Cloud-Based Water Treatment Monitoring Market Overview

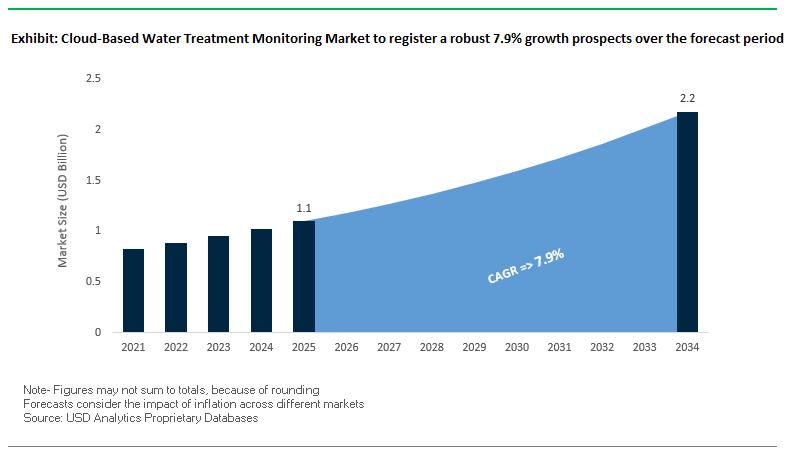

The global cloud-based water treatment monitoring market is projected to grow from $1.1 billion in 2025 to $2.2 billion by 2034, exhibiting a CAGR of 7.9%. The market is driven by the increasing adoption of cloud-based monitoring platforms that provide real-time analytics, predictive maintenance, and operational optimization for municipal and industrial water treatment systems. Cloud integration enables utilities and plant operators to reduce operational costs, manage water losses efficiently, and meet stringent regulatory standards while safeguarding critical infrastructure.

Cloud-based systems offer a comprehensive digital approach, combining AI, IoT, and secure cloud architecture to optimize chemical dosing, detect leaks, and monitor network performance. These platforms enhance decision-making by providing actionable insights, remote monitoring capabilities, and predictive intelligence, which are essential for maintaining sustainable water infrastructure and ensuring operational continuity in urban and industrial water networks.

Key Insights for Industry Stakeholders:

- Operational Cost Reduction: Cloud analytics optimize chemical dosing and predictive maintenance, reducing energy consumption by up to 10%.

- Proactive Leakage Management: Real-time leak detection addresses up to 30% water loss in distribution networks.

- Enhanced Data Security: Platforms like ABB Ability™ and Siemens Xcelerator use secure cloud architectures to protect sensitive infrastructure data.

- Regulatory Compliance: Automated reporting ensures adherence to global water quality and operational standards.

- Remote Asset Monitoring: Cloud platforms provide a centralized hub for monitoring, controlling, and optimizing water treatment systems.

Market Analysis: Recent Developments in Cloud-Based Water Treatment Monitoring

The cloud-based water treatment monitoring market has witnessed several strategic collaborations, technology integrations, and acquisitions aimed at enhancing operational efficiency and digital water management. In August 2025, RSE and Siemens signed a Memorandum of Understanding to integrate Siemens’ AI, automation, and digital technologies into RSE’s modular water treatment systems, accelerating decarbonization initiatives. The same month, Itron Inc. partnered with the Water Authority of Fiji, deploying its cloud-based Temetra platform to reduce non-revenue water through advanced analytics and real-time monitoring.

In March 2025, Siemens and KETOS formed a strategic partnership to integrate AI-driven analytics and IoT-enabled solutions into cloud-based water quality management for industrial and municipal operators. Veolia, in February 2025, partnered with Mistral AI to implement generative AI within cloud platforms, optimizing operational efficiency and resource management. Earlier, in January 2025, Siemens launched a new generation of smart meters featuring enhanced cybersecurity and integrated AI analytics for predictive network management.

Other strategic moves include Xylem Inc.’s acquisition of Idrica in December 2024, strengthening its cloud-based data analytics and digital utility platform capabilities, and Diehl Metering’s acquisition of PREVENTIO GmbH in November 2024, enhancing predictive maintenance and leak detection services. Additionally, in August 2024, ABB unveiled next-generation electromagnetic flowmeters with embedded IoT connectivity, providing greater visibility and control via cloud-based monitoring platforms.

Key Trends Shaping Cloud-Based Water Treatment Monitoring

Government Initiatives Driving Smart Water Infrastructure

The cloud-based water treatment monitoring market is significantly propelled by government-led programs promoting smart water management. India’s Jal Jeevan Mission exemplifies this trend by deploying IoT-enabled sensors across villages, transmitting real-time data to centralized cloud platforms. This enables authorities to monitor water quality, quantity, and pressure, facilitating immediate corrective actions for leaks or low pressure. Globally, regulatory bodies such as India’s Central Pollution Control Board (CPCB) are tightening effluent standards and promoting Online Continuous Effluent Monitoring Systems (OCEMS), accelerating cloud adoption for compliance, reporting, and operational transparency.

Reducing Non-Revenue Water (NRW) Through Real-Time Monitoring

Cloud-based monitoring systems are critical in reducing non-revenue water (NRW) and improving operational efficiency. In Chile, two water utilities achieved an 8% NRW reduction within three years by implementing cloud-based real-time monitoring and network analytics. Companies like Siemens leverage AI-powered cloud platforms to detect household leaks, optimize consumption, and help utilities meet regulatory targets. This trend highlights the economic and sustainability benefits of integrating cloud computing with smart water networks for precise leak detection and operational efficiency.

Integration of AI and Machine Learning for Predictive Analytics

The integration of AI and machine learning with cloud-based monitoring is enabling predictive water management. Academic studies from 2024–2025 emphasize that AI models can process massive IoT sensor datasets to predict pollution events, detect leaks, and forecast equipment failures in real-time. This proactive approach allows utilities to shift from reactive maintenance to predictive operations, extending asset life, reducing downtime, and optimizing water resource management. Predictive analytics is emerging as a key differentiator for utilities adopting cloud-based water treatment monitoring solutions.

Strategic Opportunities in Cloud-Based Water Monitoring

The market presents compelling opportunities across SaaS, PaaS, and IaaS service models, particularly for predictive maintenance, real-time process control, and regulatory compliance. Water utilities and industrial operators can leverage cloud platforms to consolidate dispersed data, run advanced AI analytics, and optimize chemical dosing, energy consumption, and asset performance. The growing need for scalable, cost-effective cloud solutions positions technology providers to capture high-margin revenue from municipalities, industrial users, and engineering firms seeking operational resilience and compliance assurance.

Market Share Insights of Cloud-Based Water Treatment Monitoring Market

Market Share by Service Model: SaaS Leads with Turnkey Solutions

Software-as-a-Service (SaaS, 68%) dominates the cloud-based water monitoring market due to its ready-to-use, subscription-based applications. Utilities and industrial operators benefit from immediate access to monitoring tools without managing software development or IT infrastructure. Platform-as-a-Service (PaaS, 22.5%) supports organizations needing custom applications, advanced analytics, and integration with legacy systems. Infrastructure-as-a-Service (IaaS, 11.8%) is less common but used by large utilities seeking full control over cloud-hosted applications while leveraging virtualized computing resources. This segmentation underscores the market’s preference for turnkey, scalable, and flexible cloud solutions.

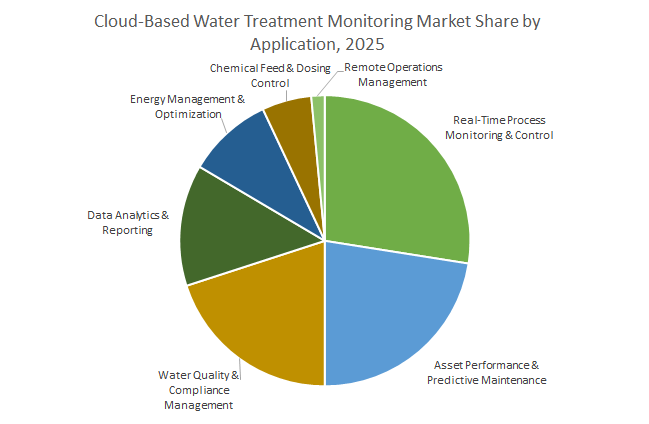

Market Share by Application: Real-Time Monitoring and Predictive Maintenance Drive Adoption

Real-Time Process Monitoring & Control (26.9%) is the largest application, offering situational awareness of flows, pressures, and tank levels across facilities. Asset Performance & Predictive Maintenance (22.5%) enables utilities to anticipate pump, motor, and instrument failures, avoiding costly downtime. Water Quality & Compliance Management (20.9%) automates reporting and ensures regulatory compliance. Data Analytics & Reporting (13.2%) converts raw operational data into actionable insights, informing capital planning and operational improvements. Energy Management & Optimization, Chemical Feed Control, and Remote Operations further enhance efficiency, cost savings, and operational flexibility. Together, these applications illustrate the transformative impact of cloud computing on water treatment operations.

Market Share by End-User: Municipal Utilities Dominate, Industrial Users Drive Efficiency

Municipal Water & Wastewater Utilities (64.3%) lead adoption due to their extensive infrastructure, regulatory mandates, and budget constraints. The cloud-based OpEx model aligns with municipal financial strategies, allowing them to modernize without significant upfront investments. Industrial Users (35.7%) adopt cloud monitoring to optimize process water, reduce compliance risks, and enhance operational efficiency. Within industrial applications, Food & Beverage, Power Generation (8–10%), and Chemicals & Pharmaceuticals (7–9%) are significant adopters due to high water intensity and stringent quality requirements. Cloud-based monitoring provides these industries with real-time insights for water conservation, regulatory compliance, and cost optimization.

United States: Federal Investments and Corporate Consolidation Driving Cloud-Based Water Monitoring

The United States cloud-based water treatment monitoring market is experiencing rapid growth, supported by massive government investments and industry consolidation. The U.S. Environmental Protection Agency (EPA), through the Bipartisan Infrastructure Law (BIL), has allocated over $50 billion for modernizing water infrastructure. This funding is accelerating the deployment of cloud-enabled monitoring platforms, IoT devices, and predictive analytics to track water quality in real time and address contaminants such as PFAS. With the EPA finalizing new Maximum Contaminant Levels (MCLs) for PFAS, utilities and industries now rely heavily on cloud-based continuous monitoring systems for compliance and regulatory reporting.

Corporate innovation further strengthens this momentum. The Xylem–Evoqua merger (2023) created a powerhouse in industrial wastewater management with advanced cloud-native platforms. Meanwhile, Badger Meter’s 2024 acquisition of Trimble’s Telog telemetry units expanded its portfolio for remote cloud monitoring in both utilities and industrial settings. With rising capital costs for PFAS treatment equipment, many municipalities are adopting cloud-based predictive maintenance as a cost-effective alternative. The U.S. market is thus driven by infrastructure modernization, regulatory compliance, and operational efficiency.

China: National Water Reforms Accelerating Cloud-Based Smart Water Management

The China cloud-based water treatment monitoring market is expanding at scale, driven by sweeping national reforms. Policies such as the “Water Ten Plan” and the “Sponge City” program, coupled with the 14th Five-Year Plan, are channeling billions into water infrastructure modernization. By 2025, rural China’s tap water penetration and centralized water supply rates are projected to reach nearly 90%, fueling demand for cloud-native platforms to manage water networks efficiently.

China’s technological ecosystem is increasingly adopting smart water management (SWM) solutions that integrate IoT sensors, AI-powered analytics, and cloud computing. Siemens China is pioneering real-time water quality cloud solutions, while a Chinese wastewater treatment project earned international recognition for sustainable resource innovation. Urban flood control, rainwater management, and agricultural runoff monitoring are among the key applications, making cloud-based platforms essential for predictive maintenance, data integration, and nationwide scalability.

India: Digital Water Grid and IoT-Cloud Synergies Driving Market Growth

The India cloud-based water treatment monitoring market is gaining momentum, led by ambitious government missions and private sector innovation. The Jal Jeevan Mission is rolling out sensor-based IoT systems across six lakh villages to monitor rural water supply, with cloud platforms playing a crucial role in data integration. A 2025 government report highlighted the urgency of establishing a Digital Water Grid backed by public-private partnerships (PPPs) to accelerate investments in AI-powered cloud platforms for national-scale water monitoring.

Corporate and technological advancements are also reshaping the landscape. Pani Energy’s 2024 partnership with Murugappa Water Technology & Solutions has introduced cloud-hosted AI-driven water analytics across India. In parallel, AI-powered cloud platforms are analyzing usage patterns, detecting leaks, and forecasting demand, reducing operational costs and optimizing chemical dosing. With its twin priorities of river rejuvenation and urban wastewater management, India is rapidly becoming a leading adopter of cloud-enabled water treatment monitoring.

Germany: EU Wastewater Regulations Boosting Cloud-Enabled Compliance Systems

The Germany cloud-based water treatment monitoring market is heavily shaped by regulatory pressures from the European Union. The EU Urban Wastewater Treatment Directive (2025 revision) mandates a “4th purification stage” for removing micropollutants, driving demand for cloud-enabled monitoring and compliance solutions. These platforms allow utilities to monitor emissions and optimize treatment plant operations while meeting strict EU standards.

The German Federal Environment Agency (UBA) highlights that cities are embracing digital twins, IoT-enabled monitoring, and AI-based predictive analytics to address climate change impacts. Institutions such as Fraunhofer IGB are leading R&D on digital water platforms, focusing on creating robust data communication infrastructures for cloud-integrated smart process control. Germany’s market is thus being propelled by stringent regulations, climate adaptation strategies, and advanced cloud-driven digital water innovations.

United Kingdom: Smart Meter Rollouts and AI-Powered Cloud Platforms Driving Market Evolution

The United Kingdom cloud-based water treatment monitoring market is undergoing transformation under the Asset Management Period (AMP) 8, which mandates the deployment of 10 million smart meters by 2030. This large-scale rollout is generating substantial demand for cloud-native data management and predictive monitoring platforms.

Industry innovation is accelerating this trend. Siemens launched its Water Quality Analytics as a Service (WQAaaS) in 2024, offering utilities real-time water quality insights hosted entirely on cloud systems. Additionally, the Smart Meter Read Hub (2025) now enables wholesalers and retailers to access cloud-hosted consumption data seamlessly. Meanwhile, Northumbrian Water’s 2025 adoption of agentic AI video intelligence for asset management highlights the growing integration of AI and cloud platforms to improve asset resilience. These advancements position the UK market as a pioneer in AI-driven, cloud-hosted water monitoring for modernization and infrastructure resilience.

Singapore: Smart PUB Roadmap Making Singapore a Global Leader in Cloud-Based Water Monitoring

The Singapore cloud-based water treatment monitoring market is recognized as a global benchmark due to PUB’s Smart Water Meter Programme. Under this initiative, Singapore is rolling out smart meters across residential, commercial, and industrial buildings, providing daily digital meter readings hosted on the cloud.

Strategic investments further strengthen this framework. In January 2024, PUB partnered with Itron and SP Group to connect over 300,000 meters to an industrial IoT and cloud network, enabling advanced water conservation. On the technology front, Hydroleap introduced its Advanced Electrochemical Treatment (AET) in 2024, which significantly reduces operational labor while integrating seamlessly into cloud-based monitoring platforms. With its strong focus on non-revenue water reduction, operational efficiency, and long-term water security, Singapore sets a global model for cloud-native water treatment solutions.

Competitive Landscape of Cloud-Based Water Treatment Monitoring Market

The cloud-based water treatment monitoring market is highly competitive, with key players emphasizing digital transformation, IoT integration, AI-driven analytics, and secure cloud platforms to deliver real-time, actionable insights for water utilities and industrial operators. Companies differentiate through scalability, cybersecurity, and the ability to integrate multi-source data for predictive decision-making and operational optimization.

Xylem Inc. leads in cloud-enabled water management solutions

Xylem offers a robust ecosystem of cloud-based water technologies via its Sensus brand and Xylem Vue platform, integrating data from smart meters, sensors, and pumps for holistic network optimization. The 2024 acquisition of Idrica enhanced its capabilities in cloud-based analytics and intelligence for water utilities. Xylem’s Avensor service allows remote monitoring of pump stations and other assets, delivering real-time insights that reduce operational costs and on-site interventions.

SUEZ S.A. pioneers cloud-driven network optimization

SUEZ leverages AQUADVANCED®, a digital suite providing real-time monitoring, predictive analytics, and cloud-enabled simulation for water networks. With over 7 million smart meters deployed globally, SUEZ integrates cloud technology for asset management, leak detection, and operational efficiency. The October 2023 partnership with SAMP further accelerates cloud-based digital twin deployment, supporting large-scale industrial and municipal water projects.

Veolia Environnement S.A. drives cloud and AI integration

Veolia utilizes its Hubgrade platform, a cloud-based AI and analytics solution for centralized control of water and energy infrastructure. In February 2025, Veolia partnered with Mistral AI to integrate generative AI into cloud-based operations, optimizing resource management. Its GreenUp strategic plan and the 2024 launch of Hubgrade Water Footprint demonstrate Veolia’s commitment to digital transformation and sustainability.

Schneider Electric SE transforms water treatment with cloud automation

Schneider Electric deploys its EcoStruxure platform to provide IoT-enabled, cloud-based automation for water and wastewater treatment plants. The January 2024 contract to automate Mumbai’s largest water treatment facility highlights EcoStruxure’s capabilities in improving efficiency for 22 million residents. Schneider’s solutions enhance operational performance, energy efficiency, and CO2 reduction across critical water infrastructure.

ABB Ltd. expands cloud-enabled digital water solutions

ABB integrates industrial automation, software, and digital technologies via the ABB Ability™ platform, a cloud-based suite for process automation, predictive maintenance, and smart grid management. Strategic partnerships with RSE in August 2025 and new electromagnetic flowmeters in August 2024 illustrate ABB’s commitment to real-time monitoring, predictive analytics, and cybersecurity through secure cloud platforms, supporting utilities and industries in achieving decarbonization and resource efficiency goals.

Cloud-Based Water Treatment Monitoring Market Report Scope

Cloud-Based Water Treatment Monitoring Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.1 Billion

|

|

Market Size (2034)

|

$2.2 Billion

|

|

Market Growth Rate

|

7.9%

|

|

Segments

|

By Service Model (Software-as-a-Service (SaaS), Platform-as-a-Service (PaaS), Infrastructure-as-a-Service (IaaS)), By Application (Real-Time Process Monitoring & Control, Water Quality & Compliance Management, Asset Performance & Predictive Maintenance, Energy Management & Optimization, Chemical Feed & Dosing Control, Data Analytics & Reporting, Remote Operations Management), By End-User (Municipal Water & Wastewater Utilities, Industrial Users), By Deployment Type (Public Cloud, Private Cloud, Hybrid Cloud), By Component (Software, Services)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Xylem Inc., Siemens, Itron Inc., ABB Ltd., Schneider Electric, Veolia, SUEZ, Evoqua Water Technologies, Badger Meter, Trimble Inc., Hach (Danaher Corporation), Honeywell International Inc., Oracle Corporation, IBM Corporation, Bentley Systems, Incorporated

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Cloud-Based Water Treatment Monitoring Market Segmentation

By Service Model

- Software-as-a-Service (SaaS)

- Platform-as-a-Service (PaaS)

- Infrastructure-as-a-Service (IaaS)

By Application

- Real-Time Process Monitoring & Control

- Water Quality & Compliance Management

- Asset Performance & Predictive Maintenance

- Energy Management & Optimization

- Chemical Feed & Dosing Control

- Data Analytics & Reporting

- Remote Operations Management

By End-User

- Municipal Water & Wastewater Utilities

- Industrial Users

- Power Generation

- Oil & Gas

- Chemicals & Petrochemicals

- Food & Beverage

- Pharmaceuticals & Healthcare

- Mining & Metals

- Pulp & Paper

By Deployment Type

- Public Cloud

- Private Cloud

- Hybrid Cloud

By Component

- Software

- Analytics Platforms

- Asset Management Suites

- SCADA Integration Tools

- Compliance & Reporting Modules

- Services

- System Integration & Implementation

- Training & Consulting

- Support & Maintenance

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Cloud-Based Water Treatment Monitoring Industry include-

- Xylem Inc.

- Siemens

- Itron Inc.

- ABB Ltd.

- Schneider Electric

- Veolia

- SUEZ

- Evoqua Water Technologies

- Badger Meter

- Trimble Inc.

- Hach (Danaher Corporation)

- Honeywell International Inc.

- Oracle Corporation

- IBM Corporation

- Bentley Systems, Incorporated

*- List not Exhaustive

Research Coverage

The Cloud-Based Water Treatment Monitoring Market Report by USDAnalytics this report investigates how secure cloud platforms, IoT telemetry, and AI analytics are redefining real-time visibility, regulatory assurance, and cost efficiency across municipal and industrial water assets; it highlights breakthroughs in predictive maintenance, anomaly detection, and remote operations; delivers analysis reviews on cybersecurity-by-design, data governance, and SLA/uptime contracting; and synthesizes adoption playbooks that de-risk modernization at scale. Anchored in evidence from live deployments and vendor roadmaps, this report is an essential resource for utility executives, plant managers, and technology buyers seeking measurable gains in energy use, chemical dosing, and NRW control while future-proofing critical water infrastructure. Scope Includes-

- By Service Model: SaaS; PaaS; IaaS

- By Application: Real-Time Process Monitoring & Control; Water Quality & Compliance Management; Asset Performance & Predictive Maintenance; Energy Optimization; Chemical Feed & Dosing; Data Analytics & Reporting; Remote Operations

- By End-User: Municipal Water & Wastewater Utilities; Industrial Users (Power, Oil & Gas, Chemicals & Petrochemicals, Food & Beverage, Pharmaceuticals & Healthcare, Mining & Metals, Pulp & Paper)

- By Deployment: Public Cloud; Private Cloud; Hybrid Cloud

- By Component: Software (Analytics Platforms, Asset Suites, SCADA Integration, Compliance Modules); Services (Integration, Training, Support)

- Geographic Scope: “Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.”

- Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies (Profiles of 15+ companies): Xylem Inc.; Siemens; Itron Inc.; ABB Ltd.; Schneider Electric; Veolia; SUEZ; Evoqua Water Technologies; Badger Meter; Trimble Inc.; Hach (Danaher Corporation); Honeywell International Inc.; Oracle Corporation; IBM Corporation; Bentley Systems, Incorporated

Methodology

USDAnalytics applies a mixed-methods design that triangulates primary interviews (utilities, plant operators, OEMs, integrators) with secondary intelligence (tenders, regulatory dockets, vendor filings, technical standards). Bottom-up models quantify connected assets, users, and workloads by service model and application; top-down checks align against capex/opex trends, funding flows, and disclosed rollouts. Forecasts (2025–2034) incorporate PFAS/MCL timelines, cybersecurity posture requirements, network availability (LPWAN/5G), energy price scenarios, and software adoption curves. Comparative scoring evaluates interoperability, latency/availability SLAs, data residency controls, and total cost per monitored m³ to deliver decision-grade projections.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Cloud-Based Water Treatment Monitoring Market

1. Executive Summary

1.1. Market Highlights & Key Projections

1.2. Global Market Snapshot

1.3. Key Findings

2. Cloud-Based Water Treatment Monitoring Market Overview (2025–2034)

2.1. Introduction

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $1.1 Billion

2.2.2. Forecasted Market Size (2034): $2.2 Billion

2.2.3. Projected Compound Annual Growth Rate (CAGR): 7.9%

2.3. Market Drivers and Challenges

2.3.1. Drivers: Operational Cost Reduction, Efficiency, and Remote Management

2.3.2. Challenges: Data Security and High Integration Costs

2.4. Key Insights for Industry Stakeholders

3. Key Market Trends and Recent Developments

3.1. Government Initiatives Driving Smart Water Infrastructure

3.2. Reducing Non-Revenue Water (NRW) Through Real-Time Monitoring

3.3. Integration of AI and Machine Learning for Predictive Analytics

3.4. Recent Developments & Strategic Moves (2024–2025)

3.4.1. Strategic Collaborations and Acquisitions

3.4.2. Technology Integrations and Platform Launches

4. Cloud-Based Water Treatment Monitoring Market – Segmentation Insights

4.1. By Service Model

4.1.1. Software-as-a-Service (SaaS) (68% Market Share)

4.1.2. Platform-as-a-Service (PaaS) (22.5% Market Share)

4.1.3. Infrastructure-as-a-Service (IaaS) (11.8% Market Share)

4.2. By Application

4.2.1. Real-Time Process Monitoring & Control (26.9% Market Share)

4.2.2. Asset Performance & Predictive Maintenance (22.5% Market Share)

4.2.3. Water Quality & Compliance Management (20.9% Market Share)

4.2.4. Data Analytics & Reporting (13.2% Market Share)

4.2.5. Other Applications (Energy Management, Chemical Feed Control, etc.)

4.3. By End-User

4.3.1. Municipal Water & Wastewater Utilities (64.3% Market Share)

4.3.2. Industrial Users (35.7% Market Share)

4.4. By Deployment Type

4.4.1. Public Cloud

4.4.2. Private Cloud

4.4.3. Hybrid Cloud

4.5. By Component

4.5.1. Software

4.5.2. Services

5. Country Analysis and Outlook: Cloud-Based Water Treatment Monitoring Market

5.1. United States: Federal Investments & Corporate Consolidation

5.2. China: National Water Reforms & Smart Water Management

5.3. India: Digital Water Grid & IoT-Cloud Synergies

5.4. Germany: EU Regulations & Cloud-Enabled Compliance

5.5. United Kingdom: Smart Meter Rollouts & AI-Powered Platforms

5.6. Singapore: Smart PUB Roadmap & Global Leadership

6. Cloud-Based Water Treatment Monitoring Market Size Outlook by Region (2025–2034)

6.1. North America Cloud-Based Water Treatment Monitoring Market Size Outlook to 2034

6.1.1. By Service Model

6.1.2. By Application

6.1.3. By Country (US, Canada, Mexico)

6.2. Europe Cloud-Based Water Treatment Monitoring Market Size Outlook to 2034

6.2.1. By Service Model

6.2.2. By Application

6.2.3. By Country (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

6.3. Asia Pacific Cloud-Based Water Treatment Monitoring Market Size Outlook to 2034

6.3.1. By Service Model

6.3.2. By Application

6.3.3. By Country (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

6.4. South America Cloud-Based Water Treatment Monitoring Market Size Outlook to 2034

6.4.1. By Service Model

6.4.2. By Application

6.4.3. By Country (Brazil, Argentina, Rest of South America)

6.5. Middle East and Africa Cloud-Based Water Treatment Monitoring Market Size Outlook to 2034

6.5.1. By Service Model

6.5.2. By Application

6.5.3. By Country (Saudi Arabia, UAE, South Africa, Egypt, Rest of MEA)

7. Competitive Landscape: Key Companies

7.1. Xylem Inc.

7.1.1. Company Overview

7.1.2. Cloud-Enabled Water Management Solutions

7.2. SUEZ S.A.

7.2.1. Company Overview

7.2.2. Cloud-Driven Network Optimization

7.3. Veolia Environnement S.A.

7.4. Schneider Electric SE

7.5. ABB Ltd.

7.6. Other Prominent Companies

7.6.1. Siemens

7.6.2. Itron Inc.

7.6.3. Badger Meter

8. Methodology

8.1. Research Scope

8.2. Market Research Approach

8.3. Data Sources and Validation

8.4. Assumptions and Limitations

9. Appendix

9.1. Acronyms and Abbreviations

9.2. List of Tables

9.3. List of Figures