Containerized Water Treatment Systems Market Overview

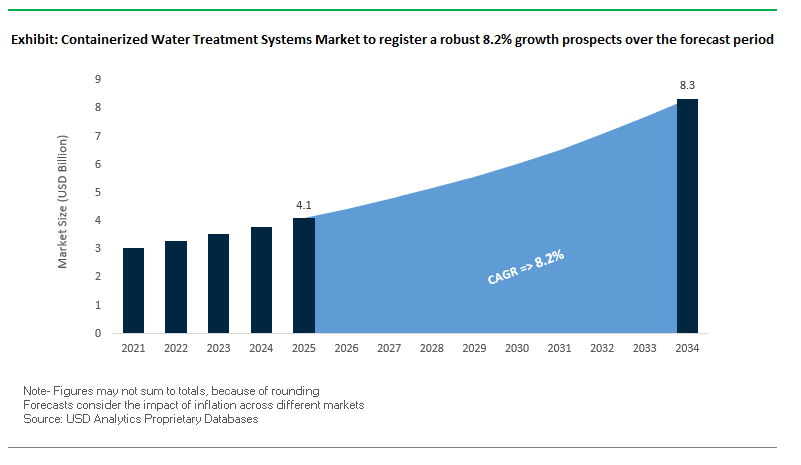

The containerized water treatment systems market is projected to expand from USD 4.1 billion in 2025 to USD 8.3 billion by 2034, representing a CAGR of 8.2%. The growth trajectory is supported by escalating demand for plug-and-play water purification systems that can be rapidly deployed across diverse applications, from industrial wastewater treatment in mining operations to emergency potable water supply in disaster-stricken areas.

Industry professionals continue to look at pre-assembled containerized water units due to their ability to save on on-site installation and civil works, facilitating near-immediate operational readiness. This is paramount in applications such as offshore oil and gas production facilities, seasonal or temporary industrial additions, and disaster relief. These systems' applications range to pharmaceutical, semiconductor, municipal, and distant community water supplies, further reinforcing their application across both developed and emerging markets.

Technically speaking, the market continues to be based on membrane technology, primarily reverse osmosis (RO) and ultrafiltration (UF) because they have a superior ability to produce high-quality waters through the rejection of dissolved solids, pathogens, and trace pollutants. Subsequent development phase will be stimulated by sustainability-focused innovation like low-energy membrane materials, optimally designed process arrangements, and higher water recovery ratios to meet corporate ESG targets and environmental policy drivers enacted by governments.

Strategic Imperatives for Shareholders:

- Invest in containerized systems with modular scalability to address both emergency and long-term water treatment needs.

- Target industries with high-purity water demands including pharmaceuticals, semiconductors, and food & beverage as key revenue drivers.

- Align R&D with energy efficiency and low-carbon footprint goals to meet regulatory and corporate sustainability benchmarks.

- Develop regional service hubs for faster deployment and maintenance support in high-growth markets.

Market Analysis: Strategic Deployments and Infrastructure Investments Fueling Growth

The containerized water treatment systems market is witnessing strong momentum as both private companies and governments prioritize rapid water infrastructure deployment. In August 2025, Veolia Water Technologies delivered a containerized ORION™ 2000S RO and CEDI unit to a major pharmaceutical manufacturer, enabling a 40% reduction in water footprint while boosting production capacity demonstrating how containerized systems are advancing sustainability alongside operational efficiency.

Veolia cemented further its offshore oil and gas market presence in September 2025 after winning a multi-million-dollar Petrobras contract for state-of-the-art seawater desalter units to be fitted aboard two FPSOs operating off Brazil. It illustrates a demand for small units of high reliability in space-limited applications.

SUEZ is also running large-scale initiatives, such as recently opening a 300,000 m³/day industrial membrane-based desalination plant in China on behalf of Wanhua Chemical Group. The plant features integrated containerized and modular concepts and has shown scalability in addressing huge industrial water requirements. Concurrently, SUEZ has announced three new initiatives in Singapore, China, and the Philippines involving digital integration, seawater desalination, and water reuse.

In municipal technology, Xylem Inc. launched the Rivo™ I system in August 2024, a flexible analyzer and control system allowing for real-time monitoring and accurate chemical dosing for municipal potable water, scalable to future network extension. H2O America's July 2025 acquisition of Quadvest in the North American market for USD 540 million covers more than USD 500 million dedicated for modernization of infrastructures to include containerized systems to supply fast-growing communities.

The market’s humanitarian and emergency segment continues to expand as well. SSI Aeration, Inc. has developed fully functional containerized wastewater treatment systems for disaster relief, remote military bases, and temporary construction sites. Government initiatives are also influencing growth, with Algeria announcing in October 2024 a USD 3 billion investment in six new desalination plants by 2030, where modular and containerized systems are expected to play a key role in achieving deployment timelines.

Trends and Opportunities in Containerized Water Treatment Systems Market

Trend 1: Military & Defense Sector Adoption for Forward Operations

Containerized water treatment units are increasingly becoming a part of global military forces' choices to provide secure, stand-alone water supply within forward operating bases, combat theaters, and humanitarian efforts. Military-specification units are capable of quick, stand-alone deployment within a matter of about 90 minutes employing minimal personnel, thus cutting down logistics reliance on bottled water supply. Highly versatile units can treat a variety of waters ranging from freshwater and brackish waters to seawater while efficiently eliminating chemical, biological, and radiological contaminants. Besides potable water production, special units such as the Deployable Aerobic Aqueous Bioreactor (DAAB) serve to treat wastewater within forward bases, treating up to 25,000 gallons a day and reducing risks associated with off-site waste transportation. Increased defense agencies' use of containerized systems is a testament to their tactical relevance in secure water supply, operational flexibility, and forward deployment effectiveness.

Trend 2: Modular Disaster Response Systems with Renewable Power Integration

Increased natural disaster occurrence has opened up possibilities for integrated containerized water treatment units powered by renewable energy like solar power or hybrid power. Such units help ensure a sustainable off-grid supply of drinking water where centralized infrastructures have been destroyed. Solar units used in disaster affected regions, for instance, can generate 0.5 cubic meters of drinking water per hour while powered by minimal energy without creating pollution like diesel engines. Such use of renewable energy helps achieve energy autonomy, lowers logistical costs, and makes environmentally friendly disaster response a reality. Such transportable units further need to be constructed to international levels of health and safety standards like EU directives and World Health Organization (WHO) requirements in a bid to supply hazard-free and consistent supplies of drinking water among affected populations.

Opportunity 1: Offshore Oil & Gas Industry Compliance

Offshore oil and gas operations pose a huge opportunity for containerized water treatment applications due to operating requirements and environmental regulations. Bilge and produced waters require treatment to within allowable limits of discharge, typically below a concentration level of 15 ppm oil-in-water. High-end units such as silicon carbide (SiC) ceramic membrane technology-based units can reach oil concentration levels below 1 ppm to meet stringent environmental regulations. These units also provide high purity waters needed in critical industrial applications such as boiler feed and water injection while reducing shore-based transportation of waters. Due to their compact size, ruggedness, and self-contained nature, containerized units become an attractive solution ideally suited to offshore platforms and FPSO-based Floating Production, Storage, and Offloading units.

Opportunity 2: Smart Cities & Temporary Urban Infrastructure

It's pushing cities to use flexible, scalable solutions such as containerized water treatment systems due to rapid urbanization and periodic spikes in population. At plant upgrade or maintenance times, these units can be used as bypass units to provide uninterrupted potable water supply. In fast-growing urban centers, municipal authorities can use modular containerized wastewater treatment plants to easily increase capacity without permanent facilities' attendant time and upfront capital investment. They can equally be utilized for event applications such as music festivals or sports events to create safe, potable water while preserving municipal infrastructure and limiting environmental harm due to single-use plastics. It makes containerized water treatment solutions indispensable to modern urban water management and disaster response.

Containerized Water Treatment Systems Market Share Insights

Market Share by System Type: Filtration Systems at the Core, Desalination as Strategic Growth

Filtration systems are projected to account for around 34.7% of the global containerized water treatment systems market by 2025, underscoring their role as the foundation of treatment trains. Technologies such as membrane bioreactors (MBR) and ultrafiltration (UF) are widely deployed across both water and wastewater treatment, ensuring solids and pathogen removal at scale. In contrast, desalination systems are the strategic growth engine, with containerized reverse osmosis (RO) units becoming indispensable in coastal cities, island economies, and arid regions where water scarcity is intensifying. The segment’s growth reflects a global push toward water security through decentralized desalination capacity.

.png)

Market Share by Container Size & Configuration: Standard ISO Containers Dominating Global Deployments

Standard ISO containers command nearly 60.6% of the market share, driven by their compatibility with international shipping and ease of multimodal transport. The global standardization minimizes deployment complexity, making ISO-based systems the preferred option for emergency mobilization and industrial rental fleets. Customized containers, while smaller in share, are increasingly favored in applications requiring multi-stage treatment trains or expanded layouts for complex industrial wastewater treatment. Their ability to optimize internal design makes them critical in niche high-performance deployments.

Market Share by Mobility & Deployment: Plug-and-Play Systems as the Industry Benchmark

Plug-and-play containerized treatment units represent about 48.6% of global market share, solidifying their role as the most desirable deployment configuration. Pre-assembled, factory-tested, and requiring only basic onsite connections, these systems significantly reduce installation risks and commissioning delays, aligning with the industry’s demand for fast, reliable, low-risk deployments. Skid-mounted systems remain prominent in semi-permanent installations where containerized shelters double as stable enclosures. Meanwhile, rapid deployment systems continue to gain traction in disaster response and defense sectors, reflecting heightened demand for tactical mobility and resilience in water supply.

Market Share by End-Use Industry: Industrial Sector Retains Lead, Municipal Adoption Accelerating

The industrial sector leads the containerized water treatment systems market with about 44.8% share, leveraging these solutions for temporary process water, wastewater pretreatment, and utilities in remote mining and oil & gas operations. The dominance is fueled by industries valuing mobility, scalability, and reduced downtime during expansions or turnarounds. Municipal and public utilities are emerging as a critical growth driver, with containerized plants deployed for emergency backup, rural water supply, and decentralized capacity expansion in underserved areas. The commercial sector remains niche, concentrated in resorts, islands, and construction camps, where self-contained water independence is both strategic and cost-effective.

Market Share by Level of Automation: Fully Automated Systems Defining Market Leadership

Fully automated systems account for approximately 56.1% of market share, reflecting the industry’s move toward SCADA/IoT-enabled, remotely monitored water treatment plants. By reducing dependence on local operator expertise, these units ensure consistent compliance and operational reliability in remote or critical infrastructure applications. Semi-automated systems provide a balanced option for industrial users and smaller municipalities that can staff operators while seeking partial automation benefits. Manual operation systems are limited to low-resource settings, where capital constraints outweigh performance consistency, making them a shrinking segment as automation adoption accelerates globally.

Country Analysis of the Containerized Water Treatment Systems Market

United States: Rapid-Deployment Systems for Infrastructure Upgrades and Emergencies

The U.S. containerized water treatment systems market is fueled by investments made in the Bipartisan Infrastructure Law, dedicating more than $50 billion to improve drinking water and sewer systems, including replacing lead service lines and cleaning up PFAS contamination. Plug-and-play containerized systems find wider application to provide uninterruptable water service while these upgrades are carried out. Fluence Corporation's application of Membrane Aerated Biofilm Reactor (MABR) containerized systems in Colorado and Indiana demonstrates a wider demand for municipal applications of scalable and modular solutions. Portable treatment units find applications in demand during emergencies, military camps, mining centers, and temporary industry applications, where quick installation and operational adaptability become essential.

China: Compact, IoT-Enabled Systems for Industrial and Environmental Compliance

China's market for containerized water treatment plants is on the rise due to governmental initiatives like the policies of the Ministry of Water Resources advocating for water conservation and the Water Pollution Control Law's secondary list of hazardous water pollutants. Such initiatives generate demand for small-footprint, energy-sipping treatment plants that can facilitate advanced water reuse. Technologies like membrane filtration and monitoring by IoT are gaining popularity, while containerized plants become a frequent constituent of industrial parks to treat and recover process water. Such a development is aligned with Chinese overall environment protection policies and rising concerns about sustainable use of water.

India: Rural Access and Innovative Modular Solutions

India's Jal Jeevan Mission focuses on safe drinking water in rural homes, inducing the use of containerized and modular potable water systems in places where centralized systems aren't economical. Government initiatives such as AMRUT 2.0 and the Water Technology Initiative (WTI) facilitate startups and R&D in decentralized water technology. Organizations use "water ATMs" and containerized treatment plants to supply potable water in water-deficit states. Grants and financial incentives promote innovative use of water technology while making containerized water treatment a key element of India's urban and rural water system.

Saudi Arabia: Flexible Containerized Solutions for Industrial and Municipal Needs

Saudi Arabia is investing heavily in wastewater and industrial water infrastructure under its National Water Strategy 2030. Containerized reverse osmosis (RO) plants and T-MBBR wastewater systems are being deployed to provide rapid, flexible solutions for municipal, industrial, and agricultural applications. Enviromatch Inc. has delivered containerized plants in Dammam with capacities up to 7,200 m³/day, meeting WHO and SASO standards. Large-scale infrastructure projects, such as new cities and industrial parks, drive further demand for temporary and permanent containerized water treatment solutions, highlighting their role in project commissioning and operational efficiency.

Japan: Disaster-Ready and Compact Modular Water Treatment Units

Japan’s emphasis on disaster preparedness has accelerated innovation in portable, decentralized, and containerized water treatment systems. Kubota Corporation’s advanced membrane bioreactor (MBR) technology allows for downsized, efficient containerized treatment plants suitable for rapid deployment. Nansei Corporation’s modular approach, including collaboration on systems like NK-O3 BlueBallast, demonstrates the focus on compact, low-maintenance solutions. These innovations support emergency water supply, decentralized wastewater treatment, and scalable containerized solutions across urban and remote areas.

Germany: Modular, Energy-Efficient Containerized Water Solutions

Germany is witnessing growing adoption of flexible, containerized wastewater treatment plants designed for rapid deployment in locations lacking centralized sewer connections. Companies are integrating energy-efficient membrane filtration technologies into modular units to support decentralized applications and pilot projects. The German Association for Gas and Water (DVGW) promotes innovation and water protection, encouraging containerized systems that support the circular economy and sustainable wastewater management. Regulatory compliance and emphasis on high-quality standards drive the development of plug-and-play containerized water treatment solutions across municipal, industrial, and decentralized applications.

Competitive Landscape: Leading Players in Containerized Water Treatment Systems

The containerized water treatment systems market is dominated by global leaders that combine advanced membrane technology, digital integration, and rapid deployment expertise. Their competitive edge lies in delivering scalable, high-performance systems across industrial, municipal, and emergency sectors.

Veolia Environnement S.A. – Comprehensive Solutions for High-Purity and Sustainable Water Treatment

Veolia has a portfolio diversified across UF, RO, and CEDI-based containerized systems, and its ORION™ family has been particularly developed to serve high purity applications like pharmaceutical and cosmetic water. Its strategy centers on water reuse, resource recovery, and ecological reinvention that has been supported by Latin American and Southeast Asian growth. Veolia's plants typically integrate a number of processes spanning desalination to wastewater reclamation alongside end-to-end operating services.

SUEZ S.A. – Flexible, Digitally-Enhanced Water Infrastructure for Industrial and Municipal Clients

SUEZ provides optimized rapid deployment and remote monitoring containerized RO and MBR solutions. It is known for digital water management platforms that maximize energy use and regulatory compliance. Its landmark projects like the Wanhua Chemical Group desalination plant mark it out as a capable provider to serve large-scale industrial applications and bespoke municipal solutions on a par.

Xylem Inc. – Smart, Modular, and Interconnected Water Solutions

Xylem's approach is based on plug-and-play modularity, integrating computer and hardware control systems to provide maximum flexibility. System Rivo I exemplifies a dedication to automation, scalability, and precise process control. Through telemetry and analytical knowhow in data, Xylem's containerized solutions become a component within a comprehensive integrated smart water network, enhancing operational insight both at a municipal and industrial level.

Containerized Water Treatment Systems Market Report Scope

Containerized Water Treatment Systems Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.1 Billion

|

|

Market Size (2034)

|

$8.3 Billion

|

|

Market Growth Rate

|

8.2%

|

|

Segments

|

By System Type (Filtration Systems, Disinfection Systems, Desalination Systems, Specialized Treatment Systems), By Container Size & Configuration (Standard ISO Containers, Customized Containers), By Mobility & Deployment (Skid-Mounted, Plug-and-Play, Rapid Deployment, Truckable), By End-Use Industry (Municipal & Public Utilities, Industrial, Commercial), By Level of Automation (Manual Operation, Semi-Automated, Fully Automated)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia, Xylem Inc., SUEZ, Evoqua Water Technologies (now part of Xylem), Fluence Corporation, Sustainable Biosolutions Private Limited (SUSBIO), Toshiba Water Solutions, VA Tech Wabag Ltd., Thermax Limited, Ion Exchange India Ltd., Corix Water System, RWL Water

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Containerized Water Treatment Systems Market Segmentation

By System Type

- Filtration Systems

- Reverse Osmosis (RO)

- Ultrafiltration (UF)

- Nanofiltration (NF)

- Media Filtration

- Disinfection Systems

- UV Purification

- Ozonation

- Chlorination

- Electrochlorination

- Desalination Systems

- Specialized Treatment Systems

By Container Size & Configuration

- Standard ISO Containers

- Customized Containers

- Expandable

- Stackable

- Hybrid

By Mobility & Deployment

- Skid-Mounted

- Plug-and-Play

- Rapid Deployment

- Truckable

By End-Use Industry

- Municipal & Public Utilities

- Industrial

- Oil & Gas

- Mining

- Power Plants

- Food & Beverage

- Military & Defense

- Commercial

By Level of Automation

- Manual Operation

- Semi-Automated

- Fully Automated

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Containerized Water Treatment Systems Market

- Veolia

- Xylem Inc.

- SUEZ

- Evoqua Water Technologies (now part of Xylem)

- Fluence Corporation

- Sustainable Biosolutions Private Limited (SUSBIO)

- Toshiba Water Solutions

- VA Tech Wabag Ltd.

- Thermax Limited

- Ion Exchange India Ltd.

- Corix Water System

- RWL Water

* List Not Exhaustive

Research Coverage

This report investigates the Global Containerized Water Treatment Systems Market, presenting analysis reviews of rapid deployment models, high-purity industrial applications, and technological breakthroughs driving adoption across sectors. Published by USDAnalytics, it highlights how industries from pharmaceuticals and semiconductors to oil & gas and municipalities are leveraging pre-assembled, plug-and-play containerized units to minimize downtime and civil works. The study examines the evolution of RO and UF membrane technologies, integration of renewable energy, modular scalability, and ESG-driven innovations that are reshaping the sector’s growth trajectory. With detailed insights into regional policies, defense and disaster response adoption, and corporate investments in fleet expansion, this report is an essential resource for industry professionals, regulators, and investors evaluating the future of containerized water treatment solutions.

Scope Includes:

- Segmentation: By System Type (Filtration, Desalination, Wastewater Treatment, Hybrid), By Container Size (Standard ISO, Customized), By Deployment (Plug-and-Play, Skid-Mounted, Rapid Deployment), By End-Use Industry (Industrial, Municipal, Commercial, Humanitarian/Defense), and By Automation (Manual, Semi-Automated, Fully Automated).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Historic & Forecast: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies: Profiles and strategic analysis of 15+ leading companies including Veolia, SUEZ, Xylem, DuPont, and Fluence Corporation.

Methodology

The research methodology adopted by USDAnalytics combines primary and secondary approaches to provide a balanced, data-driven perspective. Primary research involved structured interviews with utilities, industrial operators, EPC contractors, regulators, and technology providers to validate adoption trends and deployment challenges. Secondary research drew on regulatory filings, trade publications, technical journals, and company disclosures to capture global market dynamics. Market sizing and forecasts were derived through both top-down and bottom-up approaches, reinforced with triangulation across geographies, system types, and end-use industries. Scenario modeling of policy enforcement, emergency response demand, and industrial expansion cycles was also applied, ensuring robust and forward-looking insights into the containerized water treatment systems market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Containerized Water Treatment Systems Market

Table of Contents: Containerized Water Treatment Systems Market

1. Executive Summary

1.1. Market Highlights

1.2. Strategic Imperatives for Shareholders

1.3. Global Market Snapshot

2. Containerized Water Treatment Systems Market Overview (2025–2034)

2.1. Introduction to the Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $4.1 Billion

2.2.2. Forecasted Market Size (2034): $8.3 Billion at 8.2% CAGR

2.3. Key Drivers and Market Dynamics

2.3.1. Demand for Rapid-Deployment and Plug-and-Play Systems

2.3.2. Versatility Across Industrial, Municipal, and Emergency Applications

2.3.3. Technological Advancements in Membrane Technology (RO, UF)

2.3.4. Sustainability-Focused Innovation and ESG Goals

3. Market Analysis: Strategic Deployments and Infrastructure Investments

3.1. Overview of Market Momentum

3.2. Strategic Developments of Key Players

3.2.1. Veolia's High-Purity Water Solutions and Offshore Contracts

3.2.2. SUEZ's Large-Scale Industrial Plants and Digital Integration

3.2.3. Xylem's Smart Control Systems and Municipal Initiatives

3.3. Government and Humanitarian Initiatives

3.3.1. Global Investments in Desalination and Infrastructure Modernization

4. Trends and Opportunities in Containerized Water Treatment Systems

4.1. Trend 1: Military & Defense Sector Adoption for Forward Operations

4.1.1. Secure, Stand-Alone Water Supply for Remote Bases

4.1.2. Versatility in Treating Diverse Water Sources

4.2. Trend 2: Modular Disaster Response Systems with Renewable Power

4.2.1. Off-Grid Water Supply in Post-Disaster Environments

4.2.2. Hybrid Power and Environmental Sustainability

4.3. Opportunity 1: Offshore Oil & Gas Industry Compliance

4.3.1. Meeting Stringent Discharge Regulations for Produced Water

4.3.2. Compact and Rugged Solutions for Space-Limited Platforms

4.4. Opportunity 2: Smart Cities & Temporary Urban Infrastructure

4.4.1. Bypass Systems for Uninterrupted Municipal Supply

4.4.2. Scalable Solutions for Rapid Urbanization and Mega-Events

5. Containerized Water Treatment Systems Market Share Insights

5.1. By System Type

5.1.1. Filtration Systems (RO, UF, MBR)

5.1.2. Desalination Systems

5.1.3. Disinfection and Specialized Treatment Systems

5.2. By Container Size & Configuration

5.2.1. Standard ISO Containers

5.2.2. Customized Containers

5.3. By Mobility & Deployment

5.3.1. Plug-and-Play

5.3.2. Skid-Mounted and Rapid Deployment

5.4. By End-Use Industry

5.4.1. Industrial Sector

5.4.2. Municipal and Public Utilities

5.4.3. Commercial Sector

5.5. By Level of Automation

5.5.1. Fully Automated Systems

5.5.2. Semi-Automated and Manual Systems

6. Country Analysis of the Containerized Water Treatment Systems Market

6.1. United States: Infrastructure Upgrades and Emergency Preparedness

6.2. China: IoT-Enabled Solutions for Industrial and Environmental Compliance

6.3. India: Rural Access and Modular Innovation

6.4. Saudi Arabia: Flexible Solutions for Industrial and Municipal Needs

6.5. Japan: Disaster-Ready and Compact Modular Units

6.6. Germany: Modular, Energy-Efficient Water Solutions

6.7. Other Country Analysis

7. Market Size Outlook by Region (2025–2034)

7.1. North America Market Size Outlook to 2034

7.1.1. By System Type, Mobility, Capacity, Application, Water Source, Model, and Automation

7.2. Europe Market Size Outlook to 2034

7.2.1. By System Type, Mobility, Capacity, Application, Water Source, Model, and Automation

7.3. Asia Pacific Market Size Outlook to 2034

7.3.1. By System Type, Mobility, Capacity, Application, Water Source, Model, and Automation

7.4. South America Market Size Outlook to 2034

7.4.1. By System Type, Mobility, Capacity, Application, Water Source, Model, and Automation

7.5. Middle East and Africa Market Size Outlook to 2034

7.5.1. By System Type, Mobility, Capacity, Application, Water Source, Model, and Automation

8. Competitive Landscape: Leading Players in Containerized Water Treatment Systems

8.1. Veolia Water Technologies

8.2. Xylem Inc.

8.3. SUEZ

8.4. Evoqua Water Technologies (now part of Xylem)

8.5. Fluence Corporation

8.6. Sustainable Biosolutions Private Limited (SUSBIO)

8.7. Toshiba Water Solutions

8.8. VA Tech Wabag Ltd.

8.9. Thermax Limited

8.10. Ion Exchange India Ltd.

8.11. Corix Water System

8.12. RWL Water

8.13. Other Key Companies

9. Research Coverage & Methodology

9.1. Report Scope and Focus

9.2. Research Methodology

9.3. Deliverables

10. Appendix

10.1. List of Tables

10.2. List of Figures

10.3. Abbreviations