Water Metering and Monitoring Systems Market Overview

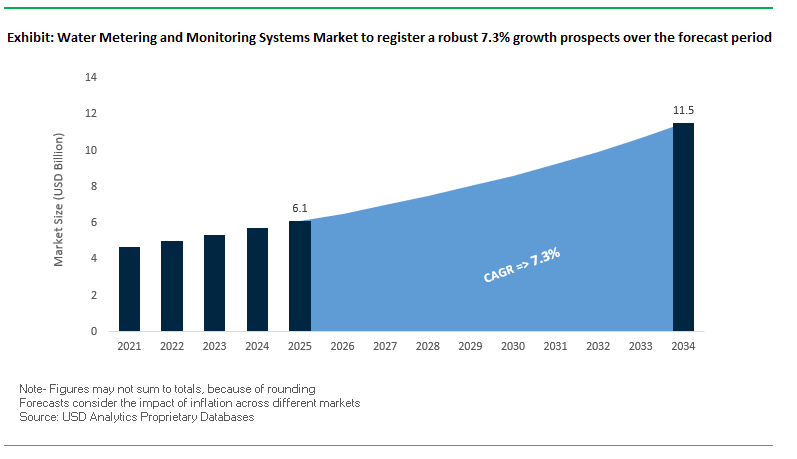

The global water metering and monitoring systems market is projected to grow from $6.1 billion in 2025 to $11.5 billion by 2034, registering a CAGR of 7.3%. This growth is fueled by the urgent need to reduce non-revenue water (NRW), replace aging infrastructure, and integrate advanced digital solutions into water networks. Utilities and municipalities are increasingly turning to smart metering and monitoring technologies to optimize operational efficiency, detect leaks proactively, and ensure sustainable water management.

The market is strongly influenced by technological advancements such as IoT-enabled meters, AI analytics, and cloud platforms, which facilitate real-time data collection and predictive maintenance. Government-led initiatives and programs, like the U.K.’s AMP8, demonstrate large-scale adoption trends, further boosting demand for modern metering solutions.

Key Insights for Industry Stakeholders:

- NRW Reduction: Smart metering projects, like the 2025 Fiji deployment, demonstrate significant potential for reducing water loss.

- Aging Infrastructure Replacement: Modern metering solutions are critical in regions undergoing large-scale network upgrades.

- Advanced Technology Integration: IoT, AI, and cloud computing enable predictive maintenance and real-time monitoring.

- Water Conservation: Real-time consumption data empowers consumers to reduce water usage and enhance sustainability.

- Government-Led Initiatives: Programs like AMP8 in the U.K. accelerate smart meter adoption.

Market Analysis: Recent Developments in Water Metering and Monitoring Systems

The water metering and monitoring systems market has witnessed multiple strategic deployments, partnerships, and technology rollouts aimed at improving operational efficiency and reducing water losses. In August 2025, Itron Inc. partnered with the Water Authority of Fiji to launch the first smart water metering project in the islands, utilizing Cyble communication modules and the cloud-based Temetra platform, targeting a significant reduction in non-revenue water. Similarly, in May 2025, the City of Midland, U.S., partnered with Gateway Collectors to modernize its Advanced Metering Infrastructure (AMI), implementing 15-minute interval remote-reading collectors to enhance leak detection and network coverage.

In March 2025, Itron expanded the Cyble communications module to the Asia-Pacific region, facilitating the automation of mechanical water meters and promoting advanced metering infrastructure adoption. In January 2025, Siemens introduced next-generation smart meters with enhanced cybersecurity and AI-powered predictive insights for improved water network management. Strategic acquisitions further bolstered market capabilities: in December 2024, Xylem Inc. acquired Idrica to strengthen its digital utility solutions, and in November 2024, Diehl Metering acquired PREVENTIO GmbH, enhancing its predictive maintenance and real-time leak detection offerings.

Earlier, in October 2024, TPG secured a 10-year contract with Southeast Water in Australia to manage and connect one million smart water meters, highlighting the growing demand for outsourced and managed services. In January 2024, ABB expanded its smart water management portfolio through the acquisition of Real Tech, a company specializing in real-time water quality monitoring sensors, reinforcing the market’s focus on data analytics and digital water solutions.

Key Trends Driving the Water Metering and Monitoring Market

Integration of IoT and AI for Predictive Water Analytics

The water metering and monitoring systems market is rapidly evolving due to the integration of Artificial Intelligence (AI) and the Internet of Things (IoT). A 2025 review published in MDPI's Water shows AI models can predict pollution events with up to 40% higher efficiency and reduce error rates by 30%, enabling proactive water management. Case studies, such as Xylem’s smart sewer technology, have demonstrated an 80% reduction in Combined Sewer Overflow (CSO) volume, saving utilities hundreds of millions in capital expenditures. This trend highlights the pivotal role of digital water monitoring and predictive analytics in enhancing operational efficiency and cost avoidance.

Focus on Reducing Non-Revenue Water (NRW)

Non-Revenue Water (NRW) reduction is a core driver of market growth. Utilities are increasingly adopting smart meters and digital twins to minimize water loss through leaks, theft, and operational inefficiencies. For instance, the Lushan Water Supply Company in China achieved significant water savings by simulating real-time operations with digital twins. Globally, regulatory enforcement initiatives, such as India’s Online Continuous Effluent Monitoring Systems (OCEMS), incentivize remote monitoring adoption, reducing pollution events and ensuring compliance. This trend underscores the market’s emphasis on efficiency, water conservation, and revenue protection.

Government Initiatives and Public-Private Partnerships

Large-scale government programs and PPPs are modernizing water infrastructure worldwide. The U.S. Infrastructure Investment and Jobs Act (2021) allocates over $50 billion to the EPA for water system upgrades. In India, initiatives like the Jal Jeevan Mission leverage community-based water testing, integrating data-driven monitoring frameworks. Hybrid annuity-based PPP models in cities such as Ayodhya and Prayagraj combine private sector efficiency with public oversight, creating opportunities for smart water metering and monitoring solutions in both urban and semi-urban utilities.

Strategic Opportunities in Water Metering and Monitoring Systems

The market offers significant opportunities in data-driven, AI-enabled, and predictive water management systems. Utilities and industries increasingly recognize that smart metering is not only about accurate measurement but also about improving operational efficiency, reducing NRW, and ensuring compliance. The adoption of Advanced Metering Infrastructure (AMI), IoT-enabled devices, and Meter Data Management (MDM) software creates high-margin growth potential for providers offering integrated solutions combining hardware, analytics, and services.

Market Share Analysis of Water Metering and Monitoring Systems Market

Market Share by Meter Type: Advanced Mechanical and Ultrasonic Lead

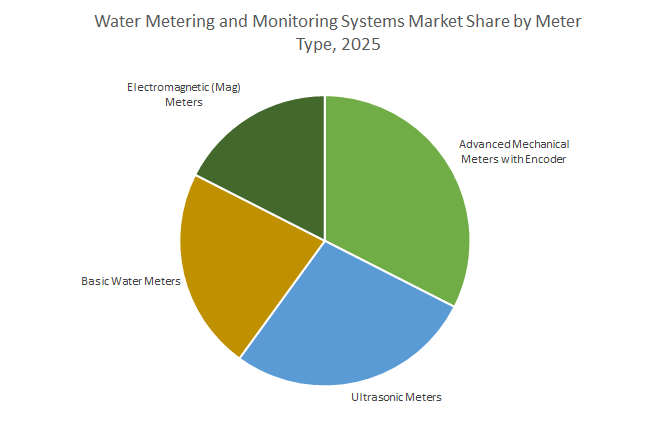

Advanced Mechanical Meters with Encoder (32.8%) lead the market, providing a cost-effective upgrade path for utilities transitioning from manual reads to AMR/AMI systems. Ultrasonic Meters (26.9%) are the fastest-growing segment due to high accuracy, no moving parts, and suitability for large-scale applications. Basic Water Meters (22.5%) remain prevalent in developing regions and low-value installations. Electromagnetic Meters (16.9%) serve niche, high-precision industrial and custody-transfer applications. This segmentation reflects the transition toward digital and high-accuracy metering technologies.

Market Share by Technology: AMI Dominates as the Future Standard

Advanced Metering Infrastructure (AMI, 48.5%) commands the largest share, offering two-way communication, granular data, and remote commands. Automatic Meter Reading (AMR, 32.8%) continues to support utilities transitioning from manual readings, while Drive-by/Mobile Reading (16.9%) and Fixed Network systems are gradually being replaced. The dominance of AMI highlights the shift toward smart, real-time monitoring and predictive analytics, enabling utilities to reduce NRW, forecast demand, and implement time-of-use tariffs.

Market Share by Component: Hardware Remains Core, Software Drives Value

The Hardware segment (64.3%) represents meters, endpoints, transmitters, and network infrastructure the capital-intensive foundation of metering systems. Software & Services (35.7%), including MDM, analytics, integration, and managed services, is the high-growth segment, enabling utilities to extract actionable insights for leak detection, water balance optimization, and operational decision-making. This highlights the market’s shift from pure hardware investment to data-driven, service-oriented solutions.

Market Share by Application: Utilities Dominate, Industrial and Commercial Grow

Water Utilities (68%) remain the primary market, driven by the need to reduce NRW, ensure compliance, and improve operational efficiency. Industrial end-users (22.5%) utilize smart meters for process water measurement, discharge monitoring, and sub-billing, making it an essential resource management tool. Commercial & Institutional applications (11.8%), such as universities, hospitals, and large office buildings, are increasingly adopting sub-metering to optimize water costs and drive sustainability initiatives. This segmentation underscores the critical role of smart water metering in municipal, industrial, and commercial water management.

United States: Smart Water Metering Accelerated by Federal Funding, PFAS Policies, and Corporate Expansions

The United States water metering and monitoring systems market is advancing rapidly, backed by strong government initiatives and regulatory enforcement. The U.S. Environmental Protection Agency (EPA), through the Bipartisan Infrastructure Law (BIL), is allocating over $50 billion to improve drinking water, wastewater, and stormwater infrastructure. This investment is directly boosting the adoption of smart water metering technologies and digital monitoring systems aimed at reducing non-revenue water (NRW) and upgrading aging pipelines. Additionally, Section 106 grants continue to fund ambient water quality monitoring across states.

Corporate activity is reshaping the market landscape. In 2024, Badger Meter expanded its portfolio by acquiring Trimble’s Telog brand remote telemetry units (RTUs), strengthening real-time monitoring and data collection solutions for water utilities. Meanwhile, regulatory policies such as newly finalized PFAS Maximum Contaminant Levels are forcing utilities to adopt advanced water quality monitoring systems. Research efforts, like those funded by the Water Research Foundation (WRF), are further fueling the next generation of AI-driven and IoT-based smart metering solutions for risk management and condition assessment.

China: IoT-Driven Water Metering Expansion Supported by Sponge City Program and Smart Infrastructure Push

China represents one of the fastest-growing markets for smart water metering and monitoring systems, driven by ambitious state-led initiatives and digital transformation goals. The government’s plan to achieve over 90% harmless disposal of urban sludge by 2025 requires widespread deployment of real-time monitoring systems. Additionally, the “Sponge City” program is promoting stormwater management, greywater treatment, and urban flooding control, accelerating adoption of advanced monitoring solutions.

China is heavily investing in IoT-enabled ultrasonic smart meters and integrated smart water management (SWM) platforms, leveraging AI, big data analytics, and predictive maintenance. In June 2025, VWSA’s delegation to LAISON highlighted global interest in China’s role as a technology hub for digital water infrastructure. With applications spanning urban water quality monitoring, industrial wastewater tracking, and sustainable rainwater management, China is positioning itself as a global leader in IoT-based smart metering and monitoring solutions.

India: IoT-Enabled Water Monitoring Scaling with Jal Jeevan Mission and Urban Smart Metering Projects

The Indian water metering and monitoring market is expanding aggressively due to nationwide government initiatives and infrastructure investments. The Jal Jeevan Mission is deploying IoT-based sensor devices across more than 600,000 villages to ensure real-time monitoring of rural drinking water systems, while the National Hydrology Project (NHP) has installed thousands of real-time data acquisition systems (RTDAS) for both groundwater and surface water. These deployments mark a significant shift toward smart monitoring technologies at a national scale.

In urban infrastructure, Chennai Metrowater’s initiative to install 100,000 smart water meters in commercial and high-rise buildings highlights the growing focus on reducing NRW and improving billing accuracy. At the regulatory level, the Central Pollution Control Board (CPCB) operates the National Water Quality Monitoring Programme (NWMP) to strengthen compliance. Key applications are emerging across river rejuvenation programs, effluent treatment plant (CETP) monitoring in industrial clusters, and rural-urban drinking water security, making India a high-growth market for IoT-enabled smart water metering systems.

United Kingdom: Smart Metering Mandates and AI-Driven Asset Management Fuel Market Growth

The United Kingdom’s water metering and monitoring market is thriving under robust regulatory frameworks and corporate innovation. The Water Industry National Environment Programme (WINEP) allocates £22.1 billion for environmental and water asset improvements, while Asset Management Period 8 (AMP8) mandates the installation of 10 million smart water meters by 2030 a transformative driver for the sector.

Corporate and technological advancements are reinforcing this momentum. Siemens’ Water Quality Analytics as a Service (WQAaaS), launched in 2024, provides utilities with real-time water quality insights. The launch of a Smart Meter Read Hub (2025) further enhances meter data accessibility for wholesalers and retailers. Additionally, Northumbrian Water’s adoption of AI-powered video intelligence for asset management exemplifies the market’s shift toward AI- and IoT-driven monitoring solutions. With aging infrastructure and service resilience concerns, the UK is a front-runner in adopting digital smart metering systems.

Singapore: PUB’s Smart Water Meter Programme Anchors IoT-Driven Water Conservation Strategy

Singapore is a regional leader in smart water metering and monitoring adoption, with the PUB’s Smart Water Meter Programme at the forefront. The first phase of the program involves installing smart meters across residential, commercial, and industrial buildings, creating daily digital readings that empower consumers to optimize water usage. The program involves an investment of approximately SGD$120 million, covering supply, installation, and long-term IT system support.

In 2024, Itron partnered with PUB and SP Group’s industrial IoT network to deploy 300,000 connected smart meters, advancing water efficiency and conservation goals. The focus remains on reducing non-revenue water (NRW) in a water-scarce environment and ensuring sustainable, secure water management. Singapore’s strategic integration of IoT metering, digital networks, and predictive analytics sets a global benchmark for smart water monitoring.

Australia: Remote Monitoring, Water Efficiency Programs, and Corporate Innovations Shape the Market

The Australian water metering and monitoring systems market is driven by a dual focus on water conservation and compliance with regulatory frameworks. The Murray–Darling Basin Authority’s Hydrometric Networks and Remote Sensing Program has added 23 upgraded hydrometric stations for transparent water allocation and management, significantly boosting monitoring coverage.

Australia is also investing in smart irrigation technologies with automated systems and water sensors to support farmers under water efficiency programs. Corporate innovation is gaining traction as well NematiQ’s graphene membrane technology (2025) introduces advanced water purification methods that rely on real-time monitoring for optimal performance. With increasing water scarcity and the push to improve compliance with water take regulations, Australia is strengthening its adoption of IoT-based monitoring, digital twins, and contract-based metering solutions.

Competitive Landscape of Water Metering and Monitoring Systems Market

The water metering and monitoring systems market is highly competitive, with key players differentiating themselves through digital integration, innovative metering technologies, global reach, and managed service capabilities. Companies compete by offering scalable solutions for utilities and municipalities to reduce NRW, enhance operational efficiency, and optimize water resources.

Itron Inc. drives advanced AMI and cloud-based meter management solutions

Itron is a global leader in smart metering and utility solutions, with a core focus on Advanced Metering Infrastructure (AMI) and communication modules. Its flagship OpenWay Riva AMI and Temetra meter data management platform provide utilities with scalable, flexible solutions. In August 2025, Itron partnered with the Water Authority of Fiji, demonstrating its capacity to deploy advanced metering solutions in emerging markets. The company manages over 100 million endpoints globally, delivering more than 285 million communicating devices.

Xylem Inc. (Sensus) integrates smart water technologies with analytics

Xylem, through its Sensus brand, combines water technologies with digital analytics to provide comprehensive smart metering solutions. The Sensus Analytics platform allows utilities to monitor real-time data for leak detection and network optimization. The December 2024 acquisition of Idrica enhanced Xylem’s digital intelligence capabilities, strengthening its ability to integrate data from multiple sources and reduce non-revenue water effectively across global networks.

SUEZ S.A. leverages digital twin technology for predictive water network management

SUEZ is renowned for providing technology-driven operational services, including smart water monitoring and network optimization. Its AQUADVANCED® suite enables real-time monitoring and predictive analytics, reducing leak detection time by up to 75%. The October 2023 partnership with SAMP promotes digital twin technology for water infrastructure, emphasizing the company’s commitment to predictive, data-driven solutions in high-growth regions like China and Singapore.

ABB Ltd. enhances water utilities with integrated automation and analytics

ABB utilizes its industrial automation expertise to optimize water infrastructure through smart sensors, SCADA, pump management, and the ABB Ability™ platform. Its January 2024 acquisition of Real Tech expanded real-time water quality monitoring capabilities, integrating data analytics to improve operational efficiency and decision-making. ABB focuses on extending asset lifetimes, energy efficiency, and sustainable water management.

Badger Meter, Inc. delivers precise and reliable smart metering solutions

Badger Meter specializes in high-accuracy flow measurement and smart metering, offering ultrasonic and electromagnetic meters along with its BEACON® SaaS platform for real-time consumption analytics. Strong demand in North America, highlighted in Q2 2025 earnings, reflects utility interest in digital offerings. The company’s innovative ultrasonic meters, with no moving parts, ensure long-term accuracy and low maintenance, supporting sustainable and efficient water management practices.

Water Metering and Monitoring Systems Market Report Scope

Water Metering and Monitoring Systems Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.1 Billion

|

|

Market Size (2034)

|

$11.5 Billion

|

|

Market Growth Rate

|

7.3%

|

|

Segments

|

By Meter Type (Basic Water Meters, Ultrasonic Meters, Electromagnetic Meters, Advanced Mechanical Meters with Encoder), By Technology (Automatic Meter Reading (AMR), Advanced Metering Infrastructure (AMI), Drive-by/Mobile Reading, Fixed Network), By Component (Hardware, Software & Services), By Application (Water Utilities, Industrial, Commercial & Institutional), By End-User (Municipal, Industrial, Commercial, Agricultural)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Itron Inc., Xylem Inc., Badger Meter, Honeywell International Inc., SUEZ, ABB Ltd., Siemens, Veolia, Landis+Gyr, The Mueller Water Products, Kamstrup A/S, Trimble Inc., Neptune Technology Group Inc., B Meters, Aclara Technologies LLC

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Water Metering and Monitoring Systems Market Segmentation

By Meter Type

- Basic Water Meters

- Ultrasonic Meters

- Electromagnetic Meters

- Advanced Mechanical Meters with Encoder

By Technology

- Automatic Meter Reading (AMR)

- Advanced Metering Infrastructure (AMI)

- Drive-by/Mobile Reading

- Fixed Network

By Component

- Hardware

- Software & Services

By Application

- Water Utilities

- Industrial

- Commercial & Institutional

By End-User

- Municipal

- Industrial

- Commercial

- Agricultural

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Water Metering and Monitoring Systems Industry include-

- Itron Inc.

- Xylem Inc.

- Badger Meter

- Honeywell International Inc.

- SUEZ

- ABB Ltd.

- Siemens

- Veolia

- Landis+Gyr

- The Mueller Water Products

- Kamstrup A/S

- Trimble Inc.

- Neptune Technology Group Inc.

- B Meters

- Aclara Technologies LLC

*- List not Exhaustive

Research Coverage

The Water Metering and Monitoring Systems Market Report by USDAnalytics investigates how utilities and industries are accelerating the shift from legacy meters to IoT-enabled, AI-driven AMI platforms to cut NRW, modernize networks, and elevate customer engagement; it highlights breakthroughs in ultrasonic metering, edge analytics, and cloud-native MDM; provides analysis reviews of rollout strategies, cybersecurity-by-design, and lifecycle cost models; and synthesizes global case learnings and procurement playbooks. By mapping meter types, communications topologies, and software stacks to measurable outcomes (leak detection speed, billing accuracy, energy use, and service resilience), this report is an essential resource for utility executives, city leaders, and technology buyers aiming to de-risk deployments, unlock data value, and deliver sustainable water management at scale. Scope Includes-

- By Meter Type: Basic Water Meters; Ultrasonic Meters; Electromagnetic Meters; Advanced Mechanical Meters with Encoder

- By Technology: AMR; AMI; Drive-by/Mobile Reading; Fixed Network

- By Component: Hardware; Software & Services

- By Application: Water Utilities; Industrial; Commercial & Institutional

- By End-User: Municipal; Industrial; Commercial; Agricultural

- Geographic Scope: “Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.”

- Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies (Profiles of 15+ companies): Itron Inc.; Xylem Inc.; Badger Meter; Honeywell International Inc.; SUEZ; ABB Ltd.; Siemens; Veolia; Landis+Gyr; The Mueller Water Products; Kamstrup A/S; Trimble Inc.; Neptune Technology Group Inc.; B Meters; Aclara Technologies LLC

Methodology

USDAnalytics applies a mixed-methods approach: primary interviews with utilities, regulators, and OEMs; buyer and installer surveys across priority regions; and secondary validation from tenders, financials, standards, and technical literature. We build bottom-up installed-base and replacement models by meter type/communication layer, reconcile them with top-down utility spend and funding flows, and triangulate using disclosed rollout counts, network coverage, and NRW baselines. Forecasts (2025–2034) incorporate tariff evolution, regulatory drivers, device lifecycles, battery/firmware roadmaps, and analytics adoption curves. Competitive benchmarking evaluates accuracy classes, cybersecurity certifications, interoperability (DLMS/COSEM, MQTT, CIP), and total cost of metering (TCM) to provide decision-grade insight.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Water Metering and Monitoring Systems Market

1. Executive Summary

1.1. Market Highlights & Key Projections

1.2. Global Market Snapshot

1.3. Key Findings

2. Water Metering and Monitoring Systems Market Overview (2025–2034)

2.1. Introduction

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $6.1 Billion

2.2.2. Forecasted Market Size (2034): $11.5 Billion

2.2.3. Projected Compound Annual Growth Rate (CAGR): 7.3%

2.3. Market Drivers and Challenges

2.3.1. Drivers: NRW Reduction, Aging Infrastructure, and Digital Integration

2.3.2. Challenges: High Upfront Costs and Cybersecurity Concerns

2.4. Key Insights for Industry Stakeholders

3. Key Market Trends and Recent Developments

3.1. Integration of IoT and AI for Predictive Water Analytics

3.2. Focus on Reducing Non-Revenue Water (NRW)

3.3. Government Initiatives and Public-Private Partnerships

3.4. Recent Developments & Strategic Moves (2024–2025)

3.4.1. Strategic Partnerships and Acquisitions

3.4.2. Technology Rollouts and New Product Launches

4. Water Metering and Monitoring Systems Market – Segmentation Insights

4.1. By Meter Type

4.1.1. Advanced Mechanical Meters with Encoder (32.8% Market Share)

4.1.2. Ultrasonic Meters (26.9% Market Share)

4.1.3. Basic Water Meters (22.5% Market Share)

4.1.4. Electromagnetic Meters (16.9% Market Share)

4.2. By Technology

4.2.1. Advanced Metering Infrastructure (AMI) (48.5% Market Share)

4.2.2. Automatic Meter Reading (AMR) (32.8% Market Share)

4.2.3. Drive-by/Mobile Reading (16.9% Market Share)

4.2.4. Fixed Network

4.3. By Component

4.3.1. Hardware (64.3% Market Share)

4.3.2. Software & Services (35.7% Market Share)

4.4. By Application

4.4.1. Water Utilities (68% Market Share)

4.4.2. Industrial (22.5% Market Share)

4.4.3. Commercial & Institutional (11.8% Market Share)

4.5. By End-User

4.5.1. Municipal

4.5.2. Industrial

4.5.3. Commercial

4.5.4. Agricultural

5. Country Analysis and Outlook: Water Metering and Monitoring Systems Market

5.1. United States: Federal Funding and PFAS Policies

5.2. China: IoT-Driven Expansion and Smart Infrastructure Push

5.3. India: Jal Jeevan Mission and Urban Smart Metering Projects

5.4. United Kingdom: Smart Metering Mandates and AI-Driven Asset Management

5.5. Singapore: PUB’s Smart Water Meter Programme

5.6. Australia: Remote Monitoring and Water Efficiency Programs

6. Market Size Outlook by Region (2025-2034)

6.1. North America Water Metering and Monitoring Systems Market Size Outlook to 2034

6.1.1. By Meter Type

6.1.2. By Technology

6.1.3. By Country (US, Canada, Mexico)

6.2. Europe Water Metering and Monitoring Systems Market Size Outlook to 2034

6.2.1. By Meter Type

6.2.2. By Technology

6.2.3. By Country (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

6.3. Asia Pacific Water Metering and Monitoring Systems Market Size Outlook to 2034

6.3.1. By Meter Type

6.3.2. By Technology

6.3.3. By Country (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

6.4. South America Water Metering and Monitoring Systems Market Size Outlook to 2034

6.4.1. By Meter Type

6.4.2. By Technology

6.4.3. By Country (Brazil, Argentina, Rest of South America)

6.5. Middle East and Africa Water Metering and Monitoring Systems Market Size Outlook to 2034

6.5.1. By Meter Type

6.5.2. By Technology

6.5.3. By Country (Saudi Arabia, UAE, South Africa, Egypt, Rest of MEA)

7. Company Profiles: Leading Players

7.1. Itron Inc.

7.1.1. Company Overview

7.1.2. Advanced AMI and Cloud-Based Solutions

7.2. Xylem Inc. (Sensus)

7.2.1. Company Overview

7.2.2. Integration of Smart Water Technologies with Analytics

7.3. SUEZ S.A.

7.4. ABB Ltd.

7.5. Badger Meter, Inc.

7.6. Other Key Players

7.6.1. Honeywell International Inc.

7.6.2. Siemens

7.6.3. Veolia

7.6.4. Landis+Gyr

7.6.5. The Mueller Water Products

7.6.6. Kamstrup A/S

8. Methodology

8.1. Research Scope

8.2. Market Research Approach

8.3. Data Sources and Validation

8.4. Assumptions and Limitations

9. Appendix

9.1. Acronyms and Abbreviations

9.2. List of Tables

9.3. List of Figures