Market Overview: Bonding Films Market Growth Fueled by EV Electronics, Semiconductor Wafer Bonding, and Bio-Based Adhesive Chemistry (2025–2034)

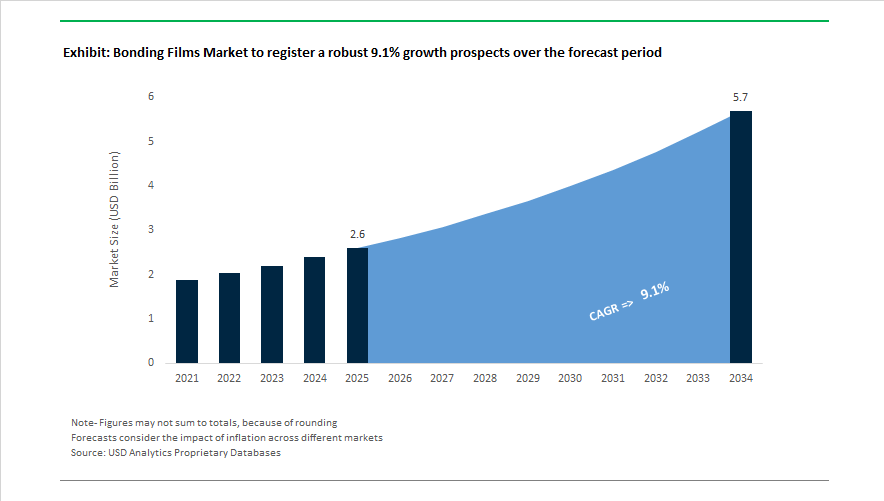

The bonding films market is projected to expand from USD 2.6 billion in 2025 to USD 5.7 billion by 2034, reflecting a CAGR of 9.1% supported by rapid adoption in electric vehicles, semiconductor packaging, advanced displays, aerospace composites, and sustainable packaging systems. Market momentum accelerated in February 2024 when Park Aerospace Corp. launched the Aeroadhere FAE-350-1 structural film adhesive engineered for composite aircraft structures. In July 2024, Henkel inaugurated a new polyurethane film line in Asia-Pacific to supply electronics and automotive OEMs with high-performance bonding films. November 2024 developments included 3M introducing a high-temperature silicone adhesive film for EV battery modules, delivering electrical insulation and thermal stability critical for high-energy battery packs, while Dow Inc. partnered with automotive OEMs to engineer films enabling lightweight bonding between carbon fiber and aluminum components.

Product innovation expanded significantly through 2025. In March 2025, Avery Dennison launched recyclable PET bonding films aligned with circular packaging requirements. During 2025, 3M introduced its SAF6045 structural adhesive film designed for load-bearing automotive metal joints, improving assembly precision in body-in-white production. In October 2025, Henkel debuted an EMI shielding film for automotive electronics to manage electromagnetic interference in sensors and control units. Semiconductor applications advanced in November 2025 when Toray Industries developed PFAS-free temporary bonding materials for ultra-thin wafers used in high-bandwidth memory chips for AI hardware.

Strategic acquisitions, AI integration, and sustainable chemistry are defining the competitive landscape entering 2026. In January 2026, 3M showcased AI-driven virtual material simulation at CES to accelerate custom film development for automotive displays and data center thermal management. In February 2026, Henkel partnered with Sekab to integrate bio-based ethyl acetate into film production and signed an agreement to acquire specialty coatings company Stahl to strengthen its flexible bonding portfolio. During the same month, H.B. Fuller highlighted its Beyond Bonding strategy, focusing on multifunctional films with conductive, flame-retardant, and biodegradable properties.

Electrification and Advanced Electronics Driving Trends and Opportunities in the Bonding Films Market

Thermoplastic and Reworkable Bonding Films Enable EV Battery Repair and Recycling

The electrification of mobility is shifting bonding film selection from permanent thermoset adhesives to thermoplastic formulations that support the full lifecycle of high-voltage battery systems. Global battery regulations require design for disassembly and higher recycled content, making reversible bonding a material selection priority for EV OEMs. New bonding films launched at The Battery Show Europe in June 2025 can deliver structural strength up to 12 MPa during operation and selectively debond during maintenance activities. The adoption of digital twin simulations and automated debonding platforms in major engineering centers further validates that thermoplastic bonding films can replace traditional mica insulators and non-serviceable resin systems. This transformation enhances battery module serviceability, enables second-life utilization, and lowers end-of-life processing costs.

Ultra-Thin Anisotropic Conductive Films Advance Semiconductor Miniaturization and Optical Data Transfers

Packaging innovation in semiconductors and photonics is increasing the importance of ultra-thin Anisotropic Conductive Films (ACF). With leading AI and 5G chipsets requiring denser interconnections, ACF materials below 10 micrometers are becoming essential for forming precise Z-axis electrical pathways. Recent material platforms demonstrated at OFC 2025 introduced reliable, fine-pitch bonding for optical modules operating at 800 Gbps and above. Laser-assisted ACF curing has also reduced bonding cycle time and supported less-than-30-micron pitches needed for chip-on-glass and chip-on-flex assemblies. The shift to ACF is also driven by thermal reliability and space savings compared to solder-based joints, strengthening their role in smartphones, medical wearables, and advanced displays.

Structural Bonding Films Enable Lightweight Composite Assembly in Aerospace

Bonding films are increasingly selected in aerospace production to reduce fastening complexity and minimize stress concentration in carbon fiber reinforced polymer structures. Replacing rivets in secondary assemblies and interiors can create 15 to 20% weight reduction, improving aircraft fuel consumption. High-temperature epoxy and acrylic films are now deployed for composite bonding in nacelles and fan blades and are engineered for durability in humid or high-erosion environments. These advances support broader adoption by emerging electric Vertical Takeoff and Landing aircraft manufacturers, where manufacturing speed, safety, and structural lightness directly influence travel range and payload.

Optically Clear Adhesive Films Unlock Micro-LED Displays and Foldable Form Factors

Demand for high-purity Optically Clear Adhesive (OCA) bonding films continues to expand alongside commercialization of Micro-LED screens and flexible electronics. Premium bonding films require transmission rates above 99% and extremely low haze values to prevent optical distortion while bonding pixel-scale LEDs to substrates. Mechanical performance is equally critical, particularly as foldable devices require more than 200,000 fold cycles without delamination or color change. Leading suppliers are investing in bio-based and UV-curable OCA platforms that maintain clarity and peel strength while lowering volatile organic emissions. These performance attributes are also enabling rapid adoption in curved automotive head-up displays and expanding digital cockpit designs.

Bonding Films Market Share and Segmentation Insights

Market Share by Type: Epoxy Films Lead Structural Applications While Polyurethane and Acrylic Drive Flexibility and Optics

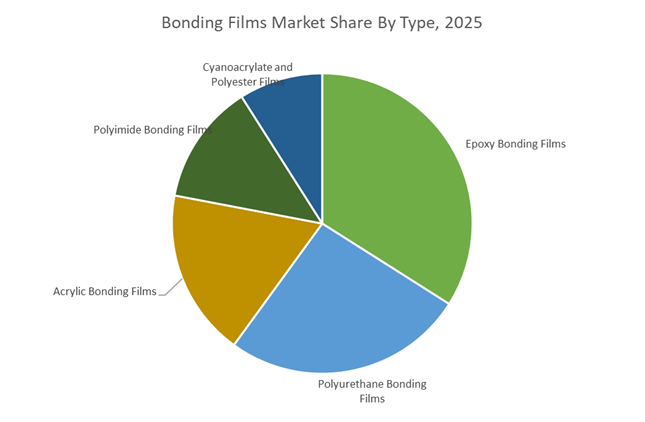

Epoxy bonding films hold 34% of the Bonding Films Market in 2025, reflecting their unmatched mechanical strength, chemical resistance, and sustained thermal performance beyond 200°C, making one-part heat-cured epoxies the standard for aerospace composites, automotive lightweight structures, and electronics encapsulation. Polyurethane bonding films represent the second-largest segment, valued for flexibility, impact resistance, and low-temperature durability, particularly in bonding dissimilar substrates across automotive interiors, medical devices, and flexible packaging, with TPU-based films gaining share. Acrylic bonding films support display assemblies and architectural glazing through optical clarity and UV resistance, closely tracking consumer electronics cycles. Polyimide bonding films serve high-temperature specialty needs above 250°C in flexible printed circuits and defense electronics, constrained by high cost. Cyanoacrylate and polyester films remain smaller-volume solutions for rapid assembly and general-purpose lamination, delivering cost efficiency in mature applications.

Market Share by Application: Electronics Dominate as EVs and Medical Devices Accelerate Adoption

Electrical and electronics account for 36% of bonding film demand in 2025, driven by flexible PCB lamination, EMI shielding attachment, display bonding, and camera module assembly, reinforced by device miniaturization, foldable form factors, and 5G transparency requirements. Automotive follows as the second-largest segment, replacing mechanical fasteners with bonding films for interior trim, headlamp modules, battery pack insulation, and CFRP-aluminum hybrids, supported by EV safety and lightweighting initiatives. Aerospace remains a high-value segment using epoxy and polyimide films in fuselage composites and honeycomb panels, with long qualification cycles balanced by program longevity. Packaging leverages polyurethane and polyester films in retort pouches and sterile laminates, while medical applications are expanding rapidly through biocompatible acrylic and polyurethane films in wound care, wearables, and surgical assemblies, supported by aging populations and home healthcare adoption.

Competitive Landscape Analysis of the Bonding Films Market

The global bonding films market in 2026 is being driven by rapid advances in EV battery assembly, aerospace composites, semiconductor packaging, AR/VR displays, and smart construction materials. Competition is intensifying around structural bonding films, electrically conductive adhesive films (ECFs), anisotropic conductive films (ACF), and thermal management laminates, with sustainability, digital simulation, and miniaturization emerging as key differentiators. Leading manufacturers are shifting from standalone adhesive products to system-level bonding solutions, integrating AI-driven materials design, carbon footprint transparency, and application-specific engineering. This has positioned bonding films as mission-critical enablers across electric mobility, 5G/6G electronics, advanced air mobility, and next-generation medical devices.

AI-driven bonding films from 3M Company power next-gen electronics and mobility

3M enters 2026 in a major R&D reinvigoration phase, leveraging AI to compress bonding film development cycles. At CES 2026, the company unveiled an AI-powered materials simulation platform that enables virtual testing of bonding films in extreme environments, including high-heat data centers, before physical prototyping. Its portfolio of structural bonding films and electrically conductive adhesive films (ECFs) is now essential for miniaturized sensors and 5G/6G communication modules. Strategically focused on “virtual materials” and digital-first manufacturing, 3M integrates ceramics, nanotechnology, and nonwovens to create metamaterial films that support lighter EVs, sharper displays, and improved recyclability in consumer electronics.

Sustainable EV battery bonding leadership from Henkel AG & Co. KGaA

Henkel dominates sustainability-driven bonding films in 2026, emphasizing transparent carbon accounting and bio-based chemistry. The late-2025 expansion of its Brandon, South Dakota facility doubled capacity for LOCTITE® and BERGQUIST® thermal management and adhesive films, strengthening its North American EV supply chain. In February 2026, Henkel partnered with Sekab to integrate bio-based ethyl acetate into industrial film production, reducing fossil dependency. Through its HEART platform, customers now receive audited cradle-to-gate and use-phase carbon data per batch. Henkel remains a market leader in EV battery and electronics bonding, delivering films that combine structural integrity with advanced heat dissipation.

Aerospace-grade structural bonding innovation from Solvay

Solvay continues to set aerospace benchmarks with its FM® structural bonding film series and FusePly™ platforms. In 2026, FusePly™ 250 and 350 gained traction by forming covalent bonds directly within composite structures, eliminating labor-intensive surface preparation such as sanding or peel-ply removal. FM® grades remain the global standard for metal-to-metal and metal-to-composite bonding in aircraft exposed to extreme vibration and thermal cycling. Strategically targeting Advanced Air Mobility (eVTOL), Solvay supplies lightweight, high-reliability bonding films for composite airframes. Its unmatched aerospace qualification base creates a formidable barrier to entry across defense and commercial aviation.

System-based construction bonding from H.B. Fuller Company

H.B. Fuller differentiates itself through agile customization and a “system thinking” approach to bonding films. In 2026, the company is transitioning from standalone adhesive products to complete bonding systems for commercial roofing, façades, and insulating glass, where films function as part of multi-layer assemblies. Recent launches include plasticizer-resistant adhesives that prevent failure in luxury vinyl tile installations. Expanded Global Technical Centers of Excellence now provide localized processing simulation for construction clients. H.B. Fuller’s engineering adhesive films bridge the gap between liquid glues and tapes, delivering structural epoxy strength with film-level precision for modern building envelopes.

High-barrier medical and water-filtration films from DuPont

Following the late-2025 spin-off of its electronics unit into Qnity Electronics, DuPont refocused its bonding film assets within Water & Protection. In 2026, DuPont films play a critical role in medical packaging and industrial water purification, providing sterile, high-barrier seals for pharmaceuticals and medical devices. The company maintains aggressive cost-productivity and share buyback programs, targeting a 90% free cash flow conversion rate through a streamlined manufacturing footprint. DuPont’s core strength lies in structural resilience, producing bonding films that withstand high pressure and chemically aggressive environments, particularly in reverse osmosis filtration modules and life-science applications.

Ultra-thin display bonding leadership from Dexerials Corporation

Dexerials is the precision specialist for display and optics bonding in 2026, supplying anisotropic conductive films (ACF) and Optical Elastic Resin for smartphones, foldables, and micro-LED platforms. The company is the primary provider of ultra-thin ACFs that connect micro-LED displays to drive circuits, while its new smart bonding films deliver optical clarity for AR/VR headsets without altering lens refractive indices. Strategically shifting toward automotive cockpit evolution, Dexerials supports large curved displays with vibration-resistant, wide-temperature films. Its micron-level thickness control underpins next-generation wearables and compact medical devices, reinforcing its leadership in advanced miniaturization.

Japan Bonding Films Market: Semiconductor-Centric Bonding Films Anchoring 6G, EV, and Solid-State Battery Roadmaps

Japan’s bonding films industry is being structurally driven by advanced semiconductor packaging, optical electronics, and next-generation energy storage, with domestic materials science leaders setting global benchmarks. In June 2025, OKI and NTT Innovative Devices announced a major breakthrough in mass production of high-power terahertz devices using Crystal Film Bonding technology. This adhesive-free approach achieves near-100% yield and directly targets emerging 6G communication infrastructure, positioning bonding films as a core enabler of heterogeneous material integration. Parallel innovation is occurring in wafer-level processes. In November 2025, Toray Industries introduced a specialized temporary bonding film that enables wafer thinning to 30 micrometers or below, a critical requirement for high-bandwidth memory stacks used in AI accelerators and advanced logic chips.

Regulatory and sustainability pressures are reinforcing material innovation. Japanese suppliers commercialized PFAS-free mold release and bonding films during 2024–2025, responding to global health regulations while also reducing contamination risks in leading-edge fabs. Optical bonding is another high-growth pillar, with Toray’s March 2025 launch of a nano-multilayer HUD bonding film that eliminates double imaging for polarized sunglasses, addressing a persistent limitation in automotive cockpit displays. Beyond electronics, government-funded research through the Japan Science and Technology Agency in late 2025 is accelerating the use of ion-conductive bonding films to enhance thermal stability in solid-state lithium–sulfur batteries. Capacity investments underpin these advances, with Toray expanding Lumirror™ release film production to support MLCC manufacturing growth driven by electric vehicle electrification.

United States Bonding Films Market: PFAS Phase-Out and Aerospace Lightweighting Redefining Performance Benchmarks

The U.S. bonding films market is undergoing a fundamental reset driven by PFAS elimination commitments, aerospace lightweighting, and medical-grade adhesive expansion. 3M remains central to this transition, with its public commitment to exit all PFAS manufacturing by the end of 2026. By July 2025, the company had already launched 126 new products, many of them PFAS-free bonding films and industrial adhesive alternatives, signaling a decisive shift toward compliant chemistries without sacrificing performance. Aerospace remains a premium demand center. In 2025, 3M Aerospace introduced the Scotch-Weld™ EC-9370 epoxy adhesive film, delivering a density below 0.7 g/cm³ and enabling weight reductions exceeding 50 kg per wide-body aircraft through honeycomb interior applications.

Supply chain and policy considerations are also reshaping formulation strategies. Following trade de-escalation in May 2025, U.S. manufacturers prioritized tariff-exempt raw material chemistries to stabilize industrial adhesive supply chains. Medical bonding represents another structurally attractive segment. In October 2025, H.B. Fuller appointed dedicated leadership to scale its MedTech bonding film portfolio, reflecting rising demand for biocompatible and sterilization-resistant materials. Sustainability-led packaging innovation further broadens the market. Henkel, through its U.S. and global operations, launched Loctite Liofol LA 7837 in July 2025, a solvent-free retort bonding system that eliminates energy-intensive drying and materially lowers emissions in food packaging applications.

India Bonding Films Market: Electronics PLI and Semiconductor Packaging Creating Structural Demand Pull

India’s bonding films industry is transitioning from import dependence toward localized production, driven by aggressive electronics manufacturing incentives and semiconductor ecosystem build-out. In May 2025, the Indian government approved a ₹22,919 crore Production-Linked Incentive scheme for electronic components, explicitly targeting advanced PCB fabrication, display modules, and sub-assemblies where bonding films are mission-critical for structural integrity and thermal management. By March 2025, cumulative realized investments in the electronics sector reached ₹1.76 lakh crore, with Gujarat emerging as a focal point for semiconductor packaging and display fabs, creating sustained demand for high-purity bonding agents.

The downstream impact is already visible. India became a net exporter of electronic components in FY 2024–25, while domestic production of metallized films used in capacitors and LED chip packaging surged 146% compared to 2021 levels. The revised PLI framework actively encourages joint ventures with foreign technology leaders, accelerating the transfer of substrate bonding, die-attach, and semiconductor packaging expertise into Indian chemical and electronics hubs. This combination of scale, policy certainty, and JV-enabled technology access is positioning India as a long-term growth market for advanced bonding films rather than a commodity adhesive consumer.

Germany and the European Union Bonding Films Market: Regulation-Driven Innovation and Circular Packaging Focus

In Europe, the bonding films landscape is being shaped by regulatory compliance and circular economy mandates rather than volume expansion. In August 2025, Henkel introduced a new generation of phthalate-free PVC-based sealants and bonding compounds under the Darex COV range, pre-emptively aligning with tightening REACH rules on endocrine disruptors. This shift is accelerating material substitution across construction, automotive interiors, and industrial sealing applications.

Packaging remains a priority innovation domain. Henkel’s solvent-free aliphatic adhesive systems launched in July 2025 allow European manufacturers to reduce material consumption and carbon intensity while maintaining retort and food-contact performance. Public funding is reinforcing longer-term technology pipelines. In December 2025, joint green-technology funding initiatives involving European agencies and Asian partners, including the Japan Science and Technology Agency, were established to advance bonding solutions for alternative energy systems, signaling cross-border collaboration in high-performance, low-impact adhesive technologies.

China Bonding Films Market: Consumer Electronics Scale Driving Thermally Robust Bonding Films

China continues to dominate global demand for bonding films through its scale in consumer electronics and display manufacturing. In July 2025, 3M reported that China led its global growth in industrial adhesives and electronics bonding films, underscoring the country’s central role in smartphones, wearables, and connected devices. Chinese manufacturers are increasingly specifying thermally cured bonding films over pressure-cured variants, reflecting the need for higher heat and chemical resistance in compact, high-performance smart devices.

The country’s display and photonics ecosystem further reinforces this trend. At SEMICON Taiwan 2025, Chinese suppliers showcased strong participation in panel-level packaging and hybrid bonding materials for photonic integrated circuits, highlighting rapid progress in mass-transfer and advanced display assembly technologies. This positions China as both the largest volume market and a fast-evolving innovation center for next-generation bonding films.

Comparative Snapshot: Bonding Films Industry by Country

Bonding Films Market County Level Snapshot

|

Country / Region

|

Primary Demand Driver

|

Structural Industry Shift

|

|

Japan

|

Semiconductors, 6G, EV electronics

|

Ultra-thin, PFAS-free, high-precision bonding films

|

|

United States

|

PFAS phase-out, aerospace, medical

|

Lightweight, compliant, high-performance adhesive films

|

|

India

|

Electronics PLI, semiconductor packaging

|

Localization and JV-led technology transfer

|

|

Germany / EU

|

REACH, circular packaging

|

Phthalate-free and solvent-free bonding systems

|

|

China

|

Consumer electronics and displays

|

Thermally cured films for high-density devices

|

Bonding Films Market Report Scope

Bonding Films Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.6 Billion

|

|

Market Size (2034)

|

$5.7 Billion

|

|

Market Growth Rate

|

9.1%

|

|

Segments

|

By Type (Epoxy Bonding Films, Polyurethane Bonding Films, Acrylic Bonding Films, Polyimide Bonding Films, Cyanoacrylate and Polyester Films), By Technology (Thermally Cured, Pressure Sensitive, UV Cured), By Substrate Compatibility (Metal to Metal, Composite to Composite, Heterogeneous Bonding), By Application (Aerospace, Electrical and Electronics, Automotive, Medical, Packaging), By Feature (PFAS Free and Solvent Free, Optical Clarity, Conductive and Insulating)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M, Henkel, Toray Industries, H B Fuller, Hexcel, Arkema, Sika, Solvay, DuPont, Mitsubishi Chemical Group, Nitto Denko, Gurit, Master Bond, Avery Dennison, Rogers Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Bonding Films Market Segmentation

By Type

- Epoxy Bonding Films

- Polyurethane Bonding Films

- Acrylic Bonding Films

- Polyimide Bonding Films

- Cyanoacrylate and Polyester Films

By Technology

- Thermally Cured

- Pressure Sensitive

- UV Cured

By Substrate Compatibility

- Metal to Metal

- Composite to Composite

- Heterogeneous Bonding

By Application

- Aerospace

- Electrical and Electronics

- Automotive

- Medical

- Packaging

By Feature

- PFAS Free and Solvent Free

- Optical Clarity

- Conductive and Insulating

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Bonding Films Industry

- 3M

- Henkel

- Toray Industries

- H B Fuller

- Hexcel

- Arkema

- Sika

- Solvay

- DuPont

- Mitsubishi Chemical Group

- Nitto Denko

- Gurit

- Master Bond

- Avery Dennison

- Rogers Corporation

*- List not Exhaustive