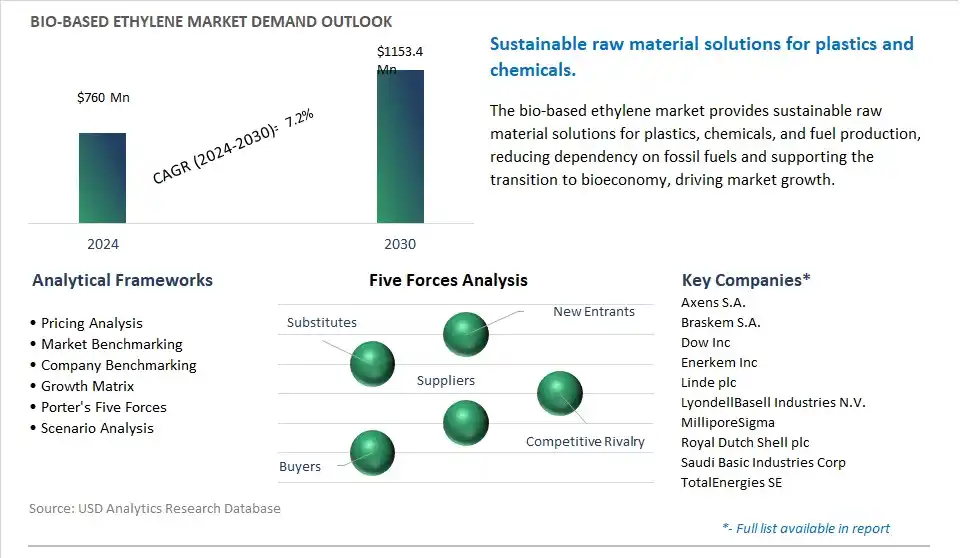

The global Bio-based Ethylene Market is poised to register a 7.2% CAGR from $760 Million in 2024 to $1153.4 Million in 2030.

The global Bio-based Ethylene Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Raw Material (Sugars, Starch, Lignocellulosic Biomass), By End-User (Packaging, Detergent, Lubricant, Additives).

An Introduction to Global Bio based Ethylene Market in 2024

The market for bio-based ethylene is gaining momentum as the chemical industry seeks renewable alternatives to fossil fuels for ethylene production, a key building block for a wide range of petrochemicals and plastics. Key trends shaping the future of this industry include the development of biotechnological processes for the microbial fermentation of renewable feedstocks such as sugarcane, corn, and cellulose to produce ethanol, which can be subsequently converted into ethylene through dehydration or other chemical processes. Additionally, advancements in fermentation technology, enzyme engineering, and metabolic pathway optimization enable the production of bio-based ethylene with high yields, purity, and process efficiency, meeting the performance requirements of various downstream applications. Moreover, the adoption of sustainability certifications, carbon offset programs, and renewable energy sourcing drives market demand for bio-based ethylene, fostering innovation and market expansion in this sector. As industries transition towards a circular economy and decarbonization, the demand for bio-based ethylene is expected to increase, driving further innovation and market development in sustainable petrochemical feedstocks.

Bio-based Ethylene Market Competitive Landscape

The market report analyses the leading companies in the industry including Axens S.A., Braskem S.A., Dow Inc, Enerkem Inc, Linde plc, LyondellBasell Industries N.V., MilliporeSigma, Royal Dutch Shell plc, Saudi Basic Industries Corp, TotalEnergies SE.

Bio-based Ethylene Market Dynamics

Bio-Based Ethylene Market Trend: Shift Towards Renewable and Sustainable Feedstocks in Petrochemical Industry

A prominent trend in the market for bio-based ethylene is the shift towards renewable and sustainable feedstocks in the petrochemical industry. Ethylene is a key building block chemical used in the production of plastics, packaging materials, detergents, and various other industrial products. With increasing concerns about climate change and finite fossil fuel reserves, there is a growing interest in sourcing ethylene from renewable biomass feedstocks such as sugarcane, corn, or lignocellulosic biomass. Bio-based ethylene offers a sustainable alternative to ethylene derived from fossil fuels, reducing greenhouse gas emissions and dependency on non-renewable resources, thus aligning with the global push towards a circular economy and green chemistry practices.

Bio-Based Ethylene Market Driver: Environmental Regulations and Corporate Sustainability Goals

A key driver behind the demand for bio-based ethylene is the implementation of environmental regulations and corporate sustainability goals by governments and companies worldwide. Regulatory initiatives aimed at reducing carbon emissions, promoting renewable energy, and incentivizing bio-based products encourage the adoption of bio-based ethylene as a greener alternative to fossil fuel-derived ethylene. Additionally, companies are setting ambitious sustainability targets and commitments to reduce their environmental footprint, enhance resource efficiency, and meet the growing demand for sustainable products from consumers and investors. Bio-based ethylene enables companies to achieve these goals by offering a renewable and low-carbon solution for ethylene production, thereby driving market demand and investment in bio-based chemicals and materials.

Bio-Based Ethylene Market Opportunity: Investment in Advanced Biorefinery Technologies

An emerging opportunity in the market for bio-based ethylene lies in investment in advanced biorefinery technologies for biomass conversion and chemical synthesis. While bio-based ethylene holds promise as a sustainable feedstock for the petrochemical industry, challenges remain in terms of technological scalability, cost competitiveness, and supply chain integration. Opportunities exist for collaboration between technology developers, chemical manufacturers, and biomass suppliers to advance research and development efforts in biorefinery processes. By leveraging innovations in biotechnology, catalysis, and process engineering, stakeholders can optimize biomass conversion pathways, improve ethylene yield and purity, and reduce production costs. Additionally, investments in infrastructure, logistics, and supply chain management can enhance the commercial viability and scalability of bio-based ethylene production, unlocking new opportunities for growth and sustainability in the petrochemical industry.

Bio-based Ethylene Market Ecosystem

The bio-based ethylene Market Ecosystem encompasses diverse critical stages, beginning with feedstock production where sugarcane and beet growers, corn and cassava farmers, and forestry companies provide renewable materials. Specialized pre-treatment companies, including LIG Renewable Fuels, facilitate the breakdown of cellulosic biomass for efficient conversion.

Fermentation processes, managed by companies including Braskem and Dow, produce bio-ethanol from sugars, followed by dehydration into bio-ethylene by integrated facilities or established chemical companies. Purification, quality control, and testing ensure bio-ethylene meets industry standards, with producers including Braskem and Dow engaging in these activities. Distribution and sales channels involve logistics companies experienced in handling ethylene, along with bio-based ethylene producers and chemical distributors including Brenntag and Univar Solutions, catering to various industrial customers.

In end-use applications, bio-ethylene substitutes traditional ethylene in plastics and chemicals production, with major players including Dow and ExxonMobil adopting bio-based solutions into their manufacturing processes.

Bio-Based Ethylene Market Share Analysis: Sugars held the dominant revenue share in 2024

Among the segments in the Bio-Based Ethylene Market, Sugars emerge as the largest, driven by diverse significant factors contributing to their dominance. Sugars, derived from various renewable sources such as sugarcane, corn, and beet, serve as a key feedstock for the production of bio-based ethylene through fermentation and subsequent chemical processes. Sugars offer diverse advantages as a raw material for bio-based ethylene production, including high availability, ease of processing, and favorable economics. Additionally, the established infrastructure for sugar production and processing further supports their prominence in the bio-based ethylene market. In addition, advancements in biotechnological processes and fermentation technologies have enhanced the efficiency and yield of bio-based ethylene from sugars, driving their widespread adoption by manufacturers. As industries seek sustainable alternatives to fossil fuels and petrochemicals, the dominance of Sugars in the Bio-Based Ethylene Market is expected to persist, offering manufacturers and suppliers significant opportunities for growth and market expansion.

Bio-Based Ethylene Market Share Analysis: Packaging is the fastest growing market segment over the forecast period to 2030

The Packaging segment is the fastest-growing segment in the Bio-Based Ethylene Market, driven by diverse key factors contributing to its rapid expansion. Bio-based ethylene serves as a sustainable alternative to traditional petroleum-based ethylene in the production of various packaging materials, including films, bottles, and containers. With increasing environmental concerns and regulatory pressures to reduce plastic waste and carbon emissions, there is a growing demand for bio-based packaging solutions derived from renewable sources. Bio-based ethylene offers advantages such as biodegradability, reduced greenhouse gas emissions, and lower environmental impact compared to conventional plastics, making it a preferred choice for environmentally conscious consumers and packaging manufacturers. In addition, technological advancements in bio-based polymer processing and formulation have improved the performance and cost-effectiveness of bio-based packaging materials, further driving their adoption across industries. As the global demand for sustainable packaging solutions continues to rise, fueled by shifting consumer preferences and corporate sustainability initiatives, the Packaging segment in the Bio-Based Ethylene Market is expected to experience sustained growth, presenting significant opportunities for manufacturers and suppliers to capitalize on this trend.

Bio-based Ethylene Market Report Scope-

By Raw Material

Sugars

Starch

Lignocellulosic Biomass

By End-User

Packaging

Detergent

Lubricant

Additives

Bio-based Ethylene Market Companies Profiled

Axens S.A.

Braskem S.A.

Dow Inc

Enerkem Inc

Linde plc

LyondellBasell Industries N.V.

MilliporeSigma

Royal Dutch Shell plc

Saudi Basic Industries Corp

TotalEnergies SE

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Bio-based Ethylene Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Bio-based Ethylene Market Size Outlook, $ Million, 2021 to 2030

3.2 Bio-based Ethylene Market Outlook by Type, $ Million, 2021 to 2030

3.3 Bio-based Ethylene Market Outlook by Product, $ Million, 2021 to 2030

3.4 Bio-based Ethylene Market Outlook by Application, $ Million, 2021 to 2030

3.5 Bio-based Ethylene Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Bio-based Ethylene Industry

4.2 Key Market Trends in Bio-based Ethylene Industry

4.3 Potential Opportunities in Bio-based Ethylene Industry

4.4 Key Challenges in Bio-based Ethylene Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Bio-based Ethylene Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Bio-based Ethylene Market Outlook by Segments

7.1 Bio-based Ethylene Market Outlook by Segments, $ Million, 2021- 2030

By Raw Material

Sugars

Starch

Lignocellulosic Biomass

By End-User

Packaging

Detergent

Lubricant

Additives

8 North America Bio-based Ethylene Market Analysis and Outlook To 2030

8.1 Introduction to North America Bio-based Ethylene Markets in 2024

8.2 North America Bio-based Ethylene Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Bio-based Ethylene Market size Outlook by Segments, 2021-2030

By Raw Material

Sugars

Starch

Lignocellulosic Biomass

By End-User

Packaging

Detergent

Lubricant

Additives

9 Europe Bio-based Ethylene Market Analysis and Outlook To 2030

9.1 Introduction to Europe Bio-based Ethylene Markets in 2024

9.2 Europe Bio-based Ethylene Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Bio-based Ethylene Market Size Outlook by Segments, 2021-2030

By Raw Material

Sugars

Starch

Lignocellulosic Biomass

By End-User

Packaging

Detergent

Lubricant

Additives

10 Asia Pacific Bio-based Ethylene Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Bio-based Ethylene Markets in 2024

10.2 Asia Pacific Bio-based Ethylene Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Bio-based Ethylene Market size Outlook by Segments, 2021-2030

By Raw Material

Sugars

Starch

Lignocellulosic Biomass

By End-User

Packaging

Detergent

Lubricant

Additives

11 South America Bio-based Ethylene Market Analysis and Outlook To 2030

11.1 Introduction to South America Bio-based Ethylene Markets in 2024

11.2 South America Bio-based Ethylene Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Bio-based Ethylene Market size Outlook by Segments, 2021-2030

By Raw Material

Sugars

Starch

Lignocellulosic Biomass

By End-User

Packaging

Detergent

Lubricant

Additives

12 Middle East and Africa Bio-based Ethylene Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Bio-based Ethylene Markets in 2024

12.2 Middle East and Africa Bio-based Ethylene Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Bio-based Ethylene Market size Outlook by Segments, 2021-2030

By Raw Material

Sugars

Starch

Lignocellulosic Biomass

By End-User

Packaging

Detergent

Lubricant

Additives

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Axens S.A.

Braskem S.A.

Dow Inc

Enerkem Inc

Linde plc

LyondellBasell Industries N.V.

MilliporeSigma

Royal Dutch Shell plc

Saudi Basic Industries Corp

TotalEnergies SE

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Raw Material

Sugars

Starch

Lignocellulosic Biomass

By End-User

Packaging

Detergent

Lubricant

Additives

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)