produce reclaimed water that meets stringent reuse standards.

Market Share by End-User: Municipal Utilities Anchor the Market While Industrial Buyers Expand Investment

Municipalities and public utilities dominate with a projected 55% market share in 2025, reflecting their responsibility for large-scale wastewater treatment infrastructure and compliance with stricter nutrient discharge standards. Their long-term planning cycles and budget-driven procurement decisions ensure steady demand for established technologies like ASP, while leaving room for adoption of hybrid nutrient removal solutions. Industrial facilities, contributing about 35%, represent a diverse but highly value-driven end-user base, investing in advanced systems to meet compliance requirements and reduce freshwater dependency through reuse. Within the segment, cost efficiency and operational reliability are the decisive factors. The commercial and institutional sub-segment, holding roughly 10%, remains a niche but notable buyer group, consisting of universities, hospitals, and resorts deploying packaged treatment plants that prioritize compactness, automation, and low OPEX.

Market Share by Technology: Suspended Growth Processes Dominate While Hybrid Systems Gain Momentum

Suspended growth processes such as ASP and sequencing batch reactors (SBR) are expected to capture nearly 50% of market share in 2025, continuing their dominance as the global standard for municipal secondary treatment. Their widespread use reflects decades of operational reliability, familiarity, and scalability across urban wastewater treatment plants. However, attached growth systems like moving bed biofilm reactors (MBBR) and rotating biological contactors (RBC) are set to capture around 30%, driven by their resilience in handling shock loads and their efficiency in retrofit applications where space is limited. Hybrid systems, representing approximately 20%, are gaining traction as utilities increasingly adopt Integrated Fixed-Film Activated Sludge (IFAS) designs to optimize treatment within existing tanks, particularly to meet stringent nutrient removal mandates without costly new infrastructure.

Country Analysis of the Secondary Water and Wastewater Treatment Equipment Market

United States: Infrastructure Funding and Technological Expansion Drive Secondary Treatment

The United States is a main market for secondary water and wastewater treatment equipment, fueled by heavy federal investment and corporate growth. Over $50 billion has been devoted by the Bipartisan Infrastructure Law toward drinking water and wastewater system upgrades across the nation, placing a direct demand boost on secondary treatment technologies. U.S. Environmental Protection Agency (EPA) regulatory push seeks to eliminate the "wastewater access gap," encouraging both municipal and industrial adoption of higher-end secondary treatment solutions. Top players are building out capabilities: Xylem Inc.'s procurement of Evoqua bolsters secondary wastewater treatment capabilities within North America and Europe, and Ecolab's procurement of Barclay Water Management in 2024 enhances its offerings within advanced secondary treatment equipment. Innovations at the research level are influencing the market as well, with the University of North Carolina at Charlotte advancing NanoResin materials toward optimum removal of organic matter. Strategic acquisitions by A.O. Smith Corporation of Atlantic Filter within Florida (2022) and Master Water Conditioning Corporation within Pennsylvania (2021) further underscore strategic expansion within the market with the U.S. representing a high-growth region within secondary treatment equipment.

China: Policy-Driven Expansion of Secondary Treatment Solutions

China's secondary water and wastewater treatment equipment market is growing amidst stringent government regulations and 95% wastewater treatment targets. 95% wastewater treatment targets at the county-level city government level are spurring investment in sophisticated secondary treatment technologies. National policy initiatives aimed at chemical oxygen demand (COD), ammonia nitrogen (NH4), and total phosphorus are inducing strong demand for equipment that can eliminate these contaminants during secondary treatment steps. Urban wastewater treatment and recycling infrastructure was earmarked at RMB 430 billion under the 12th Five-Year Plan and aimed at improving sewage pipeline and treatment network expansions. SUEZ is constructing an industrial wastewater treatment works at Jining New Materials Industrial Park in partnership with its joint venture partner Shandong Public using sophisticated technology that can recycle up to 100% wastewater. These projects show China's strategic move toward sustainable wastewater management using effective secondary treatment technologies.

India: Government Programs and Innovative Technologies Fuel Market Growth

India's water and wastewater treatment equipment market is significantly driven by government-wide programs and technological breakthroughs. The Namami Gange program has approved 488 projects costing more than ₹39,730 crore with attention on expansion of sewage treatment capacity and rehabilitation of the Ganga basin. Firms such as Enviro Infra Engineers are carrying out projects of Zero Liquid Discharge (ZLD) with secondary treatment steps, while Technocraft Ventures has a strong order book of projects under AMRUT and Namami Gange. Guidelines have been issued by the Central Pollution Control Board (CPCB) to encourage the reuse of treated wastewater for agricultural use, industrial cooling, and thermal power. Startups such as Earthy are constructing biomimetic membranes marketed under the tag of "Aquaporin Inside," using aquaporin proteins to move water very efficiently and offer sustainable secondary treatment solutions. Larsen & Toubro's Water Business Group is carrying out megascale drinking water and wastewater management projects and solidifying India's advanced water treatment equipment market.

Germany: Advanced Technologies and Smart Solutions in Secondary Treatment

Germany’s secondary water and wastewater treatment equipment market is shaped by stringent EU Water Framework Directive regulations and sustainability priorities. The market is seeing widespread adoption of membrane filtration, energy-efficient treatment systems, and innovative technologies to optimize secondary treatment processes. Companies like Veolia are deploying smart solutions combining sensors and applications for real-time monitoring of wastewater treatment plants, improving performance and cost efficiency. SUEZ’s contract with Silkeborg Spildevand A/S to upgrade Denmark’s Søholt wastewater treatment plant using biomass densification technology (inDense) highlights innovations by companies with significant operations in Germany. Ambitious climate targets aligned with the Paris Agreement are encouraging continued investment in technologies that enhance water quality and reduce energy consumption, positioning Germany as a leading European hub for secondary treatment equipment.

Saudi Arabia: Strategic Wastewater Infrastructure Expansion

Saudi Arabia’s secondary water and wastewater treatment equipment market is expanding under the National Water Strategy 2030, with significant investment in infrastructure projects. The Jeddah Airport 2 Independent Sewage Treatment Project (ISTP) utilizes Nereda technology, a biological treatment system employing activated sludge, to treat up to 500,000 m³/day. ACCIONA’s Madinah-3 Wastewater Treatment Plant serves over 1.1 million residents, with an initial capacity of 200,000 m³/day, expandable to 375,000 m³/day, and uses LUCAS technology for secondary biological treatment. The Taif Independent Sewage Treatment Plant employs Waterleau’s proprietary LUCAS® Cyclic Activated Sludge technology, integrating key secondary treatment phases in a compact, energy-efficient design. The Dammam plant is under construction with Moving Bed Biofilm Reactor (MBBR) technology, which leverages microorganisms to decompose organic waste during secondary treatment. These projects reflect Saudi Arabia’s strategic focus on modern, sustainable wastewater treatment solutions.

Japan: Disaster-Resilient and Portable Secondary Treatment Systems

Japan’s secondary water and wastewater treatment equipment market emphasizes innovation in disaster-resilient and portable systems. WOTA Corp. has developed a small-scale, portable water recycling system capable of reclaiming over 98% of wastewater, deployed in areas affected by the 2024 Noto Peninsula Earthquake. The Ministry of Land, Infrastructure, Transport, and Tourism (MLIT) promotes sewage sludge conversion into fertilizer and energy, utilizing secondary treatment equipment in recycling processes. Kurita Water Industries, in partnership with lunar exploration company ispace, plans to transport a water purification demonstration system to the moon after 2027, highlighting specialized secondary treatment technologies for extreme environments. Japan’s focus on decentralized, portable wastewater treatment systems including secondary filtration and biological treatment components ensures resilient water supply during emergencies and supports sustainable water reuse initiatives.

Competitive Landscape: Global Leaders Driving Smart, Sustainable, and Resource-Efficient Treatment

The competitive environment in the secondary wastewater treatment equipment market is defined by innovation, integrated solutions, and a growing emphasis on sustainability. Leading companies are expanding product portfolios, forming strategic partnerships, and adopting smart technologies to improve operational efficiency and meet stricter environmental standards.

Xylem Inc. – Driving Energy Efficiency Through Digital Optimization

Xylem has one of the widest secondary treatment portfolios, ranging from Sanitaire aeration systems to Wedeco disinfection technologies. Solutions include activated sludge, MBBR, clarifiers, and nutrient removal systems. The Xylem Edge Control platform, which is the company's offering, allows real-time process suggestions, saving up to 25% aeration energy. The September 2024 agreement to bring to market advanced AnMBR technology is an example of its dedication to resource recovery. The 2023 purchase of Evoqua Water Technologies brought considerable industrial treatment capabilities to Xylem.

Veolia Environnement S.A. – Integrated Solutions for Ecological Transformation

Veolia provides turnkey secondary treatment plants, such as activated sludge, MBR, and BNR technologies, in addition to its own AnoxKaldnes™ MBBR process. Its June 2025 "smart services" SCADA-based offering and energy-efficient Amonit™ system are indicative of its digitally driven strategy. The July 2025 complete purchase of WTS adds to its international reach and integration ability, especially in those projects that integrate water reuse with sludge-to-biogas energy recovery.

SUEZ S.A. – Compact, High-Performance Biological Processes

SUEZ specializes in high-efficiency biological treatment solutions to eliminate carbon, nitrogen, and phosphorus, even where space is limited. Its December 2024 waste-to-energy concession in France demonstrates its capability in sludge-to-biomethane transformation. SUEZ is also committing to micropollutant removal technologies, including PFAS-targeting processes, in response to tighter environmental regulations and expanding water reuse programs.

Pentair plc – Sustainable Solutions for Industrial and Commercial Applications

Pentair provides solid aeration, pumping, and separation solutions for industrial and municipal use. It is renowned for its durability and energy efficiency, and its packaged systems are well-suited to small-to-medium-size projects. In October 2024, the acquisition of Porous Media has expanded its filtration and separation capabilities as key to advanced secondary treatment and reuse processes.

DuPont Water Solutions – Advanced Membrane Technologies for Water Reuse

DuPont's secondary treatment solutions focus on its MemPulse MBR systems and high-end membrane filtration, such as UF, NF, and RO technologies. Its FilmTec Prime RO membranes, specifically designed with maximum fouling resistance, provide high-quality effluent that is safe for reuse. The December 2022 decentralized MBR project in India by the company showcases its innovation in compact, on-site treatment solutions designed to address local water reuse requirements.

Secondary Water and Wastewater Treatment Equipment Market Report Scope

Secondary Water and Wastewater Treatment Equipment Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$26.1 Billion

|

|

Market Size (2034)

|

$40.8 Billion

|

|

Market Growth Rate

|

5.1%

|

|

Segments

|

Biological Treatment Systems (Activated Sludge Process (ASP) Equipment, Biofilm Systems, Membrane Bioreactors, Lagoon Systems), Nutrient Removal Systems (Denitrification Filters, Biological Nutrient Removal (BNR) Systems, Chemical Phosphorus Removal Systems), Advanced Oxidation & Disinfection (Ozone Generators, UV Disinfection Units, Chlorine Contact Tanks), By Application (Municipal Wastewater Treatment Plants (WWTPs), Industrial Wastewater Treatment, Food & Beverage, Pharmaceuticals, Pulp & Paper, Textiles, Water Reuse & Recycling Systems), By End-User (Municipalities & Public Utilities, Industrial Facilities, Commercial & Institutional), By Technology (Suspended Growth Processes (ASP, SBR), Attached Growth Processes (MBBR, RBC), Hybrid Systems)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia, Xylem Inc., Ecolab, DuPont, Pentair, SUEZ, Kurita Water Industries, Evoqua Water Technologies (now part of Xylem), Calgon Carbon Corporation, Thermax Limited, VA Tech Wabag

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Secondary Water and Wastewater Treatment Equipment Market Segmentation

By Type

- Biological Treatment Systems

- Activated Sludge Process (ASP) Equipment

- Biofilm Systems

- Membrane Bioreactors

- Lagoon Systems

- Nutrient Removal Systems

- Denitrification Filters

- Biological Nutrient Removal (BNR) Systems

- Chemical Phosphorus Removal Systems

- Advanced Oxidation & Disinfection

- Ozone Generators

- UV Disinfection Units

- Chlorine Contact Tanks

By Application

- Municipal Wastewater Treatment Plants (WWTPs)

- Industrial Wastewater Treatment

- Food & Beverage

- Pharmaceuticals

- Pulp & Paper

- Textiles

- Water Reuse & Recycling Systems

By End-User

- Municipalities & Public Utilities

- Industrial Facilities

- Commercial & Institutional

By Technology

- Suspended Growth Processes (ASP, SBR)

- Attached Growth Processes (MBBR, RBC)

- Hybrid Systems

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Secondary Water and Wastewater Treatment Equipment Market

- Veolia

- Xylem Inc.

- Ecolab

- DuPont

- Pentair

- SUEZ

- Kurita Water Industries

- Evoqua Water Technologies (now part of Xylem)

- Calgon Carbon Corporation

- Thermax Limited

- VA Tech Wabag

* List Not Exhaustive

Research Coverage

This report investigates the Global Secondary Water and Wastewater Treatment Equipment Market, delivering in-depth analysis reviews of market dynamics, breakthrough technologies, and strategic shifts shaping the industry. Developed by USDAnalytics, the study highlights how regulatory compliance, urbanization, water scarcity, and sustainability goals are fueling investments in advanced treatment systems. It underscores how technologies such as MBR, Anammox, hybrid MBBR/IFAS, and digital optimization platforms are transforming the competitive landscape. With coverage of corporate expansions, M&A activities, and resource recovery initiatives, this report is an essential resource for utilities, industries, policymakers, and solution providers seeking actionable insights into the long-term opportunities and challenges of secondary treatment solutions.

Scope Includes:

- Segmentation: By Equipment Type (Biological Systems, MBR, ASP, MBBR, IFAS, AOPs), Application (Municipal, Industrial, Water Reuse), End-User (Utilities, Industrial, Commercial/Institutional), and Technology (Suspended Growth, Attached Growth, Hybrid Systems)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa

- Timeframe: Historic data from 2021–2024 and forecast data from 2025–2034

- Companies: Competitive analysis and profiles of 15+ global leaders and emerging innovators

Methodology

The research methodology applied by USDAnalytics combines both primary and secondary data collection techniques to ensure comprehensive and reliable market insights. Primary research included interviews with municipal utility managers, technology providers, EPC contractors, regulators, and industry stakeholders to capture real-world adoption patterns. Secondary research drew from regulatory databases, government publications, annual reports, technical papers, and recognized industry journals. Market sizing was conducted using both top-down and bottom-up approaches, followed by data triangulation, sensitivity analysis, and scenario forecasting to validate findings. The process was further refined through expert validation, ensuring that the projections and insights presented in this study provide a robust foundation for strategic decision-making.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Secondary Water and Wastewater Treatment Equipment Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Insights for Industry Stakeholders

1.3. Global Market Snapshot

2. Secondary Water and Wastewater Treatment Equipment Market Outlook (2025–2034)

2.1. Introduction to the Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $26.1 Billion

2.2.2. Forecasted Market Size (2034): $40.8 Billion at 5.1% CAGR

2.3. Key Drivers and Market Dynamics

2.3.1. Regulatory Drivers

2.3.2. Smart Treatment Plants

2.3.3. Decentralized Treatment Adoption

2.3.4. Water Reuse Momentum

3. In-Depth Market Analysis and Recent Industry Developments

3.1. Overview of Market Transformation

3.2. Mergers, Acquisitions, and Strategic Expansions

3.2.1. Veolia's Acquisition of Water Technologies and Solutions

3.2.2. Pentair's Everpure PFAS Reduction Systems

3.2.3. SUEZ's Waste-to-Energy Concession

3.3. Technological Partnerships and Capital Investments

3.3.1. Xylem's AnMBR Commercial Partnership

3.3.2. Pentair's Acquisition of Porous Media

3.3.3. Solenis's Polymer Manufacturing Expansion

3.3.4. Veolia's Smart Wastewater Services

4. Key Market Trends Driving Innovation

4.1. Membrane Bioreactor (MBR) Dominance

4.1.1. MBRs in Nutrient-Sensitive and Space-Constrained Regions

4.1.2. MBRs vs. Activated Sludge Processes (ASP)

4.2. Mainstream Anammox Adoption

4.2.1. Anammox for Energy-Neutral Wastewater Treatment

4.2.2. Global Implementation of Anammox

4.3. High-Value Opportunities

4.3.1. Hybrid MBBR/IFAS Systems for High-Strength Industrial Wastewater

4.3.2. Sidestream Treatment for Nutrient Load Reduction and Energy Recovery

5. Market Share and Segmentation Insights

5.1. By Equipment Type

5.1.1. Biological Treatment Systems

5.1.2. Nutrient Removal Systems

5.1.3. Advanced Oxidation & Disinfection

5.2. By Application

5.2.1. Municipal Wastewater Treatment Plants (WWTPs)

5.2.2. Industrial Wastewater Treatment

5.2.3. Water Reuse & Recycling Systems

5.3. By End-User

5.3.1. Municipalities & Public Utilities

5.3.2. Industrial Facilities

5.3.3. Commercial & Institutional

5.4. By Technology

5.4.1. Suspended Growth Processes

5.4.2. Attached Growth Processes

5.4.3. Hybrid Systems

6. Country Analysis and Regional Outlook

6.1. United States: Infrastructure Funding and Technological Expansion

6.2. China: Policy-Driven Expansion

6.3. India: Government Programs and Innovative Technologies

6.4. Germany: Advanced Technologies and Smart Solutions

6.5. Saudi Arabia: Strategic Wastewater Infrastructure Expansion

6.6. Japan: Disaster-Resilient and Portable Systems

6.7. Other Country Analysis (e.g., UK, France, Australia)

7. Secondary Water and Wastewater Treatment Equipment Market Size Outlook by Region (2025–2034)

7.1. North America Market Size Outlook to 2034

7.1.1. By Equipment Type

7.1.2. By Application

7.1.3. By End-User

7.1.4. By Technology

7.2. Europe Market Size Outlook to 2034

7.2.1. By Equipment Type

7.2.2. By Application

7.2.3. By End-User

7.2.4. By Technology

7.3. Asia Pacific Market Size Outlook to 2034

7.3.1. By Equipment Type

7.3.2. By Application

7.3.3. By End-User

7.3.4. By Technology

7.4. South America Market Size Outlook to 2034

7.4.1. By Equipment Type

7.4.2. By Application

7.4.3. By End-User

7.4.4. By Technology

7.5. Middle East and Africa Market Size Outlook to 2034

7.5.1. By Equipment Type

7.5.2. By Application

7.5.3. By End-User

7.5.4. By Technology

8. Company Profiles: Leading Players in Secondary Water and Wastewater Treatment Equipment Market

8.1. Veolia

8.2. Xylem Inc.

8.3. Ecolab

8.4. DuPont

8.5. Pentair

8.6. SUEZ

8.7. Kurita Water Industries

8.8. Evoqua Water Technologies (now part of Xylem)

8.9. Calgon Carbon Corporation

8.10. Thermax Limited

8.11. VA Tech Wabag

8.12. Aquatech International LLC

8.13. Lenntech B.V.

8.14. Parkson Corporation

8.15. Ovivo

9. Research Coverage & Methodology

9.1. Report Scope and Focus

9.2. Research Methodology

9.3. Deliverables

10. Appendix

10.1. List of Tables

10.2. List of Figures

10.3. Abbreviations