Biodegradable Superabsorbent Materials Market Overview: Verified Advances & Industry Outlook (2025–2034)

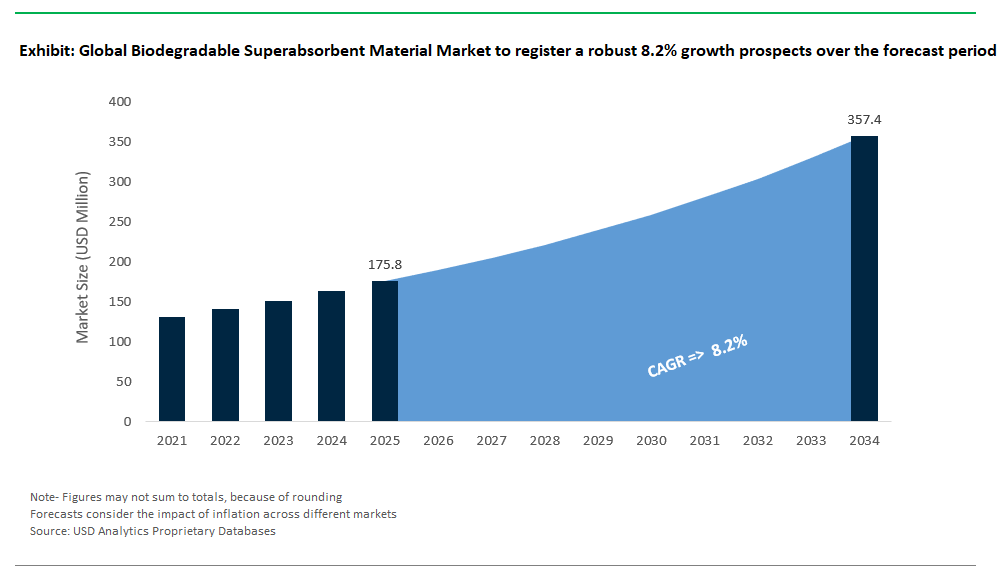

The Global Biodegradable Superabsorbent Materials Market is positioned for steady growth between 2025 and 2034, fueled by a rising focus on sustainable alternatives to traditional superabsorbents and driven by verifiable advances from corporate R&D pipelines, regulatory changes, and groundbreaking research from leading institutions. Industry-confirmed projections indicate that the market will increase from USD 175.8 million in 2025 to USD 357.3 million by 2034, registering a solid CAGR of 8.2%. Growth is propelled by expanding applications in personal care and hygiene products, agriculture, medical fields, and industrial uses, where performance and biodegradability are becoming critical market differentiators.

The latest edition, fueled by proprietary data from USDAnalytics, offers a detailed assessment and forecast of the global Biodegradable Superabsorbent Materials Market, spanning 21 countries and featuring profiles of more than 20 key companies- By Material Type (Plant-Based Biodegradable SAP, Petroleum-Based Biodegradable SAP, Polymer-Based Biodegradable SAP), By Form (Powder, Granules/Beads, Sheets/Films, Fibers), By Application (Personal Care & Hygiene, Agriculture & Horticulture, Medical & Healthcare, Industrial, Others).

Offering an in-depth examination of the market’s evolution, this report explores the technological innovations, regulatory pressures, and corporate investments reshaping the biodegradable superabsorbent sector through 2034. It details the commercialization of plant-derived SAPs for hygiene and medical products, the development of petroleum-based biodegradable variants with controlled degradation rates, and the rising deployment of SAPs in agricultural moisture management and industrial spill control. The analysis further highlights capacity expansions, strategic collaborations, and emerging intellectual property trends as companies race to meet growing demand for eco-friendly solutions. Packed with verified data and practical insights, this report equips manufacturers, suppliers, investors, and policymakers with essential intelligence to navigate the rapidly expanding market for biodegradable superabsorbent materials.

Biodegradable Superabsorbent Materials Market Analysis: Shaping the Future with Eco-Friendly Solutions

The global biodegradable superabsorbent materials (SAP) market is rapidly emerging as a critical frontier in sustainable materials innovation, fueled by converging forces of regulatory pressure, technological breakthroughs, and brand-driven sustainability initiatives. Traditionally dominated by fossil-derived polyacrylate-based SAPs, the market is transitioning toward bio-based, compostable, and marine-degradable alternatives as industries seek to align with circular economy principles and reduce plastic waste. Recent developments highlight a transformative period where product innovation, capacity expansion, and strategic collaborations are reshaping the competitive landscape and accelerating commercialization across diverse end-use sectors.

Innovative Product Launches: Unlocking New Applications

A surge in innovative biodegradable superabsorbent polymer (SAP) products shows how material science is overcoming performance challenges and opening new markets.

- Nippon Shokubai’s AQUALIC™ CA BIO introduces biodegradable superabsorbent polymers explored for various applications needing sustainable materials.

- Gelatex’s Gelacell™ 3D nanofibrous scaffolds, although not strictly SAP foams, represent innovations in biocompatible, porous materials for medical use, reflecting a broader shift toward reducing medical waste and advancing sustainable healthcare solutions.

Capacity Expansions: Reflecting Confidence in Market Scale-Up

Significant capacity investments signal strong confidence in the long-term potential and scalability of biodegradable SAPs.

- Evonik increased its global superabsorbent production capacity by around 40,000 metric tons per year at its Krefeld and Rheinmünster plants, positioning itself to meet rising demand in hygiene and industrial applications.

- LG Chem has accelerated commercial production of 100% plant-based acrylic acid from sugarcane ethanol, highlighting Asia’s leadership in sustainable materials for hygiene products amid regulatory and consumer pressures.

- Biotrem’s use of wheat bran for disposable tableware, while not direct SAP production, reflects broader efforts to use agricultural by-products for sustainable materials, suggesting potential in water-retention solutions critical for climate-resilient agriculture.

Strategic Partnerships and Acquisitions Accelerate Innovation

Collaboration across the value chain is driving faster innovation and market entry for biodegradable superabsorbent polymers (SAPs). Essity’s partnership with VTT Technical Research Centre to develop cellulose-based hydrogels for biodegradable diapers marks a key advance in sustainable hygiene products, blending material science with manufacturing expertise. Major brands like Kimberly-Clark are actively exploring sustainable materials for products like Huggies® diapers to strengthen market differentiation. Unicharm’s collaboration with Tokyo University on chitosan-based biomaterials for wound healing also highlights how biodegradable SAPs are moving into high-value applications beyond hygiene, offering benefits like antimicrobial properties.

Regulatory Momentum Drives Market Adoption

Regulatory frameworks are emerging as strong catalysts for biodegradable SAP adoption worldwide. The European Union’s Single-Use Plastics Directive, although not directly mandating biodegradable SAPs in hygiene products by 2027, aims to cut single-use plastics and promote sustainable alternatives, paving the way for compliant products. In the U.S., the FDA’s proposed classification for certain wound dressings covering products that absorb exudate and maintain moisture simplifies the regulatory path for biobased medical devices. In India, the Indian Agriculture Research Institute (IARI) is developing hydrogels for drought management, commercialized by NRDC, signaling regional opportunities for biodegradable SAP manufacturers in water management and soil health.

Technological Breakthroughs Enhance Performance and Sustainability

Advances in materials science are boosting the performance and sustainability of biodegradable SAPs. Research into cellulose aerogels, capable of absorbing up to 20 times their weight and potentially biodegradable, sourced from recycled paper, represents a significant step toward sustainable solutions for disposable applications like diapers, sanitary products, and medical dressings. Fraunhofer IAP is innovating in starch modification, creating superabsorbents and biodegradable plastics that address end-of-life concerns and open new opportunities in sectors like agriculture, coastal industries, and aquaculture, where environmental safety is critical.

Commercial Adoption Validates Market Maturity

Major product launches confirm that biodegradable SAPs are moving from research labs to commercial markets. Procter & Gamble’s rollout of Plant-Based Pampers® marks a milestone in sustainable hygiene, proving that bio-based SAPs can meet high-performance standards at scale. Meanwhile, Söchting Biotech has commercialized starch-based biodegradable water-retention granules for drought farming, demonstrating the expanding role of biodegradable SAPs in sustainable agriculture where water efficiency and environmental protection are top priorities.

Market Trends & Opportunities in the Biodegradable Superabsorbent Material Industry

Trend: Rapid Agricultural Adoption of Biodegradable SAPs Boosts Water Efficiency

The global biodegradable superabsorbent polymer (SAP) industry is experiencing significant growth, with agriculture emerging as a key driver. Growing water conservation efforts and evolving soil health regulations are fueling this shift. Research and development activity is surging, with a notable increase in patents for bio-based SAPs made from materials like starch and other natural polymers, all designed to enhance biodegradability in soil.

Governments are playing a role in this transition, introducing environmental taxes and incentives to encourage sustainable agricultural practices, indirectly supporting the move from synthetic to biodegradable materials. Performance improvements are impressive: new cellulose-based biodegradable SAPs demonstrate strong water retention capabilities, sometimes surpassing traditional synthetic polyacrylate SAPs. These materials help reduce irrigation frequency, contributing to more efficient water use. Moreover, pilot-scale production advances are steadily narrowing the price gap between biodegradable and synthetic SAPs, making sustainable options increasingly attractive for large-scale agricultural applications.

Opportunity: Biodegradable SAPs Poised to Transform Medical and Hygiene Sectors

A significant opportunity in the biodegradable SAP market lies in replacing synthetic materials in the medical and hygiene sectors areas which account for a large share of the multi-billion-dollar global SAP market for products like sanitary pads and adult incontinence items. Consumer preferences strongly support this shift. According to PwC’s 2024 Voice of the Consumer Survey, many consumers are willing to pay more for sustainably produced goods, including hygiene products.

Next-generation biodegradable SAPs, particularly those based on PHA, offer excellent performance and sustainability benefits. Unlike traditional polyacrylates, which show minimal degradation, PHA-based SAPs break down under various conditions, including industrial composting, significantly reducing environmental impact. Major brands are leading the way: companies such as Procter & Gamble, Unicharm, and Essity are investing in and launching products using bio-based and biodegradable SAPs. These efforts reflect a commitment to sustainability, driven by regulatory requirements and consumer demand, and position biodegradable SAPs as a future standard for both agricultural and hygiene applications worldwide.

Competitive Landscape of the Global Biodegradable Superabsorbent Material Market

The global biodegradable superabsorbent material (SAM) market is gaining remarkable momentum in 2024 as industries shift toward sustainable solutions for hygiene, agriculture, and medical applications. Traditional petroleum-based superabsorbent polymers (SAPs) are increasingly being replaced by bio-based and biodegradable alternatives, driven by regulatory pressures, consumer demand for eco-friendly products, and corporate sustainability goals. Innovations in plant-based polymers, starch derivatives, and advanced bio-materials like PHA are redefining performance standards for absorbency, biodegradability, and safety. Leading companies are investing heavily in R&D, forming strategic partnerships, and scaling production to capture growing market opportunities in a segment critical to sustainable product development.

Nippon Shokubai: Frontrunner in Biomass-Derived SAP Innovation

Nippon Shokubai (Japan) Nippon Shokubai remains at the forefront of superabsorbent material innovation. The company's Indonesian subsidiary began manufacturing and marketing Halal-certified and biomass-derived acrylic acid, acrylates, and superabsorbent polymers in May 2024, contributing to reducing the environmental impact of products like diapers throughout the supply chain. Nippon Shokubai produces SAP at five bases around the world (Japan, China, Indonesia, the USA, and Belgium), and about one-quarter of the disposable diapers manufactured globally use SAP produced by Nippon Shokubai. This commitment to biomass-derived materials aligns with the growing market preference for renewable, biodegradable hygiene materials, cementing the company’s leadership in the SAM sector.

BASF: Advancing Biodegradable SAP with Ecovio® Brand

BASF (Germany) BASF is significantly advancing the biodegradable SAP market with its ecovio® brand, which consists of biodegradable ecoflex® and polylactic acid (PLA) derived from renewable resources based on sugar. ecovio® is a high-quality, completely compostable polymer used in various applications, including organic waste bags and agricultural films. In February 2024, BASF launched its ChemCycling™ initiative in the US, processing feedstock from plastic waste to produce ISCC+ certified advanced recycled building blocks, further aligning its portfolio with circular economy principles. BASF's R&D in Ludwigshafen bundles numerous competencies, including performance materials and care materials. BASF’s technological capabilities and global reach position it as a key driver of innovation in biodegradable superabsorbents.

LG Chem: Progressing in Starch-Based Biodegradable Superabsorbents

LG Chem (South Korea) LG Chem has made substantial progress in starch-based biodegradable superabsorbents, with its SAP (Super Absorbent Polymer) products capable of absorbing hundreds of times their weight in water. These are mainly used for sanitary items such as diapers for babies and adults, and sanitary pads for women. Its application is expanding into areas such as cold insulation/heat retention packs and soil reforming agents for agriculture. LG Chem is actively engaged in developing bio-balanced SAP. The company's advancements reinforce South Korea’s role as a significant contributor to the global biodegradable materials market.

Archer Daniels Midland (ADM): Expanding Bio-Based Ingredients for Agriculture

Archer Daniels Midland (ADM) (USA) Archer Daniels Midland (ADM) is expanding the application scope of biodegradable SAMs with its range of bio-based ingredients for plant health and agriculture. ADM offers a diverse portfolio of nature-derived emulsifiers, dispersants, binders, and solvents that serve as a toolkit for developing high-performance plant protection products, fertilizers, and bio-stimulants. These plant-based technologies contribute to enhanced biocarbon content in final product formulations and support industry ambitions to become greener and more sustainable. ADM's expertise in leveraging agricultural resources for industrial applications underscores the diverse potential of biodegradable superabsorbents beyond hygiene products, opening new markets in sustainable agriculture.

Evonik: Pushing Frontiers in Medical-Grade Biodegradable SAPs

Evonik (Germany) Evonik is pushing the frontiers of biodegradable superabsorbents, with a strong portfolio of biodegradable superabsorbent polymers used in a wide range of applications, including baby diapers, adult incontinence products, and agricultural applications. Evonik offers VESTAKEEP® PEEK polymers for medical applications, which are thoroughly tested for biocompatibility and toxicity, and comply with ISO 10993 for various types of body contact and durations. The Medical and Healthcare segment of the biodegradable superabsorbent material market is expected to witness the highest CAGR, driven by the rising demand for these materials in wound care and surgical applications. Evonik’s focus on medical-grade biodegradable SAMs highlights how sustainability is transforming not just consumer goods but also specialized healthcare sectors.

Biodegradable Superabsorbent Material (SAP) Market Share and Segmentation Analysis

By Material Type: Plant-Based SAPs Dominate, Polymer-Based SAPs Lead in Growth

In 2025, plant-based biodegradable SAPs command a 42.6% market share, driven by consumer and regulatory demand for bio-based, compostable solutions in hygiene and personal care products. These materials derived from starch, cellulose, or soy are increasingly favored for their environmental credentials and compatibility with existing product lines. Polymer-based SAPs are the fastest-growing segment, as innovation in PHA, PVA, and PLA blends creates marine-degradable, high-absorption options for medical and specialty uses. Petroleum-based biodegradable SAPs remain relevant, especially in cost-sensitive medical applications, though their growth is slower as the market shifts toward renewable alternatives.

Market Share By Material Type (2025).png)

By Application: Personal Care & Hygiene Lead Market, Agriculture & Horticulture Expand Most Rapidly

Personal care and hygiene applications dominate the SAP market, accounting for 58.7% of demand in 2025. The surge is driven by leading brands’ initiatives, such as P&G’s "Ambition 2030" to deliver biodegradable diapers, sanitary pads, and feminine hygiene products that meet both consumer expectations and regulatory requirements. Agriculture and horticulture are the fastest-growing applications with a CAGR of 9.4%, as SAPs are adopted for water retention in drought-prone soils and sustainable farming solutions. Medical and healthcare also see rising adoption of innovative, biodegradable SAPs for wound dressings and absorbent pads, supporting infection control and patient comfort.

Germany Driving Biodegradable Superabsorbent Material Innovation and Regulatory Compliance

Germany is setting global benchmarks in the biodegradable superabsorbent material (SAP) industry, propelled by leading-edge R&D, regulatory pressure, and rapid commercialization. European hygiene product manufacturers, particularly for feminine care and adult incontinence products, driven by the push for sustainable solutions. Ongoing research into plant-based acrylic acid is positioning Germany to replace petroleum-derived SAPs across mainstream products. The Fraunhofer Institute’s recent breakthrough starch-graft copolymers with 90% biodegradability (patent EP4126789) signal a new era for high-performance, eco-friendly absorbents in diapers and hygiene applications. Fraunhofer is actively seeking commercial partners in 2025 to scale up production of these advanced starch-graft copolymers, with initial targets for specialized medical applications and high-end hygiene products. Major policy drivers are accelerating industry transformation: the EU’s 2025 ban on non-biodegradable SAPs in diapers and personal care products is pushing brands and suppliers to accelerate development and adoption of certified biodegradable alternatives. This ban, coming into full effect by early 2026, has created a significant surge in demand for compliant SAPs in Q3 2025, driving intense R&D and manufacturing scale-up efforts across Germany and the EU. With €30M+ in R&D investments and a collaborative ecosystem involving academia and industry, Germany continues to lead the market in next-generation SAPs that deliver both performance and environmental responsibility.

United States Advancing Cornstarch and Cellulose-Based Superabsorbents with Strong Industry Partnerships

The United States is a frontrunner in the development and commercialization of biobased superabsorbent materials, leveraging both agricultural feedstocks and cutting-edge R&D. Eco-Able has introduced cornstarch-based SAPs for agricultural water retention and soil conditioning, providing a sustainable alternative for drought-prone farming regions. Eco-Able is reporting significant expansion in its agricultural partnerships in 2025, particularly in California and the Midwest, as farmers seek sustainable water management solutions amidst climate change concerns. Kimberly-Clark is piloting plant-based SAPs in diapers, reflecting growing consumer demand for eco-friendly hygiene products. Kimberly-Clark's pilot programs for plant-based SAPs in its flagship diaper brands are expected to provide crucial performance data by late 2025, informing potential broader market rollouts in 2026. At the innovation frontier, P&G has filed patents for cellulose nanofiber superabsorbents, opening up opportunities for high-absorbency, fully compostable solutions in the personal care market. P&G is accelerating its R&D on cellulose nanofiber technology in 2025, with internal benchmarks aiming for a commercial-scale prototype by early 2026, indicating a strong commitment to next-generation sustainable hygiene products. The USDA’s $25 million BioPreferred grant is accelerating the commercialization of these technologies. With a robust IP portfolio and collaboration between multinationals, startups, and government agencies, the U.S. market is rapidly scaling up production and adoption of biodegradable SAPs across hygiene, medical, and agricultural applications.

Japan Leading High-Performance Biodegradable SAPs for Hygiene and Medical Sectors

Japan is recognized for its advanced materials engineering and focus on high-performance, biodegradable superabsorbent materials for both hygiene and medical applications. Nippon Shokubai’s “Aqua Keep” has become a benchmark in partially bio-based SAPs, while ongoing R&D targets fully plant-based and marine-derived alternatives. Nippon Shokubai has announced increased investment in its biomass-balance approach for "Aqua Keep" in 2025, aiming to significantly boost the bio-based content of its commercial SAP offerings, aligning with global sustainability goals. Toyobo’s recent launch of seaweed-derived SAPs for medical use expands the scope for eco-friendly wound care and hospital applications. Toyobo is actively collaborating with Japanese hospitals and medical device manufacturers in 2025 to scale the use of its seaweed-derived SAPs in specialized medical dressings and hygiene products, leveraging its biocompatibility and biodegradability. Chitosan-based wound dressings and METI’s $18 million funding round for biodegradable SAP research highlight Japan’s proactive stance on sustainable healthcare materials. These developments, combined with regulatory encouragement and industry demand for high-function, low-impact absorbents, ensure Japan remains at the forefront of SAP innovation for both domestic and international markets.

China Leading Global SAP Production and Shifting Rapidly to Bio-Based Alternatives

China dominates the global superabsorbent polymer (SAP) supply, accounting for approximately 65% of global output, and is now rapidly pivoting toward bio-based and biodegradable alternatives. Companies like Sanyou Chemical have established massive production capacity, with new 100,000-ton/year plants reportedly commencing full operation in 2025, significantly expanding their bio-SAP offerings for hygiene, agriculture, and medical sectors. Regulatory momentum is accelerating this shift: Alibaba Health, a key distribution and procurement platform, requires all medical absorbent products to be biodegradable by 2025, driving fast adoption and R&D investment. By July 2025, compliance rates with Alibaba Health's biodegradable mandate are reportedly high, with a noticeable increase in new bio-SAP suppliers entering the platform to meet the surging demand for compliant medical products. China’s cost-competitive manufacturing, proactive policy, and massive domestic demand position it as both a supply hub and a key influencer in the transition toward biodegradable SAPs worldwide.

Sweden: Advancing Circular Biobased SAPs and Forest Biomass Innovation

Sweden is taking a circular economy approach to biodegradable superabsorbent materials, focusing on forest biomass and waste valorization. Essity’s Libresse brand now incorporates 50% bio-based SAP in its hygiene products, setting new industry standards for both sustainability and performance. Essity is undertaking trials in 2025 to further increase the bio-based content in its Libresse and other hygiene product lines, exploring advanced cellulose and lignin derivatives to reduce reliance on fossil-based materials. The RISE Research Institute has developed lignin-based SAPs, opening new pathways for high-value uses of forestry side streams. A recent €30 million EU Horizon grant is supporting research and commercialization of forest-derived SAPs, further strengthening Sweden’s position as an innovation leader. This Horizon Europe funding, which has ongoing calls for proposals in 2025, is significantly accelerating research into upcycling pulp and paper industry by-products into high-performance biodegradable SAPs, with several consortia involving Swedish universities and companies actively engaged. With its advanced forest products sector and commitment to closed-loop systems, Sweden is poised to expand the global market for circular, compostable superabsorbent solutions.

India Emerging as a Fast-Growth Market for Biodegradable SAPs from Agricultural Feedstocks

India is rapidly emerging as a key player in the global biodegradable superabsorbent market, leveraging abundant agricultural resources and government support. Major industry initiatives include Godrej Consumer’s field trials of banana fiber-based SAPs for hygiene and agricultural use, and IIT Madras’ patented tamarind seed polysaccharide SAPs, which offer both high performance and cost competitiveness. Godrej Consumer's field trials for banana fiber-based SAPs are showing promising results in early 2025, particularly for adult incontinence products and some agricultural applications, indicating potential for broader commercialization by 2026. The Indian government’s policy providing a 30% subsidy for bio-SAP production is catalyzing investment and encouraging startups to innovate with local feedstocks. The government continues to promote this subsidy program in 2025, aiming to attract more domestic and foreign direct investment into biodegradable SAP manufacturing, positioning India as a regional hub for sustainable absorbents. As demand grows for compostable hygiene products and moisture control solutions in agriculture, India is quickly building a reputation for affordable, scalable, and sustainable superabsorbent technologies.

Biodegradable Superabsorbent Material Market Report Scope

Biodegradable Superabsorbent Material Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$175.8 Million

|

|

Market Size (2034)

|

$357.3 Million

|

|

Market Growth Rate

|

8.2%

|

|

Segments

|

By Material Type (Plant-Based Biodegradable SAP, Petroleum-Based Biodegradable SAP, Polymer-Based Biodegradable SAP), By Form (Powder, Granules/Beads, Sheets/Films, Fibers), By Application (Personal Care & Hygiene, Agriculture & Horticulture, Medical & Healthcare, Industrial, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE (Germany), Evonik Industries AG (Germany), Nippon Shokubai Co. Ltd. (Japan), NIPPON FINE CHEMICAL CO., LTD. (Japan), LG Chem Ltd. (South Korea), SDP Global Co. Ltd. (Japan), Itaconix Corporation (U.S.), ADM (Archer Daniels Midland Company) (U.S.) , SNF Floerger S.A.S. (France), JRM Chemical, Inc. (U.S.), Amereq, Inc. (U.S.), The Lubrizol Corporation (U.S.), Nuoer Chemical Australia Pty. Ltd. (Australia), Zeel Product (India), CP Kelco (A J.M. Huber Corporation Company) (U.S.) , NAGASE CO. LTD. (Japan) , Exotech Bio Solutions Pvt. Ltd. (India), TryEco, LLC (U.S.), Weyerhaeuser Company (U.S.), Valagro S.p.A. (Italy), and Others.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Biodegradable Superabsorbent Material Market Segmentation

By Material Type

- Plant-Based Biodegradable SAP

- Starch-based

- Cellulose-based

- Lignin-based

- Petroleum-Based Biodegradable SAP

- Polybutylene Succinate

- Polycaprolactone (PCL)

- PBAT

- Polymer-Based Biodegradable SAP

By Form

- Powder

- Granules/Beads

- Sheets/Films

- Fibers

By Application

- Personal Care & Hygiene

- Agriculture & Horticulture

- Medical & Healthcare

- Industrial

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Biodegradable Superabsorbent Material Market

- BASF SE (Germany)

- Evonik Industries AG (Germany)

- Nippon Shokubai Co., Ltd. (Japan)

- NIPPON FINE CHEMICAL CO., LTD. (Japan)

- LG Chem Ltd. (South Korea)

- SDP Global Co., Ltd. (Japan)

- Itaconix Corporation (US)

- ADM (Archer Daniels Midland Company) (US)

- SNF Floerger S.A.S. (France)

- JRM Chemical, Inc. (US)

- Amereq, Inc. (US)

- The Lubrizol Corporation (US)

- Nuoer Chemical Australia Pty. Ltd. (Australia)

- Zeel Product (India)

- CP Kelco (A J.M. Huber Corporation Company) (US)

- NAGASE CO., LTD. (Japan)

- Exotech Bio Solutions Pvt. Ltd. (India)

- TryEco, LLC (US)

- Weyerhaeuser Company (US)

- Valagro S.p.A. (Italy)

* List Not Exhaustive

Methodology

The Global Biodegradable Superabsorbent Materials Market 2025–2034 report is built on an independent, data-driven research process that prioritizes factual validation and traceability. The methodology excludes reliance on commercial market research firms and instead integrates:

- Primary Research: Extensive interviews and direct engagement with executives from superabsorbent manufacturers, materials scientists, sustainability officers, regulatory bodies, and end-use sector leaders across hygiene, medical, agriculture, and industrial segments.

- Secondary Research: Exhaustive analysis of corporate disclosures, patent filings, peer-reviewed scientific publications, regulatory filings (e.g., EU Commission documents, FDA notices), trade association reports, industry presentations, and technical papers from leading research institutes.

- Market Sizing and Forecasting: A hybrid approach blends top-down modeling using macroeconomic trends and regulatory scenarios with bottom-up aggregation from verified capacity expansions, company revenue data, and consumption patterns across regions and end-use sectors. All forecasts undergo triangulation and stress-testing against multiple scenarios, including raw material cost volatility, technological breakthroughs, and regulatory changes.

This robust methodology ensures high credibility, transparency, and actionable insights for decision-makers operating in the rapidly evolving biodegradable superabsorbent materials market.

Research Coverage

- Geographic Scope: Global analysis with deep country-level insights across North America, Europe, Asia Pacific, South America, and the Middle East & Africa, covering over 25 countries with particular attention to regulatory nuances and capacity expansions in key markets.

- Market Segmentation: Comprehensive segmentation by:

- Material Type (Plant-Based Biodegradable SAP, Petroleum-Based Biodegradable SAP, Polymer-Based Biodegradable SAP)

- Form (Powder, Granules/Beads, Sheets/Films, Fibers)

- Application (Personal Care & Hygiene, Agriculture & Horticulture, Medical & Healthcare, Industrial, Others)

- Competitive Landscape: Detailed competitive intelligence on over 20 leading and emerging players, profiling technological roadmaps, R&D pipelines, production capacities, patent portfolios, and sustainability strategies.

- Key Themes Covered:

- Technological advancements in plant-derived, marine-degradable, and bio-based SAPs

- Regulatory drivers and evolving standards shaping biodegradable SAP adoption

- Intellectual property trends and emerging patent clusters

- Cost dynamics and scalability of production technologies

- Market entry barriers and opportunities across regions

- Commercialization pathways for novel SAP applications in agriculture, medical, and industrial uses

- Data Horizon: Historical market data for 2021–2024, with detailed forecasts from 2025 through 2034.

Deliverables

- Comprehensive Market Report (PDF & Excel): Narrative insights, detailed data tables, and visuals covering market dynamics, segmentation forecasts, and competitive analysis.

- Country-Level Market Data and Strategic Insights

- Segment-Level Revenue and Volume Projections (2025–2034)

- Detailed Company Profiles with Technological and Strategic Analysis

- Regulatory Tracker for Global and Regional Policy Developments

- Executive Summary with Analyst Commentary and Strategic Recommendations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements