Market Overview: Bioactive Ingredients Market Growth Fueled by AI Discovery, Fermentation Platforms, and Functional Nutrition Expansion (2025–2034)

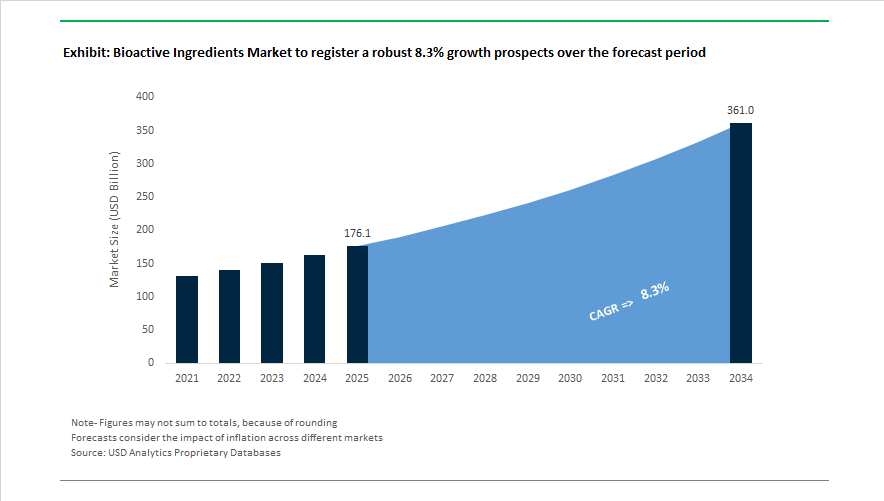

The bioactive ingredients market is projected to rise from USD 176.1 billion in 2025 to USD 360.9 billion by 2034, representing a CAGR of 8.3% supported by rapid integration of biotechnology, precision fermentation, and AI-driven discovery platforms across nutrition, personal care, and functional food systems. Market development accelerated in 2024 when dsm-firmenich expanded algae-derived omega-3 bioactives for pet nutrition, reinforcing the shift toward sustainable, non-marine sources of essential fatty acids. In November 2024, CABIO Biotech and Nourish Ingredients formed a commercial partnership to scale Tastilux precision-fermented fats for Asia-Pacific food applications, marking increased adoption of animal-free lipid bioactives. Innovation cycles shortened in January 2025 when Debut launched the BeautyORB AI platform to accelerate development of biotech-derived cosmetic bioactives, demonstrating how digital biology tools are reshaping ingredient pipelines.

Functional food and personal care bioactives gained strong momentum through 2025. In March 2025, Isobionics introduced fermentation-derived natural flavor bioactives with consistent purity independent of agricultural seasonality. During the same month, Cargill unveiled pectin replacers and functional starch blends in India, addressing cost-sensitive demand for healthier indulgence formats. In May 2025, private equity firm Astorg acquired a majority stake in Solabia Group to accelerate expansion in cosmetic bioactives. In October 2025, BASF launched Ameriflor Calm, a regenerative-sourced botanical bioactive aimed at skin resilience. In November 2025, ADM received industry recognition for its postbiotic Lactobacillus gasseri CP2305, reflecting the expansion of clinically supported mental wellness ingredients into food and beverage systems.

Advanced precision health and formulation science are shaping the next phase of growth. In January 2026, Debut launched DermCeutical EDL, a genomics-informed topical bioactive targeting dermal fibroblast activation. In February 2026, BioAro secured UAE approval for its AI-designed BioActive Longevity Stack, demonstrating regulatory acceptance of multi-component longevity formulations. Sensory science and delivery formats are evolving as well. In January 2026, Kerry Group released Supplement Taste Charts emphasizing lifestyle-led supplement formats that improve palatability of strong bioactives. In February 2026, Ingredion reported record growth in functional fiber and sugar-reduction bioactives.

Trends and Opportunities Reshaping the Bioactive Ingredients Market

Market Trend: Clinical Validation and Molecule Standardization Drive Competitive Advantage in Cognitive Health

A core structural change in the Bioactive Ingredients Market is the transition from broad functional claims toward clinically validated, biomarker-specific ingredients. Magnesium L-threonate and standardized saffron extracts are emerging as benchmark examples, largely because they demonstrate blood-brain barrier permeability and measurable neurological benefit.

Data presented at CPHI Frankfurt in late 2025 positioned Magtein® as one of the first bioactive ingredients to advance into what industry analysts refer to as the "Pharma 5.0" zone, where efficacy is measured using pharmaceutical-grade outcomes. Randomized controlled trials show Magtein® improves cognitive focus and stress resilience across geriatric and younger populations, expanding its total addressable market beyond traditional "brain aging" categories. The IAFNS Cognitive Health Committee is additionally driving standardization frameworks to harmonize potency and ensure uniformity across saffron extracts such as affron®, reducing the historic inconsistency associated with botanical sourcing. For ingredient manufacturers, this shift means future competitive differentiation will depend on clinical datasets, validated biomarkers, and consistent chemistry rather than mere "natural" positioning.

Market Trend: Precision Fermentation Enables Nature-Identical Bioactive Supply for Longevity and Immunity

Precision fermentation is rapidly reshaping access to rare and high-potency bioactives that could not scale using conventional plant extraction. The sector is leveraging bioreactors for L-ergothioneine, Urolithin A, and other longevity-linked compounds, allowing brands to launch clean-label formulations at global scale and avoid heavy metal contamination or seasonal yield variation.

Ergothioneine exemplifies this transition. In August 2025, a clinical trial published in Nutraceuticals reported that Blue California’s ErgoActive® (25 mg/day) significantly improved memory scores in adults aged 55–79 and increased leukocyte telomere length in women, positioning it as a scientifically supported anti-aging ingredient. With 99% purity levels achieved through fermentation, companies now have predictable yearly supply and can rely on GMP-compliant facilities to meet pharmaceutical-grade quality needs. This structural shift is also changing how procurement teams evaluate suppliers: instead of origin or farming practices, ESG and supply chain resilience metrics now include CO₂ footprint per kilogram, traceability audits, and production scalability.

Market Opportunity: Muscle Stem Cell Activation and Sarcopenia Solutions Create a Premium Growth Segment

Nutrition for aging populations is transitioning away from generic protein supplementation toward molecular-level intervention. Bioactives that activate muscle stem cells (satellite cells) and improve mitochondrial ATP production are forming a new premium category.

In January 2025, Nestlé Research identified a combination of nicotinamide (B3) and pyridoxine (B6) that activates muscle stem cells through the β-catenin and AKT signaling pathways. When translated into consumer nutrition, this research establishes a defensible IP-based advantage for companies developing muscle restoration formulations. Parallel to this, Biophytis’ plant-derived BIO101 (20-hydroxyecdysone) is progressing in its Phase 3 SARA trial. With EMA approval to explore obesity-linked muscle loss, BIO101 reflects the convergence of sarcopenia solutions with GLP-1 weight-loss outcomes, creating a multi-billion-dollar crossover market where sports nutrition and clinical therapeutics intersect.

This category offers premium pricing power because efficacy is quantifiable — biomarker movement in muscle protein synthesis, recovery speed, and strength metrics provide data-driven justification for formulators and investors.

Market Opportunity: Precision Prebiotics and Postbiotics Enable Scalable, Shelf-Stable Microbiome Products

The microbiome category is moving into its "post-probiotic" era. Precision prebiotics and postbiotics offer improved safety, stability, and regulatory flexibility, making them ideal for food and beverage platforms where refrigeration and contamination risks previously limited probiotic innovation.

Research in September 2025 (Frontiers) confirmed postbiotics as the preferred bioactive for large-scale F&B integration because they can withstand thermal processing and remain effective in shelf-stable beverages, powders, and baked goods. Meanwhile, fermentation-derived Human Milk Oligosaccharides (2'-FL, LNnT) are gaining adoption in adult gut health and metabolic formulations. These HMOs are clinically shown to support gut barrier function and modulate systemic immune response by selectively nourishing Bifidobacterium species.

For brands, this opens a high-margin innovation pipeline — adult HMOs carry a "clinical relevance" halo from the infant formula sector and offer strong SEO demand signals across search terms tied to metabolic health, immune resilience, and prebiotic formulas.

Bioactive Ingredients Market Share and Segmentation Insights

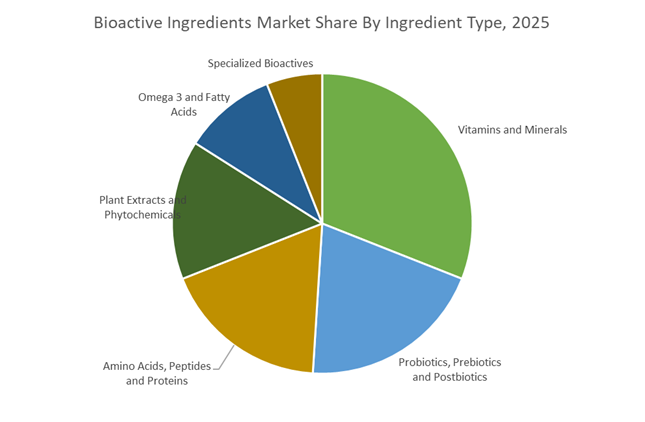

Market Share by Ingredient Type: Vitamins Lead Volume While Microbiome and Specialty Bioactives Accelerate Growth

Vitamins and minerals account for 31% of the Bioactive Ingredients Market in 2025, maintaining leadership due to broad fortification across dietary supplements, functional foods, and clinical nutrition. High-volume products such as vitamins D, B12, and C, along with magnesium, anchor demand, with fermentation-derived vitamins gaining traction for purity and sustainability advantages. Probiotics, prebiotics, and postbiotics represent the fastest-growing segment, fueled by expanding microbiome research and applications spanning gut, immune, skin, and mental health, with postbiotics emerging as stable, shelf-friendly alternatives. Amino acids, peptides, and proteins benefit from sports nutrition and active aging trends, led by collagen peptides, BCAAs, and plant-based proteins. Plant extracts and phytochemicals such as curcumin, green tea, ginger, and ashwagandha are advancing through bioavailability-enhanced formats. Omega 3 fatty acids remain established in cardiovascular and prenatal health, with algal DHA gaining share. Specialized bioactives including coenzyme Q10, carotenoids, glucosamine, and MSM command premium pricing through targeted clinical positioning.

Market Share by Application: Supplements Dominate While Functional Foods and Pet Nutrition Expand Rapidly

Dietary supplements and nutraceuticals lead application demand with a 41% share in 2025, supported by preventive healthcare spending, convenient delivery formats such as gummies and ready-to-drink products, and expanding e-commerce and direct-to-consumer channels. Functional food and beverages form the second-largest segment, integrating bioactive ingredients into fortified dairy, plant-based milks, energy drinks, and protein snack bars, with sugar reduction and natural fortification driving innovation. Animal feed and pet nutrition is a rising growth engine as producers adopt probiotics, omega 3s, and phytogenics to support antibiotic-free livestock production and premium functional pet food, reinforced by pet humanization trends. Pharmaceuticals and clinical nutrition require high-purity, clinically validated bioactives for medical foods and OTC formulations, benefiting from aging populations and chronic disease management. Personal care and nutricosmetics, though smallest by volume, are the fastest-growing niche, combining ingestible collagen, hyaluronic acid, and astaxanthin with clean beauty positioning.

Competitive Landscape Analysis of the Bioactive Ingredients Market

The bioactive ingredients market is rapidly shifting toward human-centric health solutions, driven by demand for metabolic support, gut-brain axis nutrition, immunity enhancement, and longevity-focused formulations. Competitive differentiation in 2026 centers on microbiome science, postbiotics and probiotics, ultra-pure vitamins, advanced delivery systems, and flavor-masking technologies that improve daily compliance. Market leaders are moving away from commodity nutrition into clinically validated, lifestyle-integrated bioactives, supported by AI-enabled formulation, vertically integrated agricultural supply chains, and CDMO-scale manufacturing. Strategic priorities include GLP-1 companion nutrition, clean-label sourcing, personalized health platforms, and hybrid food-supplement formats spanning beverages, gummies, skincare, and medical nutrition.

Archer Daniels Midland drives metabolic health innovation through microbiome-led bioactives

ADM is repositioning itself as a leader in human resilience, transitioning from commodity grains to a specialized Health & Wellness platform. Its BPL1 postbiotic and probiotic line anchors a growing microbiome solutions portfolio spanning snacks, supplements, and skincare. In late 2025, ADM released its 2026 Flavor & Color Trend Report, guiding formulation toward citrus-driven “authentic wellbeing” cues aligned with immune-support bioactives. Early 2026 saw the launch of Pepzyme AG, a collagen-digesting enzyme positioned for GLP-1 support and satiety management. Strategically, ADM targets metabolic health and longevity, developing nutrient-dense ingredients for consumers transitioning off anti-obesity medications while expanding companion nutrition ecosystems.

dsm-firmenich accelerates gut-brain and diet transformation with biotech-enabled bioactives

Following restructuring in 2025 and 2026, dsm-firmenich has emerged as a pure-play leader in Nutrition, Beauty, and Taste. The company is finalizing divestment of its Animal Nutrition business to focus exclusively on human bioactives across Taste, Texture & Health and Health, Nutrition & Care. A pioneer in Human Milk Oligosaccharides, dsm-firmenich is expanding HMO applications into adult gut-brain supplements and elderly medical nutrition. Its Global Food Innovation Center in Delft applies biotechnology to convert plant proteins into bioactive-rich meal replacements. Flavor innovations like Frosted Star Anise support odor masking for high-potency vitamins and botanical extracts.

BASF scales ultra-pure vitamins and omega platforms through Verbund integration

BASF leverages its chemical heritage to supply ultra-pure bioactive intermediates, with a 2026 emphasis on sustainable human nutrition. The company remains a global leader in vitamins and carotenoids while expanding high-purity omega-3 fatty acids for premium health applications. BASF is executing a Focus on Core Ingredients strategy, evaluating divestment of feed enzymes to concentrate on pharmaceutical-grade excipients and human bioactives. Production is ramping at its Zhanjiang citral facility, supplying key precursors for aroma and vitamin synthesis. Supported by Verbund integration and renewable electricity at major sites, BASF offers ESG-aligned scale for global wellness brands.

Cargill integrates farm-to-fermentation bioactives for beauty and gut health

Cargill is extending its agricultural dominance into nature-derived bioactives for personal care and human health. Through its Beauty division, Cargill supplies skin lipid mimetics and botanical beads, while EpiCor postbiotic is being adapted from supplements into beauty-from-within beverages. In early 2026, the company showcased SmartCare, originally developed for dairy calves, now serving as a foundational gut-health technology for human platforms. Cargill’s sustainable sourcing initiatives ensure full traceability of bioactive thickeners and antioxidants. Its unique soil-to-supplement integration stabilizes pricing and supply, enabling scalable postbiotic and fermented ingredient production during global disruptions.

Kerry Group combines clinical bioactives with advanced flavor masking technologies

Kerry Group has transformed into a Taste & Nutrition powerhouse, specializing in making functional ingredients enjoyable for everyday consumption. Its BC30 probiotic and Wellmune immunity platforms anchor a growing portfolio of lifestyle-led formats including gummies and dissolving strips. In January 2026, Kerry released its Nutritional Supplement Flavor Map for APMEA, highlighting fermented and natural profiles as key bioactive carriers. The company’s Category Crashers strategy targets hybrid products such as savory energy bars and coffee-infused supplement shots. Kerry differentiates through science-backed taste systems, pairing clinical substantiation with flavor technologies that enable daily wellness rituals.

Lonza pioneers complex bioactive manufacturing and personalized nutrition modalities

Lonza stands as the world’s leading CDMO for complex bioactive molecules and delivery systems. Its Capsules & Health Ingredients division features UC-II undenatured type II collagen, a gold standard for joint health formulations. In early 2026, Lonza completed integration of its Vacaville site while restructuring its CHI business into a pure-play biologics and health actives platform. AI-driven image analysis tools introduced in late 2025 now detect polysorbate degradation, extending shelf life of liquid supplements. Lonza’s 2026 R&D focus centers on complex modalities, including bioconjugates and mRNA-based nutrition, targeting future personalized, gene-informed bioactive therapies.

United States Bioactive Ingredients Market: Model-Based Safety, Peptide Scale, and Upcycled Inputs

The United States bioactive ingredients landscape is being reshaped by regulatory modernization, capital-intensive biomanufacturing, and rapid translation from discovery to commercialization. Following full implementation of the FDA Modernization Act 2.0, developers are increasingly relying on in-silico modeling and organ-on-a-chip systems to substantiate safety, materially reducing dependence on animal testing while accelerating timelines for novel bioactives. This shift has expanded the pipeline of peptides, metabolites, and small molecules designed with computational toxicology and efficacy screens.

Manufacturing depth is scaling in parallel. In April 2025, Thermo Fisher Scientific announced a USD 2 billion investment across U.S. manufacturing, with a meaningful allocation to sterile fill-finish and bioactive peptide production. Contract development capacity followed suit as Polypeptide Laboratories and peers expanded U.S. footprints in late 2025 to meet demand for GLP-1 analogues and metabolic-regulating peptides. Innovation at the consumer edge is also accelerating. Startups supported by National Institutes of Health introduced stabilized NAD+ precursors and Urolithin A variants in late 2025 for longevity positioning. Sustainability is now embedded in approvals. Updated 2026 GRAS guidance from the United States Department of Agriculture and the U.S. Food and Drug Administration rewards upcycled agricultural side-streams, such as grape pomace polyphenols, with expedited certification.

India Bioactive Ingredients Market: Policy-Led Biomanufacturing and Botanical Commercialization

India’s bioactive ingredients industry is advancing through a coordinated policy framework that prioritizes scale, indigenous knowledge, and export readiness. The BioE3 Policy ratified in August 2024 established national Bio-Enabler Hubs for high-performance biomanufacturing, with emphasis on bio-based vitamins and probiotics to serve domestic nutrition and global supply chains. This policy clarity has catalyzed private investment and public infrastructure build-out.

Ecosystem expansion is visible on the ground. In late 2025, the Office of the Principal Scientific Adviser to the Government of India announced expansion of Science and Technology Clusters from 8 to 25 hubs, focusing on commercialization of indigenous botanical extracts and Ayurveda-inspired bioactives. Energy-chemicals convergence is unlocking new intermediates as Reliance Industries Limited integrates bio-refinery modules to produce renewable precursors for antioxidant bioactives. Discovery is being accelerated by a USD 250 million joint fund launched in November 2025 by the Department of Biotechnology and Biotechnology Industry Research Assistance Council, targeting AI-driven enzyme and postbiotic development. Deal flow momentum from Global Bio-India 2025 secured a USD 500 million investment pipeline for Make-in-India bioactives bound for EU and North American markets.

South Korea Bioactive Ingredients Market: Large-Scale Biologics and Nutricosmetic Innovation

South Korea is consolidating leadership in bioactive proteins and consumer-facing bioactives by pairing mega-scale infrastructure with fast product cycles. In early 2025, Lotte Biologics began construction of its USD 3.3 billion Songdo Bio Campus, designed to host three biomanufacturing plants totaling 360,000 liters for bioactive proteins and antibodies. This scale positions Korea as a preferred manufacturing base for complex bioactives requiring stringent quality systems.

Demand pull from beauty and wellness is equally strong. Capitalizing on K-Beauty leadership, Korean firms introduced microencapsulated ceramides and fermented vegan collagen bioactives in December 2025 to enhance skin-barrier penetration and bioavailability. Digital oversight is being layered in. The Ministry of Food and Drug Safety launched a 2026 Digital Health Initiative to integrate supplement tracking with national health apps, enabling monitoring of efficacy in personalized nutrition programs and improving post-market surveillance.

Germany Bioactive Ingredients Market: Carbon-Neutral Bioactives and Circular Feedstocks

Germany’s bioactive ingredients industry is defined by carbon neutrality targets, circular feedstocks, and rigorous compliance. In 2025, BASF SE expanded its Scopeblue portfolio with carbon-neutral bio-based carotenoids produced using renewable electricity and bio-based inputs at Ludwigshafen. This aligns premium bioactives with audited sustainability credentials demanded by EU buyers.

Circular infrastructure is advancing discovery and conversion. In September 2025, the Federal Ministry of Education and Research funded a EUR 100 million program to build biofoundries capable of converting industrial CO2 into omega-3 fatty acids via specialized microbial strains. Regulatory leadership remains a differentiator. German manufacturers have moved early to comply with IFRA 52nd Amendment requirements, ensuring fragrance and flavor bioactives meet the 2026 skin-sensitization benchmarks and de-risking downstream brand adoption.

China Bioactive Ingredients Market: Fermentation Scale, Healthy Aging, and Export Qualification

China continues to scale bioactives through fermentation leadership, targeted public health priorities, and export-grade compliance. Shandong province has consolidated global leadership in fermentation-derived hyaluronic acid and EPA/DHA algae oils, with AI-managed bioreactors delivering yield gains of roughly 15% in 2025. This operational sophistication supports consistent quality at industrial scale.

Policy alignment is steering R&D. The Healthy China 2030 agenda has catalyzed government-backed programs targeting bioactives for healthy aging, including compounds addressing macular degeneration and bone density. Export readiness is improving as well. In late 2025, Chinese producers achieved European Food Safety Authority Novel Food status for several monk fruit-derived bioactives, unlocking high-purity export channels into the EU and reinforcing China’s position across nutraceutical and functional food applications.

Country-Level Strategic Snapshot: Bioactive Ingredients Industry

Bioactive Ingredients Market County Level Snapshot

|

Country / Region

|

Strategic Focus

|

Key Developments

|

|

United States

|

Model-based safety and peptide scale

|

FDA Modernization 2.0 adoption, Thermo Fisher investment, GLP-1 CDMO expansion, upcycled GRAS pathways

|

|

India

|

Policy-led biomanufacturing

|

BioE3 hubs, S&T cluster expansion, AI-driven enzyme funding, export deal pipeline

|

|

South Korea

|

Large-scale biologics and nutricosmetics

|

Songdo Bio Campus build-out, microencapsulated skin bioactives, digital health integration

|

|

Germany

|

Carbon-neutral and circular bioactives

|

Scopeblue carotenoids, CO2-to-omega-3 biofoundries, IFRA compliance leadership

|

|

China

|

Fermentation scale and export qualification

|

AI-managed bioreactors, Healthy China 2030 R&D, EFSA Novel Food approvals

|

Bioactive Ingredients Market Report Scope

Bioactive Ingredients Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$176.1 Billion

|

|

Market Size (2034)

|

$360.9 Billion

|

|

Market Growth Rate

|

8.3%

|

|

Segments

|

By Ingredient Type (Vitamins and Minerals, Amino Acids Peptides and Proteins, Probiotics Prebiotics and Postbiotics, Omega 3 and Fatty Acids, Plant Extracts and Phytochemicals, Specialized Bioactives), By Source (Plant Based, Animal Based, Microbial Based), By Purity and Form (Ultra High Purity, Standardized Extracts, Powder Liquid Capsule and Microencapsulated), By Application (Functional Food and Beverages, Dietary Supplements and Nutraceuticals, Personal Care and Nutricosmetics, Pharmaceuticals and Clinical Nutrition, Animal Feed and Pet Nutrition), By Functionality (Immunity and Respiratory Support, Cognitive Health and Nootropics, Gut Health and Microbiome Support, Metabolic and Cardiovascular Health, Longevity and Anti Aging)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Archer Daniels Midland Company, BASF SE, Cargill Incorporated, DSM Firmenich, Kerry Group, International Flavors and Fragrances, Lonza Group, Ingredion Incorporated, Evonik Industries, Givaudan, Glanbia, Ajinomoto, Symrise, Arla Foods Ingredients, Sabinsa Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Bioactive Ingredients Market Segmentation

By Ingredient Type

- Vitamins and Minerals

- Amino Acids Peptides and Proteins

- Probiotics Prebiotics and Postbiotics

- Omega 3 and Fatty Acids

- Plant Extracts and Phytochemicals

- Specialized Bioactives

By Source

- Plant Based

- Animal Based

- Microbial Based

By Purity and Form

- Ultra High Purity

- Standardized Extracts

- Powder Liquid Capsule and Microencapsulated

By Application

- Functional Food and Beverages

- Dietary Supplements and Nutraceuticals

- Personal Care and Nutricosmetics

- Pharmaceuticals and Clinical Nutrition

- Animal Feed and Pet Nutrition

By Functionality

- Immunity and Respiratory Support

- Cognitive Health and Nootropics

- Gut Health and Microbiome Support

- Metabolic and Cardiovascular Health

- Longevity and Anti Aging

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Bioactive Ingredients Industry

- Archer Daniels Midland Company

- BASF SE

- Cargill Incorporated

- DSM Firmenich

- Kerry Group

- International Flavors and Fragrances

- Lonza Group

- Ingredion Incorporated

- Evonik Industries

- Givaudan

- Glanbia

- Ajinomoto

- Symrise

- Arla Foods Ingredients

- Sabinsa Corporation

*- List not Exhaustive